Cardiovascular Industry Report 2022: Technological Advancement and Diversified Innovation as the Key to Breakthrough

Preface

Since 2020, national volume-based procurement (VBP) programs have been successively launched for coronary stents, occluders, and defibrillators. Meanwhile, pilot procurement schemes at the provincial level or above have been continuously introduced for consumables such as pacemakers, balloons, and electrophysiology devices. The normalization of centralized procurement has undoubtedly exerted a significant impact on the cardiovascular industry. In the face of policy pressures and an increasingly mature market, key questions have garnered widespread attention: How much value remains in the cardiovascular sector? What will its future development trajectory look like? And how should companies within this sector mitigate risks?To clarify how the cardiovascular industry can break through in the future, VCBeat Research surveyed multiple cardiovascular-related companies and, combining its previous research findings, produced this report. The report aims to analyze the cardiovascular industry under the new landscape from three major dimensions: current industry status, industry value, and future trends.

We believe:

1. The cardiovascular market is vast and growing, with rapid technological iteration; the primary market remains optimistic, and the sector’s value persists.

2. Although centralized procurement compresses corporate profits, it does not drive prices below the ex-factory level; by guaranteeing purchase volumes, it eliminates sales expenses, which is conducive to the development of leading enterprises in the medium to long term.

3. Future focus will be on the fields of valvular disease and heart failure management, with tricuspid valves and artificial hearts being the most promising areas.

4. Technological upgrades and diversified innovation are the keys to breaking through the impasse. Innovative technologies worthy of attention include bioresorbable stents, intravascular lithotripsy (IVL) balloon technology, anti-regurgitation TAVR valves, bioresorbable occluders, leadless pacemakers, pulsed field ablation (PFA) systems, ventricular assist devices (VADs), and atrial shunts.

Industry Status:

Under Volume-Based Procurement, the Cardiovascular Industry Has Gradually Matured

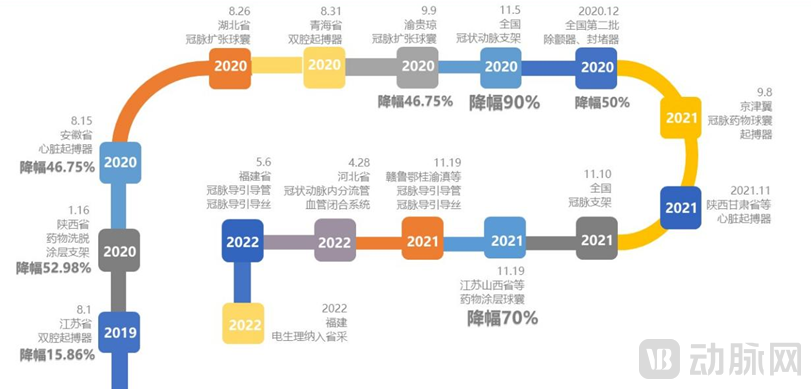

Normalization of Centralized Procurement:Coronary ArteryPioneering Comprehensive Centralized Procurement, with Localized Centralized Procurement Launched in Other Sectors

According toAccording to the centralized procurement information compiled by VCBeat Research Institute, in addition to stents, occluders, and defibrillators, which have already been included in the national centralized procurement list, regional centralized procurement has also been launched for pacemakers, balloons, electrophysiology, and other fields, with average product price reductions ranging from 50% to 90%.Comprehensive Centralized Procurement of Cardiovascular Consumables May Be Implemented in the Future。

Statistics on Centralized Procurement of Cardiovascular Consumables

Source: VCBeat Research Institute, compiled from public information

Accelerated Domestic Substitution: Continuous Technological Breakthroughs and Rising Market Share

Domestic manufacturers have broken the import monopoly in multiple fields, with their market share gradually increasing., especially the coronary branchesIn the stent and balloon industries, the domestic production rate has reached as high as 80% and 40%, respectively. In addition to being driven by centralized procurement policies, more importantly, the technological gap between domestic and international players has gradually narrowed.

The Competitive Landscape Is Becoming Clearer: From a Fragmented Field to the Emergence of Market Leaders

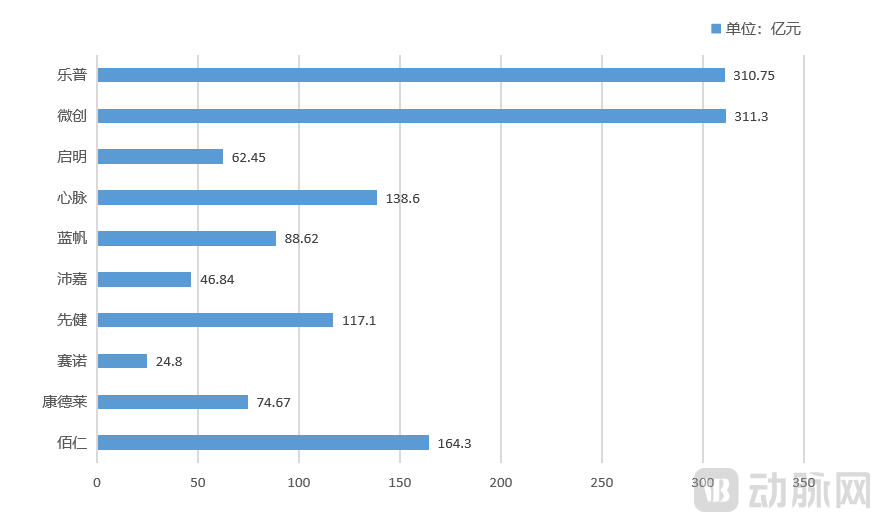

A number of leading enterprises have emerged in China, with the successive IPOs of companies such as Lepu Medical, MicroPort, LifeTech Scientific, and Peijia Medical, there are now more than ten listed companies in the cardiovascular sector. Capital continues to concentrate among leading enterprises, and China’s cardiovascular industry has transitioned from a previously fragmented landscape of numerous competitors to a new competitive paradigm. In terms of listing performance,Lepu Medical and MicroPort’s dominant positions remain unshakable.

Top 10 Listed Cardiovascular Companies in China by Market Capitalization (as of June 10, 2022)

Source: VCBeat, compiled from public data

Industry Value:

Value Remains Intact: Valve Interventions and Heart Failure Management Emerge as Key Highlights for the Future

Value Analysis: High Industry Ceiling, Continued Optimism in the Primary Market

Patient demand for diagnosis and treatment is inelastic and continues to expand,The market is vast.The patient population is large and the mortality rate is high. According to statistics, the number of existing cardiovascular patients in China is as high as 330 million. Meanwhile, changes in national lifestyle, accelerated population aging, and unhealthy daily routines have exacerbated heartThe incidence of vascular diseases and the number of cardiovascular patients are increasing year by year, with a trend toward affecting younger populations. In the future, the market size for high-value cardiovascular consumables is expected to maintain a compound annual growth rate (CAGR) of over 16%, and is projected to exceed RMB 40 billion by 2025.

Clinical demand persists, and technology continues to iterate.From a technical perspective, technologies in fields such as heart valves and heart failure remain immature. In relatively mature areas like coronary interventions and pacemakers, clinical needs are not yet fully met, and products continue to undergo optimization. Taking coronary interventions as an example, calcification remains a prominent challenge, and commonly used rotational atherectomy devices are difficult to operate.High degree, with a utilization rate of less than 1%.

