2022 Ophthalmology Industry Research Report: Unlocking Innovation Trends in a Golden Investment Sector

As a rare “dual-high” sector characterized by high growth potential and high entry barriers, the ophthalmology industry has long been hailed as the “golden track” in the capital market. In 2022, with the release of the 14th Five-Year Plan for Eye Health, the ophthalmology sector once again became a focal point. On the other hand, as ophthalmology pertains to non-life-threatening conditions, its subsectors are numerous and fragmented. Therefore, identifying the key priorities within the ophthalmology industry and clarifying the logic underlying its future development warrant close attention.

Based on this, VCBeat has authored the "2022 Ophthalmology Industry Research Report," which will focus on addressing the following questions:

1. How did the ophthalmology market develop in 2022? What were the new trends?

2. Among the three sub-sectors, which one has the greatest future potential and is most worthy of attention?

3. Which sub-sectors in the ophthalmology industry warranted particular attention in 2022, and what has been their development trajectory?

4. Why is the ophthalmology sector attracting attention from the capital market? What are the current development opportunities and challenges it faces?

5. What are the most noteworthy innovation trends in the ophthalmology industry at present?

To clarify the aforementioned issues, VCBeat Research surveyed nearly ten companies in the ophthalmology industry and, integrating its own research findings, sought toIndustry Overview, Segment Scanning, Development Opportunities and Challenges, Typical Enterprise Innovation Cases, Future Trend Analysis...and other dimensions to comprehensively analyze the ophthalmology industry, aiming to provide valuable industry insights for stakeholders and participants.

(Note: The full report can be downloaded by scanning the QR code at the end of the article.)

