2022 Future Healthcare 100: Chasing the Moon Without Pause – Data Insights into China's MedTech Innovators and Their Stories

If the next decade is to be the Age of Discovery for the healthcare industry, it will undoubtedly be a voyage filled with compelling narratives. These stories are unfolding and being celebrated across China’s fertile ground for innovation, where we are witnessing a group of tech enthusiasts and medical geniuses reshape the world of life sciences.

In the sixth year of the Top 100, we take “China Story”as the foundational perspective, withHomegrown Innovations in China: Novel Solutions from Chinese Local Innovation to Global ChallengesCentered on narrative threads, the event conveyed the unique story of China’s life sciences industry through the accounts of its protagonists. Building on this foundation, the 6th Future Healthcare 100 Cloud Summit officially commenced on June 14, 2022. Over a five-day period featuring 22 thematic forums and 78 hours of speeches and dialogues, participants gathered in the cloud to collectively narrate the story of healthcare in China.

During the annual Top 100 Future Healthcare Companies Conference, in addition to the insightful presentations at various forums, the selection of the Top 100 Future Healthcare Companies list has drawn significant attention from the industry. The selection process for this year’s list was launched in December 2021. Over a four-month application period, the organizing committee collected nearly 1,300 company submissions through methods including self-nomination by enterprises, institutional recommendations, and targeted research.Each review of an application dossier constitutes a reading of China’s narrative; we are also privileged, in this process, to gain insight into the spirit of medical innovation that underpins the stories told by healthcare innovators in China.

Seeking Answers with Questions.We believe this is the foundational backdrop of China’s healthcare narrative and the prerequisite for addressing infinite challenges with finite resources. How can we advance drug development and technological innovation to meet unmet clinical needs? The answer lies within these 1,300 documents. More than 30 AI-driven drug discovery companies are exploring the vast potential of AI in pharmaceuticals—spanning target identification, compound screening, real-world studies, and clinical trials—through algorithmic platforms and proprietary pipelines. Meanwhile, over 20 brain science enterprises are offering novel approaches to the diagnosis and treatment of neurological disorders via brain-computer interfaces, digital therapeutics, and big data analytics of electroencephalography (EEG).

Unbounded Curiosity and Enduring Stamina.In the application materials submitted by entrepreneurs and scientists, we frequently encounter terms such as “breakthrough,” “first-of-its-kind,” and “focused on,” which are used to describe individual innovative capacity, along with the underlying R&D achievements and commercial performance. By maintaining boundless curiosity, innovative entrepreneurs are able to lead their teams to sustain passion and focus amid the tedious, iterative cycles of R&D and business model refinement—this serves as the core driving force for the company’s continued progress. Meanwhile, persistent endurance has repeatedly helped scientists navigate the long, silent nights spent awaiting experimental results, enabling source innovation to progress from 0 to 1 and transforming experimental samples into marketable products. The combination of infinite curiosity and enduring perseverance constitutes the emotional resonance within China’s healthcare narrative.

Catch-up and Surpass.From inception to overtaking, from following to leading—this is the momentum of indigenous innovation in China that we have witnessed, and it defines the narrative arc of China’s story in the healthcare industry. In the corporate submissions for this review, 70% of companies systematically articulated their core products under development, addressing key dimensions such as core value, cost-effectiveness, regulatory compliance, iterative innovation, and strategic planning. It is encouraging to observe that, against the backdrop of domestic substitution in medical devices, numerous high-potential sectors have seen the emergence of innovative products with international competitiveness. Meanwhile, local pharmaceutical companies are maturing in their R&D capabilities and formulating global expansion strategies and action plans tailored to their specific circumstances. As China surges ahead and closes gaps, the world is viewing the identity and contributions of China’s explosive innovation within the global innovation landscape through a new lens.

Chase the wind and moon, never pause—paying tribute to all the innovations and stories unfolding across China.

Rankings Released

The Future Healthcare 100, established in 2015, is China’s first ranking list focused on innovative healthcare companies that are not publicly listed. It was launched by VB100, VCBeat, and VCBeat Research Institute. The initiative aims to identify Chinese innovators who truly represent the future of healthcare, uncover the core driving forces behind China’s future healthcare industry, and promote innovation and transformation within the health and medical sector. Over the past seven years, the Future Healthcare 100 ranking system has continuously expanded, gradually evolving into a global innovation ecosystem benchmark for enterprises, investment institutions, hospitals, and industrial parks. It is currently the most closely watched annual selection in the life and health sector by both industry professionals and investors.

In addition, VCBeat annually releases a Growth Report on the Top 100 Enterprises based on that year’s Future Healthcare 100 list. Coinciding with the release of the 2022 Future Healthcare 100 list, VCBeat has once again published the “2022 Future Healthcare 100 Enterprise Growth Report,” which provides a comprehensive analysis of data related to enterprises listed in the four main categories: China Innovative Medical Services, China Innovative Medical Devices, China Innovative Digital Health, and China Innovative Biopharmaceuticals. We aim to summarize patterns of enterprise growth and trends in industry evolution by analyzing the companies featured on the Future Healthcare 100 list, thereby offering valuable insights for healthcare companies and entrepreneurs. (Excerpts from the report are provided below, and instructions for accessing the full report are included at the end.)

