2022 Gene Therapy Industry Report: Curing Rare Diseases at the Genetic Root and Overcoming Technical & Manufacturing Challenges

As domestically produced products successively enter clinical stages, the notion that China’s gene therapy industry can “overtake on a bend” is no longer an empty promise. Influenced by advances in gene editing and delivery technologies, the gene therapy sector has diverged into several distinct tracks, with application scenarios no longer limited to monogenic hereditary diseases. In this process of rapid industrial iteration, identifying the key development factors and clarifying the underlying logic of industry growth are critical to strategic formulation.

Based on this, VCBeat has compiled the “2022 Gene Therapy Industry Report,” which will focus on addressing the following questions:

1. What are the trends in investment and financing, as well as market size development, in the gene therapy industry?

2. What is the level of maturity in the development of key technologies?

3. What is the development pace of the supporting CDMO industry? Is it sufficient to meet the current development needs of the industry?

4. How will future industries address challenges in technology, production, and commercialization?

5. What are the most noteworthy innovation trends in the gene therapy industry at present?

To clarify the aforementioned issues, VCBeat Research Institute conducted extensive industry-wide research and, in conjunction with its own research findings, seeks toIndustry Overview, Technological Pathways, Development Opportunities and Challenges, and Future Trend Analysis...and other dimensions to comprehensively analyze the gene therapy industry, aiming to provide valuable industry insights for stakeholders and participants.

(Note: The full report is available at(Scan the QR code at the end of the article to download)

Gene Therapy: A Root-Cause Cure with Broad Prospects

1Gene Therapy: Curative at the Root, Offering Both Clinical and R&D Advantages

Gene Therapy Offers Curative Potential from the Root, Driving Strong Unmet Need

Gene Therapy: A Cure at the Root.Gene therapy is a fundamental therapeutic strategy that precisely targets the root cause of disease—aberrant DNA. It typically involves introducing normal target genes into human target cells or knocking out abnormal genes.

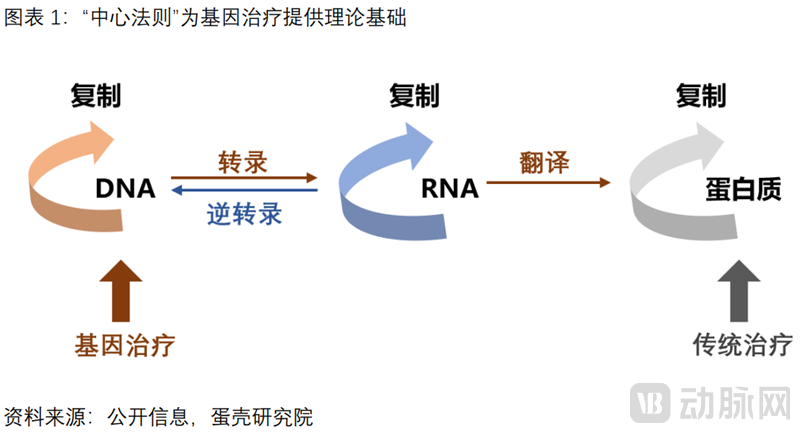

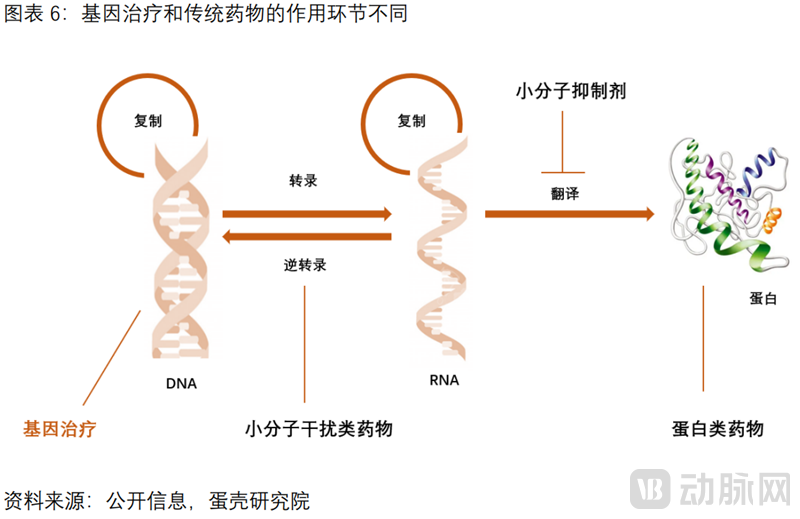

"The Central Dogma" provides the theoretical foundation for gene therapy.Central Dogma: Genetic information is transmitted along the “DNA–RNA–protein” pathway, and diseases often manifest as abnormalities at the protein level. Traditional therapies target proteins, whereas gene therapy addresses the root source of protein synthesis—DNA. By modulating DNA to alter the flow of genetic information, gene therapy changes protein phenotypes, thereby achieving fundamental disease treatment.

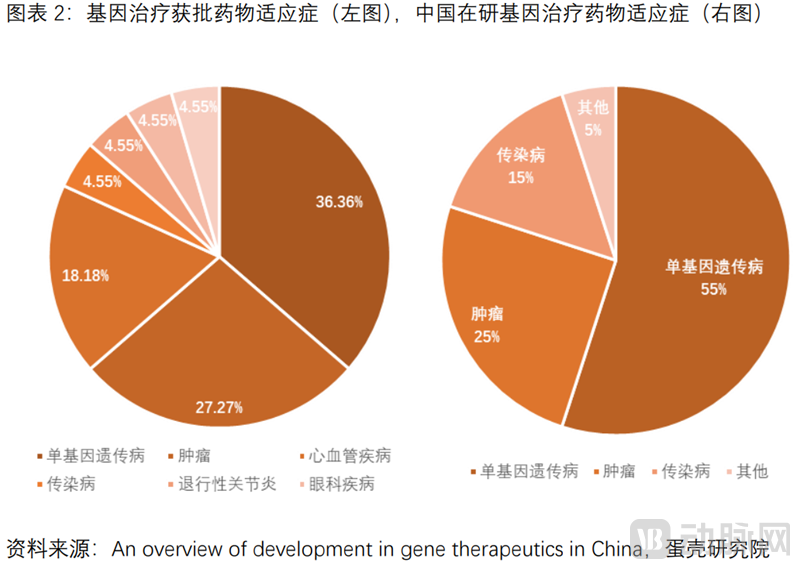

There is a strong imperative for gene therapy, with indications primarily focused on monogenic inherited diseases (rare diseases). These conditions have clearly identified pathogenic genes and lack effective treatments, resulting in significant unmet clinical needs.The vast majority of rare diseases are caused by genetic abnormalities, with more than 7,000 types identified and a total affected population of 350 million. However, over 90% of rare diseases lack effective treatments. The indications primarily focus on rare diseases, including inherited eye disorders, hemophilia, thalassemia, and motor neuron diseases.

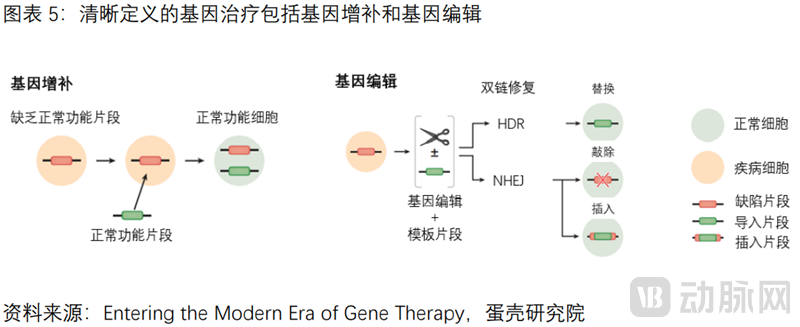

Gene therapy encompasses two technical approaches: gene augmentation and gene editing.

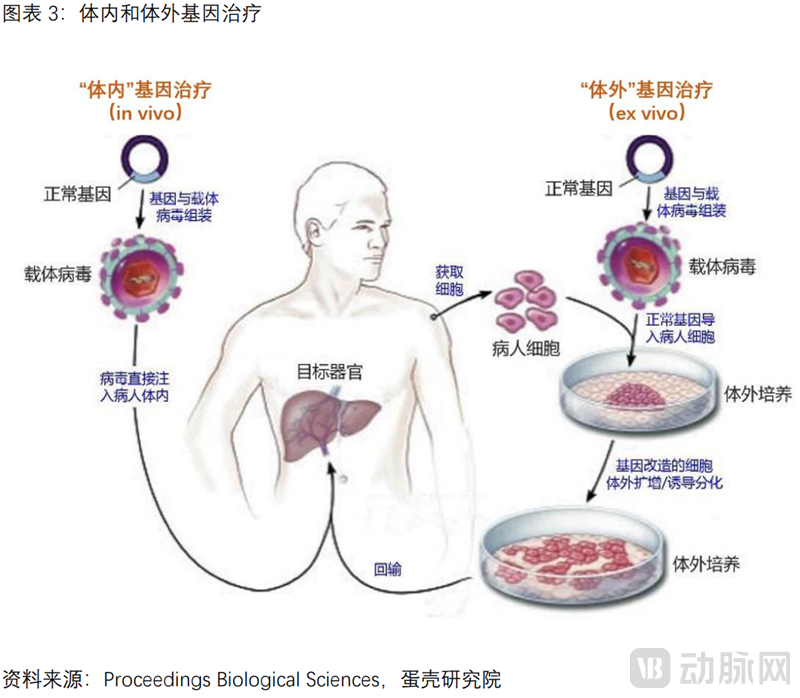

Based on the route of administration, gene therapy can be classified into two categories: in vivo gene therapy and ex vivo gene therapy.“In vivo” gene therapy involves a relatively straightforward procedure, in which recombinant vectors carrying therapeutic genes are directly delivered into the patient’s body. “Ex vivo” gene therapy additionally entails genetic modification of cells (autologous hematopoietic stem cells) outside the body, including cell isolation, transfection, expansion and culture, and reinfusion.

