Sequoia, Hillhouse, and Matrix Partners Bet Big as China's Trillion-Yuan Sleep Health Industry Surges

The sleep health industry is experiencing a major boom.

On June 23, De Rucci Bedding Co., Ltd. (hereinafter referred to as “De Rucci”) was listed on the Shenzhen Stock Exchange, with its stock price surging 44% within one hour to hit the daily upper limit, bringing its market capitalization to RMB 22.425 billion. This marks another sleep-health-related company to enter the secondary market, following Luolai Lifestyle and Yitong Technology.

Interestingly, De Rucci, founded in 2004, was originally a typical bedding brand. In order to find a way out of fierce market competition, it began to venture into the field of healthy sleep in 2008 and eventually succeeded in its IPO. The prospectus shows that De Rucci's shareholder list includes well-known enterprises and institutions such as Red Star Macalline and Sequoia.

The primary market remains equally hot. Multiple sleep-tech companies, including Qushui Technology, Boluobanma, TipsYou, sijo, Vesta, Mianbai Technology, 8H, and Mooring, have completed financing rounds, attracting top-tier investment firms such as Sequoia Capital, Matrix Partners, SoftBank, Redpoint Ventures, and SIG.

What has generated even more buzz within the industry is Hillhouse’s entry into the sleep health sector in 2021 with its acquisition of Ai Meng Group. The group owns several core sleep brands, including Serta, King Koil, and RUF Betten. Reportedly, the transaction amounted to a staggering $2 billion.

Behind the influx of capital and enterprises lies the rapidly growing market demand. According to the China Sleep Report 2022, over the past decade, Chinese people have been going to bed two hours later, with their sleep duration reduced by approximately 1.5 hours. Currently, only 35% of people get eight hours of sleep per day, and about 15% suffer from sleep disorders requiring treatment.

Faced with the challenges troubling contemporary young people, the “great battle” against sleep disorders has undoubtedly begun.

#01

300 Million People with Insomnia and the Trillion-Yuan Sleep Health Industry

Sleep disorders have become an increasingly serious social and medical issue.

According to the “Latest Survey Data on Global Sleep Status and Sleep Awareness, and Recent Advances in Sleep Medicine” released by the Sleep Medicine Professional Committee of the Chinese Medical Doctor Association, 30.9% of individuals require more than 30 minutes to fall asleep, and 0.9% need medication to aid sleep, with sleep disorders affecting a large portion of the population.

“Long-term sleep disorders can lead to serious physical and mental illnesses, such as chronic somatic conditions including diabetes, impaired glucose tolerance, hypertension, reduced anti-infective capacity, and tumors, while also increasing the risk of developing mental disorders such as anxiety and depression,” said Huang Zhili, Chairman of the Chinese Sleep Research Society, Distinguished Professor at Fudan University, and Doctoral Supervisor, in an interview with VCBeat.

Therefore, alleviating insomnia among 300 million Chinese citizens has become an urgent challenge for the medical and healthcare industry.

From the current perspective, sleep disorders are difficult to treat. This is because sleep disorders are a composite symptomatic manifestation of numerous conditions, including depression, anxiety disorders, phobias, schizophrenia, potential metabolic disturbances and immune dysfunction, various somatic diseases, and even unhealthy lifestyle factors. These underlying etiologies span different medical specialties and classifications, thereby demanding an exceptionally high level of professional expertise from physicians.

Moreover, given the scarcity of specialized and reliable diagnostic and treatment institutions for sleep disorders in China, which are predominantly concentrated in major cities, broader population access remains limited.

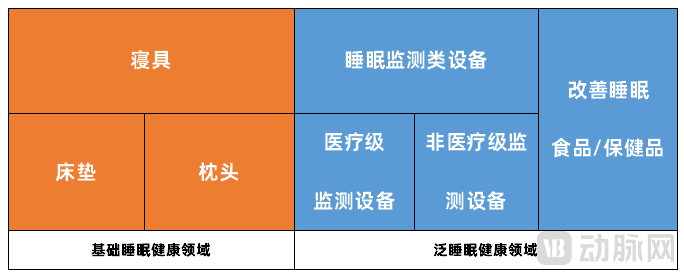

In response to these challenges, a multitude of solutions have emerged in China’s sleep health industry, which remains in a fragmented and complex state.: In addition to basic sleep products such as mattresses and pillows, many companies are also developing medical products for sleep monitoring and the treatment of sleep disorders.

“The development of the sleep industry is driven first by cognition, and second by technology.”The growing popularity of sleep medicine in recent years, coupled with advances in Internet of Things (IoT) technology, has spurred the development of more sleep-related products and services, triggering a wave of entrepreneurial activity.“Senior investor Wu Qian told VCBeat.”

According to data from Qichacha Professional Edition, there are over 2,000 companies in China focused on sleep health, with approximately 50% of them established within the past four years. On the public hospital front, top-tier Grade A tertiary hospitals, including Peking Union Medical College Hospital and West China Hospital of Sichuan University, are also actively establishing sleep centers.