The 2022 Future Healthcare Top 100 series rankings comprise the Future Healthcare Top 100 Main List, the Future Healthcare Top 100 Value Sector List, the Future Healthcare Top 100 Listed Companies Innovation Ranking, as well as two major awards: the Future Healthcare Top 100 Pengcheng Award and Weilan Award.

Main List

This selection is open to non-listed companies in the healthcare and medical sector. Based on the VB100 valuation model, the process involves self-nomination by enterprises, review by the VB100 Review Committee, cross-review by supporting institutions, and final approval by the Expert Committee. From each of the four major sectors—medical services, digital health, medical devices, and biopharmaceuticals—the top 100 innovative companies by valuation will be selected. In addition to valuation, the evaluation will focus on growth and annual performance across four primary indicators: human resources, intellectual resources, key partner resources, and market performance, encompassing a total of 17 secondary indicators.

Value Sector Rankings

Through multi-dimensional and comprehensive insights and explorations—including investor interviews, journalist interviews, and industry report analysis—this annual selection uses capital attention as the primary benchmark, supplemented by three additional criteria: media focus, heat of annual performance data of healthcare enterprises, and the projected prosperity of the future healthcare industry. It conducts a thorough review of over 60 sub-sectors across four major tracks—medical devices, biopharmaceuticals, digital health, and healthcare services—to identify the Top Ten Value Sectors of the year and select the most representative and high-growth innovative enterprises within each value sector.

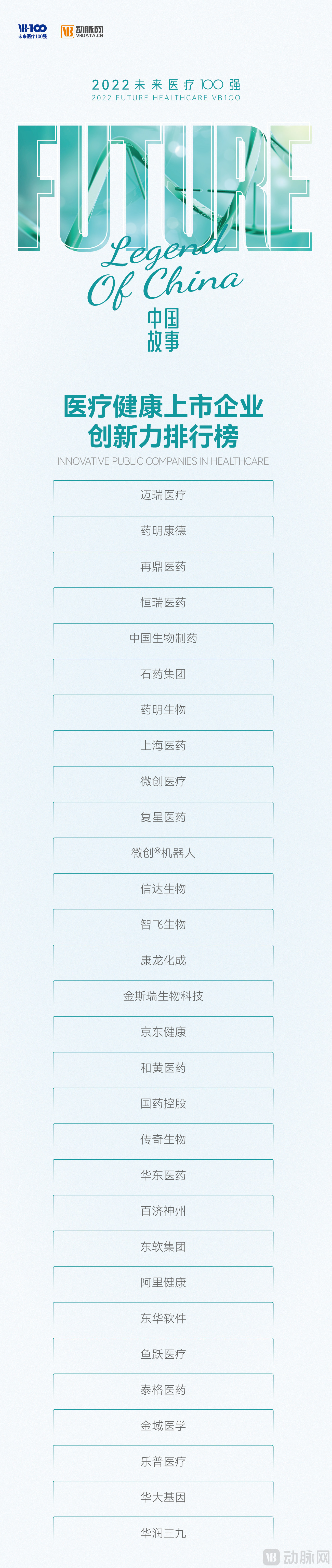

Listed Companies' Innovation Power Ranking

As a backbone of China’s economic development, listed companies’ innovation capability serves not only as the core engine for corporate growth but also holds significant practical importance for national innovation strategies and industrial upgrading. This selection is based on the 2021 annual report data of listed companies, supplemented by survey data covering more than 30 indicators across four dimensions: innovation input, innovation output, innovation efficiency, and innovation activities. The final rankings were determined by integrating these metrics with VCBeat’s assessment methodology, which evaluates the innovation trends and market potential within the specific sectors where these listed companies operate.