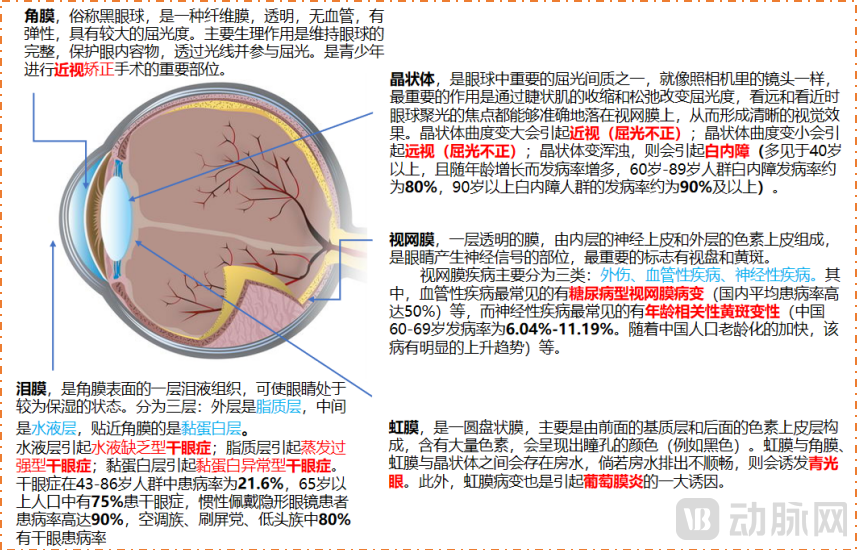

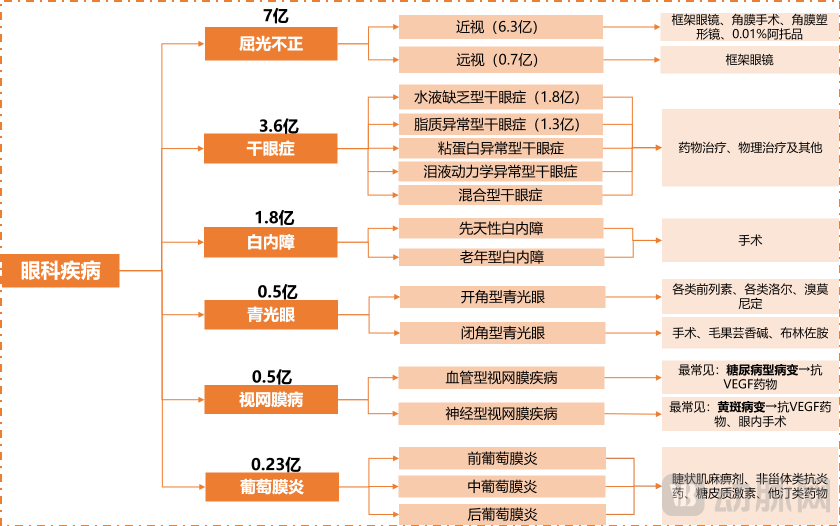

Ophthalmic diseases encompass a wide range of conditions, with refractive errors and cataracts having the highest prevalence:In 2019, the ten most common eye diseases in China included refractive errors (including myopia,hyperopia, presbyopia, and astigmatism), conjunctivitis, dry eye disease, cataracts, blepharitis, retinal diseases, strabismus, amblyopia, glaucoma, and uveitis. Among these, cataracts are the leading cause of blindness, with a prevalence rate of 80%-90% in the population aged 60 and above. Among non-blinding conditions, refractive errors are increasingly becoming a focal point of societal concern; the myopia rate among individuals under the age of 20 is approaching 70% and continues to rise.

Pathogenesis of Major Ophthalmic Diseases

Data Source: Public Information, Compiled by VCBeat.

The ophthalmology sector boasts a large patient base, presenting a blue ocean of demand:Ophthalmic indications are developing at varying rates, with refractive errors and dry eye disease having the largest patient populations. As public health awareness rises, there is a strong and growing demand not only for basic vision (“being able to see”) but also for clear and comfortable vision (“seeing clearly and comfortably”), creating a vast blue-ocean market opportunity in ophthalmology.

Ophthalmic Patient Flow

Data source: Public information, compiled by VCBeat.

Low Penetration Rate of Ophthalmic Disease Treatment, with Broad Future Market Potential:Compared with the United States, China has a significantly larger patient population, yet the market size for ophthalmic devices and pharmaceuticals is only one-eighth to one-fifth of that in the U.S. In terms of treatment rates, there remains a 4- to 5-fold room for improvement relative to the U.S. Overall, China’s ophthalmology market holds substantial growth potential in the future.

Stable Growth Trend to Continue:Since 2017, the global market for ophthalmic devices and ophthalmic pharmaceuticals has maintained a stable growth rate of approximately 5%, reaching a market size of $62.1 billion in 2021. This steady growth trend is expected to continue in the future.

Pharmaceuticals Have a Slight Edge:In terms of sub-sectors, ophthalmic devices account for approximately 42% of the market size, while ophthalmic pharmaceuticals account for around 58%.

Highly Concentrated Competitive Landscape:Overall, the ophthalmology sector features extremely high technological barriers, and the global market currently exhibits a highly concentrated competitive landscape. Companies such as Alcon, Johnson & Johnson, Bausch + Lomb, Essilor, and Novartis occupy the first tier of the market.

The “Trinity” Track: Impressive Growth in Pharmaceuticals and Medical Devices:Since 2014, China’s ophthalmology market has maintained a high double-digit growth rate, reaching a total market size of RMB 210 billion by 2021. Concurrently, the number of ophthalmology enterprises in China has also grown rapidly. Over the ten-year period from 2011 to 2020, the number of registered ophthalmology companies surged from 1,066 to over 10,300, representing a tens-fold increase.

Services Account for the Largest Share, While Pharmaceuticals Exhibit the Fastest Growth:In terms of market size by subsector, the ophthalmic services market accounts for the largest share, at approximately 71%, followed by medical devices at around 17%. Although the ophthalmic pharmaceuticals segment started later and currently holds the smallest market share, it is experiencing the most rapid growth, with a growth rate of approximately 15%, ranking first among all subsectors.