From the capital perspective, the primary market continues to favor the cardiovascular sector.According to incomplete statistics from VCBeat, there were 38 financing events in the cardiovascular industry from 2021 to May 2022, with total funding reaching tens of billions of yuan, indicating that the sector remains highly attractive.

Cardiovascular Primary Market Financing (2021 to May 2022)

Source: VCBeat Research Institute, compiled from public informationLi

Key Focus Areas: Mitral and Tricuspid Valves Show the Most Promise; Long-Term Outlook for Heart Failure Management Remains Positive

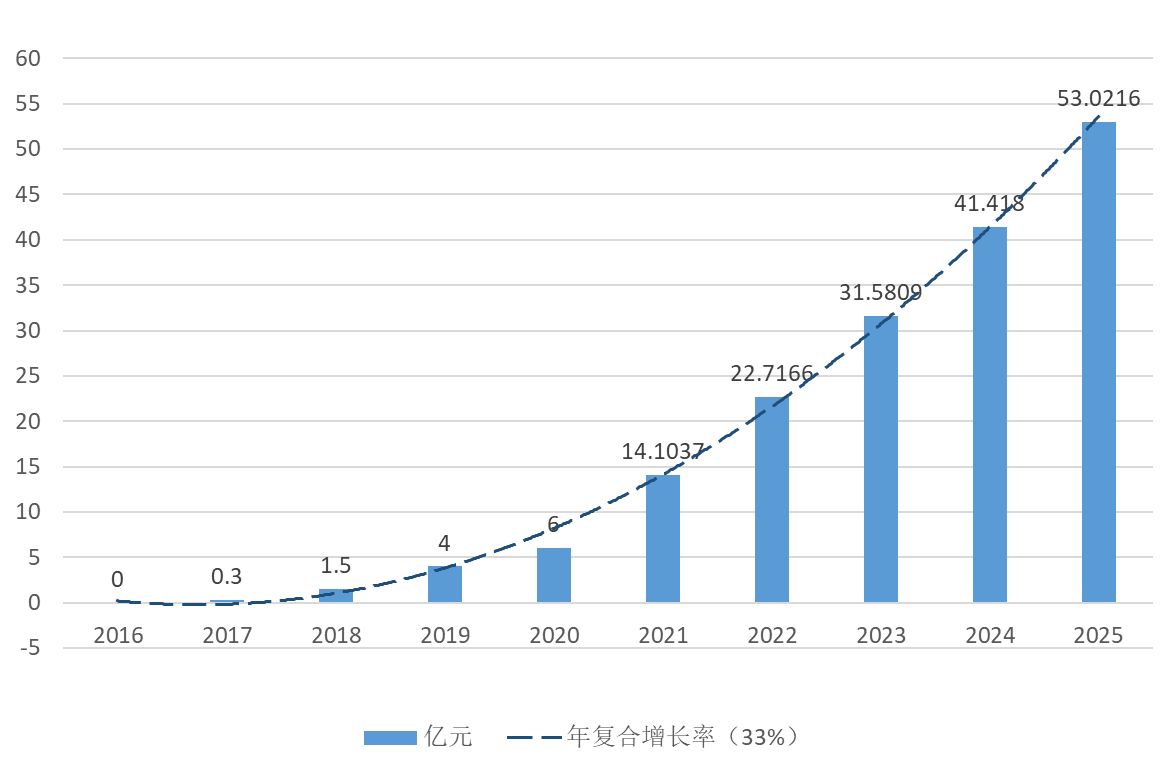

The valve industry demonstrates significant value, with the tricuspid valve sector offering potential for leapfrog development.Valves currently hold a relatively small market share but are experiencing rapid growth. According to data compiled by VCBeat Research Institute, the compound annual growth rate (CAGR) of heart valves in China is as high as 33%, with the market size expected to exceed RMB 5 billion by 2025, indicating substantial potential for incremental growth. Meanwhile, heart valves remain one of the few segments in the cardiovascular industry not yet subject to centralized volume-based procurement (VBP), and it is unlikely that VBP will be implemented in this sector within the short to medium term. For reference, during the implementation of VBP for coronary stents, the annual usage of stents in China exceeded 1.3 million units, with a domestic production rate surpassing 80%.In the field of heart valves, the localization rate is less than 5%, and the technical barriers are extremely high, with existing technological gaps. Premature centralized procurement will lead to severe domestic price competition, significantly undermining enterprises' independent R&D and innovation capabilities.

Market Size of China's Artificial Heart Valve Industry (RMB 100 Million)

Source: VCBeat

In the field of heart valves, the mitral and tricuspid valves warrant greater attention, particularly the tricuspid valve.The aortic valve market is relatively mature, while the patient population for pulmonary valve interventions is small, resulting in a limited market. In contrast, the large number of patients with mitral and tricuspid valve diseases, coupled with high technical barriers, presents a more promising outlook. According to forecasts by VCBeat Research Institute, the market size for mitral valvesAt least five times that of TAVR, the market share for mitral and tricuspid valves is projected to exceed 53% in the future. Additionally, overseas technologies for mitral and tricuspid valve interventions are not yet mature, and product development has progressed relatively slowly. With domestic and international manufacturers essentially starting from the same baseline, Chinese companies still have the potential to surpass their global counterparts.

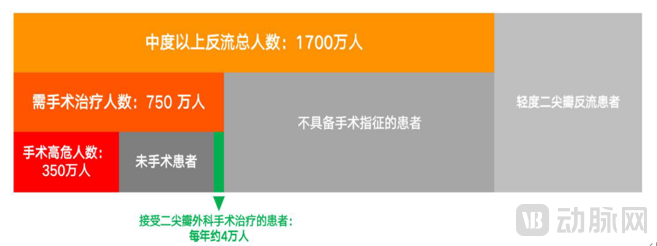

Current Status of Interventions for Mitral Regurgitation

Source: VCBeat, compiled based on relevant literature

Compared with the mitral valve, the tricuspid valve holds greater potential for future development.Mitral valve repair technologies abroad demonstrate significant advantages, whereas domestic technologies in China lag slightly in terms of originality and differentiation. Although the market size for tricuspid valves is slightly smaller than that for mitral valves, the technical barriers are higher. Currently, China has developed proprietary technologies with strong competitiveness. At present, surgical intervention remains the primary treatment for tricuspid valve disease; however, the surgical risk is extremely high, rendering a large number of patients with severe tricuspid regurgitation inoperable due to contraindications. Once transcatheter tricuspid valve intervention technology matures, it will largely replaceSurgery: Significant Room for Growth

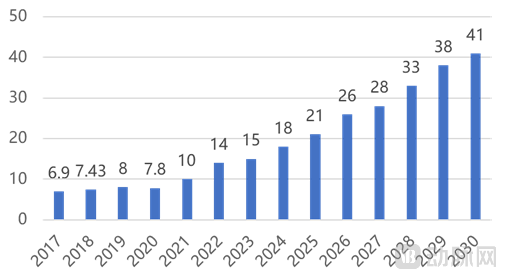

Heart failure management has emerged as another highly noteworthy area in recent years and may soon reach a tipping point.In light of the evolving spectrum of cardiovascular diseases in China, lifestyle changes in recent years have led to a rising prevalence of conditions that readily precipitate heart failure, such as atherosclerosis, diabetes, metabolic syndrome, and obesity. This has resulted in a rapid increase in the number of heart failure patients, ushering in a golden period for heart failure management. Currently, there are approximately 8 to 10 million heart failure patients in China, yet the heart failure management market remains largely untapped with limited solutions available.As market awareness deepens and technology matures, the heart failure management market is poised for explosive growth. According to data compiled and forecasted by VCBeat Institute based on Frost & Sullivan projections, the size of China’s heart failure market will reach RMB 4.1 billion in 2030, calculated at ex-factory prices.