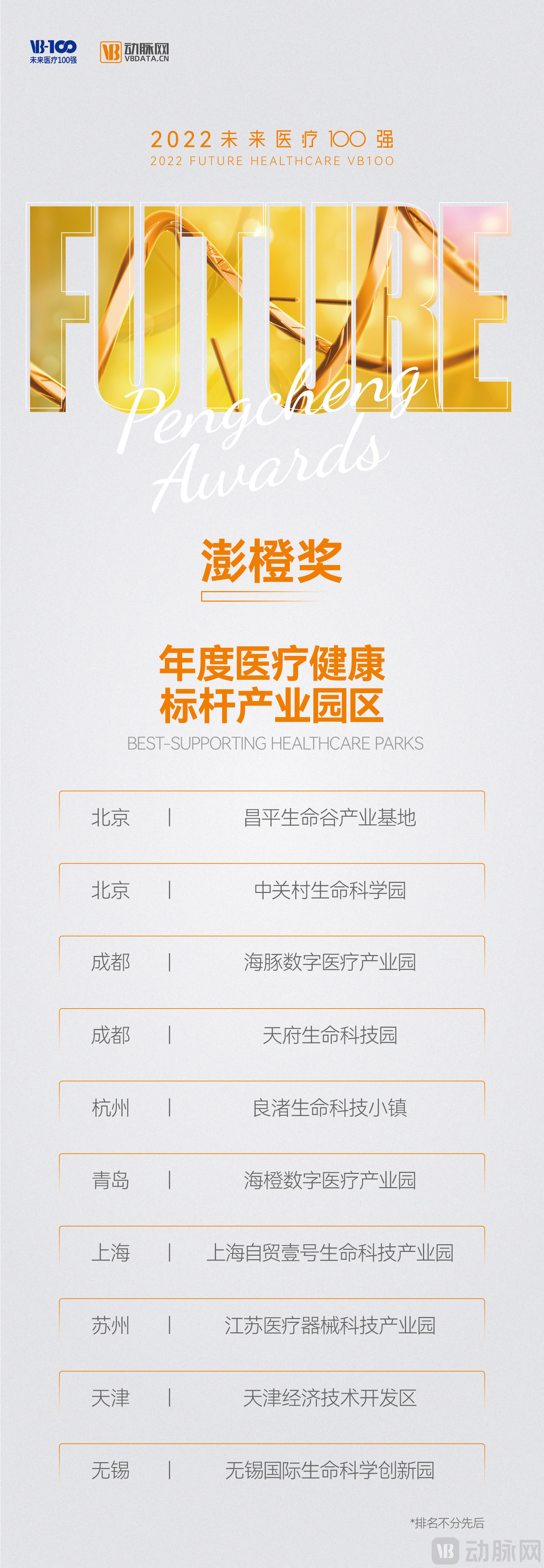

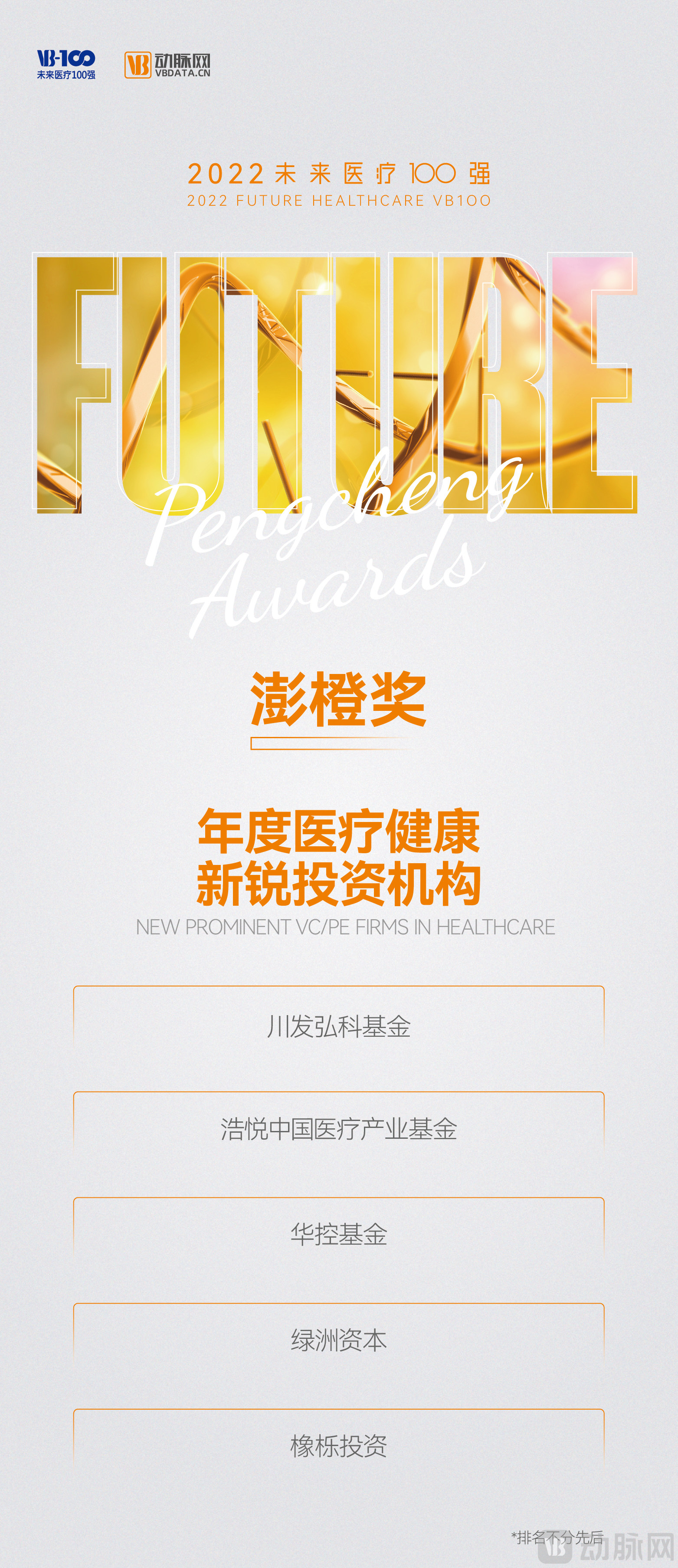

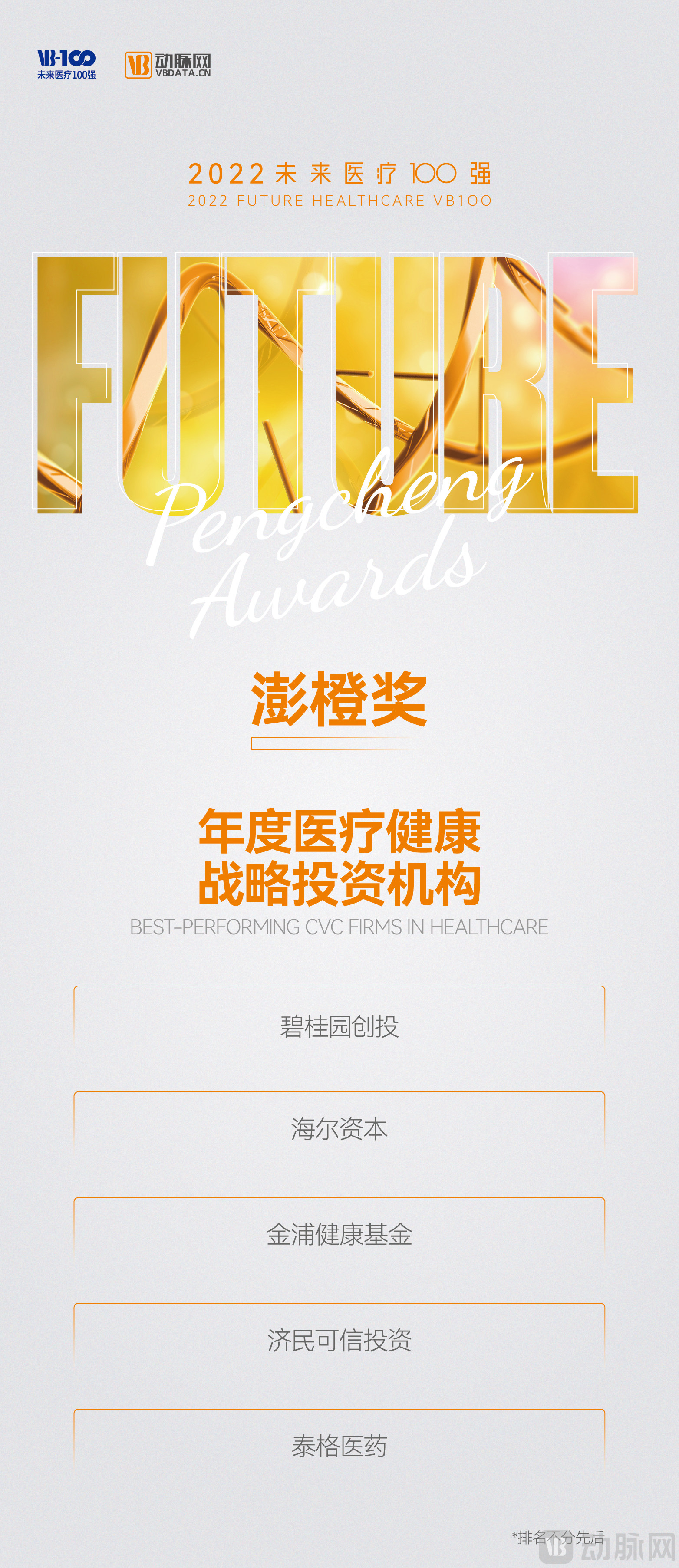

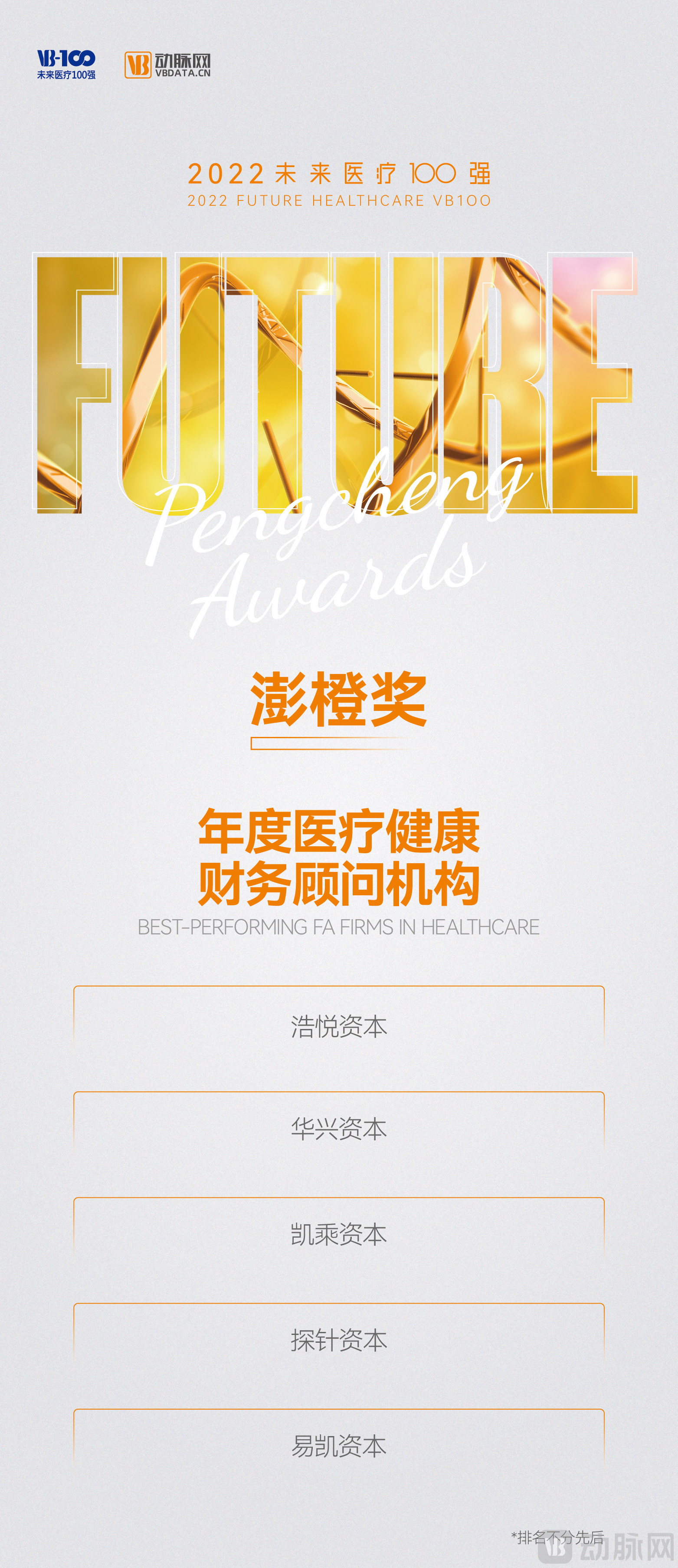

Pengcheng Award

“Pengcheng” symbolizes boundless prospects, with orange as its exclusive award color. Orange, the primary brand color of Danke Technology, represents prosperity, strength, wisdom, and vitality, embodying the spirit and demeanor of stakeholders in the healthcare sector who strive for innovation and progress. The Future Healthcare Top 100 · Pengcheng Award evaluates investment institutions, enterprises, and industrial parks in the healthcare field, with a particular focus on their annual performance and breakthroughs during the review period.

Weilan Award

“Azure Tide” symbolizes a promising future, with azure blue as its exclusive award color. Blue is the primary color of VB100, representing courage, composure, rationality, and perseverance. It embodies the qualities and spirit of innovative and pioneering healthcare professionals, investors, and entrepreneurs. The Future Healthcare Top 100 · Azure Tide Award recognizes investors, entrepreneurs, and scientists who drive innovation in the healthcare sector, with a focus on evaluating candidates’ annual innovation capacity, team leadership, and industry influence during the review period.

2022 Future Healthcare 100 Report on Corporate Growth

I. Overall Analysis of Valuations for Listed Companies

(1) The cumulative valuation has exceeded RMB 1 trillion for three consecutive years, with the valuations of the top 10 companies all surpassing RMB 10 billion.