With sustained growth on the demand side and rapid development on the supply side, the market ceiling of the sleep industry continues to rise.According to a research report by China Galaxy Securities, the market size of China's sleep industry had already exceeded RMB 400 billion in 2020 and is projected to surpass RMB 1 trillion by 2030, indicating rapid growth.

In this process, participating companies are continuously driving the industry’s explosive growth by offering increasingly diverse and differentiated products and solutions.

#02

Two Core Sub-Sectors: Opportunities and Challenges Coexist

The Sleep Health Market Is Booming.

In the market, a wide variety of sleep products have sprung up everywhere, spanning from hardware to software and from offline to online channels. HoweverOverall, the sleep health sector has primarily developed into two core sub-segments: home products centered on bedding, and sleep monitoring devices.Both sectors have garnered significant investor enthusiasm.

In the sleep health sector, which is primarily centered on bedding, companies such as De Rucci, Xilinmen, XiYue Technology, Eight, and Keeson Technology have gathered.This sector was initially dominated by traditional home furnishing brands, which have continuously expanded into the sleep health arena amid intense market competition, thereby developing functional bedding and tapping into the mid-to-high-end market.

Taking De Rucci as an example, the company began its transformation in 2008 by partnering with three major European firms, thereby introducing comprehensive sleep systems that encompassed manufacturing materials and technologies for mattresses and slatted bed bases. In addition, De Rucci has been engaged in independent research and development, leveraging AI to analyze human biometric data and utilizing its proprietary sleep big data to match sleep parameters, intelligently adjusting mattress firmness to align with individual physiological characteristics.

For another example, XiYue Tech, founded in 2018, has created the smart mattress brand Qrem and designed a matching three-piece suite—comprising a smart noise-canceling bed frame, a smart texture pillow, and a mobile app—to provide users with an enhanced sleep experience. Additionally, Qrem can adjust its firmness by leveraging three core materials: springs, latex, and foam.

“In recent years, home products such as smart mattresses have become increasingly technology-intensive, but the business remains fundamentally sales-driven,” says veteran investor Wu Qian.The core competitiveness of smart mattress companies still lies in their channel, marketing, and resource integration capabilities.

For instance, De Rucci Bedding Co., Ltd. has consistently maintained high sales expenses. Its prospectus reveals that in the first half of 2021, the company incurred sales expenses of RMB 6.8 billion, accounting for 24.22% of its operating revenue.

“Such enterprises have a large number of distributors with a relatively dispersed geographic distribution, and their business models are quite traditional. However, their cash flows tend to be stable. As a result, mainstream venture capital (VC) firms rarely invest in these companies; instead, investment primarily comes from strategic partners within the upstream and downstream segments of the home furnishings industry chain.“Senior investor Wu Qian stated.”

Next, let us examine the sleep health sector, which is dominated by sleep monitoring devices., which gathers software companies represented by Tidal, Snail Sleep, Firefly Sleep, Little Sleep, and White Noise, as well as hardware companies such as Sumian, Sleepace (Mediga Technology), Dongjing Technology, CentrePoint Insight, and Jiuan Technology.

Moreover, leading smart wearable device manufacturers such as Apple, Huawei, Xiaomi, and Huami have also introduced sleep health monitoring features in their products, becoming key players in this field.

Based on the search and download experience from VCBeat, software-based sleep health apps primarily offer two major functions: first, helping users fall asleep faster through content platforms and hypnotic sound effects, such as playing sounds of ocean waves, mountain streams, forests, and rain; second, automatically tracking users' sleep patterns to monitor sleep depth and quality. Additionally, some products incorporate social features, connecting more users by sharing recordings of sleep talking, among other interactions.

“The online app is designed to be lightweight, but it lacks genuine therapeutic functions; instead, it primarily helps users alleviate feelings of tension and anxiety.“Senior investor Wu Qian stated, ‘The business model of such apps remains questionable unless they are subsequently expanded into social products or deeply integrated with other hardware.’”

Sleep monitoring devices are currently the most closely watched sector in the capital market, primarily categorized into three types: medical polysomnography monitors, wearable detection devices, and non-wearable monitoring devices.

Specifically, polysomnography (PSG) monitors are currently the most professional devices in the field of sleep monitoring, capable of detecting various sleep disorders such as snoring, narcolepsy, pediatric obstructive sleep apnea, Kleine-Levin syndrome, hypersomnia, and insomnia.

Wearable detection devices and non-wearable monitoring devices are primarily home-use devices, including smart bracelets, sleep belts, and monitoring buttons.

(Similarities and Differences Between Sleep Health Software and Hardware Devices; Chart by VCBeat)

(Similarities and Differences Between Sleep Health Software and Hardware Devices; Chart by VCBeat)

“In the past few years, financing for testing equipment was quite frequent, but the market soon discovered that,”Smart wristbands and other monitoring devices can track sleep patterns in individuals with sleep disorders, but effectively helping patients achieve good sleep quality remains an unresolved challenge."This has also led to a cooling of financing in this niche sector," said Wu Qian, a senior investor.