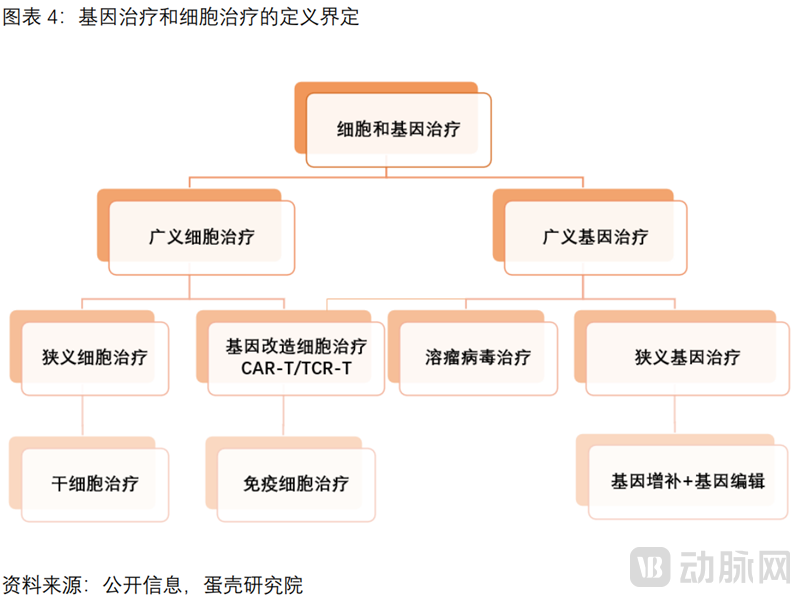

This report clearly defines gene therapy as interventions conducted at the DNA level. It primarily encompasses two major technical approaches: gene augmentation and gene editing; it excludes immunotherapies such as CAR-T, oncolytic viruses, and small nucleic acid drugs.

(1)Gene Augmentation: By utilizing delivery vectors, exogenous genes are introduced into diseased cells, and their expression products can modify the function of defective cells or enhance existing functions. Gene augmentation is currently the predominant technical approach among gene therapy products that have received marketing approval or are in clinical development.

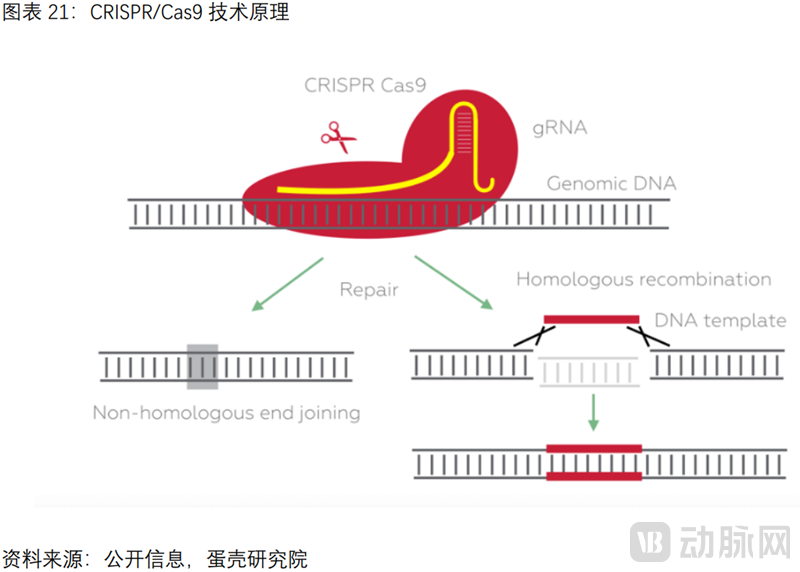

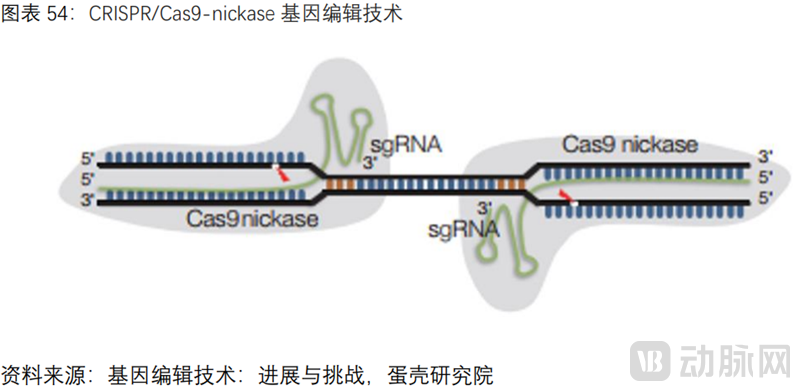

(2)Gene Editing: Precisely modify specific target genes to disrupt deleterious genes or repair mutated genes, including ZFNs, TALENs, and the CRISPR/Cas9 technology, which was awarded the Nobel Prize in Chemistry in 2020. Taking CRISPR/Cas9 as an example, the Cas9 protein, guided by sgRNA through base-pair complementarity, reaches different target sites and cleaves the target gene, enabling precise, site-specific editing of the target gene. This allows for the alteration and correction of “erroneous” genes within the patient’s original genome. The clinical translation of gene-editing systems is still in its early stages, and no products have been commercially launched to date.

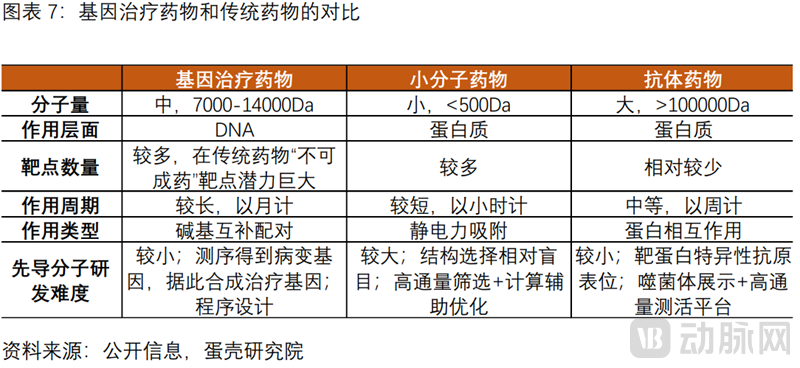

Compared with traditional drugs, gene therapy offers both clinical and R&D advantages.

The clinical advantages of gene therapy are reflected in its direct intervention at the DNA level, thereby circumventing the challenge posed by “undruggable” targets at the protein level that traditional drugs face.Currently, the majority of drugs target proteins, such as small-molecule targeted therapies and large-molecule monoclonal antibodies used in oncology. Gene therapy directly corrects disease-causing genes at the DNA level, bypassing the druggability challenges associated with traditional pharmaceuticals. It offers unique clinical advantages for diseases with well-defined genetic etiologies where protein-level targeting is difficult to achieve pharmacologically.

The R&D advantages of gene therapy are reflected in the lower difficulty of synthesizing nucleic acid sequences compared to traditional drugs.Three Common Steps in Gene Therapy: Design and Synthesis of Nucleic Acid Sequences, Delivery of Target Sequences to Target Cells, and Industrial-Scale Manufacturing. Among these, the design and synthesis of nucleic acid sequences are less challenging than those for small-molecule targeted drugs and monoclonal antibodies. Therefore, once a safe and efficient delivery method is developed, the overall development difficulty for gene therapy products is actually reduced.

2Moving Forward Amidst Twists and Turns: The Future of Gene Therapy Is Here

According to VCBeat’s compilation and analysis, the development of gene therapy can be divided into four stages: initial exploration, fervent growth, tortuous progress, and renewed prosperity. The landmark events of each period are listed below.

In 1963, American molecular biologist and Nobel laureate in Physiology or Medicine Joshua LederbergFirst Proposed the Concept of “Gene Exchange and Gene Optimization”, marking the starting point of gene therapy.

In 1970, American physician Stanfield Rogers attempted to treat two sisters for argininemia by injecting papillomavirus containing arginase, which wasThe First Human Trial Ended in Failure.

In 1990, Dr. William French Anderson, known as the "Father of Gene Therapy," led the launch ofWorld's First CaseGene Therapy for Severe Combined Immunodeficiency: The Patient Is a 4-Year-Old Girl from the United States. Following Treatment, Her Body’s Ability to Produce Adenosine Deaminase Improved, Leading to Alleviation of Her Condition.The patient is currently still alive.

In 1996,Invention of ZFN Gene Editing Technology.

In 1999, American boy Jesse Gelsinger participated in a gene therapy project at the University of Pennsylvania. Four days after receiving treatment, he died due to a virus-inducedDeath from Multi-Organ Failure Due to Severe Immune Response. This event marked a turning point in the development of gene therapy.

2003,FDA Temporarily Suspends All Uses of Retrovirusesclinical trials to modify the genes of hematopoietic stem cells, but after three months of rigorous review and deliberation, gene therapy clinical trials were permitted to resume.

2011,Invention of TALEN Gene Editing Technology.

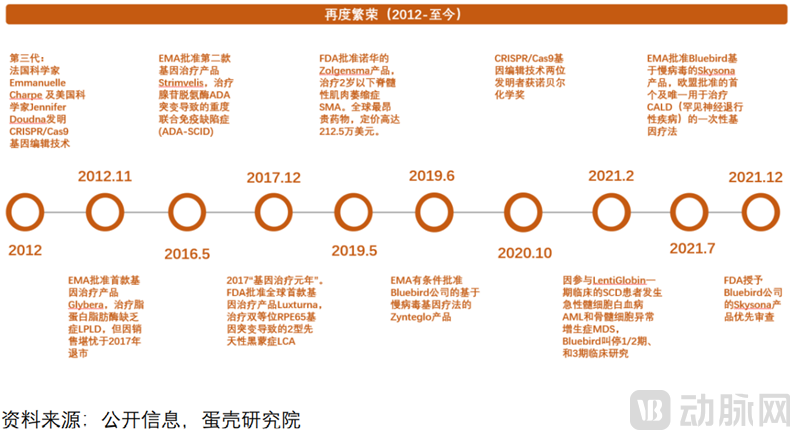

In 2012, American scientist Jennifer Doudna and French scientist Emmanuelle Charpentier invented the CRISPR/Cas9 gene-editing technology, a revolutionary milestone in the field of gene therapy.

In December 2017, the FDA approved Luxturna, the world’s first gene therapy product., for the treatment of Leber congenital amaurosis type 2 (LCA) caused by biallelic RPE65 gene mutations.2017 Was Dubbed the “Year One” of Gene Therapy。

In October 2020, the inventors of CRISPR/Cas9 gene-editing technology were awarded the Nobel Prize in Chemistry.French microbiologist Dr. Emmanuelle Charpentier and U.S. National Academy of Sciences member Dr. Jennifer A. Doudna were awarded the 2020 Nobel Prize in Chemistry. These two female scientists jointly discovered the cleavage function of Cas9 and the targeting role of crRNA, and demonstrated that crRNA and tracrRNA can be fused into a single-guide RNA (sgRNA).

