China Re Life and Magsci Health Release First Sustainable Development Report on People's Benefit Insurance to Ensure Its Stable and Healthy Growth

In recent years, a wave of “Huiminbao” (city-specific supplemental medical insurance) has swept across China, sparking strong public enthusiasm. Local governments, insurance companies, and third-party institutions have all entered the market, accelerating the implementation of Huiminbao in major cities. Consequently, ensuring its long-term, healthy, and sustainable development has become a topic of utmost concern to all sectors of society.

Recently, China Re Life Insurance, a leading player in China’s insurance industry, together with MedXin Health, an innovative medical and health service platform, released the “Series Research Report on the Development and Outlook of China’s Huiminbao Business – Insights into the Sustainable Development Trends of Huiminbao in 2022” (hereinafter referred to as the “Research Report”). The report analyzes the macro environment and development trajectory of the current Huiminbao industry and provides an outlook on its future development trends.

It is understood that the *Research Report* outlines the development trajectory of Huiminbao (city-specific supplemental medical insurance) in recent years, analyzes trends in enrollment and claims through case studies and data analysis, and proposes development recommendations across six dimensions: development positioning, product design, commercial insurance catalogs, data sharing, industry integration, and product innovation.

As a key participant in the Hui Min Bao (inclusive commercial health insurance) market, Medbanks Health continues to collaborate with insurance companies on business development, fostering the sound and sustainable growth of Hui Min Bao programs. On June 5, 2022, enrollment officially opened for Renmin Puhui Bao (Tianjin); on June 6, the upgraded “Hangzhou Citizen Insurance 2022” was launched; Inner Mongolia’s Hui Min Bao also went live on June 10; and enrollment for the 2022 editions of Shanghai’s Hu Hui Bao and Qingdao’s “Qindao e-Bao” has recently commenced.

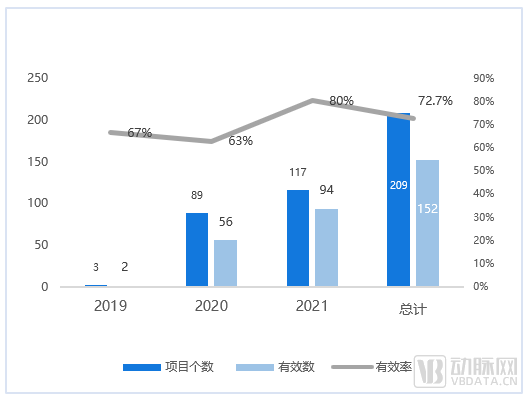

Behind the Rapid Growth of Magnesium Health Lies the Booming Huiminbao Market. According to data from the "Research Report," by the end of 2021, more than 200 "Huiminbao" products had been launched across 27 provinces, with total enrollments reaching 140 million and total premium income exceeding RMB 14 billion. Among these, 94 Huiminbao products were newly launched in 2021 alone, accumulating 101.17 million enrollees, representing a 152% increase compared to 2020.

Overall Marketed Product Statistics

In terms of the insured population, Huiminbao has currently achieved two qualitative breakthroughs, enabling near-universal coverage.

First, the expansion of coverage for the elderly population has been achieved. Based on a rough statistical summary of the age structure of Huiminbao enrollees across various regions, individuals aged 60 and above account for approximately 35% of the total. According to the overall age estimation of Huiminbao policyholders in the "Research Report," the coverage rate of Huiminbao for the population aged 60 and above exceeds 10%.

Second, the insured population has expanded from healthy individuals to those with a history of critical illnesses. Among the reimbursement models for individuals with a history of critical illnesses, the model represented by Hangzhou’s “Xihu Yilianbao” is at the forefront; it addresses equity concerns, with some products providing coverage levels for these individuals that are consistent with those for healthy individuals.

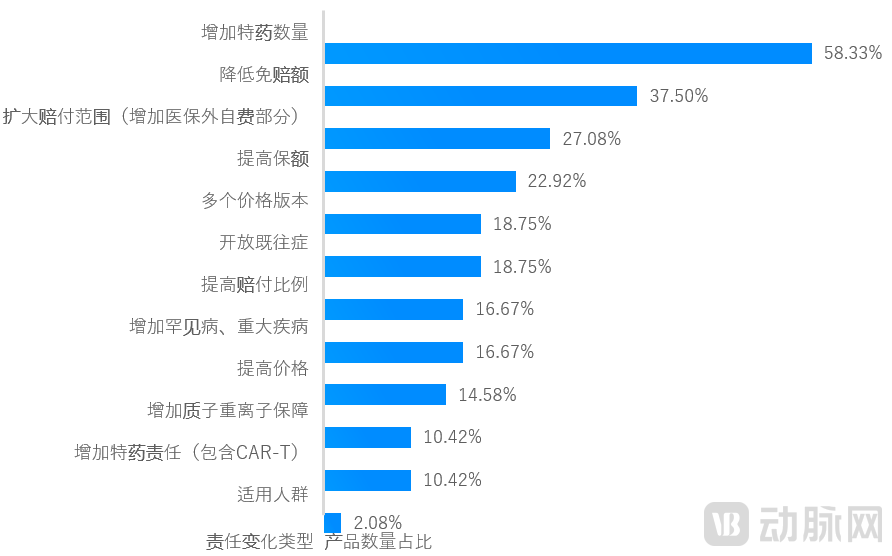

In terms of coverage scope, the liability coverage of Huiminbao has extended from covering only medical expenses within the basic medical insurance scheme to including those outside it. Adjustments to special drug coverage are the primary means of expanding this scope. The Research Report analyzed 48 renewal products launched throughout 2021. Compared with products from the previous year, only 14.58% increased their premiums; 58.33% expanded coverage by increasing the number of drugs included in special drug coverage; and an additional 10.42% added special drug coverage.

