Shantou Ultrasonic Instruments Institute, Pioneer of Domestic Ultrasound, Files for GEM IPO

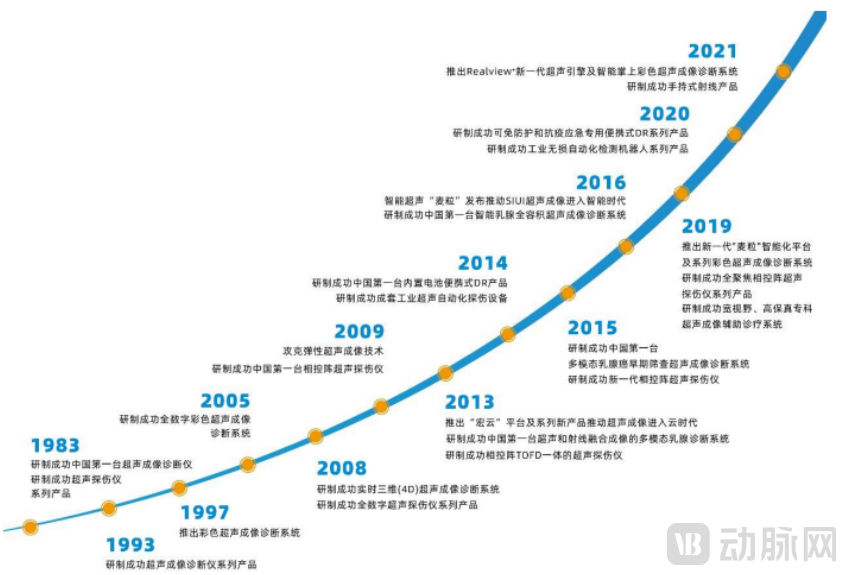

In the early 1980s, during the springtime of China’s reform and opening-up policy, a surge of foreign enterprises flooded into the country. The nascent domestic medical device sector suffered a disruptive blow and quickly ceded market share. It was not until 1983, when the CTS-18 B-mode ultrasound diagnostic system made its debut, that the first clarion call for domestic substitution was sounded, breaking the monopoly of imported B-ultrasound equipment and ending the era of zero domestically produced units in China.

The company that undertook the R&D of this ultrasound system is Shantou Ultrasonic Instrument Research Institute Co., Ltd. (hereinafter referred to as “Shantou Ultrasound”), a Guangdong-based enterprise whose predecessor was the Shantou Ultrasonic Instrument Research Institute, established in 1978. Its director, Yao Jinzhong, known as the “Father of Chinese Ultrasound,” previously worked as a radio repairman at the Shantou Radio Factory.

Under the leadership of Yao Jinzhong, SIUI achieved full self-sufficiency in corporate costs as early as 1988, transforming from a research institution with total assets of just over RMB 3 million into an industrial giant with total assets reaching RMB 170 million, thereby becoming a pioneer in China’s medical device technology sector.

Nevertheless, despite the significance of the first B-mode ultrasound device, GPS had already leveraged Kepler’s principles to enter the era of color Doppler ultrasound. Surviving in such a narrow market niche was no easy feat; Shantou Ultrasound spared no effort and finally launched its color ultrasound imaging diagnostic system in 1997 after acquiring the U.S. company ATL.

In 2002, Yao Jinzhong, who had retired from Shantou Ultrasound (SIUI), did not rest on his laurels. He led a team to establish Sonoscape Medical Corp., dedicating himself entirely to the research and development of domestically produced color Doppler ultrasound systems. In 2004, the company successfully launched China’s first portable color Doppler ultrasound system, the SSI-1000, and introduced this product to the global market.

Regrettably, Yao Jinzhong, who had long served as Chairman of Sonoscape Medical, did not live to see the full rise of China’s domestically produced ultrasound industry. On October 27, 2009, this elder statesman, who had devoted his life to the nation’s ultrasound instrumentation cause, passed away due to illness, leaving behind two ultrasound enterprises still in their developmental stages.

Over the following decade, SIUI and Sonoscape pursued their respective paths in the ultrasound sector. Carrying forward Mr. Yao’s legacy, Sonoscape finally entered the secondary market in 2017, embarking on a new chapter of growth.

Although SIUI acted slightly later, it also filed its prospectus with the ChiNext board on June 15 this year. However, as SIUI enters a new era, its ultimate destination may no longer be ultrasound.

