Collagen Protein Makes a Strong Comeback: Is the Aesthetic Medicine Upstream Facing a Material Shift?

On June 7, Jinbo Bio’s listing application materials for the Beijing Stock Exchange were accepted, once again putting collagen in the spotlight.

It is reported that Jinbo Bio will allocate a total of RMB 602 million in raised funds, of which RMB 232 million will be invested in the research and development project for new recombinant humanized collagen materials and injectable products. Notably, Jinbo Bio’s product portfolio primarily consists of recombinant collagen products and anti-HPV biological protein products. Moreover, the revenue contribution from recombinant collagen products increased from 44.21% in 2019 to 69.81% in 2021.

Based on the use of funds from this capital raise and ongoing R&D projects, it is foreseeable that Jinbo Bio will continue to increase its investment in the recombinant collagen market.

And if animal-derived collagen is also included in the discussion,The first half of 2022 was undoubtedly the highlight moment for the collagen market.

First, Bloomage Biotech announced its acquisition of a 51% stake in Yierkang, a collagen company, marking its formal entry into the collagen industry. Subsequently, Giant Biogene submitted its prospectus for an IPO on the Hong Kong Stock Exchange, sparking intense industry discussion about collagen and dressings. Now, with Jinbo Bio’s IPO application on the Beijing Stock Exchange being accepted, the industry is filled with boundless speculation about the future development of collagen.

andAmidst much speculation, the comparison between collagen and hyaluronic acid has been frequently mentioned. Questions such as “Can collagen become the next hyaluronic acid?” and “Will collagen become the next ‘dominant’ biomaterial in the field of medical aesthetics?” have occupied the center of public opinion.

The primary reason lies in the partial overlap of their application scenarios. Ironically, collagen-based medical aesthetic products received regulatory approval more than two decades earlier than hyaluronic acid products. Why did collagen, despite being the first to gain approval in the medical aesthetics sector, lag significantly behind hyaluronic acid in commercialization? And why did it experience a surge in 2019? As collagen gains momentum, can it grow to match the market size of hyaluronic acid and single-handedly sustain several publicly listed companies? Among injectable fillers, medical dressings, and functional skincare, which sub-sector holds the greatest growth potential for collagen?

Armed with numerous questions, VCBeat interviewed multiple industry practitioners to recount the development history, current challenges, and future trends of collagen from the perspectives of capital and enterprises.

Before discussing how collagen lags behind hyaluronic acid in terms of commercialization, let us clarify one point: the scope of this discussion is limited to the medical aesthetics industry. This is because medical aesthetics represents only one of the application areas for both collagen and hyaluronic acid.

The triple-helix structure of collagen endows it with properties such as stimulating cell regeneration, repairing damaged skin barriers, and promoting coagulation; meanwhile, the viscous polysaccharide structure of hyaluronic acid provides excellent hydrating and moisturizing effects (cross-linked hyaluronic acid can be used for contouring). Consequently, both substances are widely applied in the medical, medical aesthetics, and food industries.

Major Applications of Collagen

Source: Guohai Securities, “Collagen: The ‘Soft Gold’ of Skin—Industry Dividends and Competitive Landscape”

For instance, in the medical field, collagen can be used as a hemostatic material and drug carrier, while hyaluronic acid is also applied in orthopedics, ophthalmology, and other specialties; in the food sector, collagen serves as a functional food and food additive, and hyaluronic acid can be incorporated into health supplements, foods, and beverages.

Although the overall application scopes of the two are similar, their levels of adoption and developmental progress across various sectors differ. For instance, collagen is currently 80% applied in the healthcare and food & beverage industries.

However,In the field of medical aesthetics, collagen products received regulatory approval more than 20 years earlier than hyaluronic acid.

In 1981, the approval of Zyderm, the world’s first bovine collagen implant, officially ushered in the application of collagen in the field of medical aesthetics.

Subsequently, as more products gained approval, collagen accounted for approximately 90% of the soft tissue filler market around the year 2000. While becoming the mainstream injectable filler material, it also embarked on a commercialization trajectory that would ultimately see it surpassed by hyaluronic acid.

According to ASPS data, hyaluronic acid-based medical aesthetic products experienced rapid growth after their official market launch in 2004, capturing 63.16% of the soft tissue filler market share in 2006 and gradually increasing to 76.81% by 2020.

As market share was squeezed, some collagen-based medical aesthetic products also reached the end of their lifecycle. For example, Johnson & Johnson’s Evolence was discontinued within a year of its launch, and Allergan withdrew its collagen product line in 2011.

