Can Online Platforms Still Sell Medicines? The Truth Behind the New Draft Regulation

JD Health

Internet Medical and Health Service Platform Provider

AliHealth

Medical and Health Services Network Service Provider

“The State plans to prohibit third-party platforms from directly participating in online drug sales...”

On June 22, a breaking news item rapidly spread online, becoming an industry hotspot. The report indicated that the "Regulations for the Implementation of the Drug Administration Law of the People's Republic of China (Revised Draft for Comment)," recently released by the National Medical Products Administration, stipulate that third-party platform providers are prohibited from directly participating in online drug sales activities.

“Third-party platforms can no longer sell drugs?” “Online platforms are prohibited from selling pharmaceuticals?” In the wake of these regulations, a wave of speculation and discussion erupted online; the secondary market was also affected, with the stock prices of two pharmaceutical e-commerce platforms dropping by more than 10%.

The Development of Pharmaceutical E-commerce Has Secured a Significant Position in the Pharmaceutical Retail Market Landscape. From an industry perspective, amid the impact of the pandemic, online pharmaceutical sales surpassed the RMB 200 billion mark in 2021, establishing pharmaceutical e-commerce as the fourth-largest retail channel; among these, the self-operated business revenue of major pharmaceutical e-commerce enterprises has reached the tens of billions of yuan. From a demand perspective, pharmaceutical e-commerce has brought considerable convenience to residents’ medication purchases in recent years. Leveraging a hybrid model combining self-operated services and third-party platforms, consumers can select medications based on comprehensive factors such as drug prices and delivery timeliness.

If the external speculation that “online platforms cannot sell pharmaceuticals” proves true, the market will undergo significant changes from both the supply and demand sides.

However, is the policy orientation truly as such? VCBeat has conducted a more comprehensive observation by integrating the original documents, current industry status, and other factors.

A single sentence is insufficient to grasp the full picture.

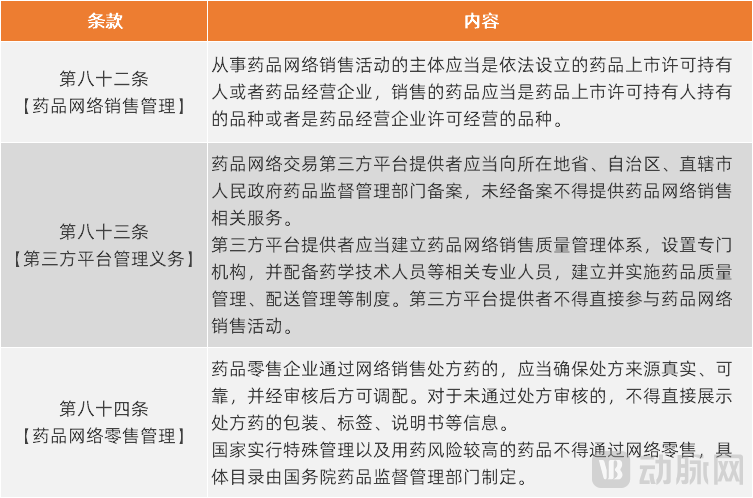

VCBeat found on the official website of the National Medical Products Administration that the "Regulations for the Implementation of the Drug Administration Law of the People's Republic of China (Revised Draft for Comment)" had already been released in May 2022. Among them, Articles 82 to 84 all stipulate matters related to online drug sales.

“Provisions on Online Drug Sales in the Implementing Regulations of the Drug Administration Law of the People’s Republic of China (Revised Draft for Public Comment),” Source: Official Website of the National Medical Products Administration

The viral headline captures only one sentence of Article 83; a more comprehensive understanding can be gained by carefully reading all three provisions:

First, third-party platform providers may offer services related to the online sale of pharmaceuticals, provided that they have completed the required filings in accordance with regulations.

Secondly, entities engaged in online drug sales activities shall be legally established drug marketing authorization holders or drug operation enterprises.

This involves the correspondence between two sets of relationships: first, online drug sales activities, where the entities are drug marketing authorization holders or drug distribution enterprises; second, services related to online drug sales, where the entity is the third-party platform provider. Meanwhile, the document further stipulates that third-party platform providers shall not directly participate in online drug sales activities, which essentially reiterates the aforementioned correspondence between these two sets of relationships.

In the above explanation, how should the key phrase “shall not directly participate” be interpreted?

Clearly, if a third-party platform provider does not possess the corresponding pharmaceutical operation qualifications, it is naturally prohibited from directly engaging in online pharmaceutical sales. However, if the third-party platform provider establishes a business entity and obtains the requisite operational qualifications, it falls under the scenario described in the first category of relationships; in accordance with the aforementioned regulations, it may then conduct online pharmaceutical sales.

It is evident that these regulations primarily address the two mainstream business models of pharmaceutical e-commerce: proprietary trading and platform-based operations. Proprietary trading involves selling pharmaceuticals, health supplements, and consumer health products through a self-operated supply chain system. Platform-based operations entail establishing an online sales marketplace, leveraging traffic entry advantages to attract merchants, and earning commissions by providing technology, operational, and other services.

Of the two business models, there is no dispute regarding the platform-based model under the new regulations: as long as merchants listed on pharmaceutical e-commerce platforms have obtained the requisite qualifications, they may engage in online drug sales. The controversy stems from the self-operated business model.