In this edition of the rankings, the total valuation of companies listed across the four categories—Medical Services, Innovative Medical Devices, Digital Health, and Innovative Pharmaceuticals—reached RMB 1462.789 billion, with an average valuation of RMB 3.657 billion per company. Approximately 76.75% of the companies fell within the RMB 1–6 billion valuation range (inclusive of RMB 1 billion). Seventeen companies achieved valuations exceeding RMB 10 billion, including seven unicorns with valuations surpassing RMB 20 billion.

(2) Device Unicorns Lead the Way, Medical Device List Has the Highest Total Valuation

The cumulative valuation of listed medical device companies has exceeded RMB 400 billion, representing the highest total among the four main rankings. In recent years, China’s medical device industry has maintained a high level of prosperity, driven by demographic shifts, the substitution of imported products with domestically produced ones, and a surge in original innovation. Leading enterprises with strong technological, clinical, and commercial value have emerged in minimally invasive interventional sectors such as cardiovascular, neurological, and orthopedic devices, attracting sustained capital interest and increased investment, resulting in robust primary market valuations. Against the backdrop of the pandemic response, IVD (In Vitro Diagnostics) companies have also achieved rapid growth, gradually expanding their layouts across upstream and downstream segments of the industrial chain, thereby accelerating the pace of financing.

(3) The biopharmaceutical sector’s valuation on the list surged by 43.74%, with cell and gene therapy leading the development of innovative drugs

