Yeasen Biotechnology, a High-Growth Life Science Reagents Unicorn, Files for STAR Market IPO

Yeasen

Tool Enzyme Raw Materials and Diagnostic Product R&D, Manufacturer

Another unicorn from the VCBeat VB100 list has entered the secondary market.

Two days ago, the listing application submitted by Yeasen, a leading domestic manufacturer of biological reagents, was accepted by the STAR Market of the Shanghai Stock Exchange, making it the sixth life science tools company to enter the capital market, following Vazyme, Fapon Biotech, Sino Biological, ACROBiosystems, and Nearshore Protein.

It is reported that Yeasen plans to issue no more than 21.0335 million shares, raising approximately RMB 1.1 billion. Of this amount, RMB 832 million will be allocated to the Yeasen headquarters and industrialization base project, while RMB 276 million will be used for the construction of its Shanghai R&D center.

Founded in 2014, Yeasen Biotechnology became a highly sought-after star project in the capital market in its seventh year of operation. In July, September, and December 2021, Yeasen completed three rounds of financing in rapid succession. According to data disclosed in its prospectus, these financing rounds, spaced only months apart, significantly boosted Yeasen’s valuation, which surged several-fold from RMB 300 million at the end of the previous year to nearly RMB 2.3 billion. By the final pre-IPO financing round, Yeasen’s valuation had reached approximately RMB 7.3 billion. During this period, prominent investors such as Legend Capital, Huimei Capital, CPE Yuanfeng, and Hantai Venture Capital injected substantial capital into the company.

Behind the surge in financing lies the rapid expansion of Yeasen’s business scale. According to its prospectus, Yeasen’s revenue grew from less than RMB 98 million in 2019 to over RMB 320 million in 2021, representing a compound annual growth rate (CAGR) of 48.67%. During the same period, its net profit soared from approximately RMB 1.8 million to RMB 101 million, with a CAGR of 282.44%.

At present, Yeasen has become the second-largest domestic manufacturer of scientific research biological reagents and the leading domestic brand of high-throughput sequencing library preparation reagents in terms of market share. It also ranks among the top three in the domestic markets for molecular diagnostic raw material enzymes and core enzymes for mRNA vaccines, bringing it one step closer to its goal of becoming a leader in the life sciences tools industry.

Strictly speaking, Huang Weihua, the founder of Yeasen, is not a typical entrepreneur with a formal background in biological scientific research, yet he remains deeply committed to technological advancement.

Born in 1979, Huang Weihua graduated with a degree in Computer Applications and Science. He has worked as both a programmer and a sales manager. While representing foreign brands, he was drawn to the promising applications of biological reagents. Biological reagents refer to biological materials or organic compounds used in fields such as life sciences research, clinical diagnosis and testing, and biopharmaceuticals, serving as one of the core tools in the life sciences sector.

Specifically, biological reagents can be categorized into three major groups: molecular, protein, and cellular. When Huang Weihua entered this field, next-generation sequencing (NGS) technology was maturing and on the verge of widespread application across research, clinical, and industrial sectors. He identified molecular enzymes as a promising direction. As core raw materials in the life sciences industry, enzymes typically exhibit catalytic efficiencies that are 10⁷ to 10¹³ times higher than those of inorganic catalysts in various experimental settings. The molecular enzyme landscape is highly complex; each type of enzyme comprises multiple distinct gene mutants, with each mutant possessing unique properties and functions tailored to different application scenarios.

In Huang Weihua’s view, molecular enzymes, as key raw materials for IVD and NGS testing, represent “blockbuster products” within the category of biological reagents. They boast broad applications, significant room for expansion, and are amenable to scalable, industrialized production. More importantly, this sector has long been monopolized by imported brands. If sufficient effort is devoted to product research and development, the domestic substitution of biological reagents in China will unlock enormous market potential.