In fact, the current B2C self-operated business model of pharmaceutical e-commerce typically involves establishing proprietary pharmacies and selling products online. Taking JD Health as an example, its primary vehicle for self-operated operations is JD Pharmacy. According to JD Health’s 2021 annual report, among its major subsidiaries and consolidated affiliated entities, three companies are responsible for the online retail of pharmaceutical products: JD Pharmacy (Qingdao) Chain Co., Ltd., JD Pharmacy (Huizhou) Co., Ltd., and JD Pharmacy Taizhou Chain Co., Ltd. Meanwhile, data from Qichacha shows that these three companies have invested in and established pharmacies across China, covering 26 provincial-level administrative regions.

In other words, the self-operated business of pharmaceutical e-commerce is essentially a drug distribution enterprise engaging in online drug sales, which complies with the provisions of Article 82 of the policy. However, this type of self-operated business involves a “proprietary pharmacy” listing on its “own platform” to sell drugs. Does this constitute the platform’s “direct” participation in online drug sales? This will depend on the wording of subsequent official documents and the practical interpretation by regulatory authorities.

However, it is certain that, based on the full text of the policy, the document should not be simply interpreted as “third-party platforms cannot sell drugs” or “online platforms cannot sell pharmaceuticals.”

On the other hand, in light of the current state of the industry, the document also embodies the principle that pharmaceutical e-commerce platforms must distinguish between their two operational roles: as platform operators and as online drug sellers.

On this basis, some industry insiders have speculated that if the policy is implemented, e-commerce platforms will be forced to choose between two identities: either purely self-operated or purely a platform.

If interpreted in this way, how will pharmaceutical e-commerce platforms make their choices? How will the industry evolve?

Currently, on major pharmaceutical e-commerce platforms in the industry, proprietary and marketplace operations have become deeply integrated. For platforms, combining proprietary and marketplace businesses to expand drug categories offers users more choices. For listed merchants, the traffic entry points of large platforms can drive incremental sales. For users, the ability to choose between platform-owned drugs and those from listed merchants—each with distinct advantages in pricing, delivery speed, and other aspects—provides significant convenience by allowing selections tailored to individual needs.

Therefore, the integrated model of self-operated business plus platform provides a relatively healthy ecosystem for all participating parties.

According to JD Health’s annual report, the company’s total revenue in 2021 was RMB 30.7 billion, of which RMB 26.2 billion came from its direct-sales business. For the fiscal year ended March 2022, AliHealth’s total revenue amounted to RMB 20.6 billion, with its pharmaceutical direct-sales business reaching RMB 17.9 billion.

The revenue structures of the two leading platforms largely reflect the current state of the industry: self-operated revenue far exceeds platform revenue. In this context, will pharmaceutical e-commerce platforms prioritize major partners over smaller ones by transitioning to a pure marketplace model? It is evident that adopting a pure marketplace model would significantly impact revenue scale. Moreover, under such a model, pharmaceutical e-commerce platforms would have limited control over the operational performance of onboarded merchants, introducing uncertainties in drug category composition, quality, delivery, and other aspects.

It is reported that Meituan, which previously operated under an O2O platform model, also registered Tianjin Meituan Grand Pharmacy Co., Ltd. in May 2022, signaling a potential expansion into self-operated pharmaceutical sales. This further underscores the strategic importance of self-operated businesses to e-commerce enterprises.

What would be the outcome if pharmaceutical e-commerce companies, considering revenue scale, opted for a pure self-operated model and abandoned platform-based business?

First, traditional pharmaceutical retail enterprises risk losing access to online traffic channels. Currently, whether for the four major listed pharmacy chains or localized small and medium-sized pharmacies, joining pharmaceutical e-commerce platforms and driving customer acquisition through online channels has become an irreversible trend.

In the absence of third-party platforms, traditional pharmaceutical retail enterprises must build their own online platforms to expand into e-commerce. While large pharmacy chains possess the capability to develop and operate such platforms, a vast number of small and medium-sized pharmacies lack this capacity, thereby hindering their online business expansion.

Secondly, the convenience of purchasing medications will be significantly compromised for users. Assuming that all offline pharmacies have the capability to build their own online platforms, users would need to search and select from a multitude of different e-commerce platforms when buying drugs, thereby reducing efficiency.

If interpreted as an “either-or” choice, adopting any single model by pharmaceutical e-commerce platforms would be detrimental to maintaining the currently healthy industry ecosystem. Admittedly, pharmaceutical e-commerce and offline pharmacies are, to some extent, in a competitive relationship. However, digital transformation across all sectors, including pharmaceutical retail, remains an overarching trend. Under this trend, the optimal path for mutual development lies in leveraging each party’s respective strengths and achieving complementary advantages.

Overall, this document is merely a draft for public comment and has not yet been finalized into an implementable regulation. In the 2019 revision of the Drug Administration Law of the People's Republic of China, provisions regarding the online sale of prescription drugs differed between the draft for public comment and the final implemented version. Therefore, it is possible that changes may occur during the current public consultation period.

How will the final document be worded? Will it have a direct impact on the industry? We still need to wait for the release of the implementation version.

In any case, pharmaceutical e-commerce has already demonstrated significant value to various stakeholders across the industry chain: it has driven the transformation and upgrading of the pharmaceutical retail sector, promoted the integrated development of online and offline channels, optimized resource allocation, innovated service models, improved service efficiency, and reduced service costs. In light of these benefits, the fundamental basis for regulatory authorities’ legislation and supervision of online drug sales is not to “block” but to “guide.” Regarding the new policies that have not yet been fully finalized, we should engage in more rational reflection and less one-sided speculation.