Overseas Vascular Interventional Robotics Companies Expand Capacity and Enter China Amid Commercial Scaling Phase

Stereotaxis

Developer and Manufacturer of Medical Robots

Robocath

Cardiovascular Medical Robotics Developer

Corindus

Research on Robot-Assisted Vascular Intervention Treatment

Recently, there has been ongoing heated discussion about vascular intervention robots.

Proponents argue that vascular interventional robots can reduce radiation exposure for physicians while improving the precision and efficiency of procedures. Opponents contend that their business model has significant flaws, and that their stability and net clinical benefit remain to be observed.

Beyond the controversy, market data for vascular intervention robots is impressive. According to Frost & Sullivan, the global market size for pan-vascular surgical robots was $31.4 million in 2020 and is projected to grow to $1.61 billion by 2026, representing a compound annual growth rate (CAGR) of 87.4% from 2016 to 2026.

According to incomplete statistics, there are currently seven vascular surgery robots approved worldwide, as shown in the figure below. Due to mergers and acquisitions, business adjustments, and other factors among companies, three products are currently more active and representative: Corindus’s CorPath GRX, Robocath’s R-One, and Stereotaxis’s Genesis RMN.

This article reviews these three representative companies and their underlying products, using specific case studies to clarify the development trajectory and process of vascular intervention robots, with the aim of providing some reference for industry professionals.

Overview of Overseas-Approved Vascular Interventional Robotic Products; Contact the Author for Any Omissions

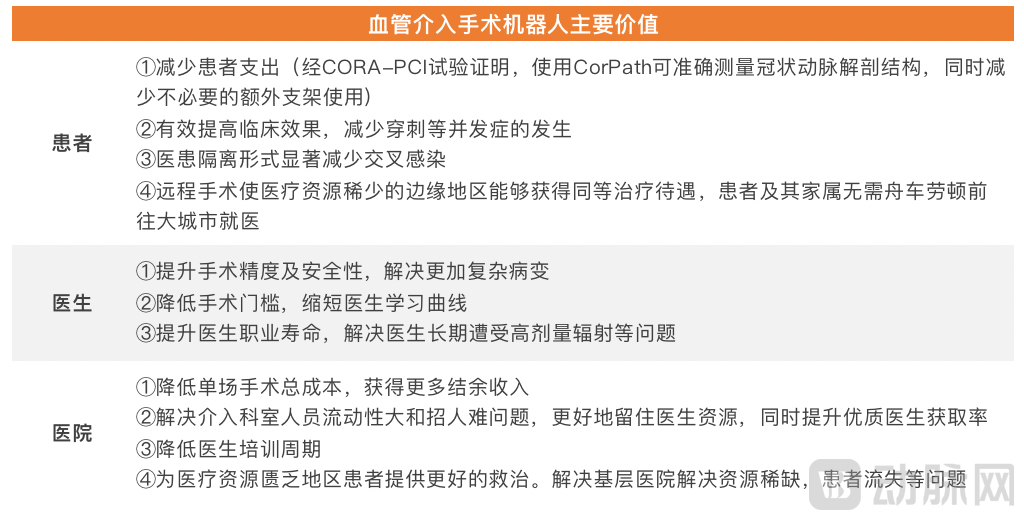

Based on clinical data disclosed by various companies, vascular interventional robots generally enable physicians to reduce radiation exposure by approximately 90%. Certain products, such as CorPath, can reduce physicians’ radiation exposure by up to 95% and help lower the risk of hospital-acquired infections to some extent. Freed from heavy lead aprons, physicians can leverage the precise positioning and clear, expansive surgical field provided by vascular interventional robotic systems to perform procedures with greater focus and efficiency.

Summary of Value Assessment for Vascular Interventional Surgical Robots

Haoyue Capital“It is believed that approved products already exist in both the orthopedic and laparoscopic surgical robot sectors, demonstrating the intrinsic value of surgical robotics through their clinical application. In vascular interventional procedures, high precision is required, while physicians face occupational hazards such as prolonged radiation exposure, which shortens their career longevity. Given the continuously growing population of cardiovascular patients, market demand for these solutions is inevitable. Furthermore, vascular intervention robots are not limited to cardiovascular applications but also extend to neurointerventional (cerebrovascular) and peripheral vascular procedures, indicating significant market potential.”

