Mega Genomics Debuts as China's First Consumer Genomics Stock, Unlocking the Value of Tens of Millions of Genetic Data

On June 22, Meiyin Gene officially listed on the Hong Kong Stock Exchange, raising over HK$200 million. In the grey market trading the day before, its opening price surged by more than 20%, with its market capitalization briefly exceeding HK$5 billion.

After many twists and turns, this debut has once again drawn market attention to the genetic testing sector, which had become somewhat lackluster. It took Only 7 years for Meinian Gene to go from establishment to IPO. Over the past seven years, Meinian Gene has grown into a giant in China's genetic testing services industry: it has completed over 12 million genetic tests cumulatively. Based on its 2021 testing volume, it averaged more than 246,000 tests per month, making it the largest consumer-grade genetic testing platform in China.

Meinuo Gene has consistently been a star project in the primary market. During its two funding rounds prior to the IPO, Meinuo Gene successively attracted top-tier investment institutions and industrial funds, including Maccura Biotechnology, Hengsai Qingxi, Shanghai E Fund, Tibet Tengyun, Ganzhou Zhangxin, and Suzhou Ruihua. Notably, upon completing its Series A financing in its year of establishment, Meinuo Gene had already achieved a valuation of RMB 1 billion, joining the ranks of innovative unicorns. It is worth noting that during the IPO phase, existing shareholder Maccura Biotechnology further increased its stake in Meinuo Gene by participating as a cornerstone investor.

In reality, discussions surrounding Meiyin Gene have never ceased. Its intrinsic growth capability has been heavily challenged by its equity and business ties with its major shareholder, Meinian Onehealth. However, setting these aside, Meiyin Gene’s success can be attributed to 70% excellence and 30% luck: at its inception, it leveraged the channel network of the leading private health checkup provider to rapidly achieve commercial scale for its products; later, amidst this transition, it benefited from the explosive demand for COVID-19 nucleic acid testing, which stabilized its growth momentum. Therefore, what sustainable growth mechanism has Meiyin Gene actually built, and what new clues does this offer for our understanding of the highly promising gene testing industry? This may well be the greatest value of this IPO.

For Meiyin Gene, 2018 and 2021 were two pivotal years, with two key transformations jointly shaping the company as it stands today.

In 2016, Meinian Gene was incubated by Meinian Onehealth. At that time, technological innovations were propelling genetic testing into the spotlight, and Yu Rong, Chairman of Meinian Onehealth, was keen to seize this opportunity. His vision quickly materialized after he met Xiao Zhe. Xiao had previously worked in the Medical Health Department of BGI Research, focusing on cancer genetics and the development and promotion of personal genomic products. He later joined Novogene to concentrate on medical product development and was equally optimistic about the application prospects of consumer-grade genetic testing. Consequently, Tianyi Assets, the parent company of Meinian Onehealth controlled by Yu Rong, invested RMB 167 million to incubate Meinian Gene, with Xiao Zhe appointed as its first CEO. In its early stages, Meinian Gene rapidly achieved critical technological accumulation, charting the course for its subsequent rapid business expansion.

In 2018, Meinian Onehealth acquired a controlling stake in Meiyin Gene to strengthen the strategic synergy between the two entities. Shanghai Tianyi Asset transferred its 33.42% equity interest in Meiyin Gene to Meinian Onehealth for RMB 388 million. Notably, as part of this equity transfer, Shanghai Tianyi Asset entered into a valuation adjustment mechanism (VAM) agreement with Meinian Onehealth, guaranteeing that Meiyin Gene’s net profits for 2018, 2019, and 2020 would reach no less than RMB 42.6273 million, RMB 88.6608 million, and RMB 123 million, respectively. This transaction marked a significant turning point for Meiyin Gene.

Subsequently, leveraging the platform traffic and commercial support of Meinian Onehealth, Meiyin Gene became the only consumer-grade genetic testing company in China to achieve profitability. Between 2018 and 2019, among Meiyin Gene’s operating revenues of RMB 196 million, RMB 124 million, and RMB 203 million, the revenue derived from transactions with Meinian Onehealth and its affiliated enterprises accounted for 47.4%, 51.1%, and 57.9% of the total revenue during the respective periods.