China's Heart Failure Ex-Factory Market Size (Billion Yuan)

Data Source: Frost & Sullivan, compiled by VCBeat.

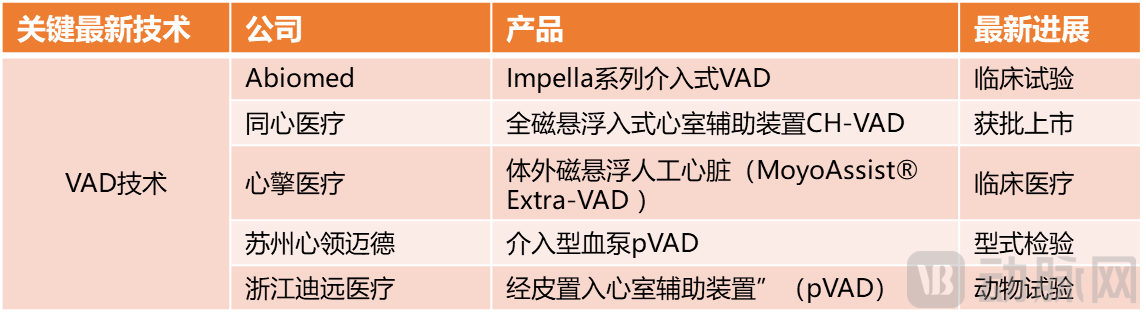

For patients with end-stage heart failure, pharmacological therapy is ineffective, and donor hearts for transplantation are in short supply. As the number of patients with advanced heart failure increases,The value of artificial hearts is becoming increasingly significant, with ventricular assist devices (VADs) being more aligned with clinical applications and offering greater commercial potential.Although China started later in the field of ventricular assist devices (VADs), it began with a high starting point and has achieved rapid progress. The domestically developed, world-leading magnetic levitation technology has provided critical support for the research and development of clinical medical devices. In November 2021, Suzhou Tongxin Medical’s independently developed third-generation fully magnetically levitated artificial heart receivedWith regulatory approval granted, domestic VAD technology now stands on equal footing with the international medical community.

VAD Company and Product Progress

Data source: Compiled by VCBeat Institute based on public information

Future Trends:

Technological Upgrades and Diversified Innovation Are Key to Breaking Through

Industry Trends: Centralized Procurement Reshapes Competitive Dynamics and Industry Landscape, Benefiting Leading Enterprises in the Long Run and Potentially Leading to an Oligopolistic Market Structure

Centralized procurement has reshaped the competitive dynamics and industry landscape of the cardiovascular sector.From a medium- to long-term perspective, volume-based procurement (VBP) benefits industry leaders and innovative enterprises. On one hand, VBP-induced price reductions have not fallen below ex-factory prices, while guaranteeing sales volumes for domestic companies and eliminating marketing expenses, which fosters the formation and growth of leading enterprises in the long run. On the other hand, it stimulates corporate innovation and accelerates product development, thereby driving industry advancement over time. VBP has made cost control, product pipelines, and innovation capability the core competencies of enterprises, compelling players in the sector to seek new pathways. Companies with a single-product portfolio and limited capital strengthPoorly performing enterprises will be eliminated, and the industry will evolve into an oligopolistic landscape in the future.

The two primary strategies adopted by companies in this sector to cope with the pressure of centralized procurement are: 1.Upgraded Product. The likelihood of innovative products being included in centralized volume-based procurement is low; optimizing products and raising prices based on quality can effectively balance performance risks. 2.Product Global Expansion. Leading enterprises have successively expanded into overseas markets. MicroPort and Lepu Medical both generate overseas revenue fromA relatively significant growth. Sino Medical has also established R&D and marketing centers in the United States, Europe, and the Asia-Pacific region.

Technological and Product Trends: Vigorous Industry Innovation with Frequent Emergence of “Black Tech”

Coronary Artery Field:Bioabsorbable Technologies Remain a Key Focus; IVL Technology May Resolve the Challenge of Calcification

Coronary intervention procedures will place greater emphasis on precision diagnosis and treatment as well as prognostic outcomes, with the integration of FFR, OCT, and IVUS opening up new possibilities.With the advancement of high-end imaging technologies, adjunctive techniques such as FFR, OCT, and IVUS are likely to become routine in clinical practice. Although the domestic market in China is currently highly competitive, no clear market leader has emerged. At present, achieving full industry chain integration remains a key strategic focus.Enterprises with integrated applications and stronger sales capabilities have a competitive advantage.