3Policy Support, Capital Frenzy, and the Promising Prospects of Gene Therapy

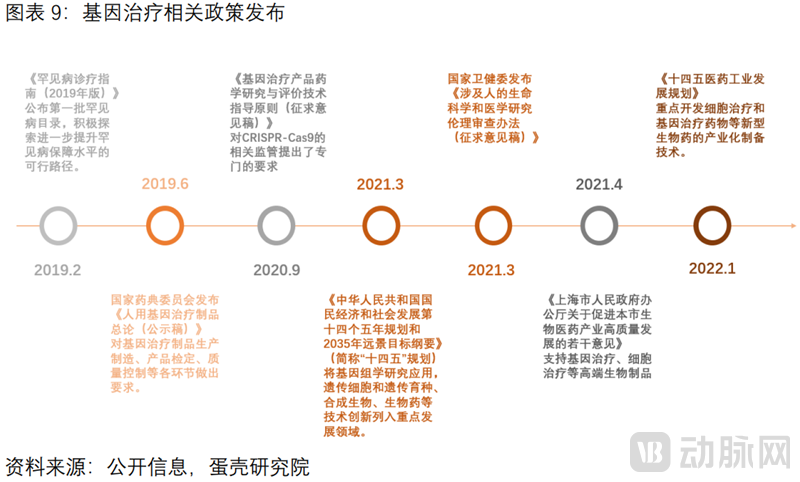

Policy Support Promotes the Healthy Development of the Gene Therapy Sector.Whether it is the inclusion of genomics research as a key development area in the 14th Five-Year Plan, policy incentives for rare diseases driving diagnosis and treatment, or regulatory requirements specifying standards for gene-editing tools such as CRISPR-Cas9, these factors have made the trajectory of gene therapy development more predictable.

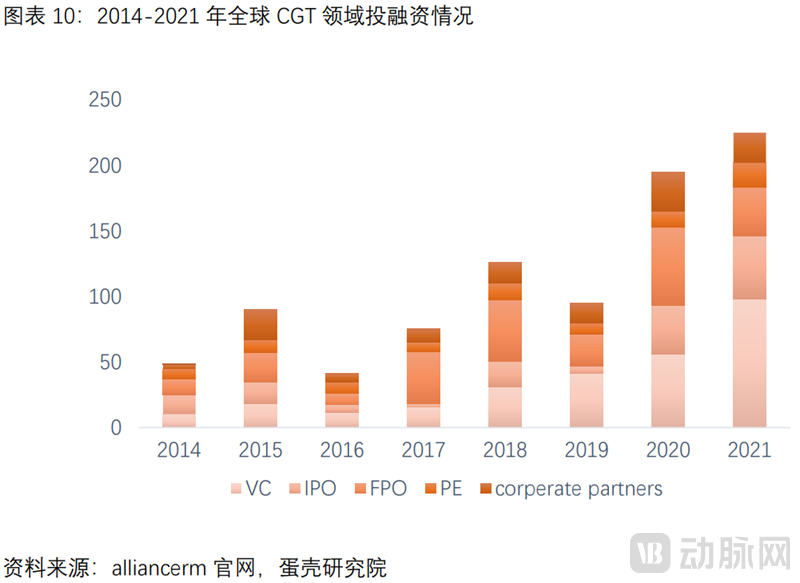

Global Financing and Investment in Cell and Gene Therapy Are Booming.Since the FDA’s approval of Luxturna, Kymriah, and Yescarta in 2017, the rapid development of the cell and gene therapy (CGT) industry has attracted substantial capital inflows. According to data disclosed by AllianceRM, global investment and financing in the CGT sector surged from approximately $5 billion in 2014 to around $23 billion in 2021.

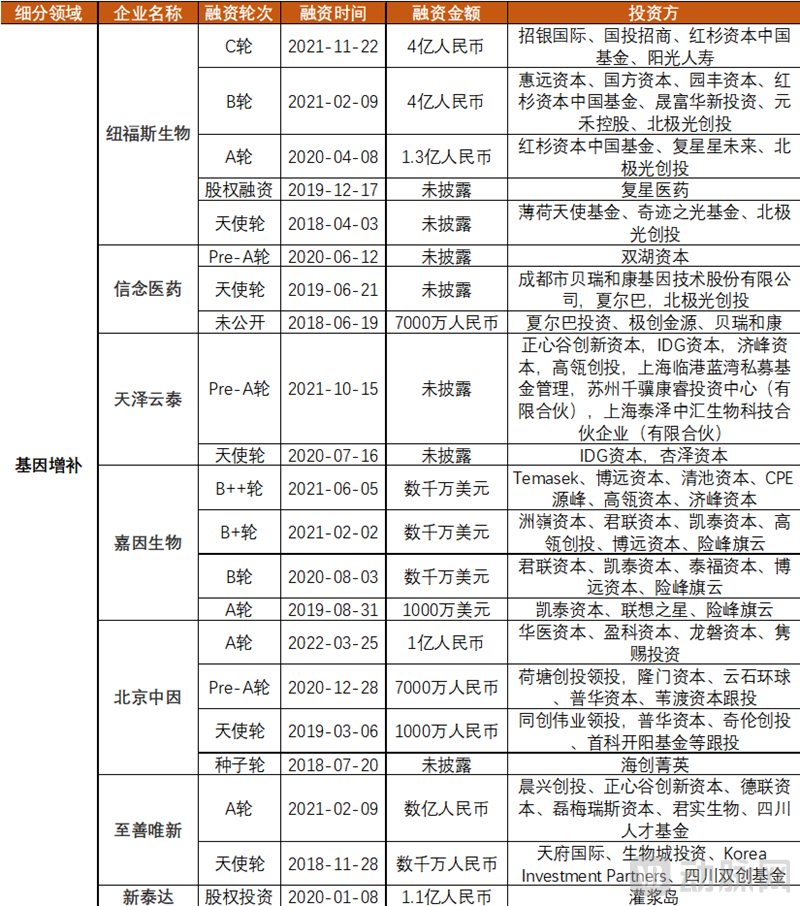

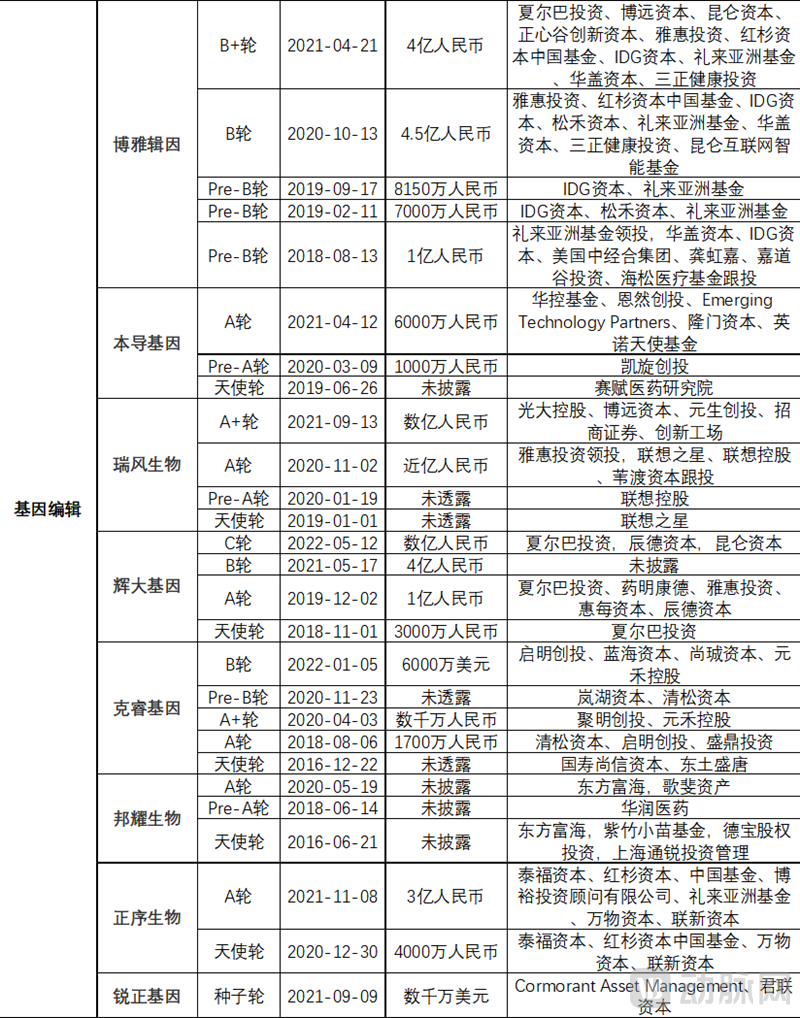

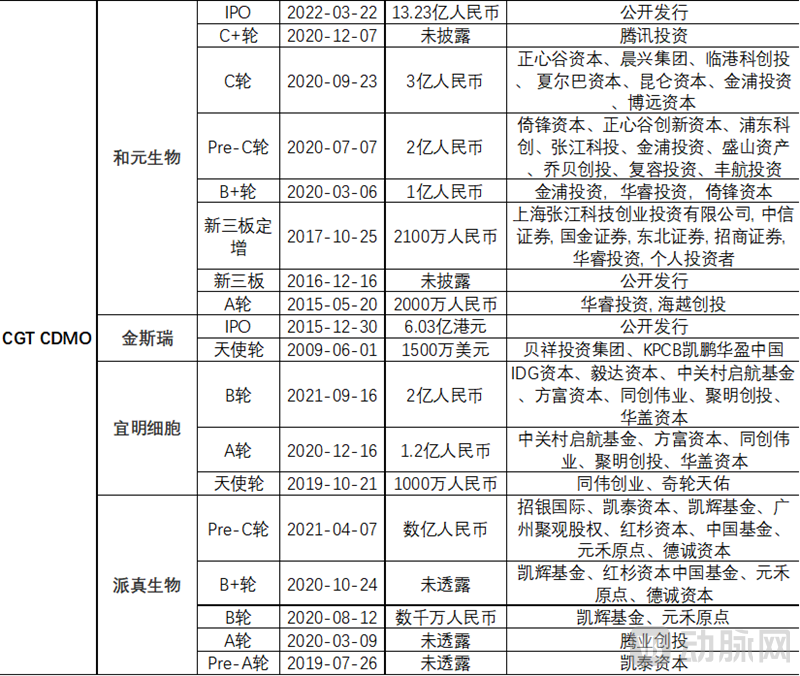

Multiple Domestic Gene Therapy Companies Secure Frequent Funding Rounds, Boosting Innovative Development.Whether in the field of gene augmentation for genetic therapy drug development or gene editing, multiple companies have secured substantial financing in recent years. For instance, Nuofu Biopharma, Hangzhou Jiayin Biotechnology, Zhishan Weixin, Boya Jiyin, Ruifeng Biotech, Huida Gene, Zhengxu Bio, and Ruizheng Gene each raised hundreds of millions of yuan in a single funding round. Meanwhile, companies providing CDMO services for CGT have also frequently secured financing; examples include Heyuan Biotech, which listed on the STAR Market on March 22, 2022, as well as GenScript, Yiming Cell Therapy, and Paizhen Biotech, all of which raised hundreds of millions of yuan in individual rounds.