In summary, it is evident that both home products centered on bedding and sleep-monitoring devices are facing new challenges after their rapid rise. In response, the industry urgently needs new approaches and solutions.

#03

Three New Opportunities in the Sleep Health Sector

In the quest to find a breakthrough path in the sleep health industry, three major trends have begun to emerge.

First, the gradual integration of home furnishing enterprises with technology companies.Tech companies integrate monitoring sensors into home furnishing products to achieve sleep monitoring and data collection. This strategy not only enhances product added value but also enables entry into the sleep services industry. By collaborating with backend big data firms and medical institutions, these companies integrate industry resources to establish a sleep health service platform centered on sleep-related products.

For instance, Maidijia has partnered with Huawei Zhixuan to jointly launch the smart sleep health brand MOK PLANET. Its developed smart latex pillow supports the HUAWEI HiLink protocol and features embedded high-precision sensors that monitor sleep data such as heart rate, respiratory rate, sleep cycles, number of turns, and instances of leaving the pillow. Users can view professional sleep reports via the Huawei AI Life app to intuitively assess sleep quality, identify sleep abnormalities, and receive recommendations for sleep improvement.

For another example, Keeson Technology and Jiuai Technology have launched the “Ai Fangxin” series of smart health beds. Based on multiphase sensing intelligent monitoring technology, these smart beds enable precise monitoring of vital signs during sleep and provide specialized features such as sleep onset assistance, snoring relief, apnea warnings, and emergency rescue triggering, thereby minimizing the risk of accidents caused by sudden issues during sleep.

“Integration is a trend we view very favorably, as products and services will be difficult to distinguish,”Home furnishing companies can shift their focus from selling products to providing services, while technology-driven hardware companies no longer need to build their own distribution channels, adopting a B2B business model and unlocking new profit opportunities.“said Wu Qian, a senior investor.

Second, the increasing maturity of digital therapeutics and the emergence of related products.Digital therapeutics are software-driven, evidence-based intervention programs used to treat, manage, or prevent diseases. Digital therapeutics can be used independently or in combination with medications, medical devices, or other therapies. Representative companies in this field include Zeen HEALTH and Udreams.

“Since the outbreak of the pandemic, digital therapeutics, represented by cognitive behavioral therapy, have become extremely popular in the industry. Many companies and products have flooded the market, making the sector highly crowded, with particularly obvious homogenization,” Professor Zhang Jihui, a researcher at Guangdong Provincial People’s Hospital, told VCBeat, emphasizing that companies must strive for differentiation.

How is it done? From the perspective of industry evolution, cognitive behavioral therapy (CBT) was initially delivered primarily online, relying mostly on text or audio. Currently, animations are being incorporated, or different modules such as text and audio are being combined. Additionally, some companies are experimenting with chatbots to improve patients’ conditions and enhance interactivity.

“More importantly, for digital behavioral therapies to gain physicians’ confidence in their use, clinical trials must be conducted to demonstrate the product’s safety and efficacy, as well as to identify which patient populations derive greater benefit, thereby providing such data,” Professor Zhang Jihui emphasized.

Third, the emergence of the lifestyle medicine sector.Lifestyle medicine is an emerging medical model that treats and manages diseases through lifestyle interventions, referring to the control of diseases through diet, exercise, stress management, smoking cessation, and other various non-pharmacological therapeutic approaches.

Prominent companies in this field include Sumian Technology. Its founder, Han Zhenya, believes that the first step in addressing sleep issues is learning how to achieve quality sleep. Lifestyle primarily encompasses diet, physical activity, and sleep. Improving these three aspects can effectively manage chronic diseases. By intervening in patients’ dietary habits, exercise levels, and sleep rhythms, and providing scientific education and training, patients can develop knowledge, belief, and action (KBA) regarding their health. This approach enables them to gradually master the skills and methods for adopting a healthy lifestyle, thereby restoring their well-being.

Taking the prevention and treatment of sleep disorders, a chronic condition, as an example, Sumian Technology, in collaboration with the Chinese Sleep Research Society and JD Health, jointly established the JD Health Youmian Center. This center promotes healthy sleep lifestyles to the general public and provides online free clinic services, enabling users to access sleep health solutions from home. Furthermore, leveraging the online JD Health Youmian Center, offline sleep centers at tertiary hospitals, and the Youmian outpatient clinic network, Sumian has established bases for sleep medicine experts across China. This initiative aims to promote tiered diagnosis and treatment for sleep disorders, thereby alleviating the supply-demand imbalance between patients and healthcare providers in the field of sleep medicine.

It is not difficult to find that,The adjustment and transformation of the sleep health industry have set sail.As batches of companies secure financing and go public, those armed with ample “ammunition” will bring more incremental growth to the entire industry.

Certainly, in the journey ahead, the key to whether such enterprises can continue to ride the wind and waves lies in how they continuously enhance their innovation and technological application capabilities.