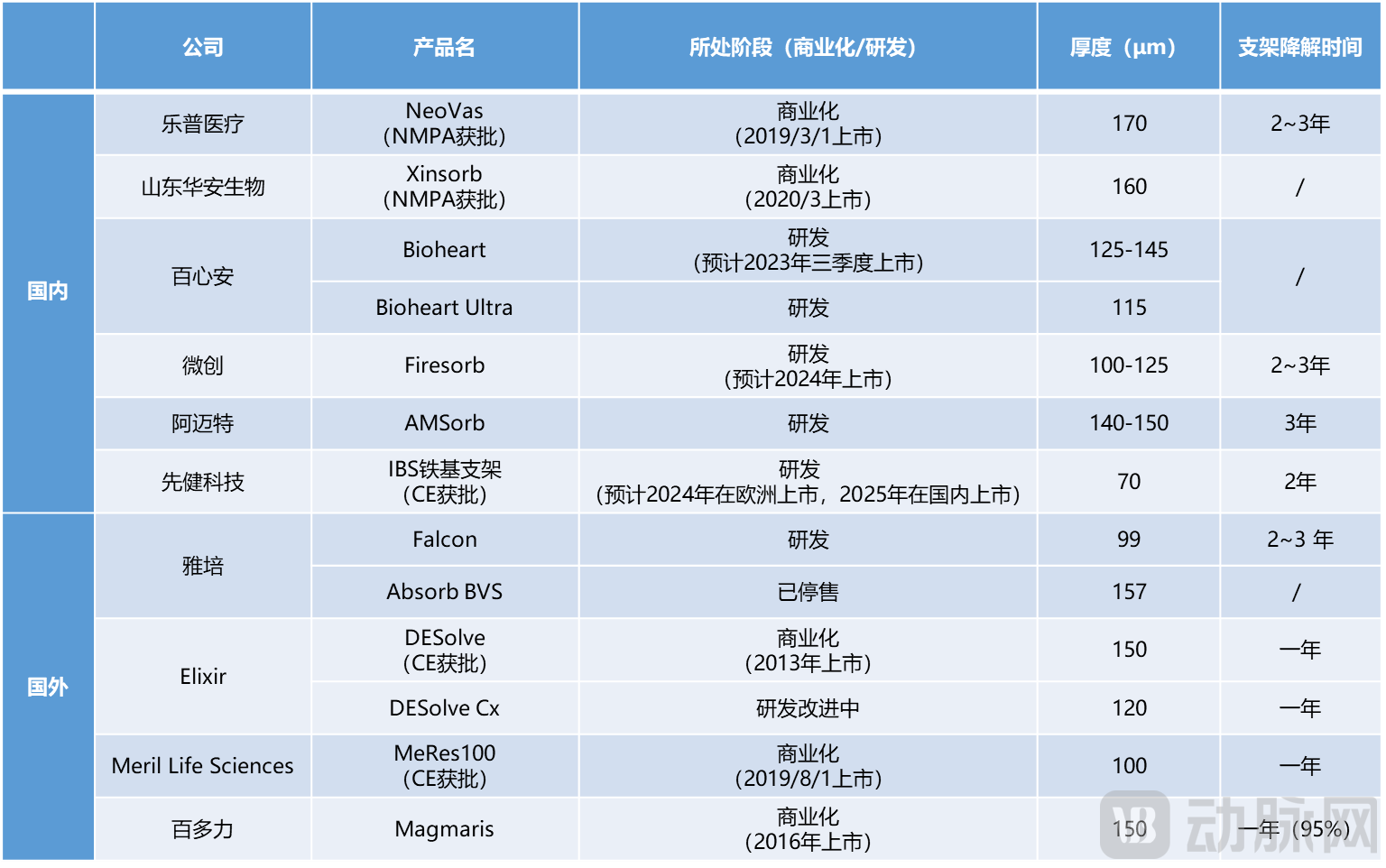

Stents will remain the mainstream products in the future, drug-coated balloons will play a supportive role, and bioresorbable technologies are the focus of research and development.Drug-coated balloons align better with the concept of "implant-free" therapy. Clinical usage data and physician feedback indicate a continuous rise in the adoption of drug-coated balloons, which are expected to capture a portion of the stent market in the future. However, due to their broader applicability and irreplaceable role in certain clinical scenarios, stents will remain the mainstream product. Bioresorbable scaffolds may represent the ultimate evolution of this technology. Currently, research on biodegradable metal scaffolds is gaining significant momentum, with magnesium-based and iron-based scaffolds showing relatively advanced progress. Zinc alloy scaffoldsDue to their favorable biocompatibility and moderate degradation rates, research interest has been steadily increasing, with related products currently in the early stages of structural design and process development.

Progress of Bioresorbable Scaffold Products

Data source: VCBeat Research Institute, compiled from public information

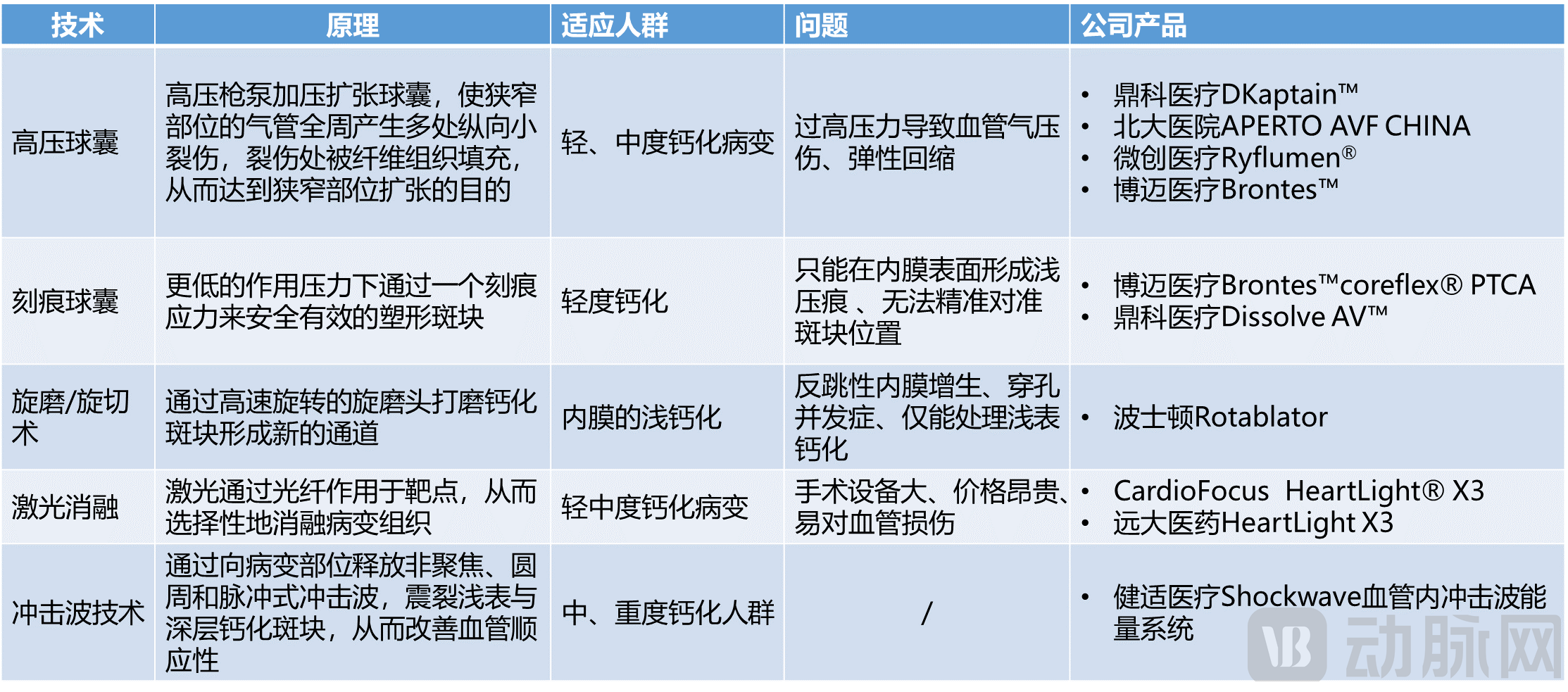

Shockwave balloon technology is poised to completely resolve the challenge of calcification.Among all patients in China requiring coronary stent implantation, approximately 30% present with moderate-to-severe calcified lesions. However, existing interventions—such as high-pressure balloons, atherectomy, and scoring balloons—have certain limitations, particularly in cases of deep, severe calcification and calcified nodules.Question.

Comparison of Common Devices for Managing Coronary Artery Calcification

Data source: VCBeat Research Institute, compiled from public information

Shockwave’s innovative Intravascular Lithotripsy (IVL) is regarded by the industry as the most promising therapeutic solution for ending the treatment challenges of coronary artery calcified lesions.Compared with traditional devices for treating calcified lesions, Shockwave offers significant advantages: 1. Significantly improved safety. The shockwave balloon allows for better directional control and avoids heat generation, thereby preventing vascular injury; 2. A novel lumen management concept that is more aligned with clinical practice. It uses shockwaves to "soften" calcified plaques, restoring elasticity to hardened vessels and recovering vascular compliance; 3. OperationSimple and with a short learning curve, this product has already been used in over 70,000 clinical cases.