According to statistics from the VCBeat database, there were 523 investment and financing events in China’s biopharmaceutical sector in 2021, representing a 57.1% year-on-year increase from 2020; the total amount involved reached RMB 118.875 billion, a 34.5% increase from 2020. The small-molecule drug and large-molecule drug sectors gradually entered a bottleneck period in 2021. The development of frontier biotechnology tracks, such as cell therapy, gene therapy, and nucleic acid drugs, was the primary driver behind the further growth of investment and financing in the biopharmaceutical sector.

(4) AI + Healthcare Flourishes Across the Board; AI-Driven Drug Development Companies Shine in Valuation on Digital Health Rankings

The overall valuations on the Digital Health list are lower than those on the Medical Devices and Biopharmaceutical lists, yet the average valuation of listed companies has reached RMB 3 billion. In 2021, frontier technologies such as artificial intelligence and brain science became deeply integrated with the healthcare sector, driving active primary-market financing for digital health enterprises. First, AI-driven drug discovery (AIDD) has entered a phase of rapid development, with star AIDD companies such as XtalPi, Insilico Medicine, and BioMap demonstrating strong performance in both R&D and fundraising. Second, digital therapeutics have remained highly popular, with companies focusing on mental disorders, psychological health, and chronic diseases continuing to attract significant capital attention.

(V) In the post-pandemic era, the development of specialized healthcare chains has gained momentum, while valuations in the medical services sector have remained stable.

Physical clinics, which struggled to survive during the pandemic, saw a recovery in their development performance in 2021 compared to 2020. In the post-pandemic era, specialized services in medical aesthetics, hair transplantation, dentistry, and mental health are expected to maintain a trend of steady growth.