From the perspective of investment and financing, the ophthalmic pharmaceuticals and medical devices sector is seeing a surge in interest:Since 2021, the number of financing events and the total amount raised in the ophthalmology sector have risen rapidly, with 90% concentrated in the field of ophthalmic pharmaceuticals and medical devices. On one hand, the mid-to-high-end market for ophthalmic pharmaceuticals and medical devices remains dominated by imported brands; however, as Chinese manufacturers enhance their technologies and products, there will be significant opportunities for domestic substitution in the future. On the other hand, the current landscape of the ophthalmic pharmaceuticals and medical devices sector is relatively fragmented, with many untapped market niches in terms of product offerings, leaving room for the emergence of industry-leading enterprises in the future.

Data source: public information, compiled by VCBeat

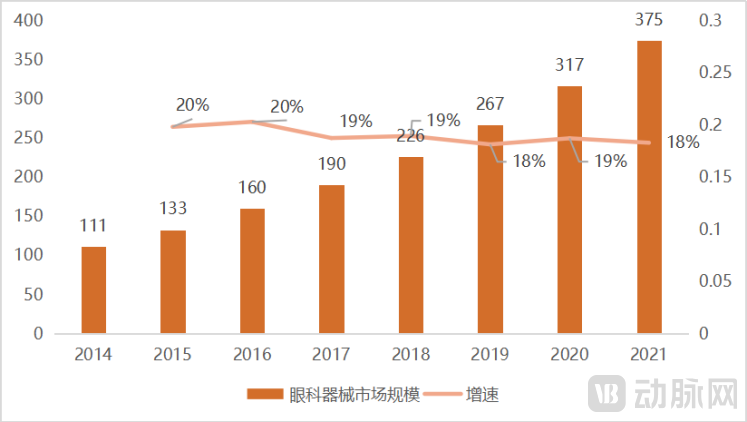

High Demand and Rapid Growth in China's Ophthalmic Device Market:Driven by the rising prevalence of refractive errors among adolescents and the increasing volume of cataract surgeries among middle-aged and elderly individuals, the market size of ophthalmic devices in China has grown rapidly, expanding from RMB 11.1 billion in 2014 to RMB 37.5 billion in 2021, with a compound annual growth rate (CAGR) of 19% over the past five years.

Market Size of Ophthalmic Devices in China

Data sources: Report on the Development of China's Medical Device Industry, Guosen Securities, VCBeat

The ophthalmic medical equipment industry exhibits an extremely high import monopoly rate due to its high technical barriers:High-end manufacturing giants from Germany, Japan, and the United States (such as Zeiss, Alcon, Topcon, etc.) occupyThe vast majority of market share; a high proportion of sales comes from mid-to-high-end devices, among which OCT is one of the products with the highest clinical value and greatest technical complexity.

Among high-value ophthalmic consumables, intraocular lenses and orthokeratology lenses are experiencing rapid development:Surgical implantation of intraocular lenses (IOLs) is the only effective treatment for cataracts, driven by rigid and strong market demand. In 2022, the IOL market size approached RMB 2.6 billion, and it is expected to maintain a continuous growth rate of approximately 10% in the future. Orthokeratology lenses areA rare, safe, and effective approach to myopia prevention and control in children and adolescents; the potential terminal market size is expected to exceed RMB 20 billion over the next five years. The current competitive landscape is favorable, with domestic brands continuously increasing their market share.

Domestic Manufacturers Accelerate Breakthroughs, Import Substitution Shows Promise:Although Chinese manufacturers started later in the field of high-value consumables, a number of ophthalmic companies at the forefront of innovation have emerged in recent years, continuously breaking through in products with high technical barriers and narrowing the gap with imported brands. For example, in 2005, Alpha Vision launched China’s first orthokeratology lens, breaking the monopoly held by imported products; in 2014, Aierbo Nuode introduced the country’s first foldable intraocular lens with independent intellectual property rights and advanced refractive capabilities, and is currently conducting clinical trials for multifocal intraocular lenses.