JianShi Medical Product Images

Data source: Materials provided by Jianshi Medical

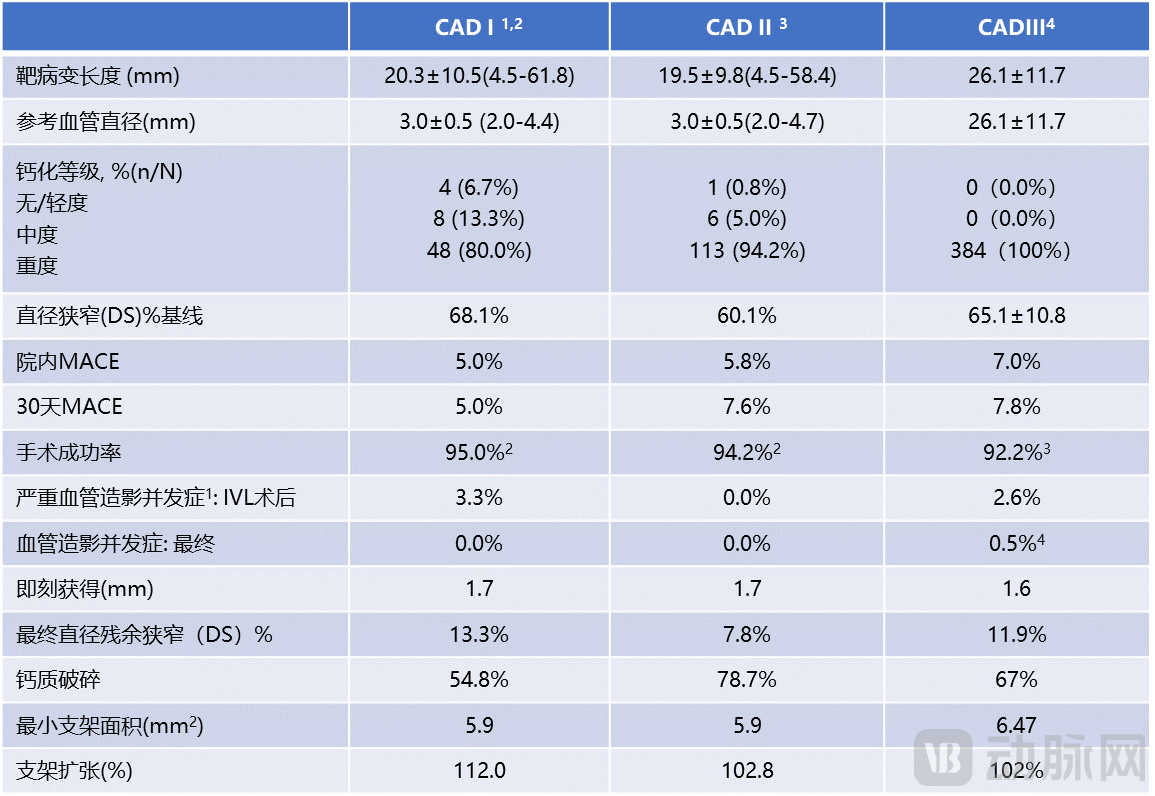

Shockwave Clinical Data Results

Data source: Information provided by GenScript Medical

Valve Field:New Valves, Process Optimization, and Technological Advancements Drive Sector Growth

Aortic Valve: Therapeutic products for valvular stenosis are continuously being optimized, with the focus in the next phase shifting to the field of regurgitation.

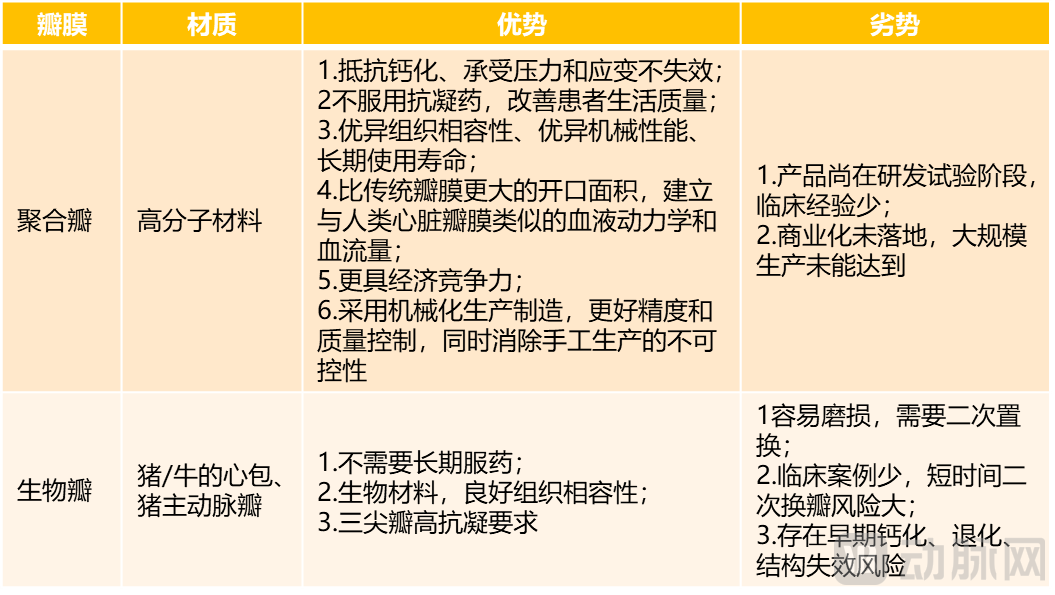

Currently, the majority of products on the market are designed for niche populations, with rapid product iteration cycles.From the valveIn terms of material, the trend toward younger patients has raised higher demands for valve durability. Polymer valves not only exhibit performance similar to that of bioprosthetic valves but also demonstrate strong resistance to calcification, extended service life, and high tissue compatibility, suggesting they may potentially replace bioprosthetic valves in the future. However, related products are still in the research and experimental stage, with limited clinical experience; thus, commercialization is expected to take considerable time.