In his presentation at SCAI 2017, Ryan Madder, MD, FACC, cited the example of two physicians who began their careers simultaneously. One decided to perform only manual PCI throughout his career, while the other chose to perform only robotic-assisted PCI. The annual radiation exposure for 100 PCIs was over 2,000 μGy (specifically 2,060 μGy) for the manual operator, compared to only 98 μGy for the physician using robotic assistance. After 20 years, the cumulative radiation exposure for the manual PCI physician amounted to 41,200 μGy, whereas the robotic-assisted physician’s exposure totaled 1,960 μGy. The cumulative radiation dose received by the robotic-assisted physician over 20 years was equivalent to the radiation exposure incurred by the manual PCI physician in just the first year.[1]

Patients treated with vascular robots experience an average 20% reduction in radiation dose, without increasing fluoroscopy time or contrast agent usage. According to the latest clinical data disclosed by Robocath at the EuroPCR conference, its R-One surgical robot achieved a 100% clinical success rate and over 95% technical success rate in recent clinical trials, with zero robot-related complications within 30 days post-operation.

Furthermore, data from Siemens CorPath indicate that accurate measurement of coronary anatomy can reduce the use of unnecessary additional stents by 8.3%. Vitor Mendes Pereira, a neurosurgeon at Toronto Western Hospital who has used Siemens Corindus, commented, “Precision is a key element in neurovascular interventions. I have clearly observed the positive impact of enhancing these delicate procedures with robotic assistance on our approach to patient care.”

Regarding the learnability of vascular interventional surgical robots, Ehtisham Mahmud, MD, FACC, stated that operators typically require 20 to 25 cases to become proficient; however, the more experienced the operator, the faster the transition to the robotic system.[1]

However, some domestic experts have pointed out that although technological advancements have led to significant progress in vascular interventional surgical robot systems, it is important to recognize that current interventional surgical robot systems still have many shortcomings. The main issues are concentrated on force feedback and the compatibility of consumable auxiliary devices.

First, the haptic feedback in most systems is limited to the contact force between the catheter tip and the tissue, lacking comprehensive force feedback for the entire interventional device within the vasculature. Most studies rely on force sensors to indirectly measure the forces exerted on the surgical catheter, which inevitably compromises procedural safety. The absence of tactile mechanical feedback restricts its application in complex and challenging cases, such as calcified lesions and chronic total occlusions, and also poses challenges regarding intraoperative vascular injury and hemostasis.

Secondly, vascular interventional procedures require a wide variety of guidewires, catheters, stents, and auxiliary devices of different specifications and models. During the procedure, it is not possible to achieve the rapid exchange of guidewires and catheters as can be done with manual operation; in particular, simultaneous manipulation of catheters and guidewires and real-time execution of stent deployment cannot be performed as effectively as with manual dexterity. Frequent instrument changes and repetitive maneuvers can cause vascular injury, leading to thrombosis, embolism, dissection, or even vessel rupture, while also increasing the patient’s radiation exposure time and the dosage of contrast agent used.[2]

Finally, the high system costs and annual maintenance fees, along with the stringent requirements for facility infrastructure and operator training, have also become barriers to its market promotion and adoption.

Based on U.S. FDA approval data, we found that vascular interventional robotic systems take an average of only four months from submission of the marketing application to approval. However, it is important to note that this timeframe does not include the entire pre-market clinical trial period. For modifications to already cleared products, the average review time is accelerated to approximately one month.

According to industry insiders, for Class III medical devices in China and abroad, the review and approval process from submission of the marketing application to final approval (excluding preliminary clinical trials) typically takes 3–4 months, provided that all documentation is complete and the regulatory review proceeds smoothly.

As an innovative medical device in a new category, the vascular interventional robot achieved such a rapid approval speed during its initial phase a decade ago, demonstrating the U.S. FDA’s recognition and acceptance of this technology.

FDA Approval Status of Vascular Interventional Robots in the United States,VCBeat Graphics (Following the acquisition of Hansen Medical in 2016, the Magellan and Sensei systems were gradually phased out and are therefore excluded.This Statistics)

Insurance plans that cover minimally invasive surgery typically also cover robotic surgery. This is indeed the case for widely held insurance programs such as Medicare. Specific coverage will depend on the individual’s policy details.

According to the health regulations issued by the Insurance Regulatory and Development Authority of India (IRDAI) in 2019, all insurance companies are obligated to cover robotic therapy. Consequently, all insurers offer this coverage, albeit with varying sub-limits and policy conditions defined in their products.[3]

“Robotic surgery is performed only at more advanced medical centers, and its operators require extensive training. Furthermore, the procedure is costly, making it an option primarily for policyholders with high coverage limits, while those with lower coverage may opt for traditional techniques. Generally, robotic surgeries account for less than 0.02% of total claims,” stated Shreeraj Deshpande, Chief Operating Officer of Future Generali India Insurance. “Depending on indications, approximately 3–4% of overall claims may involve the use of robotic technology in surgery.”[3]

In March 2022, Stereotaxis opened its new headquarters in the Global Tower in downtown St. Louis, spanning 43,000 square feet (approximately 4,000 square meters).