Thus, in 2014, Huang Weihua established Yeasen in the Shanghai International Medical Zone. At the outset of his entrepreneurial venture, Huang continued to pursue the familiar path of brand distribution. However, unlike previous efforts that focused solely on facilitating product sales, Huang and his team leveraged their experience distributing imported brands to deepen their understanding of market demand for biological reagents—a specialized product category. By thoroughly analyzing customer needs and assessing the strengths and weaknesses of competitors, they identified instability in delivery lead times for foreign products and their insufficient agility in responding to the Chinese market’s demands. These insights became the entry point for Yeasen to gradually shift its business focus toward independently developed products.

Since 2017, Yeasen has strengthened its professional product team, closely tracked the latest technologies and future development trends, anticipated customer needs ahead of time, and made proactive technical reserves. As a result, sales revenue from self-developed products quickly surpassed that of distributed products.

Today, Yeasen has evolved through continuous innovation into a high-tech enterprise dedicated to the research, development, and manufacturing of enzyme raw materials and antigens/antibodies. The company boasts comprehensive technological platforms, including a bidirectional enzyme engineering platform, a protein fermentation and purification platform, and a high-efficiency antibody screening platform. Coupled with a 3,000-square-meter ultra-clean molecular enzyme production facility, Yeasen has established six major product portfolios: qPCR series, NGS series, protein purification and analysis series, cell culture and analysis series, and antibody and reverse transcription series.

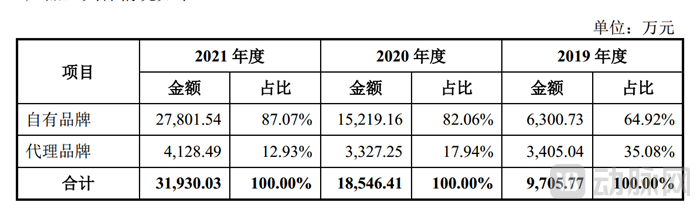

According to the prospectus, between 2019 and 2021, Yeasen’s revenue derived from sales of its proprietary-brand biological reagents increased from 64.92% to 87.07%.

Revenue from Proprietary and Distributed Brands, 2019–2021 Data Source: Yeasen’s Prospectus

Underpinning this transformation is Yeasen’s sustained and substantial investment in independent research and development. It is reported that Yeasen’s self-developed platform for bidirectional rational design and directed evolution of molecular enzymes has successfully engineered and evolved more than 130 types of high-end molecular enzymes, enabling the large-scale, stable manufacturing and industrial application of over 300 such enzymes.

Data shows that in 2021, Yeasen’s R&D expenditure accounted for 17.56% of its revenue, significantly higher than that of other companies in the same industry. After all, in the highly diversified field of biological reagents, only by continuously innovating and expanding the product portfolio to meet new demands driven by technological and product iterations can a brand achieve sufficient competitiveness.

As mentioned at the beginning of this article, Yeasen has experienced leapfrog growth in performance over the past three years, becoming a star project in the primary market. However, even before this period, the biological reagents provided by Yeasen had already gained considerable influence in the scientific research community.

According to statistics from the Zhiliao Wo big data platform, SCI papers produced using Yeasen products have accumulated a total of 8,031 citations, with a cumulative impact factor of 47,706.253. Among these, 29 papers were published in journals with an impact factor above 30, including 12 in Cell, 4 in Nature, 2 in Nature Biotechnology, and 1 in Nature Medicine. More importantly, the research teams behind these studies are distributed across China, the United States, Singapore, Egypt, Australia, Germany, South Korea, Nigeria, and other countries. This indicates that Yeasen’s biological reagents have gained certain competitiveness even within the global scientific research community.

Furthermore, according to Frost & Sullivan statistics, the current competitive landscape of China’s biological reagent research market is relatively fragmented. Foreign brands hold a dominant position by leveraging advantages accumulated over many years, while domestic brands mainly include Vazyme, Yeasen, Sino Biological, Kangwei Century, and ACROBiosystems. Among these, in 2021, Yeasen ranked second among domestic manufacturers in terms of market share among research institution users in China’s biological reagent sector.