Sources: Artery Orange Database, public information, VCBeat Research Institute

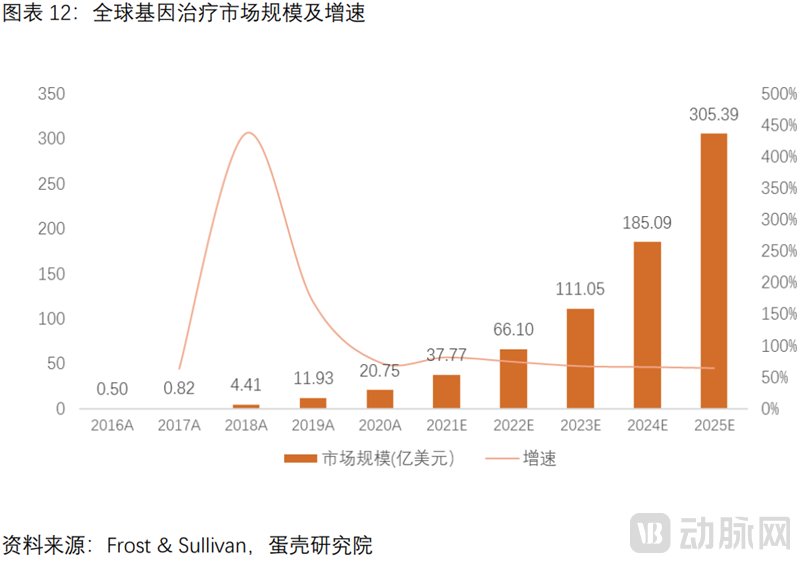

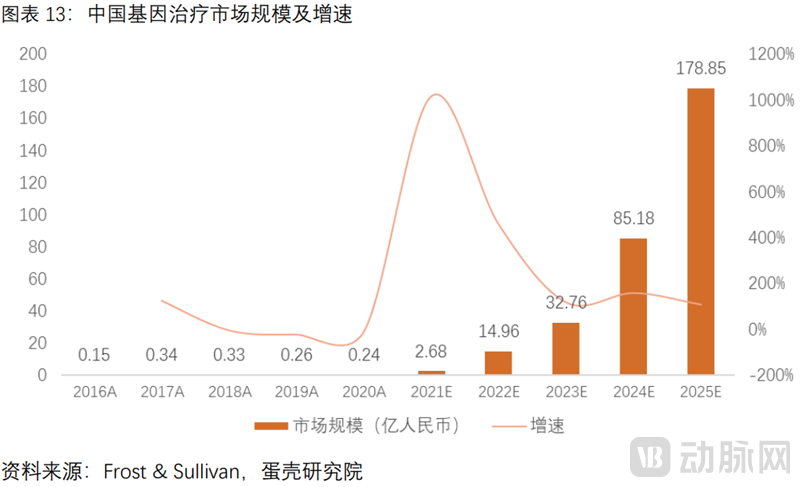

Gene Therapy Is Rapidly Advancing with Broad Prospects.The global and Chinese markets are projected to reach $30.54 billion and RMB 17.89 billion, respectively, in 2025, with CAGRs of 71.2% and 276.0% from 2020 to 2025.

Gene Therapy Effectively Cures Rare Diseases: Viral Vectors Are the Key to Gene Therapy

1Two Major Technical Pathways: Gene Augmentation Is Relatively Mature, While Gene Editing Offers “Powerful Functionality” and “Targeted Precision”

Gene augmentation therapy is relatively mature, with several products already on the market.

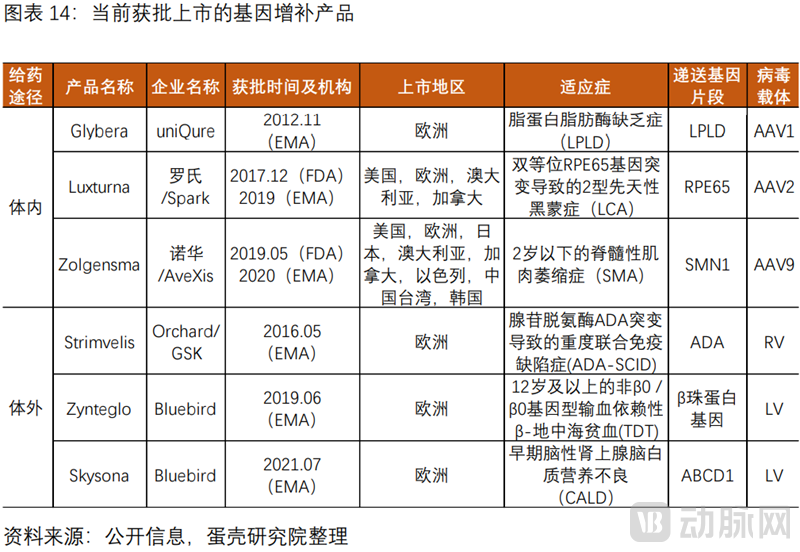

Gene augmentation therapy is relatively mature. From 2012 to 2021, the FDA approved two products, and the EMA approved an additional four, with indications concentrated in the field of rare diseases.

The FDA has approved two products, both of which are AAV vector-based in vivo therapies.Luxturna, approved for Spark in 2017, treats Leber congenital amaurosis type 2 (LCA2) caused by biallelic RPE65 gene mutations; and Zolgensma, approved in 2019, treats spinal muscular atrophy (SMA) in children under two years of age.

The EMA additionally approved four products.In 2012, the EMA approved uniQure’s Glybera, an AAV vector-based therapy for lipoprotein lipase deficiency (LPLD), marking the first such approval. However, due to poor sales, it was withdrawn from the market in October 2017. In 2016, the EMA approved the second product, GSK’s Strimvelis, an RV vector-based therapy for severe combined immunodeficiency caused by adenosine deaminase deficiency (ADA-SCID). In April 2018, GSK sold Strimvelis to Orchard Therapeutics; only five patients received treatment. In 2019 and 2021, the EMA successively approved Bluebird Bio’s LV vector-based therapies Zynteglo and Skysona, for transfusion-dependent β-thalassemia (TDT) in patients aged 12 years and older with non-β0/β0 genotypes, and early cerebral adrenoleukodystrophy (CALD), respectively.

(1) The gene augmentation therapy pipeline is robust, with numerous overseas products having entered the pre-marketing/marketing application or late-stage clinical phases.

The overseas pipeline of gene augmentation products is robust.According to VCBeat’s compilation, three products are poised for imminent market launch in 2022, six are preparing to submit Biologics License Applications (BLAs), and more than a dozen candidates have entered Phase III clinical trials.A review of overseas gene augmentation pipelines reveals that most products are in vivo gene therapies based on AAV vectors, while ex vivo therapies predominantly utilize LV vectors.Including two pending products from Bluebird Bio, beti-cel and eli-cel, with PDUFA target dates of August 19, 2022, and September 16, 2022, respectively. Beti-cel has currently received FDA Priority Review designation. If approved by the FDA, it is expected to become the first lentiviral vector gene therapy for patients with β-thalassemia in the United States. Previously, the FDA granted Instiladrin Fast Track designation, Breakthrough Therapy designation, and Priority Review designation, and accepted its Biologics License Application (BLA). If approved in 2022, this therapy would provide a promising option for patients with non-muscle-invasive bladder cancer (NMIBC) who are unresponsive to BCG. The product OTL-103 has been granted Orphan Drug designation and Rare Pediatric Disease (RPD) designation by the FDA. Etranacogene dezaparvovec has the potential to be the first gene therapy to provide durable, functional therapeutic benefits for patients with hemophilia B. BMN 270 has received Orphan Drug designation from both the FDA and the EMA for the treatment of severe hemophilia A.

(2) The overall progress of domestic gene augmentation pipelines is relatively slow, with indications concentrated on ophthalmic genetic diseases and hemophilia.

The overall progress of domestic gene augmentation pipelines is relatively slow, with most candidates in Phase I clinical trials; indications are primarily focused on ophthalmic genetic disorders and hemophilia.The pipelines with faster progress include NR082 (NFS-01) from Nuofus Biologics, BBM-H901 from Belief Medicine, LX101 from Langxin Biologics, VGB-R04 from Tianze Yuntai, EXG001-307 from Hangzhou Jiayin Biologics, and ZVS101e from Beijing Zhongyin.

A review of the domestic pipeline for gene augmentation therapies reveals that most products are administered via in vivo routes and rely on adeno-associated virus (AAV) vectors; only Bendao Gene has relevant candidates based on a lentiviral vector (LV) platform.Several domestic R&D pharmaceutical companies have received Orphan Drug Designation (ODD) from the FDA for their pipelines, including NuFores Biotech’s NR082 (NFS-01), Tianze Yuntai’s VGB-R04, and Beijing Zhongyin’s ZVS101e.

Gene Editing Technology: Precise Targeting and Powerful Functionality

Gene editing is “powerful” and “precisely targeted,” with CRISPR, the 2020 Nobel Prize winner, leading a revolutionary breakthrough.

“Powerful”: Gene editing can achieve "gene knockout" (via non-homologous end joining, NHEJ) and "gene insertion" (via homology-directed repair, HDR). In contrast, gene augmentation therapy can only mediate "gene insertion." "Targeted Precision": The CRISPR/Cas9 system precisely targets the gene of interest through base-pairing complementarity between the sgRNA and the target DNA. Meanwhile, gene augmentation therapy typically employs adeno-associated virus (AAV) or lentivirus (LV) for delivery; AAV does not integrate into the host genome, posing challenges regarding durability, whereas LV integrates randomly into the genome, carrying a risk of oncogenesis.