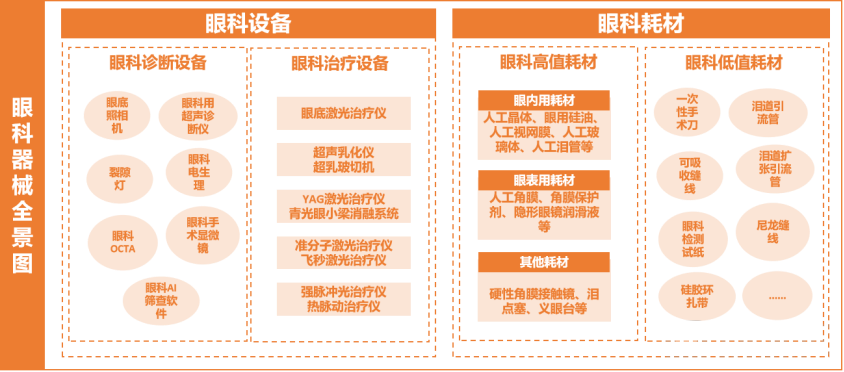

Panoramic View of China's Ophthalmic Device Landscape

Data Source: Blue Book of China's Medical Device Industry, Public Information

Dry Eye Disease and Retinal Diseases Are the Main Battlegrounds for Ophthalmic Drugs, While Myopia Prevention and Control Are Poised to Emerge as a Dark Horse:Ophthalmic drugs are currently widely used in the treatment of myopia, dry eye disease, glaucoma, and retinal diseases, among which dry eye disease, retinal diseases, and uveitis primarily rely on pharmacological therapy.

Mainstream Drugs for Ophthalmic Diseases in China

Data source: Ocumension Therapeutics' prospectus, VCBeat

Low-concentration atropine, anti-VEGF agents, and cyclosporine eye drops are the main product types, with ophthalmic solutions being the predominant dosage form:Cyclosporine eye drops are currently the most effective medication for treating dry eye disease and have become the best-selling product in the U.S. dry eye market. However, in China, sodium hyaluronate eye drops (artificial tears) remain the dominant products available on the market. Anti-VEGF agents are a core driver of ophthalmic drug sales; drugs such as ranibizumab, conbercept, and aflibercept have consistently served as key growth engines and represent one of the most important product categories in the current ophthalmic pharmaceutical market. According to the 2020 National Reimbursement Drug List (covering Basic Medical Insurance, Work-Related Injury Insurance, and Maternity Insurance), eye drops are the most mainstream dosage form, accounting for approximately 68% of all ophthalmic chemical drug categories, followed by eye ointments, ophthalmic gels, injections, oral immediate-release formulations, and implants.

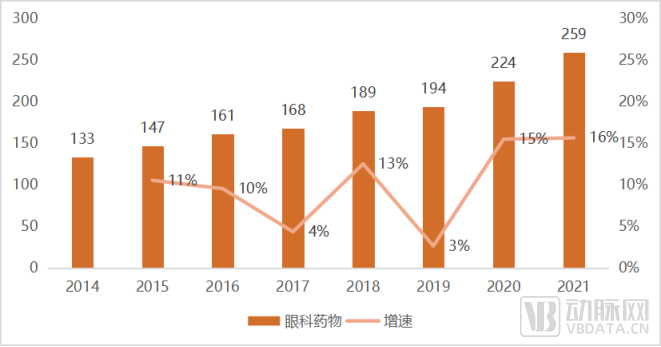

The domestic market for ophthalmic drugs is poised for a fivefold growth over the next decade, indicating immense potential:China’s ophthalmic drug market started relatively late, and its scale still lags behind the global market. Since 2015, the market size of ophthalmic drugs in China has shown steady growth, reaching nearly RMB 26 billion by 2021, with a compound annual growth rate (CAGR) of approximately 8%. As the number of patients with eye diseases continues to rise and the penetration rate of ophthalmic drugs increases, the overall market size is projected to exceed RMB 100 billion by 2030, indicating substantial growth potential.