II. Analysis of the Geographic Distribution of Listed Companies

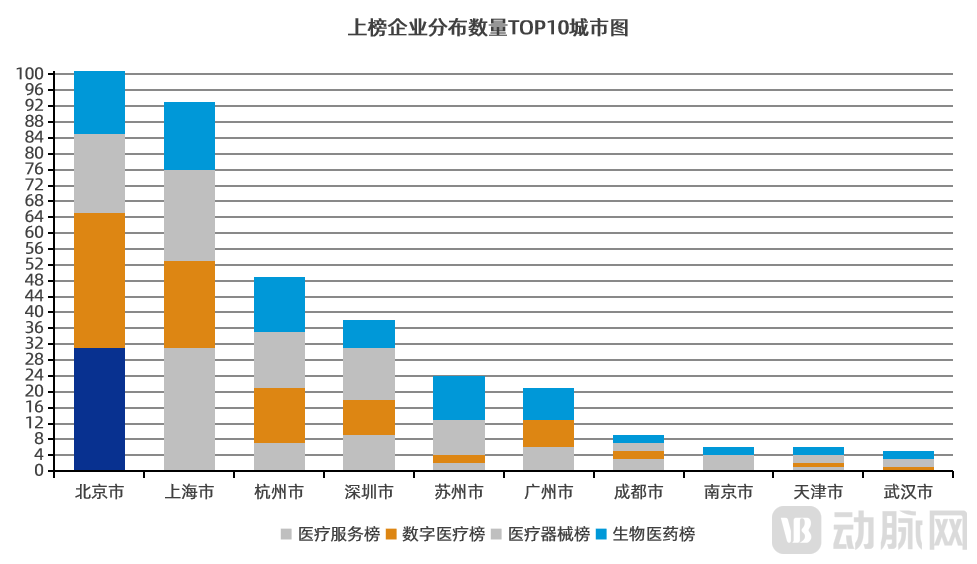

(1) Beijing and Shanghai remain the primary headquarters hubs for listed companies, with the top 10 cities by number of listed companies all being first-tier or new first-tier cities.

As with previous years’ rankings, the most fertile ground for the growth of leading health and wellness enterprises remains the first-tier cities along the eastern coast, primarily Beijing and Shanghai. Leveraging their superior geographic advantages, Beijing and Shanghai offer multifaceted benefits in policy, talent, technology, distribution channels, and market access, thereby fostering the growth of healthcare companies. The establishment of the Beijing Stock Exchange has further broadened financing avenues for innovative technology firms, significantly promoting the development of the healthcare sector in the Beijing-Tianjin-Hebei region. The “Beijing Action Plan for Accelerating Collaborative Innovation in Medicine and Health (2021–2023)” outlines key development objectives for Beijing by 2023, including realizing clinical spillover effects, advancing high-quality internationalization of the healthcare industry, and strengthening functional layouts in key areas, all of which will further stimulate regional industrial innovation and development.

(2) Shenzhen-based companies on the list had the highest average valuation, making it the only city with an average valuation exceeding RMB 4 billion.

A total of 38 companies headquartered in Shenzhen made it onto the Top 100 list. Influenced by the valuation of MGI Tech, a medical device unicorn, Shenzhen has become the only city where the average valuation of listed companies exceeds RMB 4 billion. Excluding the impact of hundred-billion-yuan unicorns on average valuations, the Greater Bay Area, with Guangzhou and Shenzhen at its core, has also emerged as the third growth pole for China’s biopharmaceutical industry. Taking Shenzhen as an example, the city enacted special legislation in 2021 to promote the development of the cell and gene therapy industry. This legislative framework addresses pain points, difficulties, and bottlenecks in industrial development through coordinated institutional solutions, thereby driving high-quality development in the cell and gene therapy sector.

(3) Chengdu Leads New First-Tier Cities in Western China, Becoming a Hub for Medical and Health Enterprises in the Region

Unlike previous editions, where listed companies were heavily concentrated in the eastern coastal regions, the geographic distribution of companies on this year’s list has become increasingly diversified. Leading cities in central and western China, such as Chengdu, Wuhan, Xi’an, and Changsha, are all home to standout enterprises that have made the list. A key driving force behind this trend is the continuous talent pipeline provided by universities in these central and western cities to innovation in the healthcare industry. In particular, the emergence of a large cohort of scientist-entrepreneurs has strengthened the capacity for original innovation, supplying core talent that fuels the growth of regional enterprises.