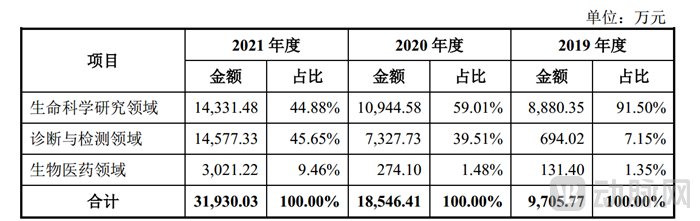

Revenue Distribution from 2019 to 2021 Data Source: Yeasen's Prospectus

According to the prospectus, between 2019 and 2021, Yeasen’s revenue from sales of biological reagents to users at academic institutions—such as universities, research institutes, and hospitals—continued to grow steadily in absolute terms, but its proportion of total revenue declined gradually from 91.5% to 44.88%, less than half. During this period, Yeasen experienced substantial growth in revenue from the clinical and pharmaceutical sectors. For instance, revenues from the diagnostics and testing sector and the biopharmaceutical sector each increased more than 20-fold.

Of course, the COVID-19 pandemic is an unavoidable factor in explaining this change. Yeasen stated that its sales revenue from COVID-19-related products amounted to RMB 46.1476 million and RMB 81.7413 million in 2020 and 2021, respectively. Beyond this, perhaps more significant is the iterative advancement of technology itself, which continuously generates new demand for biological reagents.

In recent years, the rapid advancement of global life science technologies has driven the scientific and industrial communities to continuously explore artificial methods—such as genetic engineering, enzyme engineering, and cell engineering—to modify and screen natural enzymes, aiming to obtain enzymes with higher catalytic efficiency and greater stability. Building on years of R&D investment and accumulated expertise, Yeasen has developed robust technical capabilities in enhancing the purity, activity, sensitivity, stability, amplification efficiency, amplicon length, and inhibitor tolerance of molecular enzymes. For instance, while the amplification sensitivity of natural Taq DNA polymerase is approximately 500 copies/mL, the Taq DNA polymerase developed by Yeasen through rational design and directed evolution technologies achieves a sensitivity of 200 copies/mL, simultaneously reducing the PCR amplification detection time from the original 2 hours to around 30 minutes.

Meanwhile, Yeasen’s molecular enzyme manufacturing facility, built and operated in accordance with quasi-GMP standards, features ton-scale fermentation lines, industrial-grade AKTA purification systems, and fully automated packaging lines. This infrastructure enables the production of molecular enzymes with ultra-high specific activity while progressively and precisely removing various persistent contaminants, thereby achieving ultra-clean control throughout the entire process from R&D to manufacturing. Reportedly, this ultra-clean molecular enzyme production process maintains high intra-batch and inter-batch consistency during large-scale industrial preparation, serving as a critical foundation for Yeasen’s expanding business scope from scientific research to industrial applications and its success in securing substantial orders.

For instance, according to the prospectus, from 2019 to 2020, the downstream customers of Yeasen’s protein purification and analysis product series were primarily research-oriented clients. However, in 2021, the sales revenue of Yeasen’s protein purification and analysis product series increased rapidly, mainly due to the successful sale of large quantities of Universal Nuclease to industrial clients LT Biotech and UAB. The latter is an endonuclease capable of degrading various forms of DNA and RNA; it is widely used for removing nucleic acids from biological products and is frequently applied in fields such as vaccine production, gene therapy, and cell therapy.

In fact, as indispensable core raw materials for the life sciences industry—from basic research to technology commercialization—biological reagents are being widely applied in fields such as life science research, diagnostics and testing, and biopharmaceuticals. Against the backdrop of the increasing maturity and large-scale commercial application of frontier biotechnologies like gene therapy, cell therapy, and mRNA vaccines, industrial users are poised to become a new driver of Yeasen’s sustained future growth.

For the most part, B2B biological reagent manufacturers do not take center stage.