China's Ophthalmic Drug Market Size

Data Source: Frost & Sullivan, VCBeat

The market size of ophthalmic services in China has exceeded RMB 150 billion, with double-digit growth expected to continue in the future:According to Frost & Sullivan data, the market size of China’s ophthalmic services reached RMB 159.5 billion in 2021, representing a year-on-year growth of approximately 13% compared to 2020. Over the next five years, driven by the growing patient population and increasing public health awareness, we predict that the growth momentum of the ophthalmic services market will continue.

Private Ophthalmic Hospitals Are Expanding More Rapidly and Are Poised to Become a Key Growth Driver in the Future Market:Given that ophthalmic treatment procedures are highly amenable to standardization and process optimization, offering strong replicability, private eye care institutions have successfully attracted significant capital attention. In the future, these private hospitals are poised to further increase their market share and capture ground from public hospitals.

“One Superpower, Multiple Strong Players” Competitive Landscape: The Leading Effect in the Ophthalmic Services Market Is Significant:Since its initial public offering in 2009, Aier Eye Hospital’s market capitalization has risen steadily. By 2020, Aier Eye Hospital had captured a 23.9% share of the private ophthalmic services market, becoming the undisputed leader in the sector. Starting in the second half of 2020, multiple ophthalmology companies, including Huaxia Eye Hospital, Purui Eye Hospital, and He’s Eye Hospital, filed prospectuses one after another, vying to go public. Ophthalmic patients often demand high precision in diagnosis and treatment and are more inclined to choose reputable and trustworthy institutions. Once an industry leader establishes a strong reputation, it can more readily leverage its first-mover advantage, achieve economies of scale, and rapidly enhance its influence, which then extends across all its chain facilities.

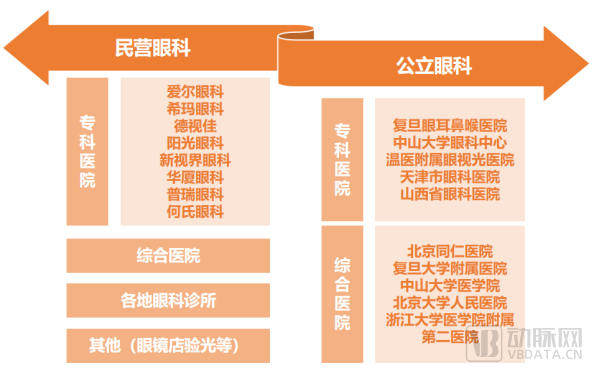

Panoramic View of China's Ophthalmic Service Enterprises

Source: VCBeat

Eye health has been elevated to a national strategic priority, with continuous policy encouragement and support from the Chinese government:Since the release of the “13th Five-Year Plan for National Eye Health (2016–2020)” in 2016, eye health has been elevated to a national strategic priority. In January 2022, the National Health Commission issued the “14th Five-Year Plan for National Eye Health (2021–2025),” marking the entry of China’s eye health initiatives into a new phase of high-quality development. For the first time, fundus diseases have been included in the national strategy, while the prevention and control of myopia among adolescents have once again become a focal point. In addition to eye health-specific policies, the government is progressively refining medical insurance policies and expanding coverage to improve the accessibility of ophthalmic surgeries and medications.

The Growing Ophthalmic Patient Population and Rising Healthcare Expenditures:As population aging intensifies, the economy develops rapidly, and electronic devices such as smartphones and computers become ubiquitous, age-related eye diseases, metabolism-related eye diseases, and fundus lesions caused by high myopia have become increasingly prominent. On the other hand, with improving economic conditions, residents’ health awareness is gradually strengthening, and the proportion of healthcare expenditure is rising. The ophthalmology sector, which has strong consumer-driven characteristics, will be a major beneficiary of this trend.