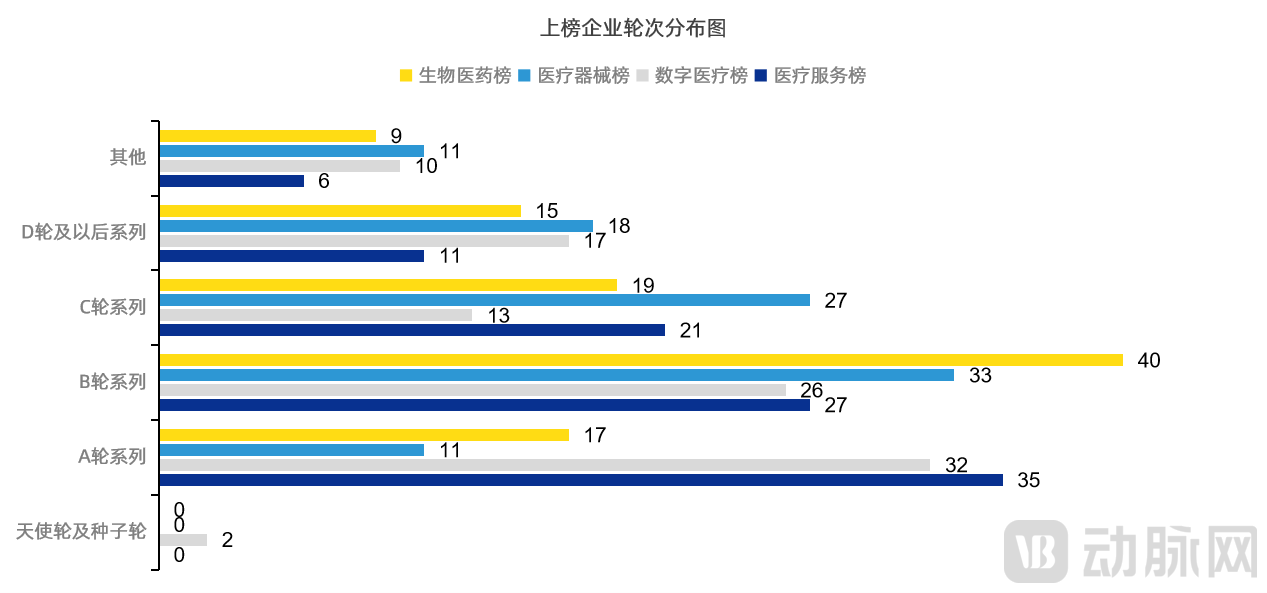

III. Analysis of Financing Rounds for Listed Companies

(1) The listed companies are primarily in the growth stage, with funding rounds concentrated in Series A and Series B.

For unlisted innovative enterprises, there is a strong correlation among their financing history, duration of growth, and scale of development. Data on the most frequent financing rounds among listed companies indicate that Series A and Series B rounds dominate, which aligns with the 2021 data on the development and financing performance of healthcare companies. According to statistics from the VCBeat Orange Database, total investment and financing in China’s healthcare industry reached a record high of RMB 219.2 billion in 2021, a year-on-year increase of 32.84%. Meanwhile, the number of financing transactions reached 1,362, up 77.57% year on year. A cohort of domestic startups with complete business models and expanding operations performed notably well during the year, with more than half completing Series A or Series B financing. Taking medical device companies as an example, when innovative medical devices are developed rapidly with a focus on meeting clinical needs and obtain medical device registration certificates, capital markets are willing to assign relatively high valuations at the early stages of corporate growth.

(2) Digital health companies are more likely to achieve higher valuations during their growth stage

Compared with the other three major sectors, digital health companies continue to secure favorable valuations even during their growth stages, a relative performance that has been consistently reflected in the data of companies listed over the past three editions. Digital health is an increasingly competitive field; in today’s early-stage investment landscape, the advantages of digital health are prominent, with high-potential startups being highly favored by capital. It is worth noting that the core competitiveness of most digital health companies on this year’s list remains technology-driven. As technological barriers continue to rise and are difficult to replicate in the short term, these companies can establish their competitive advantages early on, design their business systems around core technologies, and have more easily predictable market prospects.

(3) Biopharmaceutical Companies in Series B Financing Stand Out on the List

In the biopharmaceutical sector, China ranks second globally in the number of innovative drugs under development, and biopharma remains a key focus for investment in the health industry. Setting aside the phenomenon in 2021 where some biopharmaceutical companies’ IPOs broke their issue prices on the first day of trading, high-quality innovative drug R&D enterprises at around the Series B stage have continued to attract market favor. This is driven by the intrinsic growth logic of hot sectors such as cell therapy, gene therapy, CRO/CDMO (“shovel sellers”), and nucleic acid drugs, supported by high technical barriers and robust, breakthrough-oriented product pipelines. Abogen Biosciences, which holds China’s first clinical trial approval for an mRNA vaccine and ranks as the top biopharmaceutical company, refreshed the financing record in China’s biopharma sector in 2021 with a Series C round exceeding $700 million.