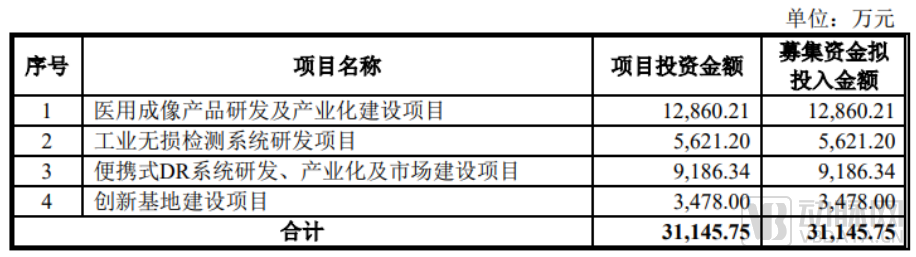

According to the prospectus submitted by SIUI, the company plans to raise RMB 311.4575 million in this IPO. The proceeds are earmarked for four areas: the R&D and industrialization project for medical imaging products, the R&D project for industrial non-destructive testing systems, the R&D, industrialization, and market development project for portable DR systems, and the innovation base construction project.

Use of Proceeds from SIUI's Fundraising

Projects related to medical ultrasound applications are included in the R&D and industrialization project for medical imaging products, with a planned investment of 129 million yuan, accounting for 41.5% of the total financing.

The prospectus reveals that SIUI is channeling this portion of funds entirely into the research, development, and industrialization of high-end breast ultrasound systems, with the aim of capturing the specialized market for breast diagnostics. Notably, nearly 60% of the funds are not being allocated to medical ultrasound applications.

To clarify the flow and purpose of the funds, let us examine the three data points provided by SIUI.

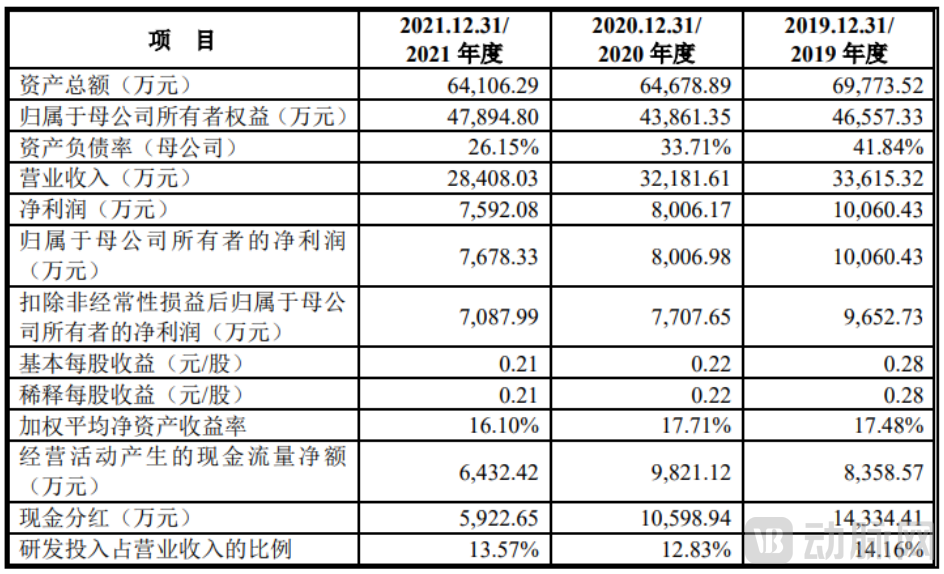

First, regarding the operating performance during the reporting period: for the three fiscal years 2019, 2020, and 2021, the Issuer’s operating revenues were RMB 336.1532 million, RMB 321.8161 million, and RMB 284.0803 million, respectively, while its net profits were RMB 100.6043 million, RMB 80.0617 million, and RMB 75.9208 million, respectively. Both operating revenue and net profit exhibited a downward trend, primarily attributable to the impact of the COVID-19 pandemic and the lag in sales strategies in the post-pandemic era.

SIUI: Key Financial Data and Financial Indicators

SIUI: Key Financial Data and Financial Indicators

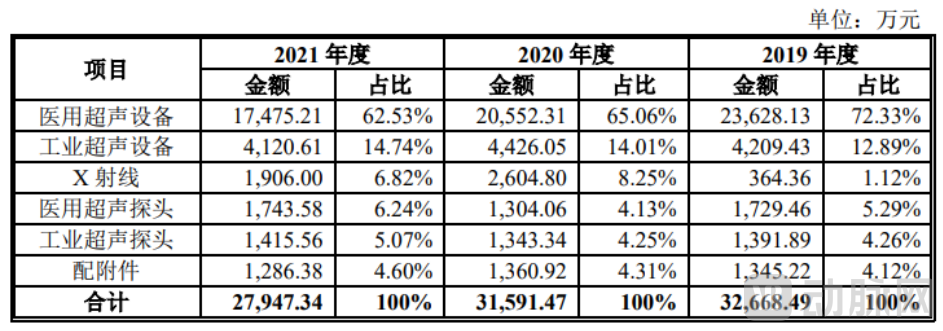

Next is the composition of revenue from principal business activities. SIUI is the company with the most concentrated business portfolio in the medical device sector, deriving its primary revenue and profits from low-end medical ultrasound systems and industrial non-destructive testing (NDT) ultrasound equipment. During the reporting period, revenue from ultrasound equipment accounted for 94.77%, 87.45%, and 88.58% of total revenue from principal business activities, respectively.