Stereotaxis was founded in 1990; the image shows its new headquarters in downtown St. Louis. Image source: stlpublicradio

In April 2022, to further the development of Corindus, Siemens relocated its headquarters from Waltham to 275 Grove Street, Newton, Massachusetts. The facility’s size expanded from 35,000 square feet (approximately 3,200 square meters) to 77,000 square feet (approximately 7,100 square meters), more than doubling its original area. The new headquarters will serve as the global center of excellence for Siemens Healthineers’ vascular robotics technology, encompassing research and development, manufacturing, and administrative functions.

In addition, the center has established a fully equipped “Customer Experience Center” to provide physicians and catheterization laboratory staff with hands-on interactive training on the CorPath GRX system. The center features simulated robotic setups mimicking those found in hospital catheterization labs and control rooms, including capabilities for remote operation via various types of connectivity.

Per Bergman, Vice President of R&D at Corindus, stated, “The spacious, dedicated laboratories in the new headquarters will provide the team with more efficient collaborative and technical spaces for innovation. The world-leading cleanrooms and model workshop will enable the company to accelerate prototyping and shorten development cycles.”

At the same time, all three companies have independently made corresponding strategic arrangements for the Chinese market.

In July 2021, Siemens Healthineers’ Corindus CorPath® GRX interventional surgical robot, the latest generation of the Tuling™ series, was approved to enter the Special Review Procedure for Innovative Medical Devices and has now passed the NMPA’s special review application for innovative medical devices. As a result, Siemens Healthineers will become the first foreign manufacturer of medical imaging equipment to enter China’s interventional robotics market through the special review application for innovative medical devices.

In August 2021, Shanghai MicroPort EP MedTech Co., Ltd. and Stereotaxis announced a partnership, under which MicroPort EP became the exclusive distributor of Stereotaxis’s magnetic navigation electrophysiology robot in mainland China. This marked Stereotaxis’s formal entry into the domestic market.

In October 2020, Shanghai MicroPort MedBot (Group) Co., Ltd. and France’s Robocath S.A.S. jointly established a joint venture in China, ZhiMai Robotics Co., Ltd., to introduce the R-ONE system into the Chinese market.

In summary, it is evident that overseas vascular interventional robotics companies have gradually entered a phase of rapid development. Siemens’ Corindus and Stereotaxis have both relocated their headquarters and expanded operations this year, striving to ensure stable mass production and commercialization. Robocath and Stereotaxis have partnered with Chinese enterprises, while Corindus has applied for the NMPA’s Special Review Channel for Innovative Medical Devices, as all these companies set their sights on the lucrative Chinese market.

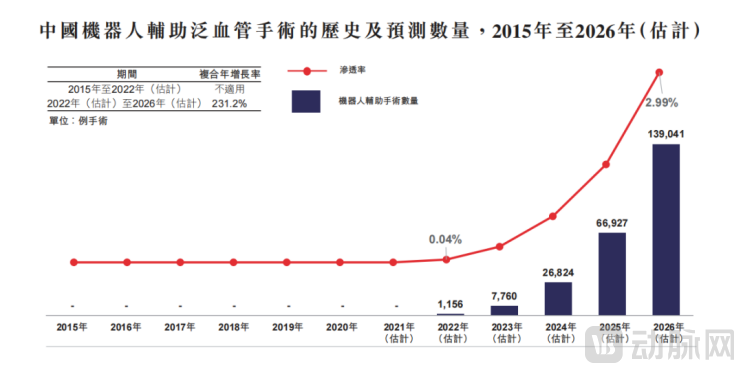

According to Frost & Sullivan, the number of robot-assisted pan-vascular procedures performed annually in China is estimated to reach 139,041 cases in 2026, representing a compound annual growth rate (CAGR) of 231.2% from 2022, with a penetration rate of approximately 3.0% in 2026. The figure below illustrates the historical and projected numbers of robotic vascular interventional procedures in China:

Source: Frost & Sullivan

According to data from Qianzhan Industry Research Institute, the penetration rate of robot-assisted pan-vascular surgery in China was preliminarily estimated at approximately 0.04% in 2022. As the prevalence of coronary artery disease continues to rise, the availability of pan-vascular surgical robots is expected to gradually increase, with the penetration rate projected to reach 2.99% by 2026.