The slow commercialization of collagen-based medical aesthetic products was primarily due to the relatively low cost-effectiveness and higher biosafety risks associated with collagen at that time.

It is reported that collagen sources at the time were primarily animal-derived, carrying a high risk of allergenicity. Surveys indicate that approximately 3% of the population is sensitive to bovine collagen. Relevant reports have stated that among patients treated with bovine collagen products (Zyderm or Zyplast) prior to 1990, about 0.04% developed cysts at the injection site. (Source: Huachuang Securities research report “Collagen’s ‘New’ Life: A Potential Blue Ocean”)

Moreover, at that time, collagen products required two rounds of skin testing prior to injection; even with negative test results, allergic reactions and other more severe adverse effects could not be completely avoided.

Furthermore, early bovine collagen products exhibited suboptimal duration of filler effects, lasting only three months, and were relatively expensive, thus lacking cost-effectiveness.

However, the turning point came in 2019.

“From the perspective of its development history, collagen is like an old tree blossoming anew,” said Dr. Xiao E, Chief Technology Officer and Chairman of Meibo Biopharmaceuticals.。

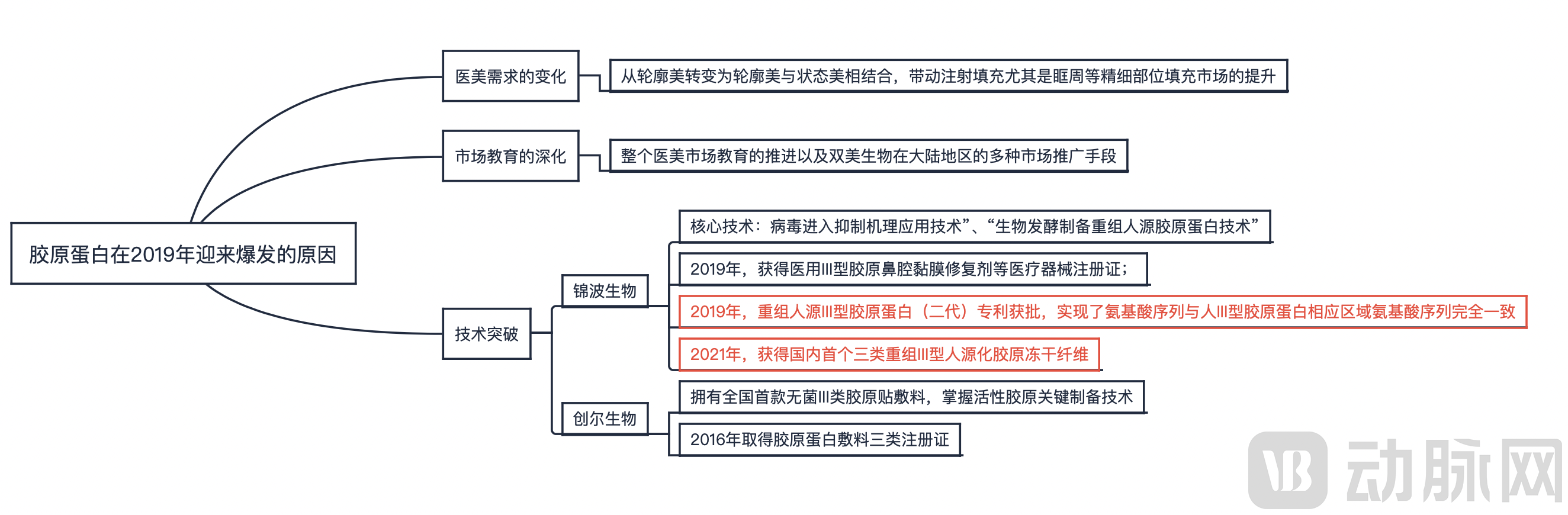

Among these years, 2019 was a particularly notable one. In that year, Bloomage Biotech, the leading enterprise in collagen-based dermal fillers, achieved a doubling of both sales volume and revenue while maintaining stable prices, thereby reversing its previous downturn in the Chinese market.

The surge in performance is merely superficial; the underlying drivers propelling collagen to a new level are primarily changes in aesthetic medicine demand, deepened market education, and breakthroughs in related technologies.

In recent years, with the steady rise in per capita disposable income of residents, the emergence of the “beauty economy,” and years of market education, public acceptance of medical aesthetics has not only increased, but the demand for beauty has also evolved into a combination of facial contour enhancement and overall aesthetic vitality.

