Is There a Future for China's Health Insurance Industry Amid Layoffs, Pay Cuts, and Contraction?

MediTrust Health

Innovative Inclusive Health Medical Service and Security Platform

The health insurance sector, which has attracted billions in financing and drawn investments from Sequoia China, Hillhouse, IDG Capital, Sinovation Ventures, Tencent, Meituan, and Ant Group, is now facing a major crisis.

Since mid-2021, with the introduction of a series of policies including the new regulations on internet-based life insurance, and the gradual dissipation of internet dividends, the rapid growth momentum of the health insurance industry has shown signs of cooling:Multiple health insurance companies exposed to layoffs, salary cuts, and business contraction.It is reported that a leading health insurance technology company began workforce optimization at the end of last year, with its current headcount having plummeted by 80% from its peak.

For a time, market skepticism poured in.“Some health insurance tech companies in the market have merely transferred traditional offline practices to online platforms, thereby reducing themselves to tools for marketing, customer acquisition, and drug sales, without demonstrating their technological capabilities,” a senior investor who has long followed the health insurance industry told VCBeat.

Moreover, several primary market investors and industry insiders have unanimously stated that the health insurance sector is already exhibiting issues such as an overly narrow strategy, tight cash flow, overheated concepts, and inflated valuations—all of which are urgent challenges that need to be addressed.

It is worth noting that, as a niche sector favored by investment institutions, health insurance companies have seen their financing amounts rise steadily in recent years, climbing from hundreds of millions to billions of yuan. This rapid growth has quickly given rise to multiple unicorn enterprises, with some already going public.

Amid the crisis, many industry observers believe that China’s health insurance sector has no future: the current fervor in the health insurance industry is a product of capital-driven hype, the purported trillion-yuan market size is questionable, and there is a distinct lack of truly innovative enterprises.

Is the health insurance industry experiencing a bubble or genuine growth? What challenges does the industry face? Does China’s health insurance industry truly have a future? The following article provides a detailed analysis.

To explore whether China's health insurance industry has a future,The first question to address is whether the trillion-yuan health insurance market represents genuine demand or pseudo-demand?

It has been argued that there are significant differences between China’s commercial health insurance market and that of the United States, making it unreasonable to predict the development of China’s health insurance industry based on the U.S. model. Under China’s broadly covered national basic medical insurance system, commercial health insurance is not considered a necessity compared to the U.S. market, resulting in low consumer reliance on such products. Therefore, China’s health insurance industry should not take the U.S. as a benchmark; demand remains uncertain, and the overall market size is limited.

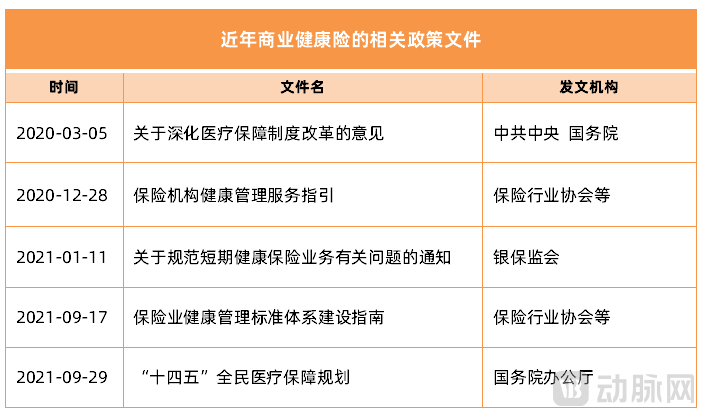

This perspective holds some merit, but it is important to recognize that although market conditions vary,Nevertheless, the development of China’s health insurance industry continues to rest on substantial foundational support: its rapid rise is, in fact, closely tied to the direction of healthcare reform.This can be gleaned from the frequent rollout of relevant policies in recent years.