So, where will the opportunities lie for domestically produced vascular interventional robots?

Although vascular interventional surgical robots started late and have low penetration rates, they are truly on the same starting line as the global market. Therefore, it is no longer necessary to discuss technologies in terms of “import surpassing” and “domestic substitution.” However, given that overseas products have gained certification advantages, where do the opportunities lie for Chinese manufacturers of vascular interventional robots?

VCBeat interviewed relevant domestic companies and found that the most frequently discussed topics centered onHigh Cost-Effectiveness, Specialized Technologies, and Expansion into New Application ScenariosThree aspects.

High overseas labor and production costs are passed on to product pricing, making the resulting high prices an invisible barrier to market adoption. Leveraging China’s advantages in labor-intensive industries, cost-effectiveness has long been a traditional strength of domestic medical device companies, and this holds true for vascular intervention robots as well.

Yang He, Founder of Weimai MedicalIt is believed that reasonable pricing is crucial. Interventional robots will serve as a standardized tool for enhancing productivity in the field of interventional therapy. If this technology is priced too high in its early stages, it will fail to achieve rapid market penetration. Therefore, during the product development process, companies must carefully calculate hospitals’ input and output costs, and even the revenue generated by specific departments. This approach will facilitate the broader adoption of the technology. Additionally, companies should avoid homogeneous competition and must possess full independent intellectual property rights to establish unique competitive advantages and maintain controllable costs.

Each company’s proprietary technologies have also become a key advantage in differentiating their offerings from overseas products.

According toRuiXin MedicalIntroduction: Compared with foreign products, its vascular interventional robot offers superior precision and flexibility. With an accuracy of up to 0.1 mm, it enables physicians to place stents or perform balloon dilation at locations and sizes that better match the lesion characteristics, thereby reducing “longitudinal geographic miss.” This advantage is particularly pronounced in complex lesions, such as multivessel disease, diffuse lesions, and chronic total occlusion (CTO). In terms of flexibility, the Ruixin product allows coordinated manipulation of three devices—guide catheters, guidewires, and stent delivery catheters—and supports a wide variety of guidewires and catheters. This means that the robotic system supports a richer and more diverse range of procedural techniques, broadening its clinical application scenarios.

Unlike overseas products, vascular interventional surgical robots from some domestic companies cover the complete surgical workflow for the diagnosis and treatment of cardiovascular diseases. TakingRainmed MedicalFor example, its product, the Flash Robot vascular intervention surgical robot, organically integrates software systems such as functional diagnostic systems, image-guided surgical navigation, and ECG monitoring, with hardware components including multi-function interventional catheters and high-pressure injectors. This integration creates a multi-system functional synergy and a closed-loop data ecosystem, achieving full automation of angiography, diagnosis, navigation, and post-operative assessment.

Currently, the primary application scenarios for vascular intervention robots include coronary intervention, peripheral vascular intervention, and cerebrovascular intervention, with substantial room for expansion in procedural techniques.

Liu Yikun, General Manager of Aopen Medical“It is believed that there are actually a wide variety of vascular interventional procedures. Developing a dedicated machine for each newly identified procedure would not only impose high costs on hospitals but also exceed the spatial capacity of catheterization laboratories. Therefore, we believe that the focus of future product design should be on enabling surgical robots to integrate into more procedural workflows, allowing a single system to perform multiple types of interventions, including those that have not yet emerged.”

In summary, the development of overseas vascular interventional robots has entered a phase of commercial scale-up, offering valuable lessons for domestic companies. Although the industry is currently in the early stages of market promotion and may face a long road ahead in this regard, it generally aligns with the prevailing trend toward precision medicine.

We believe that as related technologies continue to advance, vascular interventional robotic products, standard operating procedures, and clinical applications will further expand. We anticipate the emergence of industry giants comparable to the da Vinci Surgical System and Stryker’s MAKO, which will validate the value of this sector.

References:

1. <Cover Story The Robot Will See You Now... Robotics in the Cath Lab Have Staff Breathing a Sigh of Relief>

2. “Key Technologies and Current R&D Status of Vascular Interventional Surgical Robot Systems”

3. <Does your health insurance policy cover robotic surgery?>

4. Zhang Caini, “Siemens Healthineers Takes the Lead in Entering the Market: The Value of the Multi-Billion Yuan Potential Robotics Sector Is Significantly Undervalued”

Cover image source: https://www.corindus.com/news-events/media-kit