However, the demand for viral testing and vaccines stemming from the COVID-19 pandemic has thrust these “hidden champions” into the industry spotlight. Over the past two years, hundreds of millions in capital have been drawn to the sector, with nearly every investment firm involved in healthcare seeking opportunities in biological reagent projects. In the primary market, in addition to Yeasen, whose valuation surged three times within the year, companies such as Hanhai New Enzyme and Abclonal have successively set new records for financing amounts.

Prior to Yeasen’s submission of its listing application to the STAR Market, Biopss, Nanomicro Technology, Sino Biological, and Vazyme had successively completed their initial public offerings (IPOs), systematically filling the void of listed companies in the IVD reagent raw materials sector and creating the only market segment in 2021 with no new listings breaking their issue price. Outside the capital markets, Fapon Biotech, Kangwei Century, and Nearshore Protein had long been queued for listing. In investment strategy reports released in early 2022, 25 out of 32 securities firms highlighted this upstream segment of the life sciences and pharmaceutical industry chain, with nearly ten sell-side analysts designating it as a key recommended sector.

In fact, when assessing the growth potential of the biological reagents industry, beyond the impact of the COVID-19 pandemic, two other drivers may be more critical: the continuous expansion of downstream application areas and import substitution with domestically produced alternatives.

On the one hand, driven by technological iteration and regulatory innovation, industries such as in vitro diagnostics and testing, innovative biological drugs, and novel vaccines are flourishing, leading to a corresponding increase in demand for biological reagents, which serve as one of their core raw materials. According to statistics from Frost & Sullivan, the market size of scientific research biological reagents in China grew from RMB 8.2 billion in 2016 to RMB 15.1 billion in 2020, with a compound annual growth rate (CAGR) of 16.51%, outpacing the global biological reagent market during the same period. The market is projected to reach RMB 34.6 billion by 2025, with an expected CAGR of 18.10% from 2020 to 2025.

For instance, with the intensifying aging population, rising per capita medical expenditures, and growing health awareness among residents, the market size of China’s in vitro diagnostics (IVD) industry is expected to grow steadily, reaching RMB 219.8 billion by 2025. In this process, the upstream raw materials market will grow in tandem. According to Frost & Sullivan, the market size of IVD reagent raw materials in China is projected to reach RMB 22.8 billion by 2025, with an estimated compound annual growth rate (CAGR) of 17.01% from 2020 to 2025.

On the other hand, supply disruptions or restrictions imposed by certain international biological reagent manufacturers during the COVID-19 pandemic created opportunities for domestically produced brands with strong market competitiveness to achieve rapid growth and accelerate import substitution. As an upstream sector in the life sciences research industry chain, the biological reagents industry is knowledge- and technology-intensive, characterized by high barriers to entry and high value-added. Due to the late start of China’s biological reagents industry, domestic products have lagged behind imported ones in terms of product stability, quality control capabilities, product portfolio richness, and brand influence, resulting in long-term dominance of the domestic market by imported brands. In the post-pandemic era, policy support for building a self-reliant and controllable biological reagents supply chain has created critical opportunities for domestic brands.

Historically, imported brands have rarely engaged in direct sales within China, predominantly adopting an agency distribution model. This approach has resulted in longer inventory lead times and higher selling prices. In contrast, domestic biological reagent manufacturers can flexibly choose between direct sales and distribution channels based on customer characteristics and market conditions. This flexibility provides a cost advantage in delivering products and after-sales services, enabling timely and rapid responses to diverse customer needs. Furthermore, the gaps between domestically produced and imported biological reagents are primarily reflected in product portfolio breadth, quality stability, and brand influence. As domestic manufacturers continue to increase R&D investment, enhance technical capabilities, expand product categories, and strengthen their brand advantages, the disparity between domestic and imported products is gradually narrowing.

For Yeasen, going public represents a phased success in its operations, but more importantly, it marks the beginning of participating in a larger market and engaging in more intense competition.