Decoding the Profitability Blueprint of Private Rehabilitation Hospitals: Six Key Insights

SANXING MEDICAL ELECTRIC

Provider of Integrated Smart Power Distribution and Consumption Solutions

"In the past, medical treatment was about survival; today, it is about living better."

This single sentence encapsulates the public’s advancing understanding of health and serves as a footnote to the year-on-year rise in rehabilitation demand in recent years. As one of the “four pillars of medicine,” rehabilitation medicine can reduce clinical disability rates, improve patients’ self-care abilities and quality of life, yet it has not received the attention it deserves in the past.

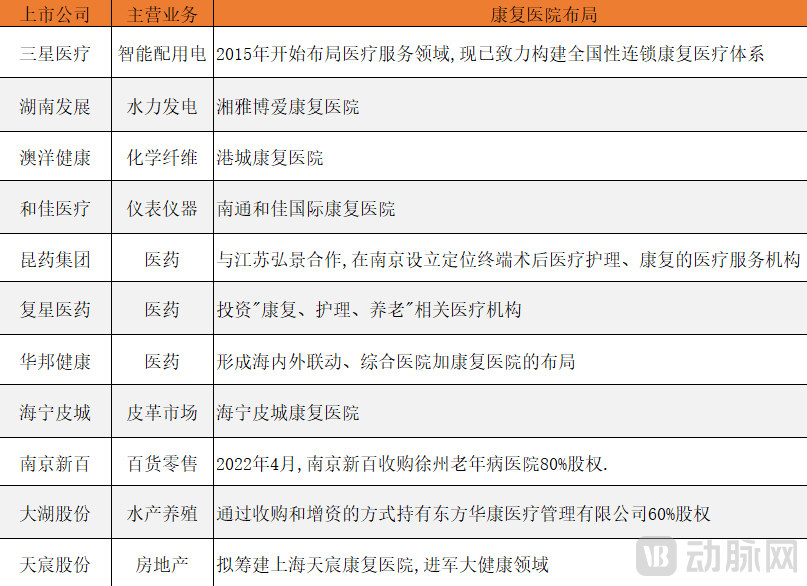

Listed Companies Entering the Rehabilitation Hospital Sector | Compiled by VCBeat

In recent years, an increasing number of listed companies have begun investing in rehabilitation hospitals. For instance, Sanxing Medical has acquired nearly 20 rehabilitation hospitals after several years of development. However, rehabilitation hospitals under Xinhua Medical and Hejia Medical continue to operate at a loss.

It is widely acknowledged that the rehabilitation medicine sector is in a golden period of development, and it is also regarded as an area where private healthcare providers can achieve significant success. So, what are the internal factors behind these losses?

When rehabilitation is mentioned, many people immediately think of physical therapy and massage. Previously, traditional rehabilitation services in China, such as those for age-related degenerative conditions and orthopedic rehabilitation, indeed had limited profit margins. From the perspective of medical insurance reimbursement, the per-diem cost ranged approximately from RMB 250 to RMB 450. Later, with the expansion of medical insurance coverage, many cases requiring intensive rehabilitation became covered. For example, the cost of a complete rehabilitation cycle in neurosurgery can reach RMB 40,000–60,000 in Wuhan, significantly increasing the profit margin.

According to statistics from the National Report on Professional Medical Services, Quality, and Safety in Rehabilitation Medicine, rehabilitation needs for conditions including stroke, degenerative changes of the spine and joints, postoperative care for fractures and sports injuries, traumatic brain injury, and spinal cord injury account for nearly 70% of the overall rehabilitation demand in China.

Furthermore, on August 3, 2021, the National Healthcare Security Administration, in conjunction with the Ministry of Civil Affairs, issued the "Assessment Standards for Disability Levels in Long-Term Care (Trial)," which serves as an evaluation criterion for long-term care targeting elderly individuals with disabilities and dementia.