The core advantage of CRISPR/Cas9 lies in its targeting mechanism; since sgRNA is easier to synthesize than proteins, it offers the benefits of high efficiency, convenience, and low cost.CRISPR/Cas9 is currently the most widely used gene-editing tool, based on the adaptive immune system of bacteria that defends against viral invasion. In October 2020, the inventors of CRISPR/Cas9 gene editing were awarded the Nobel Prize in Chemistry.

(1) The overseas gene-editing pipeline is essentially dominated by the “Big Three”

The overseas pipelines for gene editing are essentially dominated by the “big three,” with CTX001, the most advanced CRISPR-based candidate, expected to submit a Biologics License Application (BLA) by the end of 2022.The R&D pipeline is focused on CRISPR/Cas9. The three inventors—Emmanuelle Charpentier, Jennifer Doudna, and Professor Feng Zhang—founded globally leading gene-editing companies: CRISPR Therapeutics, Intellia Therapeutics, and Editas Medicine, respectively. In China, the overall gene-editing pipeline remains in the early stages of clinical development.

CTX001, a CRISPR-based therapy, is the most advanced ex vivo gene-editing treatment globally.The BLA is scheduled for submission by the end of 2022 for the treatment of transfusion-dependent β-thalassemia (TDT) and sickle cell disease (SCD). It has been granted Regenerative Medicine Advanced Therapy (RMAT) designation, Fast Track Designation (FTD), and Orphan Drug Designation (ODD) by the U.S. FDA, as well as ODD by the European Commission.Latest Developments: As of March 30, 2021, all 15 patients with transfusion-dependent thalassemia (TDT) were transfusion-independent, and none of the 7 patients with sickle cell disease (SCD) experienced vaso-occlusive crises (VOCs).

Intellia’s NTLA-2001 is an innovative in vivo gene editing therapy.Utilizes lipid nanoparticles (LNPs) to deliver all-nucleic acid gene-editing therapeutics (Cas9 mRNA + sgRNA) for the treatment of hereditary transthyretin-mediated amyloidosis with polyneuropathy (ATTRv-PN). In October 2021, the U.S. Food and Drug Administration (FDA) granted Orphan Drug Designation (ODD).Latest Updates: As of March 1, 2022, serum TTR levels in 15 patients showed a dose-dependent reduction, with no serious adverse events reported.

Editas’ AGN-151587 (EDIT-101) is the world’s first in vivo gene editing therapy.Treatment for Leber Congenital Amaurosis Type 10 (LCA10).Early Clinical Outcomes: Only confirmed safety, with suboptimal outcomes in disease improvement.

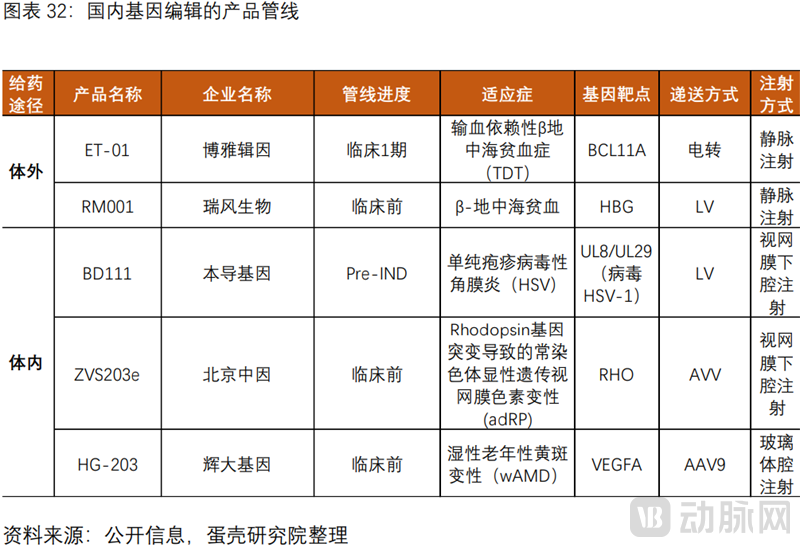

(2) The overall pipeline of gene editing in China remains in the early clinical stages.

Domestic gene editing pipelines remain largely in the early stages of clinical development.The most advanced candidate is Boya Ji Yin’s ex vivo therapy ET-01, which is in Phase I clinical trials. Other ex vivo therapies include BRL101 from Bangyao Biotechnology and RM001 from Ruifeng Biotechnology. In vivo therapies include BD111 from Bendao Gene, ZVS203e from Beijing Zhongyin, HG-203 from Huida Gene, and relevant pipelines from Ruizheng Gene.

2Viral vectors are the key to gene therapy, with AAV being the most widely used due to its safety advantages.

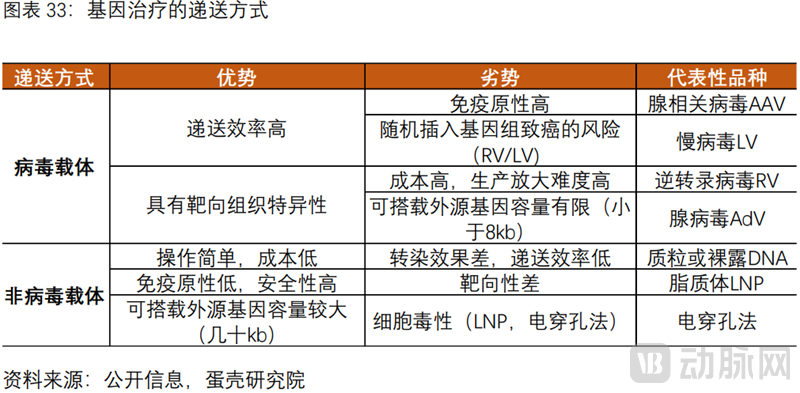

A core aspect of gene therapy is the delivery method, and an ideal delivery method must possess multiple key attributes.First, it can eliminate the ability to replicate its own vector, possessingHigh transduction efficiency; capable of targeting specific cells, and can stably express the transgene over the long term; possessesLower Immunogenicity, does not cause inflammation.

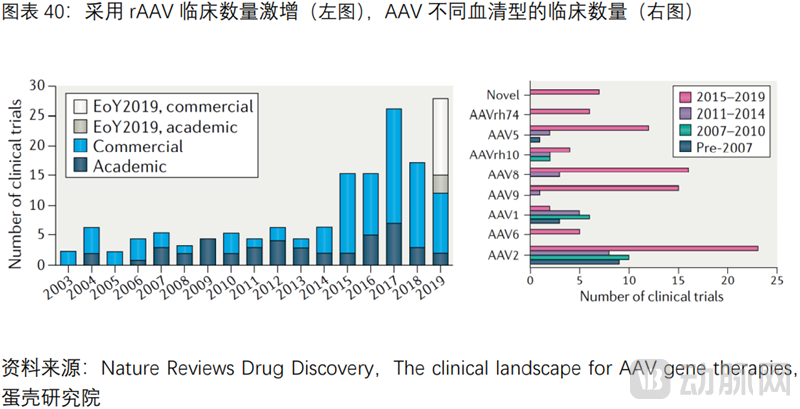

Currently Widely Used Delivery Methods: Viral Vectors Engineered to Lose Pathogenicity, with Their Key Advantage Being High Natural Transduction Efficiency.According to the ASGCT, 89% of CGT projects under development utilize viral vectors for delivery.

Common Viral Vectors: Retroviral vector RV, lentiviral vector LV, adeno-associated viral vector AAV, and adenoviral vector AdV.

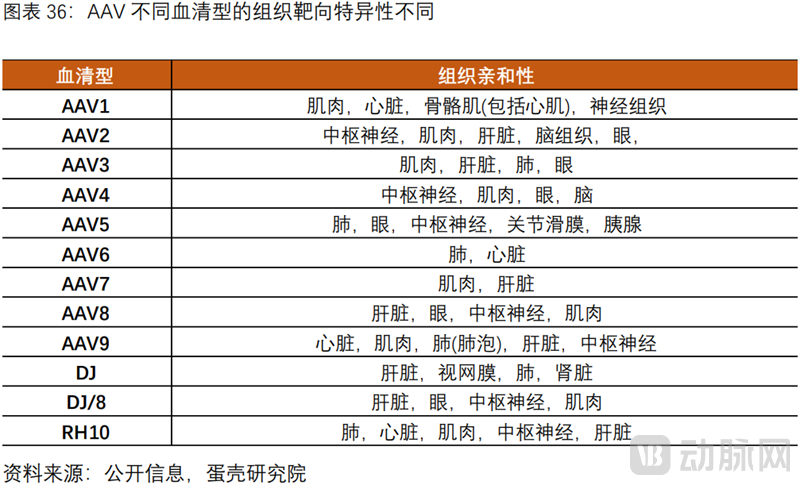

Core Advantages Driving the Widespread Application of AAV: Currently the safest viral vector, with low immunogenicity and non-pathogenic; it does not integrate into the host genome, thereby avoiding oncogenic risk, and natural AAV serotypes provide tissue-specific targeting.

CGT CDMOs Address Bottlenecks in Large-Scale Viral Vector Production, Accelerating Commercialization

1Upstream of the gene therapy industry chain is dominated by viral vector production, which is central to the commercialization of gene therapy.