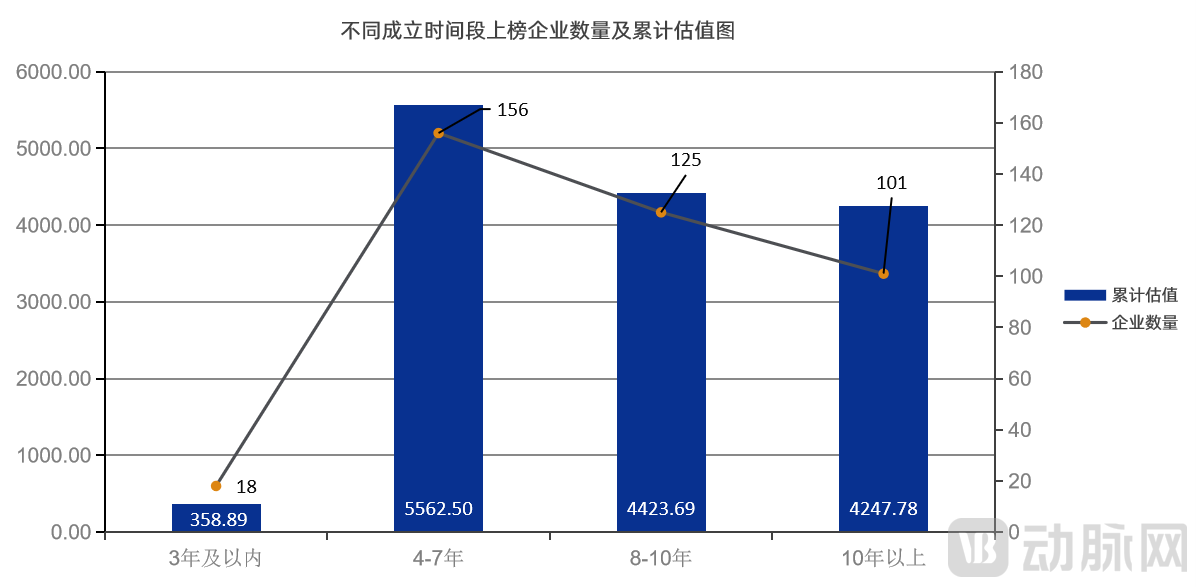

IV. Analysis of the Founding Dates of Listed Companies

(1) The average time for companies to make the list was 8.84 years, an increase from the 7.6 years required in the previous year.

Based on the founding dates, companies required an average of 8.84 years to be listed in the 2022 Future Healthcare Top 100, which is 1.24 years longer than in 2020–2021. VBInsight attributes this to two main factors. First, the number of innovative enterprises applying this year increased by 54% compared to the same period last year. The participation of numerous leading companies and unicorns in corresponding sectors squeezed out the listing opportunities for startups, thereby extending the average time required to make the list. Second, primary market financing in 2021 was generally more subdued. Investors exercised greater caution regarding early-stage companies’ products, business models, and chosen sectors. Only a few standout startups secured significant early-stage funding, while other innovative enterprises lacked valuation advantages in the ranking process.

(2) Biopharmaceutical companies have the shortest average time to make the list, while healthcare service providers have the longest.

Unlike in previous years, when digital health companies required the shortest average time to make the list, biopharmaceutical companies took the least time this year, requiring only 8.57 years. Data from the 2022 Future Healthcare 100·China Innovative Biopharma List shows that 51% of the listed companies were founded within the past seven years. This indirectly indicates that biopharmaceutical enterprises experienced active financing in the primary market in 2021, securing high valuations at early stages.

On the other hand, innovative medical service companies required the longest time to make the list, with an average of 9.06 years. In terms of the business sectors of the medical service companies on this year’s list, a total of 29 listed firms primarily specialize in private specialized medical services and integrated internet-based healthcare services. Affected by the pandemic, the expansion of offline specialized clinic chains was hindered to some extent; early-stage innovative medical service institutions struggled to survive and scale, while capital investment grew increasingly cautious. Only well-established leading specialized enterprises that had already secured significant market share were able to secure listings with relatively favorable valuations.

The above is an excerpt from the “2022 Top 100 Future Healthcare Companies Growth Report.” The report is structured as follows:

I. Description of the Ranking

II. Insight Overview

III. List Release

1. Top 100 Innovative Digital Health Companies in China

2. Top 100 Innovative Medical Services in China

3. Top 100 Innovative Medical Devices in China

4. Top 100 Chinese Innovative Biopharmaceutical Companies

IV. Overall Ranking Analysis

1. Overall Analysis of Listed Companies

2. Overall Analysis of Valuations for Listed Companies

3. Geographic Distribution Analysis of Listed Companies

4. Analysis of Funding Rounds for Listed Companies

5. Analysis of the Founding Dates of Listed Companies

V. Unicorn Analysis

1. Overview of Listed Unicorn Companies

2. Growth Analysis of Listed Unicorn Companies

VI. Analysis of the Top 100 Companies in Innovative Medical Devices

VII. Analysis of the Top 100 Companies in the Innovative Biopharmaceuticals Ranking

VIII. Analysis of the Top 100 Companies in the Innovative Digital Healthcare Ranking

IX. Analysis of the Top 100 Companies in the Innovative Medical Services List

X. Case Studies on Corporate Growth

BioKnow:International Intelligent Pharmaceutical and Precision Medicine Informatics + AI Service Platform

Baize Medical:Building China's Leading Full-Cycle Oncology Healthcare Group

Cheng Tian Technology:Exoskeleton Robots Lead the Consumer-Side Implementation in Rehabilitation and Elderly Care

Huamei Haolian:Full-Lifecycle Digital and Intelligent Health Management Service Platform

Huimei Technology:CDSS-Based AI Healthcare Solutions

Kang'an International:One-Stop Preclinical/Clinical CRO/CMO/CSO Service Platform for Pharmaceutical Companies Expanding into Southeast Asia

MediTrust Health:Industry-Leading Innovative Healthcare Service Platform

Quege Psychology:Comprehensive Digital Mental Health Platform

Tongshu Gene:Pioneer in Tumor Liquid Biopsy Gene Technology

MicroCloud AI:An International Industrial AI Group with Artificial Intelligence, Robotics, and Machine Vision as Its Core Technologies

Yisheng Jiankang:Women's Health At-Home Testing and Health Management Service Platform

The above is an excerpt from the “2022 Future Healthcare 100 Growth Report.” For the full report, please scan the QR code below.

For more detailed information on the listed companies, please scan the QR code below.