Comparison of Polymer Valves vs. Bioprosthetic Valves

Source: VCBeat Research Institute, compiled from public information

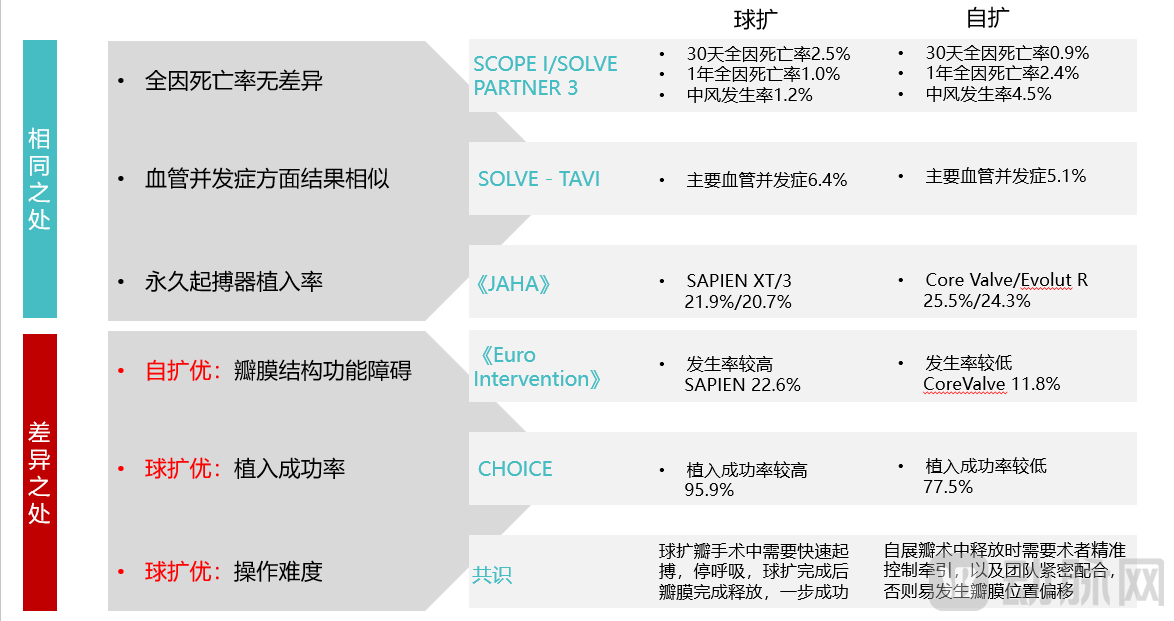

Valve dilation methods are also continuously evolving, with balloon-expandable and self-expanding valves expected to complement each other in the future.. Currently, due to the high rate of valve calcification in China, self-expanding valves will continue to dominate the market over the next 3–5 years. However, balloon-expandable valves offer significant advantages in delivery, deployment, and apposition, making them highly likely to become the mainstream product in the future. Self-expanding valves, owing to their retrievability, cancould serve as a strong complement.

Comparison of Valve Dilation Methods

Data Sources: ClinicalTrials, JAHA, EuroIntervention

Interventional therapy for aortic stenosis has become relatively mature; in the future, interventional treatment of aortic regurgitation will emerge as a key challenge to be addressed in the field of aortic valve disease.Currently, most products on the market rely solely on radial force for fixation, which can provide sufficient support only when there is a certain degree of calcification in the aortic valve.Only half of the patients can be treated, and existing products are difficult to use in patients with reflux.

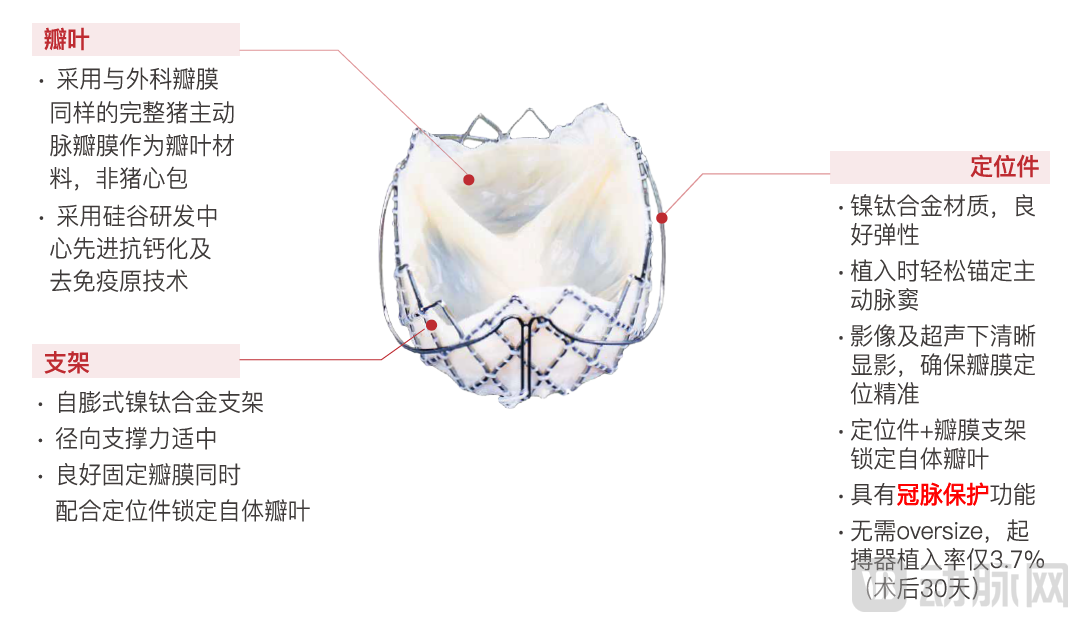

“J-Valve Transapical Valve” is the first domestically developed original aortic valve capable of treating both aortic stenosis and aortic regurgitation (insufficiency).Unlike other aortic valves, Jiecheng Medical's independently developed positionableThe valve enables autonomous navigation and positioning for valve implantation, while also effectively treating regurgitation.

In addition to its dual indications, the unique design of the J-Valve addresses many limitations of existing products: it employs intact aortic valve leaflets—the same material used in surgical bioprosthetic valves—rather than pericardial tissue. Meanwhile, its larger-diameter delivery sheath minimizes compressive damage to the valve, thereby ensuring excellent durability. The concave design at the top of the J-Valve’s short stent provides effective coronary protection, even in cases with low coronary ostia or a narrow or low sinotubular junction.

J-Valve Product Image

Source: VCBeat Research, compiled from public information

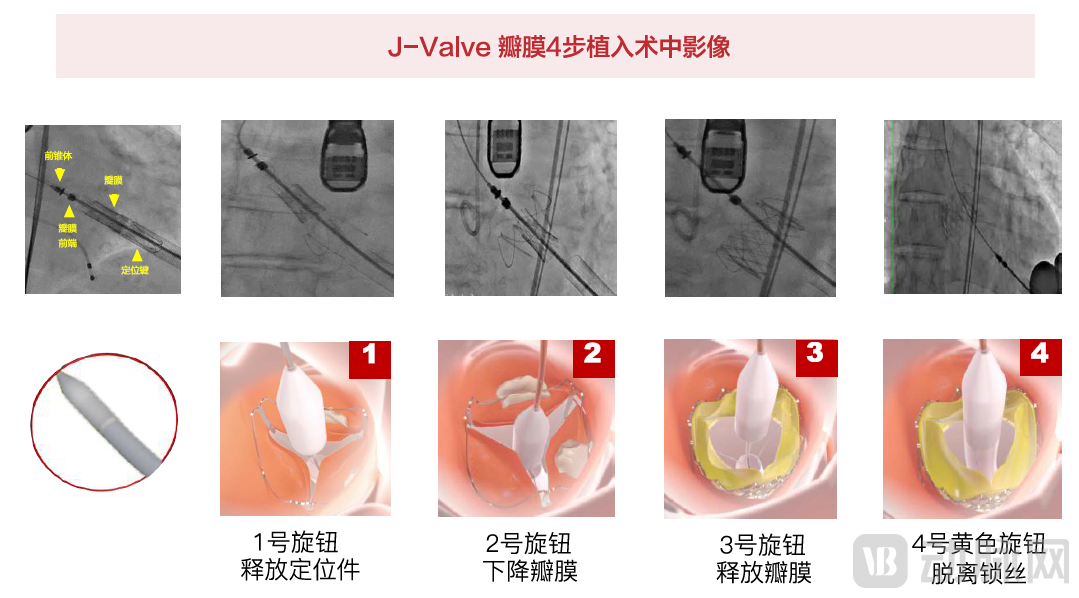

From a clinical perspective,The J-Valve demonstrates excellent post-procedural outcomes and offers operational convenience, with a short device manipulation time that allows valve replacement to be completed within 10 minutes.The transapical J-Valve has currently received approval from the National Medical Products Administration (NMPA), while the transfemoral J-Valve has also entered the clinical trial phase. In the future, these two access routes will complement each other.Bright prospects.