The change occurred in 2021, as Meinian Gene gradually divested itself from the influence of Meinian Onehealth. Although Meinian Onehealth remained the largest shareholder of Meinian Gene prior to its IPO, its stake fell to less than 20% after several rounds of share reduction.

The underlying reason is that from 2018 to 2020, Meiyin Gene reported profits of RMB 22.04 million, RMB 29.69 million, and RMB 79.10 million, respectively. Despite achieving profitability, it failed to meet the performance targets stipulated in the valuation adjustment mechanism (VAM) agreement, prompting Meiyin Gene to shift its strategy toward growth driven by internal capabilities.

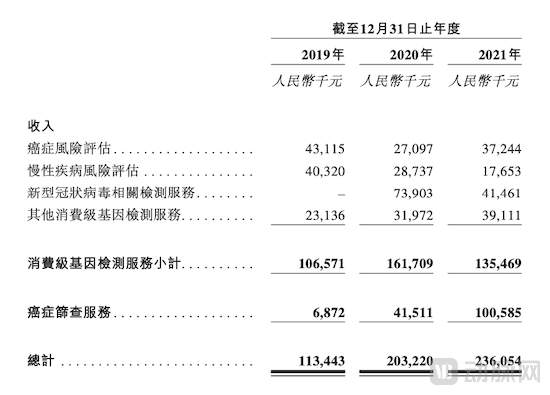

This marked the second major turning point for Meiyin Gene, as adjustments to its equity and organizational structures led to an immediate surge in both the revenue scale and proportion of its cancer screening business. From 2019 to 2021, revenue generated from cancer screening services skyrocketed from RMB 6.872 million to over RMB 100 million, representing a compound annual growth rate (CAGR) of nearly 40%. Meanwhile, the share of this business segment in total revenue grew from 6% to 42.6%. In its prospectus, Meiyin Gene also stated that it would further increase R&D investment in in vitro diagnostic (IVD) products for cancer screening.

Meiyin Gene Revenue Data Source: Prospectus

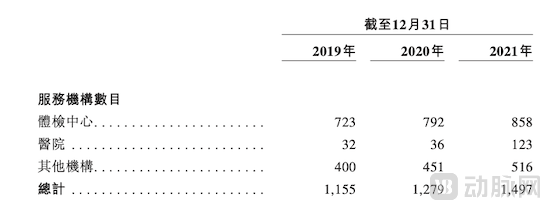

A closer look at the prospectus reveals that 2021 held significance for Meiyin Gene beyond the surface level, with more profound changes occurring in the adjustment of its user structure. According to the prospectus, the number of hospital clients served by Meiyin Gene increased from 36 in 2020 to 123 in 2021. This growth aligns with the company’s strategic shift from consumer-grade genetic testing toward cancer screening with a stronger emphasis on clinical evidence, and it also lays the commercialization groundwork for its upcoming in vitro diagnostic (IVD) products.

Meiyin Gene User Structure Data Source: Prospectus

“Building a genetic gateway for the Chinese population.” This sentence on the homepage of Because of Health’s website also elucidates the underlying logic behind the company’s business boundary expansion. Born during the period of blind, rapid growth in China’s consumer-grade genetic testing industry and having matured amidst the fierce “red ocean” competition of the early market, Because of Health—leveraging channel advantages from its parent company alongside a powerful combination of product, marketing, and R&D strategies—is now in its prime.

First, by accurately grasping market demand, Meinian Gene has built a targeted product portfolio. With a long-term focus on screening for diseases caused by common genetic defects, Meinian Gene is likely the consumer-grade genetic testing service provider that best understands the needs of Chinese users.

Research indicates that many disease-causing genetic defects are deleterious. For instance, common ApoE gene variants may affect the synthesis of apolipoprotein E, a human lipoprotein present in serum and the central nervous system, thereby influencing blood lipid regulation, cholesterol homeostasis, and neuronal regeneration in the central nervous system. These variants are highly correlated with the onset and progression of cardiovascular and cerebrovascular diseases. Similarly, MTHFR gene abnormalities may lead to impaired folate metabolism, thereby increasing the risk of H-type hypertension, coronary heart disease, stroke, and other cardiovascular and cerebrovascular conditions. Furthermore, the risk of developing high-incidence cancers—such as gastric cancer, colorectal cancer, liver cancer, breast cancer, thyroid cancer, prostate cancer, and pancreatic cancer—is often associated with specific susceptibility gene variants.