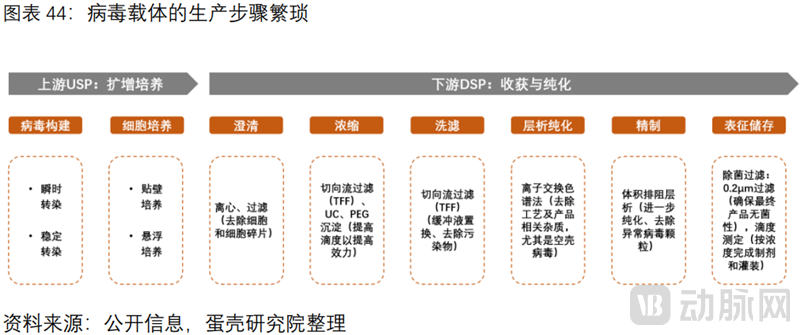

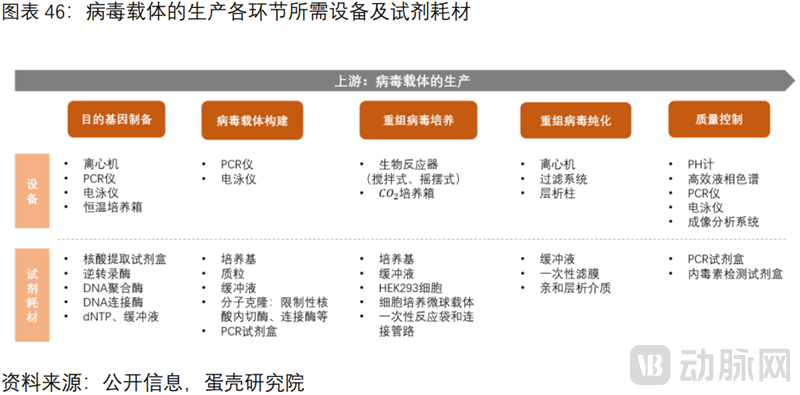

The gene therapy industry chain can be divided into upstream, midstream, and downstream segments.Upstream consists of viral vector manufacturers. The production process for viral vectors includes steps such as target gene preparation, viral vector construction, recombinant virus culture, recombinant virus purification, and quality control, each involving various equipment, reagents, and consumables. Midstream comprises gene therapy pharmaceutical companies, including those focused on gene augmentation and gene editing therapies. Downstream are patients with various rare or genetic diseases, including Leber congenital amaurosis type 2 (LCA), spinal muscular atrophy (SMA), transfusion-dependent β-thalassemia (TDT), hemophilia A/B, and inherited retinal dystrophies.

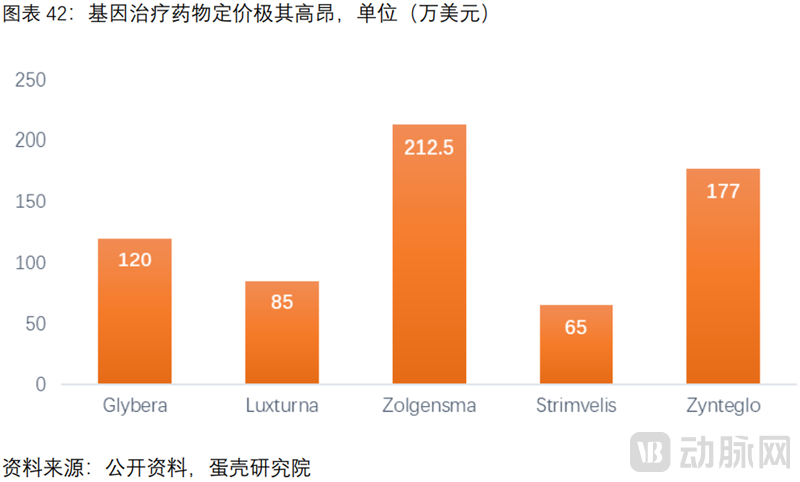

The commercial pricing of gene therapy products is generally extremely high.。“The World’s Most Expensive Drug,” Zolgensma, is priced at a staggering $2.125 million (equivalent to RMB 14 million). The average treatment cost for several other products also exceeds $1 million.

High pricing hinders commercialization.Glybera and Strimvelis, two gene therapy products approved by the EMA in 2012 and 2016 respectively, were both withdrawn from the market due to poor commercial performance: Glybera was forced off the market in 2017, and Strimvelis was sold by GSK in 2018.

Controlling the production cost of viral vectors is key to the reasonable pricing of end products.

(1) Viral vectors account for one-third of the cost: According to The New York Times, one-third of the R&D costs for gene therapies are allocated to the upstream production and preparation of viral vectors; reducing the production costs of viral vectors can effectively control end-product pricing.

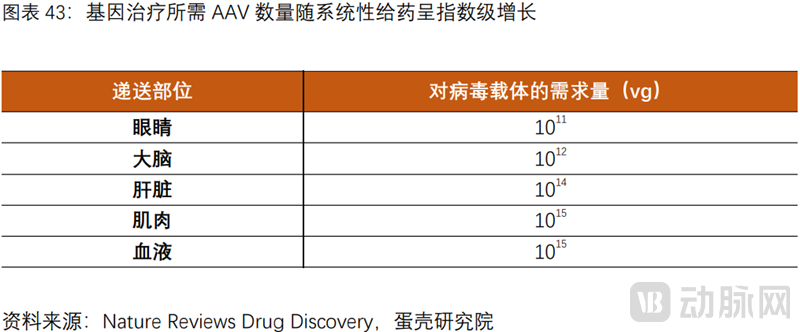

(2) The expansion of administration routes has led to an exponential increase in demand for carriers, resulting in a significant rise in end-user pricing.: Luxturna, administered via subretinal injection, is priced at $850,000, whereas Zolgensma, delivered through systemic intravenous infusion, costs as much as $2.12 million. This disparity arises because the quantity of viral vectors required per patient increases exponentially as the route of administration expands from localized ocular injection to the brain, then to muscle tissue, and ultimately to systemic circulation.

2The scaled production of viral vectors faces numerous barriers, resulting in an extreme shortage of manufacturing capacity.

Viral vector production involves multiple processes and is procedurally complex.Upstream: viral vector construction and cell expansion culture; downstream: multiple processes including cell lysis, clarification, concentration, chromatographic purification, and polishing.

(1) The production of viral vectors faces numerous process-related and talent-related barriers.Upstream challenges: how to reduce the amount of plasmid required for transient transfection; how to scale up cell culture capacity, etc. Downstream challenges: in the chromatography purification step, the overall yield of DSP is only 20-30%, with the main difficulty being the empty viral capsids present in the USP. In China, there is an extreme scarcity of multidisciplinary talents who possess expertise in virology, process development, and production management.

(2) The production of viral vectors faces high financial barriers.Establishing facilities and equipment that comply with cGMP standards requires substantial capital investment (hundreds of millions of US dollars), and each stage relies on a variety of imported equipment, reagents, and consumables. Equipment includes bioreactors, centrifuges, and chromatography columns, while reagents and consumables include plasmids, culture media, and HEK293 cells.

There is an extreme global shortage of viral vector production capacity, and the bottleneck cannot be resolved in the short term.According to L.E.K., the global average wait time for CGT CDMO services is as long as 16 months, or even two years. According to RootsAnalysis, the current capacity shortfall is at least one to two orders of magnitude, which must be addressed before future product demand can be met.

3CGT CDMOs Resolve Viral Vector Production Bottlenecks, Becoming Indispensable Participants in the Industry Chain

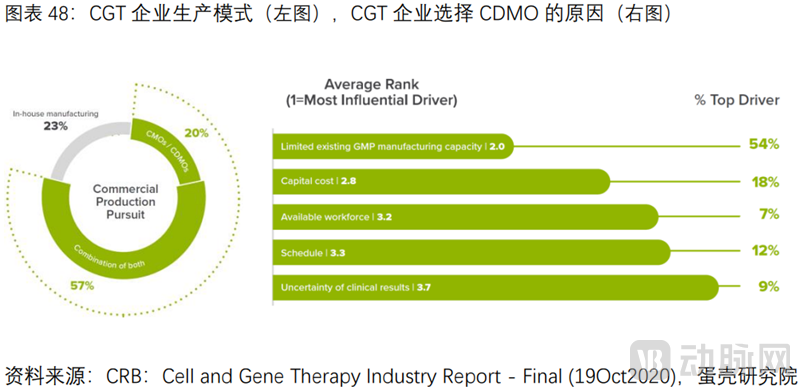

CGT CDMOs Reduce Costs and Increase Efficiency, with Production Outsourcing Penetration at 65%, Far Higher Than the 35% for Traditional Drugs.In 2021, a CRB survey of 150 companies revealed that only 23% opted to build their production lines entirely in-house, while the vast majority chose to outsource either fully (20%) or partially (57%).

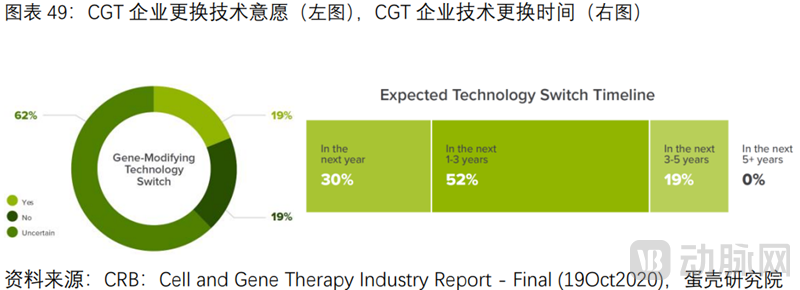

CDMOs are indispensable participants in the industry chain.Survey results indicate that the primary reasons for companies to outsource are: lack of GMP-grade production capacity (54%), with 18% and 12% of companies citing R&D costs and timelines, respectively. Additionally, up to 81% of companies may change their R&D technologies within the next five years. Since the FDA requires clear definition of manufacturing processes at the IND stage, any significant changes necessitate re-submission. Therefore, CDMOs provide pharmaceutical companies with flexible options for diverse manufacturing processes.