Domestic Companies Enter the Market Successively, with Technological Innovation Driving a New Round of Growth:In recent years, the ophthalmology sector has garnered increasing attention, attracting numerous domestic manufacturers and fueling a robust trend in pharmaceutical and medical device innovation. In the medical device segment, Chinese brands such as Haohai Biological Technology, Aierbode (Aibo Medical), Shivi Imaging, 3N, and Shijing Medical have achieved breakthroughs in frontier technologies—including intraocular lenses, optical coherence tomography (OCT), orthokeratology lens care systems, and digital therapeutics—thereby breaking the monopoly previously held by foreign companies. In the pharmaceutical segment, industry leaders such as Hengrui Medicine, Xingqi Eye Pharmaceutical, Ocumension Therapeutics, and Extreme Vision have continuously overcome technical barriers through independent research and development, while also introducing advanced overseas products and technologies to serve the broader consumer base. In the service sector, innovations and upgrades in surgical techniques have significantly improved treatment outcomes. Overall, technological advancements have not only led to product upgrades but also enhanced consumers’ willingness to pay, resulting in simultaneous growth in both sales volume and pricing, thereby driving faster and more robust market development.

Domestic R&D foundations are relatively weak, and product homogenization is severe:For high-end ophthalmic devices, equipment, and innovative ophthalmic drugs, the technical barriers are substantial. Chinese manufacturers entered the market relatively late and face a severe shortage of talent in research and development, clinical trials, and sales. Consequently, there remains a significant gap between domestic and foreign companies in terms of technological accumulation. The ophthalmic pharmaceutical industry exhibits similar characteristics; currently, the mainstream pipelines of Chinese ophthalmic pharmaceutical companies are dominated by generic drugs and improved new drugs, with limited independent innovation. This has resulted in serious homogenization, failing to significantly narrow the gap between domestic and international ophthalmic drugs.

Domestic enterprises entered the market late, and foreign-funded companies still occupy the majority of the market:Foreign pharmaceutical companies account for approximately 60%–70% of China’s ophthalmic drug market, while foreign enterprises monopolize 80% of the market share for high-value ophthalmic consumables. In the field of ophthalmic medical equipment, foreign brands currently hold around 95% of the market. Although domestic companies have increasingly entered the ophthalmic market in recent years, their late start means that further time and accumulation are required to achieve initial breakthroughs.

Weak patient awareness in China, limited understanding among capital markets, and unclear regulations in frontier fields:Although the prevalence of ophthalmic diseases in China is significantly higher than in the United States, patient awareness regarding treatment remains relatively low, resulting in a substantial gap in diagnosis rates for major mainstream ophthalmic conditions compared to the U.S. Furthermore, while capital market attention toward the ophthalmology sector has gradually increased in recent years, overall understanding remains insufficient, particularly concerning the latent market potential driven by cutting-edge products. Finally, in more advanced fields such as cell therapy and gene therapy, the absence of domestic products has led to unclear regulatory and approval frameworks, posing certain challenges for pioneering enterprises.

To uncover the latest and most comprehensive innovation trends in the market, VCBeat. conducts a comprehensive analysis from three dimensions. First, weGlobal Leading Ophthalmic Enterprisesof innovation dynamics and the status of pipelines under development, providing a comprehensive review and analysis; secondly, we alsoHot Companies in Primary Market Investment and Financing...provided in-depth insights into the dynamics of ; finally, we also explored existing treatment options from the perspective of pathogenesisUnmet Needs, thereby identifying the most noteworthy innovations to watch in the ophthalmology industry.

Unmet Clinical Needs in Mainstream Diseases

Data Source: VCBeat

A Multi-Billion Dollar Market: Atropine Emerges as a Hotspot in Drug Development:Low-concentration atropine offers substantial market potential, making it a key focus for successive R&D efforts by major pharmaceutical companies. According to statistics, nine companies or institutions worldwide—including Jimu Biology, Zhaoko Ophthalmology, Xingqi Eye Medicine, and Ocumension Therapeutics—have entered Phase III clinical trials, positioning them to gain first-mover advantage in this market.

Orthokeratology Lenses Gain Favor from Capital; Intelligent Fitting May Accelerate Market Adoption:The fitting process for orthokeratology (OK) lenses is complex, and the high technical demands on clinicians have historically constrained the rapid development of the industry. In recent years, leading companies such as Johnson & Johnson, Haohai Biological Technology, and Autek China have introduced intelligent models for OK lens fitting and manufacturing, helping to streamline the fitting process for patients and enhance the precision of lens customization.