Let’s examine SIUI’s gross profit margins over the past three years. During the reporting period, the company’s gross profit margins from its core business were 69.17%, 64.62%, and 66.87%, respectively, on par with its peer Mindray Medical, both ranking among the industry leaders and serving as the cornerstone of SIUI’s steady growth.

Overall, the rise and fall of SIUI is deeply intertwined with the ultrasound industry. Its long-term investment in the ultrasound field has helped SIUI build a complete product portfolio and a sales network for low-end ultrasound systems, resulting in sustained high gross margins. However, from the perspective of corporate growth, its reliance on a single product structure and limited market coverage has left it unable to cope with systemic crises or achieve leapfrog growth.

Revisiting the Use of IPO Proceeds by SIUI. High-end specialized breast ultrasound systems, portable DR units, and industrial non-destructive testing systems all signal SIUI’s move beyond its traditional business lines, aiming to achieve dual breakthroughs in both production capabilities and sales models.

In other words, SIUI’s fundraising and listing initiative marks the commencement of both horizontal and vertical expansion.

From the release of “Made in China 2025” to the “14th Five-Year Plan for the Development of the Medical Equipment Industry,” China has introduced a series of policies that directly support the innovative development of domestic medical devices. In terms of regional healthcare system construction, policies such as “tiered diagnosis and treatment” and “the development of county-level medical consortia,” coupled with the trend of “domestic substitution,” have opened up market channels for Chinese-made medical devices at the grassroots level.

As overseas companies such as GE and Hitachi have long dominated China’s high-end ultrasound market and achieved significant scale, domestic enterprises seeking to break this stranglehold must first invest heavily in R&D for technological innovation, then extensively build out sales channels across China, and gradually gain hospital recognition after market entry.

Every step of the process is indispensable; neither the explicit sales and R&D costs nor the potential time costs are bearable for ordinary joint-stock companies. Therefore, domestic ultrasound brands typically deploy only a limited number of products in the mid-to-high-end ultrasound market, while focusing their efforts on the low-end market to capture share through cost and pricing advantages.

SIUI has consistently adhered to this strategic approach, maintaining its position among the top three domestic brands in China’s low-end market for an extended period. It ranks just behind Shenzhen Mindray and engages in fierce competition with Sonoscape Medical. Data indicates that in 2019, the primary healthcare market involved 31 domestic ultrasound brands, which collectively held a market share of over 75%. Among these, the three major brands—Shenzhen Mindray, Sonoscape Medical, and SIUI—accounted for more than 60% of the market share.

However, the low-end market has always had its inherent limitations.

First, low-end ultrasound systems are primarily deployed in primary healthcare settings. Compared to the plethora of ever-emerging ultrasound devices, many grassroots regions suffer more from a shortage of physicians skilled in ultrasound operation. Second, the technological barriers for low-end ultrasound are relatively low, creating vulnerability to disruptive competition from other enterprises. Third, under the “County Medical Community” and “Thousand Counties Plan” initiatives, county-level hospitals are experiencing growth, with increased demand stemming largely from the mid-to-high-end market rather than the low-end segment. Fourth, while primary healthcare institutions procure ultrasound systems through government centralized bidding—where transactions are conducted with the Health Commission—enterprises must now adapt to the more market-driven procurement processes of county-level hospitals. Particularly regarding the fourth point, the costs associated with rebuilding sales teams and the highly uncertain product adoption landscape will pose significant challenges to these enterprises.

As of 2019, both SIUI and Sonoscape held single-digit market shares in district and county-level hospitals. To capture emerging markets, SIUI must now increase its R&D investment and accelerate the commercialization of mid-to-high-end ultrasound systems.

SIUI’s strength lies in its comprehensive product portfolio. Through years of independent research and development innovation, the company has mastered functional imaging technologies ranging from structural organ imaging to organ motion analysis and elastography. It has established a complete intellectual property system covering core proprietary technologies, spanning image processing algorithms, image analysis software, core probe components, and whole-system design and development. This has enabled SIUI to offer a full range of products, including general-purpose color Doppler ultrasound systems, specialty clinical color Doppler ultrasound systems, portable color Doppler ultrasound devices, handheld wireless color Doppler ultrasound units, and AI-powered cloud platform solutions.