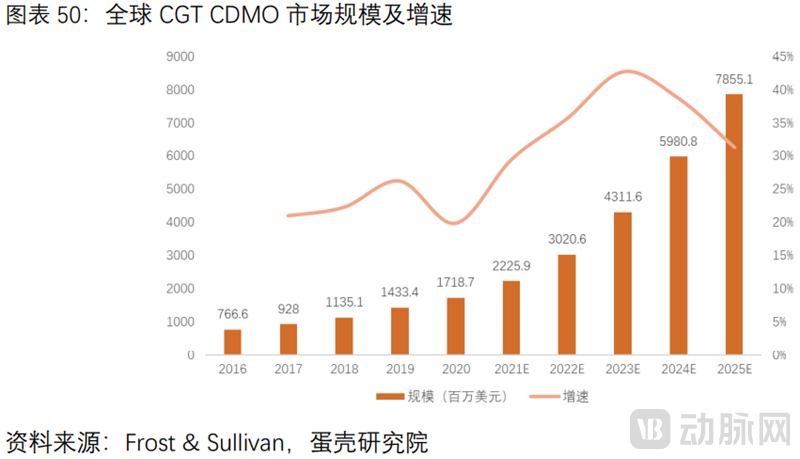

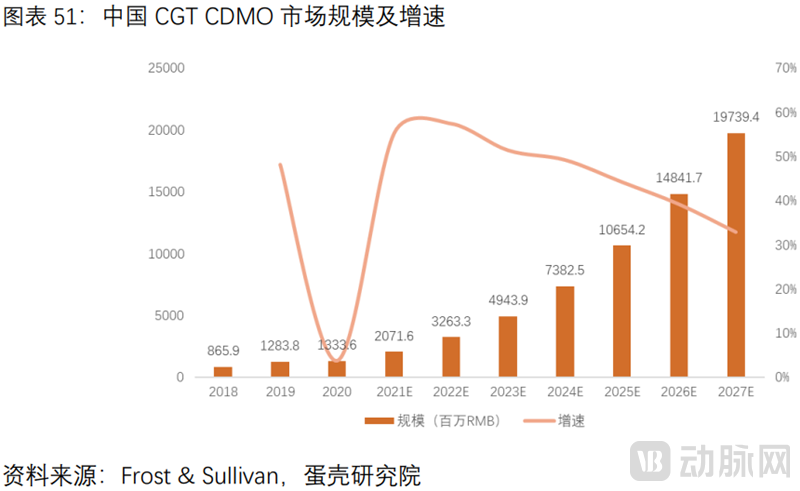

The CGT CDMO Market Is Rapidly Expanding.According to Frost & Sullivan, the global market size for CGT CDMO grew from USD 767 million in 2016 to USD 1.719 billion in 2020, representing a compound annual growth rate (CAGR) of 22.4%. The market size is projected to reach USD 7.866 billion by 2025, with a CAGR of 35.5% from 2020 to 2025. In China, the CGT CDMO market size is expected to increase from RMB 870 million in 2018 to RMB 3.26 billion in 2022, and is forecast to reach RMB 19.74 billion by 2027. The CGT CDMO sector is entering a golden period, with more companies expected to enter this field through mergers and acquisitions or expansion.

A Three-Dimensional Analysis of the Challenges and Future Trends in Gene Therapy (Technology + Manufacturing + Commercialization)

1Gene Therapy Faces Multiple Challenges in Technology, Manufacturing, and Commercialization

(1) Technical Challenges

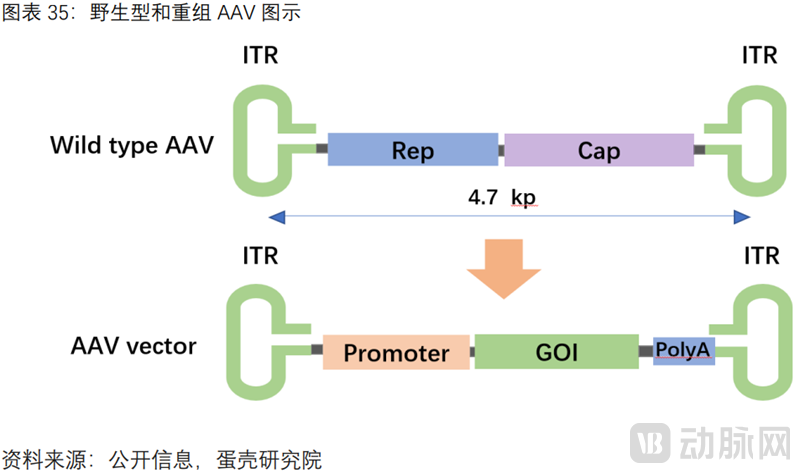

Since the synthesis of the target gene in gene augmentation therapy is relatively straightforward, the primary challenge lies in the delivery vector itself. Key technical hurdles include transduction efficiency (the efficiency with which the target gene reaches the target cells), tissue-specific targeting (off-target gene expression may lead to toxicity or trigger unwanted immune responses), AAV vector capacity (limited to 4.7 kb, preventing the packaging of larger fragments), and immunological barriers (primarily adaptive immune responses such as cytotoxic T lymphocyte [CTL] responses and neutralizing antibodies [NAbs], as well as innate immune responses following AAV transduction).

The most critical technical challenge in gene editing is the safety concern arising from off-target effects. The wild-type Cas9 protein cleaves double-stranded DNA to create double-strand breaks (DSBs), thereby increasing the likelihood of off-target effects. A study published in Nature on March 2, 2022, revealed that when mismatches occur at the 18th–20th nucleotides of the sgRNA, the Cas9 enzyme does not disengage; instead, it firmly grips the mismatched region via a finger-like domain, stabilizing the RNA-DNA duplex and making it resemble a correctly paired structure. This facilitates Cas9-mediated DNA cleavage, leading to serious safety issues known as “off-target effects”—wherein the CRISPR editing system erroneously cleaves double-stranded DNA at non-target sites in vivo.

(2) Production Bottlenecks

Challenges in the Upstream Process (USP) of Viral Vector Production Include: How to reduce the amount of plasmid required for transient transfection and improve transfection efficiency, thereby lowering plasmid costs (the primary cost driver for AAV); how to increase cell culture density to expand production capacity.

The primary challenge in downstream processing (DSP) lies in chromatographic purification, particularly in the removal of empty viral capsids.As AAV is commonly used for in vivo gene therapy, it demands high purity. However, product-related impurities such as empty capsids and degradation products are difficult to remove. Currently, the overall yield of downstream processing (DSP) for viral vectors is only 20–30%. The main challenge lies in the abundant presence of empty capsids (accounting for more than 70%) in the crude upstream process (USP) harvest: (1) although they do not contain the therapeutic gene, the capsid proteins themselves pose immunogenicity risks; (2) they compete with full capsids for limited receptors on the cell surface, thereby reducing transduction efficiency.

(3) Commercialization Dilemmas

On one hand, the patient population for rare disease indications is inherently small.Glybera is indicated for the treatment of lipoprotein lipase deficiency (LPLD), a condition that is extremely rare, with an incidence rate of approximately 1 in 1 million and a high rate of misdiagnosis. During its market availability, only one patient received this therapy. Strimvelis is used to treat adenosine deaminase (ADA)-deficient severe combined immunodeficiency (ADA-SCID) caused by ADA mutations. This disease is exceedingly rare, with only 15 new cases reported annually in Europe; consequently, only two patients had received treatment by 2017. By April 2018, when GSK sold Strimvelis to Orchard Therapeutics, only five patients had undergone this treatment.

On the other hand, the commercial pricing of gene therapy products is extremely high.。Zolgensma is priced at up to $2.125 million (approximately RMB 14 million) per dose, earning it the title of “the world’s most expensive drug.” The average treatment cost for several other products also exceeds $1 million. The exorbitant end-user commercial pricing, driven by prohibitively high R&D costs for gene therapies, coupled with an inadequate insurance reimbursement system, has left very few patients with the actual ability to pay.

2Outlook on the Development Trends of Gene Therapy from the Perspectives of Technology, Manufacturing, and Commercialization

(1) Technological Trends

In the dimension of delivery vectors, “gene expression cassette engineering” and “capsid engineering,” among others, enhance safety, efficacy, and durability.Since AAV vectors consist of two components—the genome and the capsid protein—efforts to overcome technical challenges in delivery often focus on these two aspects. To enhance transduction efficiency, “gene expression cassette engineering” is employed. To improve tissue-specific targeting, “capsid engineering” is utilized, as the AAV capsid protein determines tissue tropism; specifically, AAV entry into cells depends on the recognition of AAV capsid proteins by cell-surface glycosylated receptors. To address the limited packaging capacity of AAV vectors, two improvement strategies are available: one involves splitting a large gene of interest across two (or more) vectors and then reconstituting the AAV genome via homologous recombination mediated by ITR sequences; the other involves retaining only the functional fragments of the gene of interest. Furthermore, to overcome host immune barriers, both “gene expression cassette engineering” and “capsid engineering” can be leveraged.

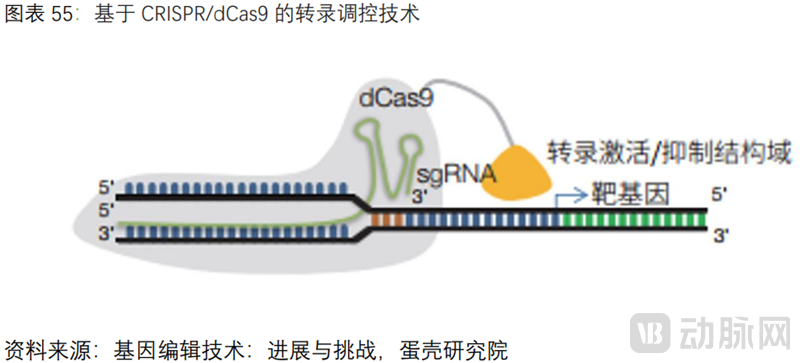

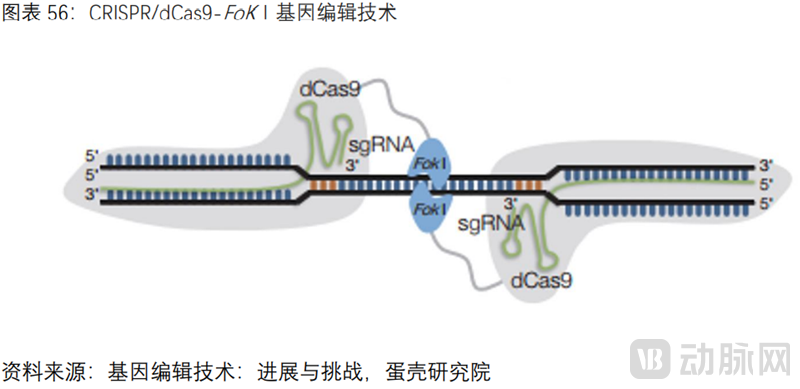

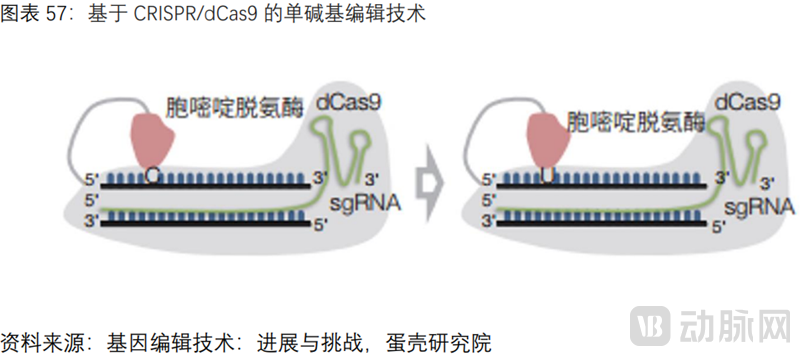

In the dimension of gene editing, modifying Cas proteins or sgRNA sequences to reduce off-target effects.First, the overarching trend in gene editing is shifting from ex vivo to in vivo approaches to reduce treatment costs, and expanding from single-gene to multi-gene editing to provide therapeutic solutions for a broader range of indications. The following section focuses on key development trends aimed at overcoming the “off-target effects” of gene editing systems. Since the CRISPR/Cas9 system consists of two components—the Cas protein and sgRNA—most current improvement strategies are based on the Cas protein. Among these, series of Cas9 mutants predominate; because wild-type Cas induces double-strand DNA breaks, off-target effects can be reduced by introducing amino acid mutations at specific sites to generate Cas9 nickases (Cas9n) with single-strand targeting cleavage activity, or fully inactive dead Cas9 (dCas9). In recent years, RNA single-base editing based on Cas13 has also become a hot spot in research and development.