Digital Therapeutics Spark New Visions for the Future: Accumulating Evidence-Based Data Is Key to Market EntryPrior to 2021, the application of digital therapeutics in ophthalmology was primarily concentrated in the field of strabismus and amblyopia. This year, Shijing Medical launched its latest digital therapeutic product for myopia prevention and control, “Beibele.” By leveraging three core mechanisms—red light biostimulation therapy, accommodative function training, and visual function training—the product effectively helps children and adolescents slow the progression of myopia, creating new opportunities and options beyond the scope of traditional devices and pharmaceuticals. Currently, the continuous accumulation of evidence-based data, along with the establishment of expert consensus and clinical guidelines, remains a central challenge for digital therapeutic products in the field of myopia prevention and control.

A Dry Eye Disease Therapeutic Device Featuring a Novel Mechanism of Action for Customized Treatment:Global Leader in OphthalmologyAlcon’s recently launched Systane iLux2 MGD Thermal Pulse System enables physicians to customize MGD treatment for each patient within 8–12 minutes. It allows patients to view their meibomian glands and the treatment process via infrared imaging and high-definition video, with results experienced in as little as one week, thereby enhancing the credibility of treatment recommendations. Currently, most therapeutic approaches still fail to stimulate natural tear secretion. In contrast, Auright Medical has innovatively introduced a drug-free, handheld dry eye treatment device approved by the U.S. FDA. This device delivers external nasal nerve stimulation to promote natural tear secretion and improve meibomian gland secretory function.

Domestic Innovation Trends in Dry Eye Disease Drugs and Therapies Are Heating Up: New Mechanisms May Open Up New Markets:Since the launch of Xiidra, the first globally approved prescription eye drop for dry eye disease, in 2016, the R&D pipeline for dry eye treatments has continued to expand both domestically and internationally. In addition to efforts aimed at enhancing the activity and increasing the concentration of existing cyclosporine-based formulations, numerous small biotechnology companies are developing novel products with improved efficacy and safety profiles by targeting new pathways or mechanisms. For Chinese companies, innovation strategies are highly diversified, with most opting to accelerate product commercialization through license-in arrangements for overseas innovative therapies.

Domestic OCT Products See a Surge in Market Launches, with OCTA Emerging as a Major Development Trend:As a significant expansion of functional OCT imaging, OCTA products play a crucial role in enabling physicians to observe retinal and choroidal vascular structures and blood flow information, thereby facilitating the understanding and exploration of disease mechanisms. Consequently, they are gradually becoming a major trend in the OCT market. Although eight domestic companies have successfully registered and launched such products, most still lag significantly behind their international counterparts. In the future, beyond further improvements in technical parameters (such as scanning speed, scanning depth, image quality, and algorithms), the next generation of OCT products—exemplified by Visioncare’s newly released “Ruyi Whole-Eye OCT”—will represent the primary trend in the OCTA industry. These systems organically integrate modules for anterior and posterior segment structural OCT, anterior and posterior segment blood flow OCT, and visualized swept-source axial length measurement, achieving “multi-functionality in a single device.”

AI-empowered refractive surgery devices enable more precise, intelligent, and personalized surgical planning:Refractive surgery has evolved over many years. In recent years, the integration of AI technology into procedures such as femtosecond laser-assisted surgery and Implantable Collamer Lens (ICL) implantation has propelled refractive surgery to a new level. Alcon has innovatively launched its AI-powered Customized Micro-Femtosecond technology, which employs the latest Phorcides surgical planning method combined with AI to assist clinicians in designing more precise, intelligent, and personalized preoperative surgical plans, thereby enabling patients to achieve clearer and more comfortable visual outcomes. Meanwhile, the Chinese company Airdoc has also explored the application of AI technology in ICL surgery, with studies demonstrating the role of artificial intelligence algorithms in assisting with the prediction of postoperative vault height and the determination of intraocular lens prescriptions.