More importantly, from the user’s perspective, health insurance can, to a certain extent, alleviate supply-side contradictions.: For users, the value of health insurance lies in its ability to address uncertain future medical expenses through affordable upfront premiums. After all, although most diseases are currently covered by national basic medical insurance and drug prices have shown a significant downward trend under the volume-based procurement policy, the out-of-pocket medical burden on individuals remains substantial.

Therefore, from both the policy and consumer perspectives, the demand for health insurance is genuine and robust.This is also a key driver supporting health insurance as a trillion-yuan blue-ocean market.

Of course, the challenges currently facing the health insurance industry urgently require solutions and breakthroughs from health insurance companies.

As indicated above, the health insurance market is indeed on a fast track to growth. However, amidst this sustained expansion, the entire industry continues to face significant challenges.

The primary challenge is that, despite widespread demand for medical insurance among Chinese residents, awareness and motivation to purchase commercial health insurance remain insufficient.Therefore, in the early stages of the health insurance industry’s development, user education, channel coverage, and sales innovation became key areas of focus for health insurance companies.

For instance, some small and medium-sized insurers struggle to operate long-term life insurance businesses via the internet, while their regionalized offline operations fail to achieve substantial scale due to a shortage of external marketing agents. In response, MediTrust Health, an industry leader, has established a system capable of conducting business in specific niche segments of short-term health insurance, achieving precision, specialization, and scalability.

As industry participants continue to make strategic moves, this challenge is gradually easing. However, health insurance often lacks user stickiness if efforts are limited to user education and marketing-driven customer acquisition.

In response, health insurance technology companies have begun to incorporate medical services and related coverage into their health insurance products. This aligns precisely with the broader trends in China, where population aging is accelerating and residents’ demand for medical and healthcare services is growing increasingly robust. The elderly population bears a high burden of chronic diseases, creating an urgent need for comprehensive health service support.

(Evolution of the Health Insurance Business Model, Chart by VCBeat)

(Evolution of the Health Insurance Business Model, Chart by VCBeat)

ThusIn terms of service innovation, building a “pharmaceutical-medical-insurance closed loop” has become a common consensus in the industry.: As is well known, the difficulties and high costs associated with purchasing medications, coupled with a lack of guaranteed therapeutic efficacy, are prominent issues in China’s current healthcare sector. Therefore, ensuring that high-quality medical resources are universally accessible and affordable poses a significant challenge to all stakeholders in the industry.

Taking MediTrust Health as an example, it aggregates the needs of self-paying patients and integrates healthcare with insurance, enabling patients to access cutting-edge medications and medical services at lower costs and with greater convenience. To this end, MediTrust Health has established a diversified business system encompassing patient services, commercial insurance services, and pharmaceutical company services, namely by creating three brands: Kangfu Health, Kangfu Smart Insurance, and Kangfu Smart Pharma.

How to Understand?The goal is to ensure that the general public can access, utilize, and benefit from high-quality medical resources.

For instance, in terms of practical accessibility, MediTrust Health’s active participation in Huimin Bao (city-specific supplemental medical insurance) represents a noteworthy initiative. With the exception of a few specific items, Huimin Bao allows enrollment across the entire population, thereby extending substantial coverage to individuals who were previously excluded from commercial health insurance. Furthermore, the industry places significant emphasis on comprehensive operational service capabilities for Huimin Bao. In this regard, MediTrust Health’s Kangfu Zhibao enhances the insurance value chain by providing integrated operational services for both commercial health insurance and Huimin Bao, facilitating better implementation of these insurance products and increasing enrollment rates.

In terms of “practical applicability,” MediTrust Health’s Kangfu Zhiyao serves the pharmaceutical industry by providing commercialization solutions covering the entire drug lifecycle. In terms of “service excellence,” Kangfu Health targets individual consumers, aggregating multi-party medical service resources to deliver comprehensive and high-quality healthcare experiences.