(2) Production Optimization Trends

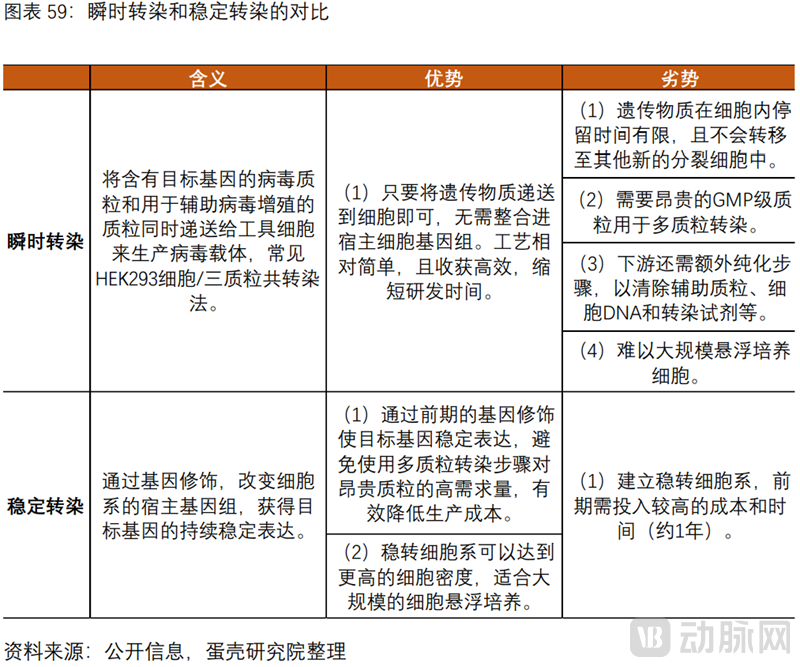

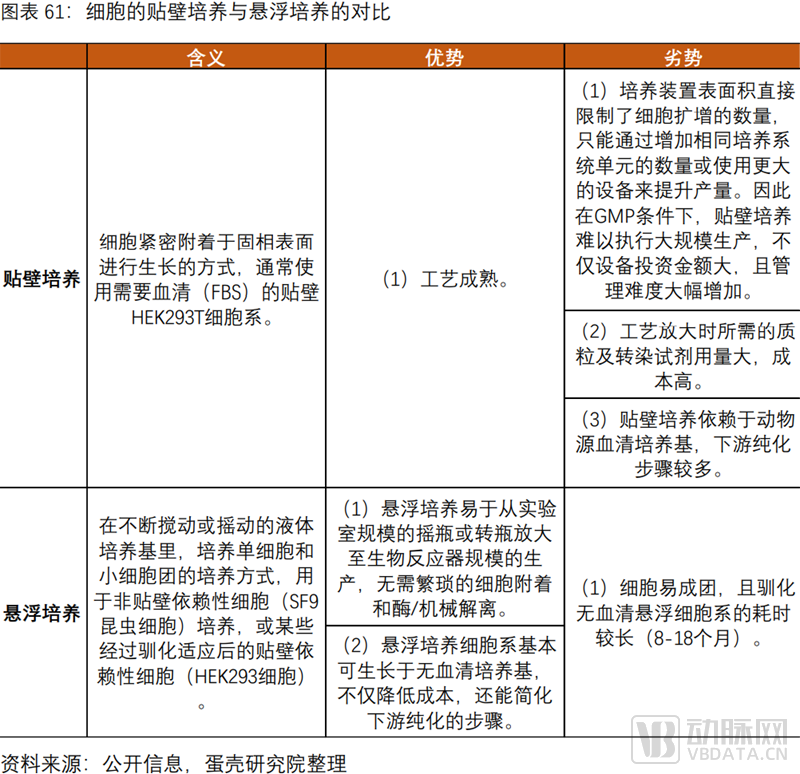

"Stable Transfection + Suspension Culture" Will Dominate Future Trends, Driving Down Costs and Expanding Production Capacity.Upstream production of viral vectors primarily involves transfection and cell expansion culture. Transfection methods include transient transfection and stable transfection, while cell expansion culture methods encompass adherent culture and suspension culture. Currently, the predominant transfection process is transient transfection via multi-plasmid co-transfection. Approximately 70% of products utilize adherent cells, including the two gene therapies approved by the FDA; meanwhile, adherent culture processes are more mature and widely applied for cell expansion. Due to the severe shortage of viral vector production capacity, from a commercialization perspective aimed at increasing yield and reducing production costs,“Stable Transfection + Suspension Culture” Will Dominate Future Trends, and the two mutually validate each other. Stable transfection is generally more suitable for suspension cell lines. The downstream processing of viral vector production involves numerous steps, with chromatographic purification being the most critical. Currently, low recovery rates in downstream processing (DSP) pose a significant challenge. Future improvements in manufacturing processes should focus on reducing the empty capsid rate, for example, by employing analytical ultracentrifugation (AUC).

Key Advantages of Stable Transfection: Avoid the cost advantage of using expensive plasmids. Since plasmids are core raw materials and a major cost driver in AAV production, reducing plasmid usage can effectively lower AAV production costs.

Key Advantages of Cell Suspension Culture: Advantages in production capacity and cost. First, it is easily scalable to bioreactor scale; second, it significantly increases cell culture density per unit volume; third, the use of serum-free media simplifies downstream purification steps. According to CRB, approximately 65% of companies are currently building or planning to build suspension cell-based viral vector production platforms.

(3) Commercialization Trends

On the one hand, indications have expanded from rare diseases to common conditions, enabling “one-time treatment.”Currently, the indications for gene therapy are primarily concentrated on rare diseases. However, the advantages of gene therapy—“curative at the root, single-dose administration”—hold immense appeal. As adeno-associated virus (AAV) vector technology and manufacturing processes become increasingly mature, the indications of more and more gene therapy pipelines under development are expanding to include common diseases. For instance, Regenxbio’s RGX-314 is indicated for wet age-related macular degeneration (wAMD), RGX-501 for homozygous familial hypercholesterolemia (HoFH), and Staidson’s STSG-0002 for hepatitis B. For the treatment of wAMD, current blockbuster anti-VEGF drugs such as ranibizumab and aflibercept require frequent monthly intravitreal injections, which are inconvenient. In contrast, RGX-314, based on the AAV8 vector, directly delivers the anti-VEGF Fab gene into the eye. Clinical results from the “one-and-done” treatment have demonstrated favorable safety and efficacy. For the treatment of HoFH, a monogenic disorder, the current RNAi drug inclisiran is delivered via a GalNAc conjugation technology platform, whereas RGX-501, based on the AAV8 vector, delivers the LDLR gene to the liver with “single-dose administration.” Regarding hepatitis B treatment, Johnson & Johnson’s JNJ-2989 and Roche’s DCR-HBVS, both RNAi drugs, are also delivered via the GalNAc conjugation technology platform. In contrast, Staidson’s STSG-0002, based on an AAV vector, delivers shRNA sequences targeting the HBV genome.

On the other hand, the insurance payment system is becoming increasingly robust.Currently, most gene therapy pharmaceutical companies are collaborating with insurance providers to introduce "installment payment" models, featuring outcome-based pricing and refunds for treatment failure. For instance, Novartis allows certain insurers to pay for Zolgensma in installments over five years at an annual cost of $425,000. In the United States, insurers have launched "commercial insurance special policies for cell and gene therapy (CGT)," enabling full coverage through commercial insurance, where enrollees simply pay monthly premiums. Bluebird Bio has proposed a five-installment payment plan, with the initial payment due at the time of Zynteglo infusion; the remaining four installments are spread over the following four years, contingent upon the patient no longer requiring transfusion therapy for transfusion-dependent thalassemia (TDT). Furthermore, Bluebird Bio has signed payment agreements with several statutory health insurance companies in Germany, stipulating that treatment fees are payable only if the therapy proves effective. Similarly, Spark Therapeutics has introduced a novel payment model: patients pay an upfront fee in the first year, with the balance of the treatment cost due only if the gene therapy remains effective after 20 years.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows,Scan the QR code to download the full report for free.:

Part I: Gene Therapy—Curative at the Root, with Broad Prospects

1.1 Gene Therapy: Curative at the Root, with Both Clinical and R&D Advantages

1.2 Moving Forward Amidst Twists and Turns: The Future of Gene Therapy Is Already Here

1.3 Policy Support and Capital Frenzy: Broad Prospects for Gene Therapy

Part II: Gene Therapy Effectively Cures Rare Diseases, with Viral Vectors as the Key to Gene Therapy

2.1 Two Major Technical Pathways: Gene Augmentation Is Relatively Mature, While Gene Editing Offers “High Potency” and “Targeted Precision”

2.2 Delivery Methods for Gene Therapy

Part 3: CGT CDMOs Address Bottlenecks in Large-Scale Viral Vector Production to Accelerate Commercialization

3.1 The upstream segment of the gene therapy industry chain, which is dominated by viral vector production, constitutes the core of gene therapy commercialization

3.2 Numerous Barriers Exist in the Large-Scale Production of Viral Vectors, Leading to Severe Capacity Shortages

3.3 CGT CDMOs Resolve Viral Vector Production Bottlenecks, Becoming Indispensable Participants in the Industry Chain

Part IV: A Three-Dimensional Analysis of the Challenges and Future Trends in Gene Therapy (Technology, Manufacturing, and Commercialization)

4.1 Gene Therapy Faces Multiple Challenges in Technology, Manufacturing, and Commercialization

4.2 Outlook on the Development Trends of Gene Therapy from the Perspectives of Technology, Manufacturing, and Commercialization

This report is part of the series for VCBeat’s 6th Future Healthcare Top 100 Conference, which will be held online from June 14 to 18, 2022. The report will be presented and released at the conference.