Imaging During J-Valve Implantation

Source: VCBeat Research Institute, compiled from public information

Mitral Valve: TEER Repair Technology Leads the Pack, While Replacement Remains the Future Direction

The technical pathways for transcatheter mitral valve repair are highly diverse; judging from current developments,TEER technology is simple and effective, and will be the mainstream approach in the future.. Abbott's MitraClip is far ahead of other products, with over 140,000 implants performed, demonstrating an absolute lead.Advantages. In China, TEER products exhibit limited substantive differentiation. The most advanced candidates are Dejin Medical’s DragonFly and Hanyu Medical’s ValveClamp, both of which have entered clinical trials.

TEER Product Comparison

Source: VCBeat, compiled from public information

Transcatheter Mitral Valve Replacement Is More Promising as the Ultimate Solution, for the following reasons: 1. Transcatheter replacement has a broader range of indications. The vast majority of transcatheter mitral valve repair products struggle to effectively address complex organic mitral valve lesions, resulting in suboptimal postoperative outcomes for patients with regurgitation. As the technology matures, more MR patients will opt for transcatheter replacement surgery in the future. 2. Repair surgery demands high technical proficiency, whereas TMVR has a shorter learning curve and is more likely to be widely adopted in the future.

Interventional Repair and Interventional Replacement

Data source: Compiled by VCBeat Research Institute based on relevant literature

The Development of Transcatheter Mitral Valve Replacement Still Requires Time; Two Domestically Produced Replacement Devices Are Highly DistinctiveCurrently, Abbott’s Tendyne is the only TMVR device worldwide to have received CE certification. The three major challenges of TMVR—anchoring, delivery access, and valve design—have yet to be fully resolved, leaving Chinese companies with significant potential to surpass imported manufacturers. Among them, MicroPort CardioFlow (Yixin Medical) and Nuomai Medical are progressing the fastest, both entering pivotal clinical trials for registration in 2021. Both products adopt a tri-leaflet bovine pericardial valve design. MicroPort CardioFlow’s MitraFix offers both transapical and transfemoral venous access, features the world’s smallest delivery system, and has demonstrated high implantation success rates and favorable postoperative outcomes in current clinical trials. It is poised to make a significant impact on the international stage and is expected to successfully launch in 2023. Nuomai Medical’s Mi-thoThe transapical approach utilizes a double-layer self-expanding partially retrievable stent. The outer stent features a D-shaped structure that better conforms to the physiological anatomy of the mitral valve, while its unique triple-layer barb anchoring system effectively prevents valve displacement, thereby enhancing procedural safety.

Progress of Mitral Valve Replacement Products

Data source: VCBeat, compiled from public information

Tricuspid Valve: High Value of Three Major Original Domestic Technologies, Promising Future

High-Value Domestic Original Technologies Hold Promising Prospects.Progress in tricuspid valve products has been slow, while repair technologies are relatively more advanced. Currently, only three repair products—Edwards Pascal, Cardioband, and Abbott TriClip—have received CE certification globally. Huihe Medical’s achievements in China are remarkable. Its independently developed K-Clip replicates Kay’s procedure via an interventional approach, demonstrating significant improvement in regurgitation, and has now entered the clinical stage.

No tricuspid valve replacement products have been launched globally yet,Domestic Tricuspid Valve Replacement Shows Strong Momentum, Even Poised to Overtake Overseas Markets. The Jian Shi LuX-Valve Plus is the first tricuspid valve replacement product with fully independent Chinese intellectual property rights; it underwent its first clinical application in hospitals in May and is highly likely to become the world’s first commercially approved tricuspid valve replacement product.

Tricuspid Valve Repair Products

Tricuspid Valve Replacement Products

>>>>

Occluder:Fully Degradable, Customizable, or the Final Form

Occluder technology has matured, leaving limited room for product optimization; future development will focus on fully bioresorbable and customized solutions.Whether for traditional congenital heart disease (CHD) occluders or left atrial appendage (LAA) occluders, biodegradable materials represent a key area of research. With the approval and market launch of Lepu Medical’s biodegradable CHD occluder, the field of CHD occlusion has entered the era of biodegradability. MemoSorb utilizes medical-grade polymer materials that gradually degrade within the human body and are safely absorbed by tissues, thereby avoiding complications and chronic inflammation.symptomatic reaction, marking a major leap forward in the development of domestically produced occluders.

Customization of Occluders Is Also a Major Future Trend. There is significant individual variation in left atrial appendage (LAA) anatomy, and no single occluder can optimally address all morphological variants. With advances in technologies such as 3D and 4D printing, customized LAA occluders are expected to better resolve this issue in the future.Currently, Lepu Medical’s Memo series has begun offering customized services.

Rhythm Management:Pulsed Field Ablation Shows High Growth Potential, Pacemakers Enter the Leadless Era

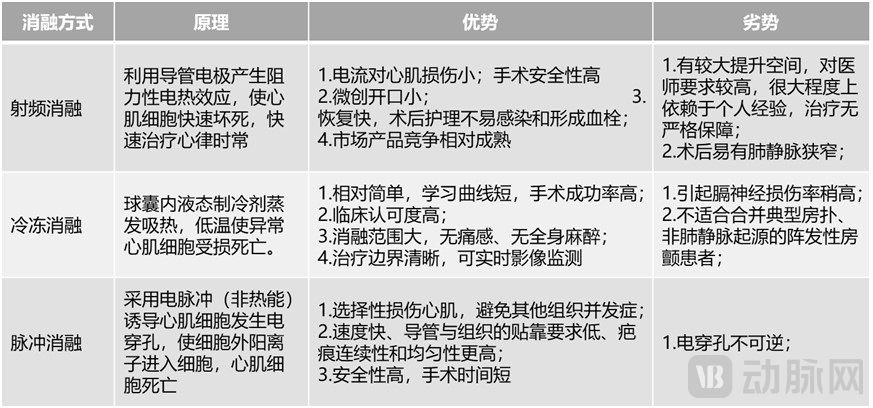

Pulsed Ablation System: Pulsed ablation is exhibiting high growth potential and is regarded as the next-generation disruptive ablation technology.