However, it is crucial to recognize that integrating the “pharmaceutical-medical-insurance closed loop” is highly challenging.The reason is that this model requires health insurance technology companies not only to possess a large base of insurance customers but also to maintain extensive service and pharmaceutical networks, as well as robust digital capabilities. This poses a significant challenge for health insurance technology companies.

For instance, during the current industry crisis, some health insurance technology companies have exhibited severe homogenization in the supply of medical services, leading to a lack of competitiveness. Despite their large scale, they have incurred substantial losses, thereby straining corporate cash flow. Therefore, establishing a closed-loop system integrating “pharmaceuticals, healthcare, and insurance” cannot be achieved merely by having a network of medical services and pharmaceutical supplies; it requires innovation and integration across multiple dimensions.

Following this line of reasoning, the second major challenge for the health insurance industry emerges: how to fully uncover users’ latent needs and drive product innovation.

For example, mainstream health insurance products currently exhibit supply-demand mismatches such as “covering healthy individuals but not substandard risks,” “providing short-term coverage but not long-term protection,” and “reimbursing only expenses within the basic medical insurance scope while excluding those outside it.” It is important to note that China has a substantial population of “substandard risks.” However, due to immature underwriting technologies and excessively high underwriting risks, insurers rarely offer insurance products tailored to this group. Consequently, a large number of individuals with pre-existing conditions are unable to select suitable insurance plans, leading to a persistent imbalance between supply and demand in the insurance industry.

It is precisely based on this issue,The market demands innovative health insurance products tailored to patients with oncology and special diseases, chronic conditions, and rare diseases.To this end, MediTrust Health’s Kangfu Health platform has developed relevant health insurance products, thereby achieving comprehensive coverage across the entire population—from individuals with pre-existing conditions to substandard and standard risks. According to official disclosures, Kangfu Health has cumulatively saved over RMB 2 billion in medical expenditures and served more than one million patients, significantly alleviating the financial burden on patients while reducing healthcare costs.

Moreover, the “Huiminbao” supplemental medical insurance products, in which MediTrust Health and insurance companies are deeply involved, are meeting a broader range of user needs. According to the report “Insights into the Sustainable Development Trends of Huiminbao in 2022,” Huiminbao has expanded coverage for elderly populations, with an estimated penetration rate exceeding 10% among individuals aged 60 and above. By the end of 2021, more than 200 Huiminbao products had been launched across 27 provinces, accumulating 140 million enrollments and generating total premium income exceeding RMB 14 billion.

It is important to note the industry background: as an inclusive supplementary medical insurance program that effectively interfaces with basic medical insurance, Huiminbao (City-Specific Supplementary Medical Insurance) constitutes a significant component of the social security system. It primarily demonstrates its inclusiveness through low entry thresholds, affordable premiums, and broad underwriting criteria, thereby imposing stringent requirements on product design.

It is evident that MediTrust Health has gradually built a high-quality system of products and services centered around user needs.

Of course, beyond user awareness and needs,The health insurance industry also faces a third major challenge: risk control security and data operations and maintenance, which largely determine whether managed care health insurance can sustain healthy operations.For instance, given the relatively weak foundation of healthcare data currently available in the market and the lack of integrated structured data platforms, it is challenging to implement actuarial pricing and risk management driven by medical data.

In response, MediTrust Health has built an intelligent insurance toolkit and technical support platform covering the entire insurance value chain—“actuarial analysis, marketing, underwriting, claims processing, and cost control”—based on real-world medical scenarios. This initiative drives data innovation, enhances end-to-end service experience, and improves policyholder renewal rates.

In summary, by linking medical service providers, pharmaceutical companies, and insurers, and leveraging its own smart technology to deliver a better healthcare experience for users, health insurance technology companies represented by MediTrust Health are helping medical service providers and insurers optimize product development and operations through innovations in sales, products, services, and data, thereby driving new growth for the health insurance industry.