These genetic variants are highly prevalent in the general population, yet they typically evade detection by conventional screening methods, thereby missing opportunities for early disease warning. Because of Health has timely filled this market gap by offering consumer-grade genetic testing services tailored to the Chinese population. These services include nutrigenomic testing—such as assessments of folate metabolism and vitamin absorption capabilities—as well as risk assessments for specific diseases based on susceptibility genes, including ApoE genotyping, cancer risk evaluation, and ankylosing spondylitis risk assessment. This strategy has enabled Because of Health to rapidly capture market share. According to its prospectus, measured by 2020 revenue, the company’s consumer-grade genetic testing services accounted for 34.2% of the Chinese market, ranking first and surpassing its closest competitor by a factor of three.

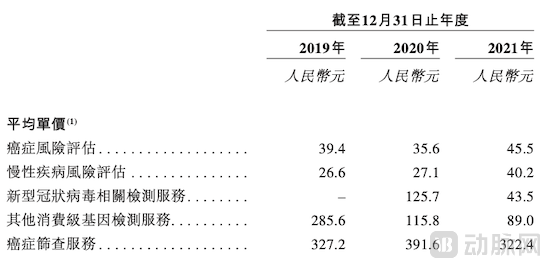

Secondly, Meinian Gene has continuously consolidated its competitive advantage in the market. According to the prospectus, from 2019 to 2021, the number of consumer-grade genetic tests completed by Meinian Gene remained at approximately 2.7 million, while the average unit price of its corresponding main testing services increased year by year. Specifically, cancer risk assessment and chronic disease risk assessment constitute the primary components of the consumer-grade genetic tests offered by Meinian Gene. The former includes P53 tumor suppressor gene testing, single-cancer risk assessment testing, DNA repair capacity evaluation, high-incidence cancer risk assessment packages, and comprehensive cancer screening risk assessment packages. The latter includes ApoE gene testing, folate metabolism capacity evaluation, and cardiovascular and cerebrovascular disease risk assessment packages. Among these, the average unit price for cancer risk assessment services rose from RMB 39.4 to RMB 45.4, while the average unit price for chronic disease risk assessment services increased from RMB 26.6 to RMB 40.2.

Average Unit Price of BGI Services Data Source: Prospectus

This indicates that, while securing stable repeat purchases from users, Meiyin has maintained a strong competitive position in transactions, thereby exercising a certain degree of pricing power over its services.

Finally, based on its existing product structure and pipeline under development, Meinian Genetics has strengthened its independent R&D capabilities. Intuitively, from 2019 to 2021, even though the COVID-19 pandemic compressed demand for offline diagnosis and treatment, Meinian Genetics’ operating revenue maintained rapid growth, doubling from RMB 113 million to RMB 236 million. If the revenue generated from COVID-19 nucleic acid testing services provided since May 2020 is excluded, Meinian Genetics still recorded revenues of RMB 113 million, RMB 129 million, and RMB 194 million over the past three years, demonstrating a favorable growth trend in its traditional consumer-grade genetic testing services and cancer screening services, which have been increasingly emphasized in recent years.

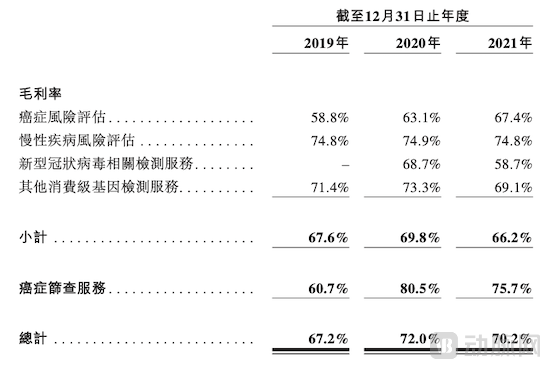

As indicated in the prospectus, Meiyin Gene has placed a significant strategic bet on cancer screening as its future growth driver. Among the eight new in vitro diagnostic (IVD) kits under development, five are clinical-grade disease screening products, with indications covering Alzheimer’s disease, colorectal cancer, gastric cancer, pulmonary nodules, and cervical cancer. The rationale behind this strategy is straightforward: since 2019, cancer screening has consistently been the business segment with the highest or second-highest gross profit margin. With the phased market launch of its self-developed IVD kits, sustained growth is clearly anticipated.