Corresponding to the shift in demand is the steady rise in the proportion of non-surgical medical aesthetic procedures. According to iResearch forecasts, non-surgical procedures will account for 48% of the domestic market in 2023. Focusing on the injectable medical aesthetics market, a collagen research report by Zheshang Securities indicates that from 2017 to 2021, the terminal retail market size for injectable medical aesthetics in China reached RMB 42.4 billion, among which collagen-based injectable products accounted for RMB 3.7 billion, representing an 8.7% share. This still lags behind hyaluronic acid and botulinum toxin.

However, even against the backdrop of a relatively small market share, the performance of dual-beauty products has still experienced explosive growth. The primary reason is that, compared with hyaluronic acid and botulinum toxin, the efficacy advantages and regulatory approval advantages of collagen are gradually becoming apparent.

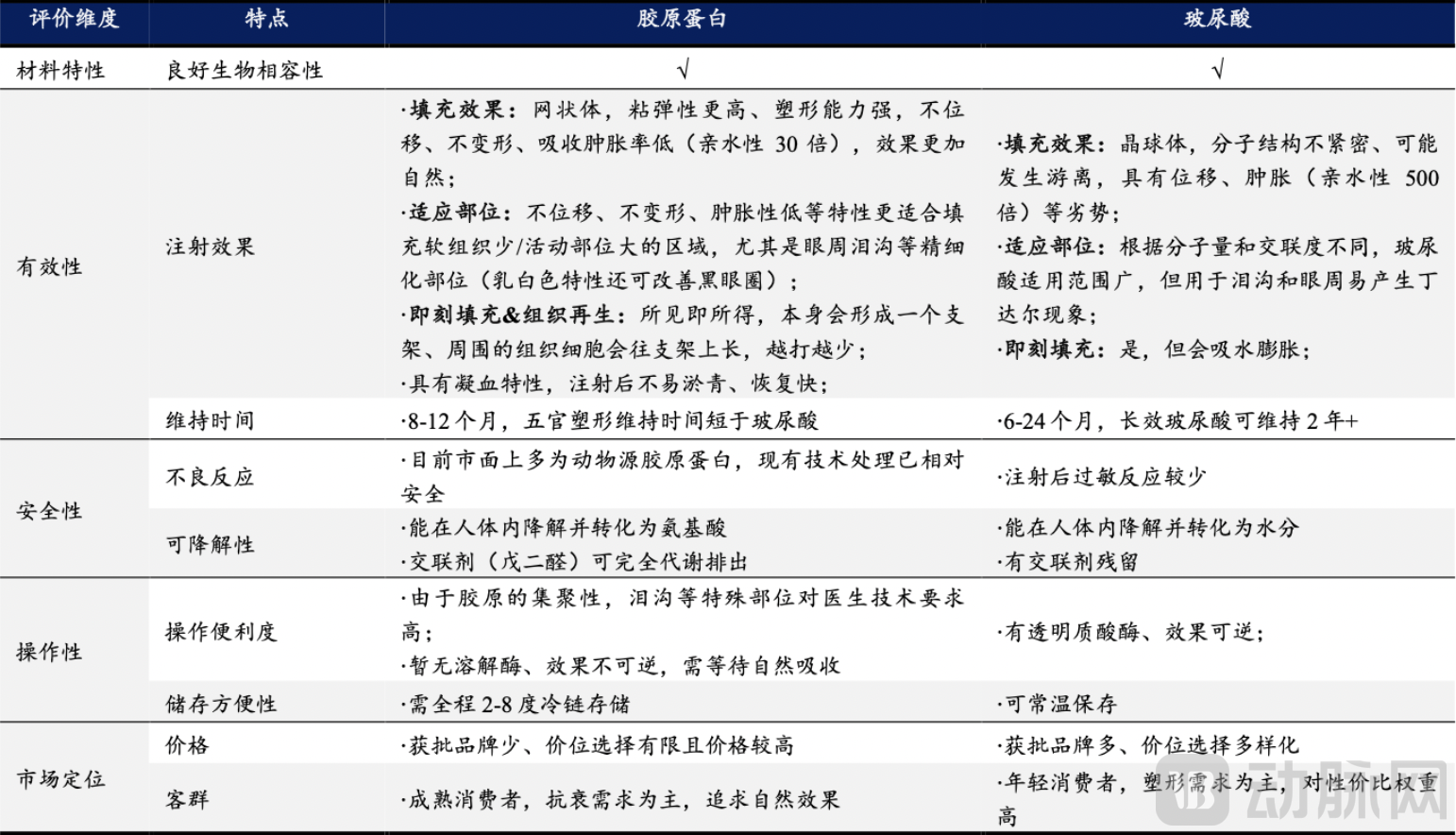

Taking injectable fillers as an example, after injection, the triple-helix structure of collagen works synergistically with elastic fibers to form a mesh-like support structure, providing robust support to the dermis. This enhances skin elasticity and increases tissue volume, thereby achieving immediate filling effects and promoting tissue regeneration, with minimal risk of migration. Hyaluronic acid does not possess this capability.