SIUI’s diverse product portfolio enables it to expand horizontally with relative ease. For instance, in recent years, there has been heightened focus on screening for the two major cancers affecting women. In response, SIUI offers specialized breast ultrasound solutions that provide automated full-volume breast scanning, which can be used not only for diagnostic purposes by physicians but also to assist surgeons in preoperative planning for breast procedures. Similarly, with the recent emergence of veterinary imaging equipment, SIUI has rapidly launched a series of related devices, catering to the varied ultrasound needs of different pet hospitals.

Overall, it is not difficult for SIUI to move beyond the low-end ultrasound market and shift its revenue streams toward the mid-to-high-end segments. This financing round also demonstrates its determination to break away from the entrenched perceptions associated with domestic Chinese ultrasound manufacturers.

However, the goal is to shift from the low-end market to the mid-to-high-end segment. At present, the company has yet to break away from the established pattern of having a single product structure, with the majority of its revenue and profits derived from ultrasound products. Looking ahead, portable DR systems are poised to become SIUI’s second growth curve, reshaping its current business landscape.

Portable DR systems are generally categorized into low-dose DR devices designed for small clinics and community healthcare settings, and high-end portable DR systems suited for disaster relief and field hospital applications.

The "2022-2026 China DR Medical Equipment Industry Market In-Depth Research and Development Trend Forecast Report" shows that in 2021, the procurement volume of DR systems in China reached 6,138 units, with a transaction value of RMB 8.2 billion; mobile DR has low penetration and a small market capacity.

However, with the Chinese government increasing its support for new hospital infrastructure and the continued ravages of the COVID-19 pandemic, mobile DR was included in the “Emergency Medical Supplies Reserve List for Major Epidemic Treatment Bases” in 2020, leading to a surge in market demand for mobile DR.

Currently, domestic alternatives have basically replaced imported products in the conventional DR equipment market in China. However, in the high-end DR equipment sector, foreign companies still hold nearly 50% of the Chinese market share, leveraging their advantages in technology, brand reputation, quality, and first-mover position. Therefore, by entering this segment, SIUI is most likely aiming to capitalize on the trend of domestic substitution and compete with Chinese manufacturers such as United Imaging, Mindray, Wandong, Angell, and Perlove.

SIUI began researching portable DR systems in 2010. According to the company’s publicly available information, the main advantages of its portable DR are its lightweight design, weighing only slightly over ten kilograms, and its achievement of a new low in radiation dose for DR imaging.

Based on the changes in SIUI’s core business composition, it can be inferred that during the 2020 pandemic, sales of this equipment surged by as much as 615.38%, before easing slightly in 2021 while still contributing nearly RMB 20 million in revenue.

Main Components of SIUI's Core Business

From the current competitive landscape, it is entirely feasible for SIUI to generate an additional RMB 300 million in revenue by leveraging portable DR systems within this RMB 10 billion market. However, in the long run, as more domestic medical device manufacturers enter the fray, SIUI will need to either expand its distributor network through a public listing or penetrate overseas markets to make a significant impact in this sector.

Both paths may become options for SIUI. As for the ultimate outcome, we must wait for time to provide the answer.

When Pioneers of Medical-Engineering Integration Enter the Secondary Market

The development journey of Shantou Ultrasound serves as a microcosm of China’s small and medium-sized medical imaging equipment manufacturers. Decades of diligent research have enabled breakthroughs from scratch, progressing from component development to the manufacture of complete systems. Throughout this process, there was virtually no capital intervention; every “national first” achieved was the result of step-by-step exploration by the company’s scientific researchers.

Yet, whenever it reaches a crossroads in the secondary market, the many achievements earned through the company’s arduous efforts invariably invite investor skepticism about its vitality.

Four Decades of Operation: SIUI Creates Multiple “Firsts in China”

Four Decades of Operation: SIUI Creates Multiple “Firsts in China”

Such bias is often unnecessary. Having survived the perilous journey of entrepreneurship and emerged victorious amidst the fierce competition from foreign medical device manufacturers, SIUI possesses its own profound heritage and strength.

Reviewing the development of technologies such as Doppler color ultrasound, automated breast volume scanner (ABVS), and AI-assisted diagnostic systems, SIUI has not missed any emerging trend. Instead, it has seamlessly integrated each innovative technology into its existing product portfolio, with steady and sustained growth serving as testament to its ability to keep pace with the times.

With this financing and listing, SIUI’s years of accumulated expertise are now bolstered by capital strength. If the company can leverage this opportunity to expand its sales channels, accelerate the commercialization of research and technological achievements, and fast-track its intelligent digital transformation, SIUI may well reclaim a leading position among domestically produced medical device manufacturers and write another brilliant chapter in its history.