PFAHighly likely to replace cryoablation and radiofrequency ablation in the future. Radiofrequency ablation and cryoablation cannot selectively destroy tissue within the ablation zone and require catheter-tissue contact, which poses a risk of injury to adjacent structures such as the esophagus, coronary arteries, and phrenic nerve. Pulsed field ablation (PFA) overcomes the limitations of these two ablation techniques by enabling selective myocardial injury while avoiding complications in other tissues. Furthermore, it is simple to operate, with a procedure time approximately half that of conventional surgeries. Numerous preclinical and clinical studies have confirmed the safety and efficacy of PFA. Clinical outcomes demonstrate that the ablation efficiency of PFASignificant improvement, with a very low incidence of complications; clinicians hold PFA technology in high regard.

Comparison of Different Ablation Methods

Data source: VCBeat, compiled from public information

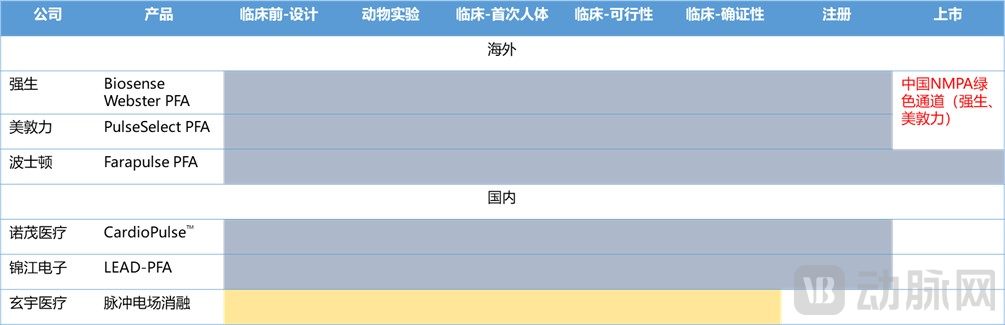

The advent of pulsed ablation has unlocked greater potential in the ablation field, with a new track beginning to take shape.Major players such as Johnson & Johnson, Medtronic, and Boston Scientific have already established their presence in the field, while Chinese enterprises are also actively positioning themselves in the PFA sector. Key products include: CardioPulse, independently developed by Nuomao Medical (with the first-in-human clinical case completed); the LEAD-PFA System by Jinjiang Electronics (type testing concluded in April 2021, currently in the registration-related clinical trial phase); and the Pulsed Field Ablation System by Xuanyu Medical (submission made).type testing).

PFA Product Progress

Source: VCBeat, compiled from public information

Pacemakers: The Era of Leadless Devices Has Arrived

Leadless Pacemaker Successfully Launched: The Pacemaker Era Enters the Leadless Age.Since the widespread adoption of pacemakers, complications related to leads and generator pockets have persisted. Leadless pacing completely frees patients from the burdens associated with leads and pockets, while also simplifying the surgical procedure. Since its official market launch in 2015, there have been over 100,000 implantations worldwide, and multiple studies have demonstrated the safety of leadless pacemakers as well as the efficacy of their electrical parameters. In terms of sales, imported leadless pacemakers hold a clear advantage: Medtronic’s Micra (the world’s first leadless pacemaker, with cumulative implants exceeding 70,000 cases) and Abbott’s Aveir (the world’s only retrievable leadless pacemaker, which launched in April). Due to high technical barriers, these products are expected to maintain a monopoly in the short to medium term, extending the timeline for domestic substitution.Relatively long.

Scope of application continues to expand.Currently, leadless pacemakers cannot sense atrial activity and are limited to sensing and pacing the right ventricle. They are primarily indicated for patients who meet the criteria for single-chamber right ventricular pacing. In the future, as leadless pacemakers become capable of secure atrial fixation or simultaneous implantation in both the atrium and ventricle, they are expected to be suitable for all patients. Meanwhile, leadless pace-The target population for pacemakers is gradually expanding, with elderly patients, children, valve replacement recipients, and other special populations becoming potential users, indicating a substantial market opportunity.

Heart Failure Management:Breaking Through Surgical Limitations Will Become a Milestone for the VAD Boom

VADInterventional procedures will become a milestone for the VAD industry.Due to technical limitations, percutaneous artificial hearts cannot provide long-term circulatory support; therefore, VAD implantation currently remains predominantly surgical. However, the steep learning curve and limited procedural volume associated with open surgery will significantly hinder the widespread adoption and utilization of VADs, thus driving the development of implantable artificial heartsWhether artificial hearts can break free from the constraints of surgical intervention will be the most critical factor in the development of ventricular assist devices (VADs).

The unexpected clinical outcome of the atrial shunt device may be related to patient selection.In February, the failure of Corvia’s Phase III clinical trial for its atrial shunt device dealt a significant blow to the atrial shunt market. However, clinical setbacks do not necessarily indicate that atrial shunting technology is unfeasible; the atrial shunt market continues to gain recognition from experts and investors. Clinical data from Corvia demonstrate that the atrial shunt device can reduce the incidence of heart failure events and improve health outcomes in patients with normal pulmonary vascular resistance, no implanted pacemakers, and no pulmonary vascular disease. This suggests that CorvThe failure of the Phase Ia clinical trial may be attributed to patient selection.

The above is an excerpt from the main content of the report. The complete framework of the report is as follows. Scan the QR code to access the mini-program and read the full report for free.

Chapter 1: Industry Status: Under Centralized Procurement, the Cardiovascular Industry Has Gradually Matured

1.1 Normalization of Centralized Procurement: Coronary Artery Products Lead the Way with Comprehensive Centralized Procurement, While Other Fields Have Also Launched Localized Centralized Procurement Initiatives

1.2 Accelerated Domestic Substitution: Continuous Technological Breakthroughs and Rising Market Share

1.3 The Competitive Landscape Is Gradually Clarifying: From a Hundred Schools of Thought to the Emergence of Market Leaders

Chapter 2 Industry Value: Value Remains Intact, with Valve Devices and Heart Failure Management as the Most Promising Areas

2.1 Value Analysis: High Industry Ceiling, Continued Optimism in the Primary Market

2.2 Key Focus Areas: Mitral and Tricuspid Valves Show the Most Promise, with Long-Term Optimism for Heart Failure Management

Chapter 3 Future Trends: Technological Upgrades and Diversified Innovation Are the Keys to Breaking Through

3.1 Competitive Factors and Industry Landscape: Centralized Procurement Benefits Leading Enterprises in the Long Term, Potentially Leading to an Oligopolistic Market Structure

3.2 Technology and Product Development Trends: Vibrant Industry Innovation with Frequent Emergence of “Cutting-Edge Technologies”

3.2.1 Coronary Artery Disease Sector: Precision PCI and Bioresorbable Technologies Remain Key Focus Areas; IVL Technology May Resolve the Challenge of Coronary Calcification

3.2.2 Valve Sector: Novel Valves, Process Optimization, and Technological Advancements Drive Sector Growth

3.2.3 Occluders: Fully Biodegradable, Customized, or the Final Form

3.2.4 Rhythm Management: Pulsed Field Ablation Shows High Growth Potential, and Pacemakers Enter the Leadless Era

3.2.5 Heart Failure Management: Breaking Through Surgical Limitations Will Be a Milestone for the VAD Boom

This report is part of the series for the 6th Future Healthcare 100 Conference hosted by VCBeat. The conference will be held online from June 14 to 18, 2022, and the report will be presented and released during the event. To access the full report, please scan the QR code.