Furthermore, for delicate areas with minimal soft tissue, such as the tear troughs around the eyes, collagen offers superior filling results due to its characteristics of non-migration, resistance to deformation, and low swelling. In contrast, hyaluronic acid injections in the tear troughs and periocular regions are more prone to causing the Tyndall effect.

Comparison of Injectable Collagen and Hyaluronic Acid

Source: Guohai Securities’ “Collagen: The ‘Soft Gold’ of Skin—Industry Dividends and Competitive Landscape”

andTwo key factors will shape the future development of botulinum toxin: First, China imposes strict regulations and high entry barriers for botulinum toxin products. In the current landscape dominated by four major players, three of the products are either imported or distributed by domestic companies through agency agreements, resulting in a relatively stable competitive structure but limiting corporate growth. Second, botulinum toxin carries a relatively high risk of side effects. Post-injection adverse reactions—particularly after long-term use—may include the so-called “frozen face,” as well as headaches and diplopia; in severe cases, these complications can be life-threatening.

“Public demand for medical aesthetics has evolved beyond mere aesthetic enhancement to include biological functionality, with consumers seeking products that can seamlessly integrate with their own tissues after use. This is where collagen comes into focus,” said Xiao E from Meibo Pharmaceutical.

However, modern society has long moved beyond the era where “good wine needs no bush.” Consequently, collagen, despite its inherent advantages, did not experience a surge in popularity before 2019, and Shuangmei once faced the crisis of withdrawing from the mainland China market.

In the review by Lin Yuting, CEO of Shuangmei Greater China, a severe lack of market transaction awareness was identified as one of the reasons.

From its entry into mainland China in 2009 until 2015, the early-stage dual-beauty sector remained an “invisible” presence within the industry, participating in neither academic forums nor exhibitions, and engaging in no academic marketing activities.

AndSince the beginning of 2018, Shuangmei has prioritized brand promotion by expanding its presence in public hospitals, actively participating in academic conferences, establishing clinical technology training bases in major cities, placing advertisements in professional journals, and publishing academic articles. These initiatives have enhanced brand visibility, deepened public awareness of collagen, and contributed to the surge in performance in the mainland China market in 2019.

Interestingly, almost at the same time, other domestic companies also achieved breakthroughs.

Since 2019, Giant Biogene has been the largest professional collagen-based skincare company in China for three consecutive years in terms of retail sales, a achievement driven by its increased production capacity.

VCBeat has learned that in 2019, Giant Biogene’s Phase II factory, with a construction area of approximately 30,000 square meters, commenced production, further expanding its production capacity. Production capacity is crucial to the collagen industry, as will be elaborated in the next section of this article.

Meanwhile, during roughly the same period, Jinbo Bio, another representative domestic enterprise in the collagen sector, also embarked on the path of industrialization following its technological breakthroughs.

It is reported that the industrialization of Jinbo Bio’s main products (recombinant collagen products and anti-HPV biological protein products) relies on breakthroughs in its two core technologies: “Application Technology for Virus Entry Inhibition Mechanism” and “Biological Fermentation Technology for Preparing Recombinant Humanized Collagen.”

Although Trauer Bio obtained the registration certificate for China’s first Class II medical device collagen dressing in 2004, its approval of China’s first sterile Class III medical device registration certificate for collagen dressings in 2016 undoubtedly elevated its business development to new heights and established significant technical barriers.

The collagen boom that erupted in 2019 has persisted to the present day, and even reached a “mini-peak” at the moment when Giant Biogene submitted its prospectus and Jinbo Bio’s listing application materials were accepted.

So, can collagen, which is highly anticipated by various parties, grow into the next hyaluronic acid?

“Objectively speaking, collagen cannot yet match the market volume of hyaluronic acid in the short term.” In the interview,MingFengDr. Wang Zhen, Partner at MingFeng Capital, stated.

ButIn a discussion with Xiao E of Meibo Pharma, he expressed a relatively optimistic view to VCBeat: “Collagen is indeed highly likely to become the next hyaluronic acid, and this transition will not take long—perhaps as little as three years, or at most five.”

Despite differing views on the potential future market size of collagen,Across various analyses, three key factors are consistently highlighted: cost, production capacity, and technology. These three elements are intrinsically interconnected and closely interrelated.