Does China’s health insurance industry have a future? This is a question that many observers continue to debate.

It is important to note that, compared with mature healthcare markets abroad, China’s healthcare market has yet to develop major payers beyond basic medical insurance. The pharmacy sector is characterized by homogeneous competition, public hospitals hold an absolute advantage without having formed chain or group-based structures, and the pharmaceutical industry remains in a developmental stage.

Overall, the fragmentation on both the supply and payment sides of healthcare presents unique challenges to China’s medical market.

Therefore, China’s healthcare services market urgently needs an ecosystem platform capable of integrating resources from payers, providers, and other stakeholders, to help build a multi-tiered healthcare security system with basic medical insurance as the mainstay, supplemented by urban policy-based insurance as supplementary medical insurance, and further layered with commercial health insurance and out-of-pocket payments.

Thus, it can be seen that China’s pharmaceutical R&D reforms initiated in 2014, the comprehensive elimination of drug markups in public hospitals in 2017, and the establishment of the National Healthcare Security Administration in 2018 to consolidate multi-party medical security responsibilities have gradually advanced the new healthcare reform centered on the “tri-medical linkage” (coordination among medical care, health insurance, and pharmaceuticals) into deep-water zones. In February 2020, the State Council issued the Opinions on Deepening the Reform of the Medical Security System, further clarifying the need to accelerate the development of a multi-tiered medical security system and promote reforms in payment methods and the supply side of pharmaceutical and medical services.

Driven by strong policy support, China’s healthcare delivery, pharmaceutical utilization, and payment systems are accelerating their optimization, moving toward a multi-tiered medical security framework. Meanwhile, markets such as commercial health insurance and health management have entered a phase of rapid growth.

Certainly, in this process, industry participants must further drive the transformation of healthcare services toward value-based care, namely healthParticipants in the commercial health insurance sector should adopt value-based healthcare as their guiding principle. By diversifying funding sources, providing insurance coverage, integrating service delivery, and strengthening industrial consolidation, they can deeply engage in the “tripartite coordination” among medical care, health insurance, and pharmaceuticals. In doing so, they will serve as a catalyst for deepening healthcare reform and, while mitigating medical cost risks, help drive the transformation of the healthcare model from a disease-centered approach to a health-centered one.Only with a profound understanding of this point can innovative healthcare payment models truly hold practical value and significance.

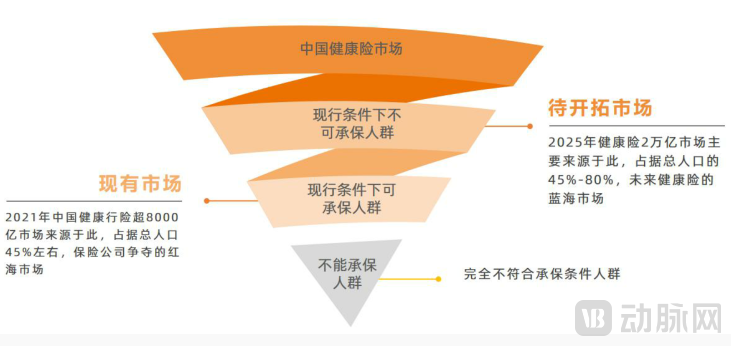

(Analysis of the Potential User Base for Future Health Insurance, by VCBeat)

(Analysis of the Potential User Base for Future Health Insurance, by VCBeat)

Moreover, from the perspective of social benefits, the professional exploration of health insurance over the next decade will continue to focus on medical and health management-driven insurance coverage, thereby providing the general public with tangible experiences in medical and health management. This not only aligns with the health service objectives required by “Healthy China 2030,” but also constitutes an indispensable component in achieving “common prosperity in health.”

In this process, some enterprises have already taken action. Although the challenges are formidable in the short term, they will inevitably drive China’s health insurance market toward maturity and foster its unique characteristics over the medium to long term.