Statistics on Changes in Policy Coverage for 48 Renewal Insurance Products in 2021 Compared to 2020

Meanwhile, the Huiminbao market is gradually becoming more standardized, forming a development model characterized by the joint participation of “the government + insurance companies + third-party service providers.” For instance, in Shanghai’s “Hu Hui Bao” project, the co-insurance consortium provides system operation support, while MedXin Health has served as the specialty drug service provider for Hu Hui Bao for two consecutive years.

The rapid and high-quality development of Huiminbao (inclusive commercial health insurance) is inseparable from government participation and support. The Research Report found that between 2020 and 2021, the level of government involvement and support for Huiminbao increased significantly. Therefore, judged from the perspective of government actions, Huiminbao will be a crucial component of the future multi-tiered medical security system.

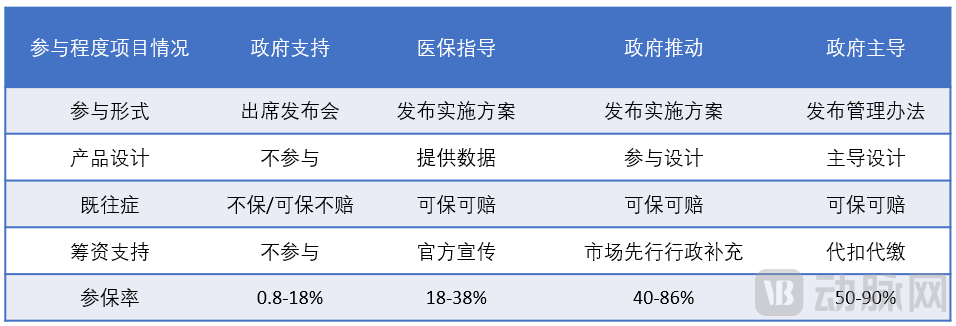

Based on the varying levels of participation in Huiminbao (inclusive supplementary medical insurance) across different regions of China, these schemes can be categorized into four types: government-supported, health insurance-guided, government-promoted, and government-led.

Forms of Government Involvement

Among these four models, the level of government involvement deepens progressively. An analysis of government-participated projects reveals that the most intuitive manifestation of government support for Huimin Bao (city-specific supplemental medical insurance), as represented by the National Healthcare Security Administration, lies in whether individual medical insurance accounts are permitted to be used for premium payments.

For instance, in the Huiminbao (city-specific supplemental medical insurance) product projects from 2020 to 2021, the average enrollment rate for plans allowing payment via personal medical insurance accounts was 15.1%, significantly higher than the 3.8% observed for plans without such support. In 2021, more than half of the product projects opened up eligibility for enrollment using personal medical insurance accounts (covering both initial enrollments and renewals), marking a substantial increase compared to 2020. The majority of enrollment volume in 2021 also came from cities that permitted the use of personal medical insurance accounts, with these cities accounting for 70% of the total market enrollment volume for the year.

It is evident that government participation and support are crucial for the sound and rapid development of Huiminbao (city-specific supplementary medical insurance). From 2020 to 2021, the intensity of government involvement and support increased significantly. Judging from governmental actions, Huiminbao is poised to gradually become a vital component of the multi-tiered healthcare security system.

Of course, while government agencies represented by the National Healthcare Security Administration have participated in and supported these initiatives, they have also raised demands for expanding the coverage population of Huimin Bao (city-specific supplemental medical insurance). As is well known, traditional commercial health insurance imposes strict requirements on age and health status, thereby excluding many elderly individuals, substandard risks, and patients with critical illnesses from obtaining coverage.

However, with the exception of a few specific items, Huiminbao (city-specific supplementary medical insurance) allows enrollment for the entire population. This represents a qualitative breakthrough in insurability for individuals previously excluded by commercial insurers. Such inclusivity has stimulated insurance uptake among these groups and made the commercial health insurance industry fully aware of the substantial untapped potential in meeting the insurance needs of non-high-net-worth individuals. This further underscores the critical role of Huiminbao as an integral component of the multi-tiered healthcare security system.

For high-risk products such as Hui Min Bao, which cover and provide compensation for pre-existing conditions, achieving high-quality, sustainable development has become the focal point of the entire market. In this regard, the Research Report points out that, logically, the sustainable development of Hui Min Bao requires achieving both funding sustainability and payment sustainability. Funding sustainability refers to maintaining a sufficiently large enrollment base over time, while payment sustainability entails effective cost control in fund management.