In terms of production costs, according to Huachuang Securities’ report “Collagen’s ‘New’ Life: A Potential Blue Ocean,” the sales price of Bloomage Biotechnology’s injection-grade hyaluronic acid raw material was RMB 113,800/kg in 2018. Based on gross margin back-calculation, the production cost of injection-grade hyaluronic acid raw material was approximately RMB 10,200/kg.

In 2020, Shuangmei’s cost for injectable collagen remained at RMB 2 million per kilogram. (Note: This figure was estimated by Huachuang Securities and may vary due to factors such as other components in the injection and costs associated with the manufacturing process.) This amount is even significantly higher than the production cost of hyaluronic acid in the 1970s (USD 100,000 per kilogram).

“Through years of technological iteration, Bloomage Biotech has reduced the cost of hyaluronic acid to its minimum. As a relatively new technology, recombinant humanized collagen still carries a comparatively high technical cost, leaving room for further reduction.”MingFengWang Zhen of MingFeng Capital stated that this is akin to the difference between “luxury cars” and “ordinary family cars.” If judged solely by sales volume, the market potential for ordinary family cars may be more significantly influenced by price factors.

In addition to high costs, collagen production lags far behind that of hyaluronic acid.

According to Frost & Sullivan data, global sales volume of hyaluronic acid raw materials reached approximately 500 metric tons in 2018, with Bloomage Biotechnology producing around 180 metric tons, accounting for 26% of the global market share; as of June 2021, Bloomage Biotechnology’s production capacity for hyaluronic acid had reached 420 metric tons.

In contrast, according to the aforementioned report by Huachuang Securities, Shuangmei Collagen has a production capacity of 1.8 tons, with an annual output of 160,000 collagen implant injections, while Changchun Botai produces approximately 100,000 collagen filler units per year. Compared with hyaluronic acid, there remains a significant gap in collagen production capacity.

Production capacity is constrained primarily by technical factors.

VCBeat has learned that as early as 2000, Bloomage Biotech achieved large-scale mass production of hyaluronic acid using fermentation technology.Currently, collagen production still relies primarily on animal extraction methods, which face limitations related to livestock management. Recombinant protein systems using Escherichia coli or Pichia pastoris encounter challenges such as difficulties in controlling extraneous enzymatic reactions. Achieving high expression levels requires simultaneous optimization of multiple parameters, including high purity, low endotoxin levels, and low antigenicity.

However, in recent years, perhaps driven by increasingly fierce competition, some domestic companies have begun to seek breakthroughs by increasing R&D investment, ultimately achieving technological breakthroughs.

For example,Giant Biogene has developed and applied high-density fermentation and high-efficiency separation and purification technologies, enabling a 90% recovery rate of target proteins from recombinant Escherichia coli after a single processing cycle, while achieving a purity level of up to 99.9% for recombinant collagen.

Jinbo Bio’s applied technologies for viral entry inhibition mechanisms and biofermentation-based production of recombinant humanized collagen have also made it the first company globally to achieve commercialization of novel humanized collagen materials and anti-HPV anhydride-modified bovine β-A company specializing in the industrialization of lactoglobulin.

Based on technological breakthroughs,Xiao E of Meibo Pharma told VCBeat, “The development of biotechnology is similar to that of semiconductor technology, generally exhibiting exponential growth. A single technological innovation can lead to a dozens-fold increase in production volume. Therefore, within three to five years, the production cost of collagen, especially recombinant collagen, will drop significantly, while production capacity will see a substantial increase.”

However, in Wang Zhen’s view, even though leading domestic collagen companies have achieved considerable technological breakthroughs, there remains significant room for further advancement in the future.

For instance, in terms of filling efficacy, hyaluronic acid and collagen are prone to degradation after injection into the body. Therefore, to enhance stability and prolong the time required for absorption and metabolism, the industry commonly employs cross-linking technology.

Cross-linking technology for hyaluronic acid is already relatively mature and widely applied, whereas cross-linked collagen injectables face challenges such as storage instability, poor cross-linking efficiency, disruption of the triple-helix structure, and high costs. Consequently, in terms of cross-linking technology, the process maturity of collagen still lags behind that of hyaluronic acid.

“The technological maturity of hyaluronic acid is already very high, leaving little room for improvement. The main future trends lie in combination formulations and expanded indications. In contrast, collagen still has significant potential for technological advancement. Moreover, the state is placing increasing emphasis on the development of collagen, particularly recombinant collagen. For instance, the recently issued notice on the establishment of the industry standard for ‘Recombinant Humanized Collagen Medical Devices’ explicitly encourages the research, development, and high-quality growth of novel biomaterials based on recombinant humanized collagen. This also signals to investment institutions that the industry is in a phase of rapid ascent. This is precisely why MingFeng Capital is actively positioning itself in the collagen sector,” stated Wang Zhen.