Cell and Gene Therapy Gains Momentum, with Ophthalmology as a Key Breakthrough Area:Among the six gene therapy products currently marketed worldwide, one is indicated for ophthalmic conditions. Of the 46 gene therapy products in Phase III clinical trials or pending approval globally, 14 are for ophthalmic indications. According to current statistics from VCBeat Institute, there are 40 gene therapy drugs and six cell therapy investigational products under development worldwide, with participating companies including leading global ophthalmic enterprises and innovative firms. Retinal diseases, such as retinitis pigmentosa and age-related macular degeneration, represent the primary indications for gene therapy; additionally, glaucoma and optic nerve disorders are areas where gene therapies await breakthroughs. In contrast, the main indications for cell therapy are corneal diseases and retinal disorders.

Innovations in Drug Administration Enhance the Safety and Efficacy of Drug Delivery:For anterior segment diseases, therapeutic agents can exert their effects directly through the cornea, conjunctival epithelium, or the blood-aqueous barrier. In contrast, posterior segment diseases typically require invasive treatments such as intravitreal injections or subconjunctival injections. As previously analyzed, eye drops remain the predominant dosage form in clinical practice for treating ocular diseases; however, their bioavailability is generally below 5%. Injection-based approaches, on the other hand, carry significant risks, including vitreous hemorrhage and retinal detachment. Therefore, researching novel drug delivery methods and dosage forms is critical to the advancement of ophthalmology. Currently, there is a substantial number of domestic and international patent applications related to drug dosage forms, primarily focusing on nanodrug delivery systems and in situ gel drug-loading systems. These novel dosage forms often simplify preparation processes, reduce costs, minimize ocular irritation, accelerate absorption, prolong retention time, and enhance bioavailability. Domestic companies, such as Kening Biotech, have independently developed innovative dosage forms like the elaSS® ocular surface drug delivery system and the DynaMC® long-acting sustained-release system for fundus protein drugs. In addition to new dosage forms, many ophthalmic companies are actively developing innovative devices or drug-device combinations to improve the precision, safety, and intelligence of traditional drug administration methods. Companies involved in these efforts include Roche, Bausch + Lomb, Jimo Bio, and Huashi Nuowei.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:Scan the QR code to download the full report for free.

Chapter 1 Industry Overview: A Multi-Billion Market, a Golden Track with Immense Potential

1.1 Atlas of Ophthalmic Diseases: Large Patient Population and High Incidence Rate

1.2 Global Market for Ophthalmology: Steady Growth and High Concentration

1.3 Domestic Ophthalmology Market: A RMB 210 Billion Market with Capital Flocking to Pharmaceuticals and Medical Devices

Part II: Sector Scan—The Trinity of “Devices + Services + Pharmaceuticals”

2.1 Medical Devices: Diverse Product Types, Accelerated Domestic Substitution of High-Value Consumables

2.2 Pharmaceuticals: Continuous Innovation in Drug Administration and Treatment Methods Brings New Opportunities

2.3 Services: Private ophthalmology emerges as a future growth driver, with pronounced leader effects

Part III: Opportunities and Challenges in Industry Development: Domestic Substitution, Winning Through Innovation

3.1 Drivers – Policy Support, Vast Potential Patient Population, and Technological Innovation

3.2 Obstacles – Weak Foundations, Technological Gaps, and Low Localization Rate

Part IV Case Studies of Representative Innovative Enterprises

Part V: Assessment of Future Trends in the Ophthalmology Industry

5.1 Myopia Prevention and Control Poised to Become a Super Blue Ocean

5.2 Emerging Hotspots in Innovative Dry Eye Treatments

5.3 Technological Innovation in High-End Medical Equipment

5.4 Surging Interest in Cell and Gene Therapies and Innovative Drug Delivery Methods

This report is part of the series for VCBeat’s 6th Future Healthcare Top 100 Conference, which will be held online from June 14 to 18, 2022. The report will be presented and released at the conference.