On the funding side, Huiminbao needs to address the challenge of maximizing enrollment and renewal rates to sustain high participation levels. Key factors influencing enrollment include product pricing, government involvement, and customer experience.

On the payment side, Huiminbao needs to address three key issues: what services should be covered by the fund, how much should be reimbursed, and how payments should be processed.

Among the Huiminbao projects launched between 2020 and 2021, over 80% included coverage for self-paid specialty oncology drugs purchased outside hospitals. These high-cost medications required for ongoing outpatient cancer treatment were incorporated into the coverage scope through a positive list mechanism under commercial insurance. Currently, coverage for self-paid specialty oncology drugs obtained outside hospitals has become a standard feature of Huiminbao products.

The advantage of this approach lies in the professionally designed positive list for out-of-hospital specialty drugs. By including medications for major diseases with high local prevalence, it achieves reasonable cost control. Meanwhile, through dynamic adjustments, innovative drugs and advanced medical technologies can be incorporated into the list in a risk-controllable manner, ensuring dynamic alignment with the National Reimbursement Drug List (NRDL). This enables the limited insurance fund to cover more and better medicines.

While there are benefits, there are also risks. Currently, in-hospital out-of-pocket expenses often lack effective cost control management. Data on current claims payouts for city-specific supplemental medical insurance (Huiminbao) indicates that the risk associated with covering in-hospital out-of-pocket expenses is gradually increasing. Surveys conducted in cities with higher claims risks reveal that claim analysis results show Huiminbao funds are not being fully utilized for reimbursement of critical and severe illnesses, but rather for medical services aimed at improving quality of life. This deviates from the fundamental positioning of Huiminbao.

Accordingly, the Research Report points out that it is imperative to expand the self-pay specialty drug coverage list for tumors in future Huiminbao plans: from out-of-hospital to in-hospital drugs; from oncology to critical and catastrophic diseases; and from single drugs to a broader scope encompassing pharmaceuticals, medical devices, consumables, and diagnostic and treatment services.

“The Research Report” points out that the current positioning of Huiminbao is reflected in its supplementary role to basic medical insurance, as well as its role in triggering a profound transformation in the structure of health insurance products. Therefore, where the future development of Huiminbao will head, and how much impact it will have on the multi-tiered medical security system, the structure of health insurance products, and their future development, will be an important issue.

Future Huiminbao products require that the leading entities of Huiminbao initiatives adopt a stronger baseline mindset and professional approach, continuously accumulate experience, analyze product issues, and optimize product design. Meanwhile, they should actively embrace industrial integration, strengthen the linkage between insurance and the pharmaceutical industry from the perspective of product design, and provide inexorable momentum for the sustainable and healthy development of Huiminbao.

Furthermore, given that the affordable pricing of Huimin Bao makes it infeasible to cover all self-pay drugs and medical consumables, cost containment will become a prominent requirement for these plans in the future. Experience from the management of China’s National Basic Medical Insurance indicates that establishing formularies is an effective measure to control fund expenditures, safeguard fund security, and promote the rational use of clinical pharmaceutical technologies.

Therefore, the Research Report states that commercial medical insurance can enhance fund payment efficiency by reasonably formulating the Huiminbao (inclusive health insurance) drug and service catalog, thereby enabling limited funds to meet more and better healthcare needs. Drawing on the mechanisms of the National Basic Medical Insurance Drug Catalog, and leveraging the opportunity presented by Huiminbao, efforts should be made to explore the theoretical foundations, practical applications, and operational mechanisms for implementing commercial insurance catalogs.

The Research Report also recommends facilitating the interconnectivity and data sharing between social health insurance and commercial health insurance. As a high-frequency medical insurance product, Hui Min Bao creates an even more urgent need for integrating social and commercial health insurance data, whether for efficient underwriting and claims processing, precise cost control, cost estimation, or risk management.

Therefore, there is an urgent need for government departments to strengthen the standardized management of data related to Huiminbao insurance schemes.

First, standardize data collection and application, including data acquisition, invocation, storage, and interface connectivity;

Second, standardize the eligible entities and forms for connectivity, clearly defining the entities responsible for interfacing with medical insurance data and those responsible for interfacing with insurance company data;

Third, increase the openness of medical insurance data and promote orderly interconnection and sharing through the application of insurtech.

Once Huiminbao breaks the traditional pattern of insurance companies operating in isolation, it can successfully attract cross-sector participation from the government, third-party service providers such as Medbanks Health, and pharmaceutical industry stakeholders. By leveraging their respective resource endowments, Huiminbao and various market entities can foster innovative industry-finance collaboration, achieve sustainable development, and jointly explore new opportunities in future infrastructure.

It is understood that this Research Report serves as the flagship publication in the series. In the future, China Re Life Insurance and MedXin Health will continue to release a series of thematic reports, elaborating on various topics centered around this Research Report. These topics will include diverse and high-profile issues such as Huiminbao product design, data analytics, and infrastructure development, thereby continuously safeguarding the steady and healthy development of Huiminbao.