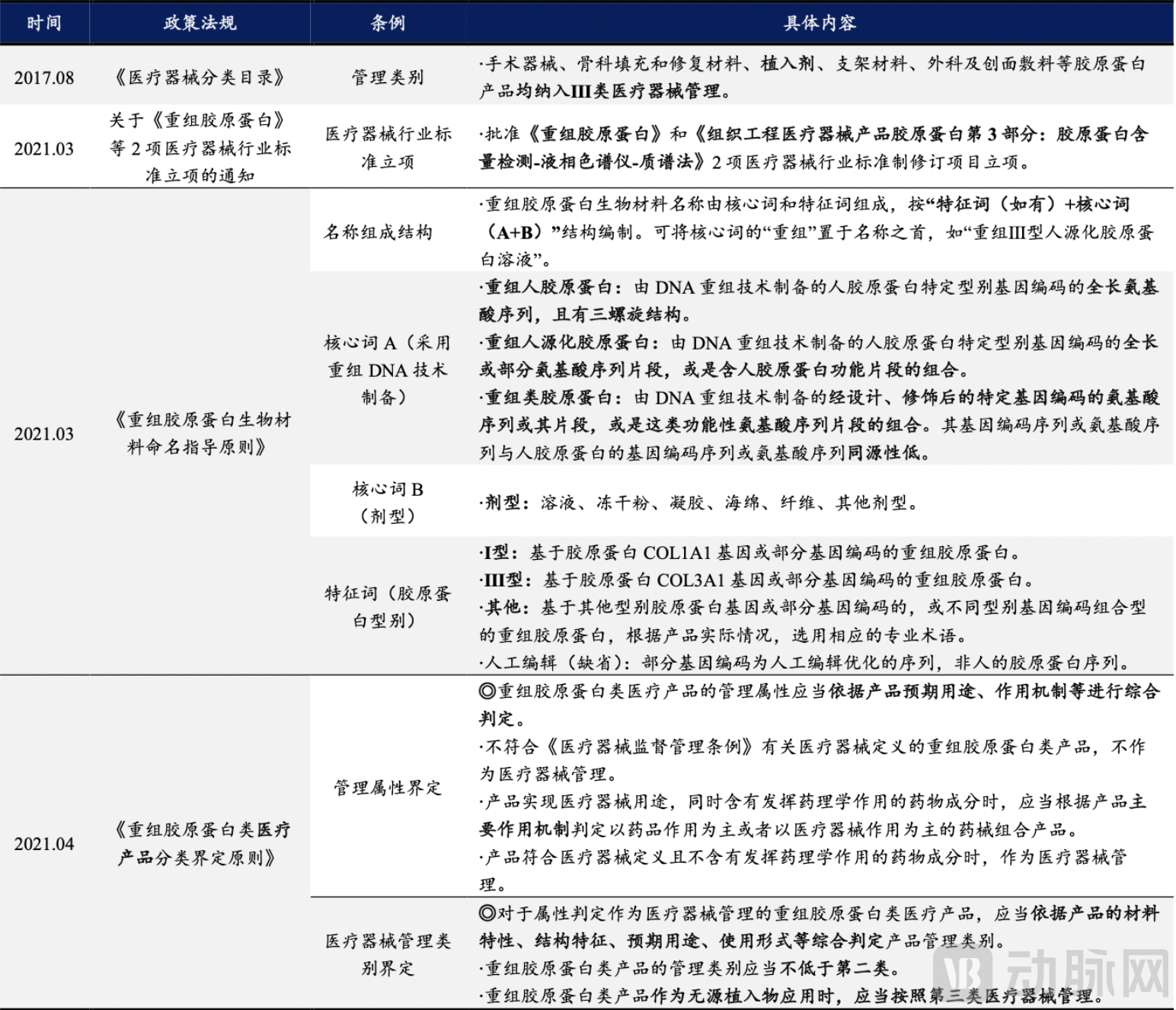

It is reported that China has relatively clear regulations on animal-derived collagen medical device products. In 2017, collagen products such as surgical instruments, orthopedic filling and repair materials, implants, stent materials, surgical and wound dressings were included in the management of Class III medical devices.

Source: Guohai Securities’ “Collagen: The ‘Soft Gold’ of Skin—Industry Dividends and Competitive Landscape”

Since 2021, a series of policies related to recombinant collagen have been successively introduced. For instance, in March 2021, the National Medical Products Administration issued the "Guiding Principles for the Nomenclature of Recombinant Collagen Biomaterials," providing guidance on the naming of recombinant collagen biomaterials in the field of medical devices.