Gross Profit Margin of Meiyin Gene Services Data Source: Prospectus

Thus, Meiyin Gene has presented its response to the exploration of genetic technology applications: bridging public curiosity about genetic science with rigorous clinical practice through disease early warning. On one side lies a broad base of potential users; on the other, efficient and innovative clinical diagnostic and therapeutic tools. By educating the market through consumer-grade genetic testing and establishing cancer screening, Meiyin Gene is building a closed-loop system for major disease screening.

Exploring Application Scenarios for Genetic Testing: An Attempt at “Crossing the River by Feeling the Stones”From the fierce competition in consumer-grade genetic testing to the red-ocean battle in oncology genetic testing, and further to tapping into both in-hospital and out-of-hospital markets for early cancer screening, each shift in application scenarios for genetic testing has spawned its own wealth-creation myths. Unlike Burning Rock Biotech, Genetron Health, and New Horizon Health, which focus exclusively on specific clinical medical settings, Meiyin Genetics targets the more upstream stage of disease warning and prediction.

This is a market with greater theoretical growth potential but limited scale at each stage. For Meiyin Gene, weaker demand makes market education more difficult, and post-listing operations face greater challenges.

On one hand, the domestic consumer-grade genetic testing market is expanding rapidly, yet its penetration rate is rising slowly. The market began to take shape around 2013; this late start means it remains in an early stage of development, with market education and business model exploration being the primary priorities during this period.

According to the prospectus of Because of Health, in 2020, the market size of consumer-grade genetic testing in China was nearly USD 500 million, with a compound annual growth rate (CAGR) of 31.0% since 2016. It is projected that by 2025, the market size will exceed USD 5 billion, corresponding to a CAGR of nearly 50%. Although the historical and projected growth rates surpass those of mature overseas markets, Chinese consumers have not yet fully adopted consumer-grade genetic testing as a routine component of physical examinations or health management. How to integrate genetic testing into users’ health management habits remains a key challenge for Because of Health, which boasts the largest user base in China.

On the other hand, China’s cancer screening market holds substantial growth potential but is characterized by intense competition. In 2020, China recorded 4.6 million new cancer cases, ranking first globally, with 2.7 million cancer-related deaths, placing it among the highest in the world. Numerous previous studies have demonstrated that cancer can be more effectively controlled or cured if detected at the precancerous or early stages. Conversely, delays in cancer diagnosis typically lead to significantly higher treatment costs and increased mortality rates. Early risk assessment and detection offer a range of interventions, from lifestyle modifications and health management to pharmacological treatments and surgical interventions. Precancerous lesions identified through cancer screening can often be surgically removed, thereby preventing malignant progression. This constitutes the fundamental rationale underlying the cancer screening market.

According to the prospectus of Meiyin Gene, the top five cancers in China’s cancer screening market—gastric cancer, colorectal cancer, lung cancer, breast cancer, and liver cancer—account for a total market size of RMB 8.8 billion. With continuous technological and product iterations, as well as deepening market education, this market is undergoing sustained expansion. Data indicates that the ultimate scale of China’s early cancer screening market will exceed RMB 100 billion.

For cancer screening service providers, focusing on developing solutions for high-incidence cancer types, securing first-mover advantages in sample accumulation and clinical validation, obtaining relevant regulatory approvals, and translating technology into commercial capabilities are key processes in building market barriers. Furthermore, given the low awareness and public acceptance of cancer screening among Chinese patients, the ability to effectively conduct consumer education is also a critical success factor. This means that GenePlus must undergo rigorous clinical validation to transition from a participant to a leader in the cancer screening market.

Listing in its seventh year of establishment marks a critical milestone in the company’s operations. However, to break through the ceiling of its existing business and become a participant in the broader gene technology market, MeiYin Genomics needs to deploy more sophisticated strategies across its product, market, and R&D portfolios.