In April of the same year, the "Principles for Classification and Determination of Recombinant Collagen-Based Medical Products" was released, standardizing the determination of regulatory attributes and classification categories for recombinant collagen-based medical products;

One year later, the project “Recombinant Humanized Collagen” was approved for initiation, encouraging research and innovation in novel biomaterials based on recombinant humanized collagen.

The successive introduction of policies has not only standardized and normalized industry development, but also raised the barriers to entry.

“Fundamentally, the collagen industry is technology-driven and characterized by significant technological barriers. Early entrants hold certain advantages in technological accumulation, brand influence, and sales channels,” said Wang Zhen.

However, this does not mean that there are no more lucrative opportunities in the industry. Overall, the development opportunities for collagen mainly lie in the following aspects.

Source: Recombinant Collagen Offers Superior Long-Term Development Prospects

As previously mentioned, collagen products are categorized into animal-derived collagen and recombinant collagen.

Specifically, from 2017 to 2021, the market size of animal-derived collagen end products was RMB 17.9 billion, accounting for 62%; the retail market size of recombinant collagen end products was RMB 10.8 billion, accounting for 38%.

According to Frost & Sullivan, the retail size of China's collagen market reached RMB 28.8 billion in 2021, with the share of recombinant collagen rising from 16% to 38%. It is projected that in 2023, the market share of recombinant collagen will surpass that of animal-derived collagen for the first time.

What Are the Differences Between Animal-Derived Collagen and Recombinant Collagen? Which Is Superior?

It is reported that animal-derived collagen mainly refers to collagen extracted from mammalian tissues through methods such as hot water extraction, acid extraction, and enzymatic extraction, among which the primary industrialized preparation methods are acid extraction and enzymatic extraction;

Recombinant collagen is produced via chemical synthesis or genetic engineering. However, due to limitations in cost, scalability, and the safety of synthetic reagents, chemical synthesis has not achieved industrial-scale translation. Consequently, the primary production method is genetic engineering based on fermentation technology for the expression and manufacturing of recombinant human-derived collagen.

In fact, both animal-derived collagen and recombinant collagen have their respective advantages and disadvantages.

For example,Animal-derived collagen extracted via either acid or alkaline methods retains an intact triple-helix structure, thereby preserving its functional integrity while offering lower costs. However, animal-derived collagen may pose risks related to immunogenicity and safety.

However, recombinant collagen can minimize immunogenicity and control the risk of pathogenic virus transmission through sequence design, thereby exhibiting favorable biocompatibility and safety. Objectively speaking, there is still room for further improvement in the biological activity and supportive effects of recombinant collagen to achieve “perfection.”

However, it is precisely due to the favorable biosafety profile of recombinant collagen that it offers greater long-term development potential compared to animal-derived collagen. Looking ahead, the core challenges that recombinant collagen companies must address remain technological and cost-related issues.

Aesthetic Medicine: The Class III Injectable Market Is Small but Has a More Favorable Competitive Landscape

From a data perspective, functional skincare products and medical dressings account for the vast majority of the market share within the collagen product subcategories.

According to Giant Biogene's prospectus, among the market sales of various collagen sub-segment products, functional skincare products and medical dressings ranked in the top two positions, achieving growth rates of 52.8% and 92.2%, respectively, from 2017 to 2021.

The high growth rate in sales of medical dressings is attributed to the increased use of photoelectric devices, microneedles, and skin boosters in recent years. As post-procedure care products for these aesthetic treatments, their sales have grown in tandem with the expanding scale of such minimally invasive aesthetic procedures.

Furthermore, according to Xiao E of Meibai Pharmaceutical, the R&D threshold for collagen-based medical dressings and functional skincare products is lower than that for Class III injectable products.

Therefore,Given current market size and technical barriers, functional skincare products and medical dressings appear more “friendly” to innovative enterprises.

However, according to Giant Biogene’s prospectus, the compound annual growth rate (CAGR) for medical dressings is projected to decline to 28.8% from 2022 to 2027, while that for functional skincare products will see a modest increase to 55%.

As growth slows, the competitive landscape has also become relatively stable.

Although Giant Biogene’s prospectus stated that in China’s medical dressing market in 2021, the top five players accounted for only 26.5% of the market share, “indicating a fragmented competitive landscape in the medical dressing market.”

However, according to a report on collagen by Guohai Securities, as of June 2020, there were a total of 467 approval documents for medical skin repair dressings in China. Class I certificates, primarily for medical cold compress patches, accounted for 90%, while Class II and Class III certificates, mainly for wound dressings, accounted for 9% and 1%, respectively. There are already many approved product types for medical dressings.

In the realm of functional skincare products, data from Biaodian Medicine shows that between July 2019 and June 2020, among the top 100 best-selling repair-type sheet masks on the Taobao Tmall platform, 28 brands each achieved sales exceeding RMB 10 million. Meanwhile, even major cosmetics companies with significant brand influence, such as Kans, Mask Family, and Shiseido, held market shares no higher than 10%.

Therefore,Considering key factors that significantly influence the sales of consumer-oriented products, such as distribution channels and brand influence, there are limited opportunities for startups to grow and scale in the medical dressing and functional skincare sectors.

“Currently, in the medical dressing market, unless startups can develop more innovative products, it is difficult for them to compete with several leading companies. The opportunities left for them may only be limited to peripheral products and contract manufacturing,” Wang Chenchen, an investor at Shaanxi Venture Capital, told VCBeat.

The competitive landscape for Class III collagen-based filler products is relatively more favorable.

Based on approval status, there are currently only four companies operating in the Chinese market: Shuangmei Biotech, Changchun Botai, Hanfu Biotech, and Jinbo Bio. In terms of product type, Jinbo Bio’s Weiyimei is the only collagen product derived from genetic engineering recombination; all others are animal-derived collagen products.

While animal-derived collagen injectable fillers offer higher concentration and superior filling effects, they still pose biosafety concerns. Although recombinant collagen injectable fillers cannot match animal-derived collagen in terms of molecular size, they are significantly superior in biosafety—a consensus currently recognized by the industry.

Therefore, when recombinant collagen achieves technological breakthroughs, attaining molecular weights comparable to those of animal-derived collagen while reducing costs and increasing production capacity, its development in the injectable filler market will undoubtedly surpass that of animal-derived collagen products.

The approval of Jinbo Bio’s Weiyimei has not only injected confidence into the industry but also charted a course for innovative enterprises.

Overall, although collagen fillers fall under the category of Class III medical devices, which are subject to the strictest regulatory oversight, the industry barriers for enterprises become even higher once they surmount the substantial entry thresholds. Furthermore, the current collagen filler market has relatively few participants, with most products being derived from animal sources, thereby presenting significant development opportunities for innovative companies with strong R&D capabilities.

Medical Field: Toward Comprehensive Expression and Toward Specific Fragmented Expression

As stated at the beginning of the first part of this article, the applications of collagen are not limited to the field of medical aesthetics. What trends are emerging for collagen in the broader medical field?

Pharmaceuticals and Regenerative Medicine: According to Xiao E of Meibo Pharmaceutical, these represent the future divergent trends for collagen. The former involves a trend toward specificity in collagen expression, characterized by increasingly shorter expressed fragments; the latter involves a trend toward completeness in collagen expression, characterized by increasingly longer chains.

As the expressed fragments of collagen become progressively shorter, their functions become increasingly specific, thereby steering their development increasingly toward pharmaceutical applications.

In the field of regenerative medicine, the applications of collagen primarily include hemostatic agents and wound dressings, bone repair materials, and tissue engineering scaffolds. “Clinical use has demonstrated that collagen significantly promotes the repair, regeneration, and reconstruction of defective tissues.”

“During normal development, not only are collagen fragments indispensable, but even mutations at specific sites can lead to developmental malformations,” explained Xiao E. “The essence of repair and regeneration lies in recapitulating the process of growth and development, with the distinction that repair is initiated by inflammation.”

Taking skin repair as an example, the entire process involves stages such as bleeding, coagulation, inflammation, granulation tissue formation, and epithelial coverage. Different stages require the functional activities of various collagen fragments. Therefore, a relatively intact collagen structure is necessary during the repair process.

Therefore, in the field of regenerative medicine, achieving complete expression of collagen has always been a goal pursued by practitioners.“Once collagen achieves a technological breakthrough that delivers both the short-term volumizing effects of hyaluronic acid and the long-term regenerative benefits of fat grafting, it will truly dominate the market,” concluded Xiao E at the end of the interview.

References:

1. Prospectus of Giant Biogene;

2. Jinbo Bio's Prospectus;

3. Huachuang Securities: “Collagen’s ‘New’ Life, A Potential Blue Ocean”

4. Guohai Securities: "Collagen: The 'Soft Gold' of Skin, Industry Dividends and Competitive Landscape"

5. China Securities Co., Ltd. “Collagen: Originating from Animal Sources, Recombinant Technology Opens a New Chapter”

6. Sinolink Securities “A Brief Analysis of the Opportunities and Barriers for Recombinant Humanized Collagen”