An elderly individual identified as having disabilities and dementia incurs approximately RMB 80,000 to 150,000 in medical insurance costs every decade. Following the onset of neurological disorders, investing RMB 40,000 to 60,000 in rehabilitation can significantly improve the patient’s subsequent quality of life. Without such intervention, there is an estimated 30%–35% probability that these individuals will progress to a state of disability and dementia. From a socioeconomic perspective, medical insurance programs are willing to invest in critical care rehabilitation.

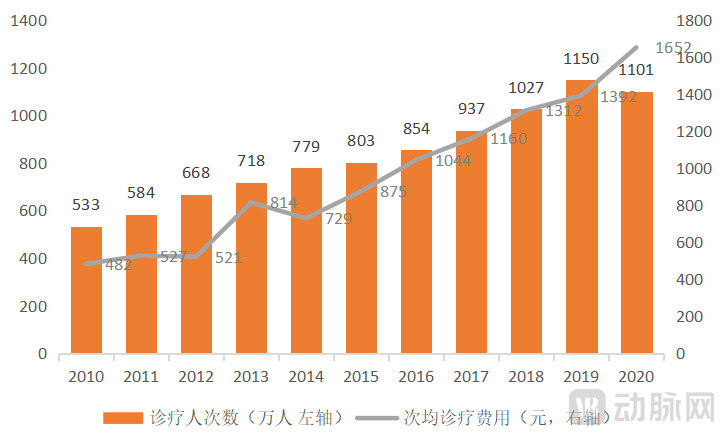

Annual Number of Patient Visits and Average Cost per Visit at Rehabilitation HospitalsData Source: China Health Statistics Yearbook

In the past, only regions with medical insurance surpluses exceeding nine months, such as Beijing and Shanghai, supported this approach. In recent years, cities including Hangzhou, Nanjing, Nanchang, Wuhan, Changsha, and Chongqing have also begun to invest in critical care rehabilitation. Meanwhile, private rehabilitation hospitals have entered the market by offering relatively lower prices, gaining policy support, and becoming eligible to apply for designation as designated medical institutions under the basic medical insurance scheme.

Taking the Shanghai region as an example, in 2020, the cost of one rehabilitation cycle after neurosurgery was RMB 120,000 at Grade A tertiary hospitals and RMB 60,000–80,000 at private hospitals, representing a 40% reduction; rehabilitation costs for neurology were RMB 40,000 at Grade A tertiary hospitals and RMB 20,000 at private hospitals, a 50% decrease; and orthopedic rehabilitation costs were RMB 20,000 at Grade A tertiary hospitals versus approximately RMB 7,000 at private hospitals, a 65% reduction.

ICU costs are RMB 5,000 per day at tertiary Grade A hospitals and approximately RMB 3,000 per day at private hospitals. For HDUs (High Dependency Units) specializing in neurosurgery, which are highly dependent on inpatient wards, the daily cost is RMB 3,000 at tertiary Grade A hospitals and RMB 2,000 at private hospitals, making private hospitals 30% cheaper. It can be seen that rehabilitation costs at private rehabilitation hospitals are indeed around 40% lower overall than those at tertiary Grade A hospitals.

In other words, critical care rehabilitation represents a new market segment carved out by medical insurance, and private rehabilitation hospitals must compete for it by leveraging their high-quality services and relatively lower prices.

The coverage of rehabilitation medical services includes the elderly, patients with chronic diseases, individuals with disabilities, women requiring postpartum rehabilitation, and postoperative inpatients. In 2020, the number of people aged 60 and above in China reached 264 million; the number of individuals with disabilities registered by the China Disabled Persons' Federation amounted to 37.8069 million. Meanwhile, the annual number of live births stood at 12.0345 million, and the total number of hospital admissions for surgeries across the country reached 66.6374 million person-times.

Even from these data alone, the enormous demand for rehabilitation services can be inferred; however, such demand remains unmet in public hospitals.

Although China is gradually improving the construction of its three-tier rehabilitation system, it remains common for tertiary hospitals to face bed shortages and for secondary hospitals to have insufficient resource allocation in their rehabilitation departments.

For public hospitals, bed turnover rate is a key performance indicator of operational efficiency. According to data from the Health Statistical Yearbook, since 2015, the average length of stay in public hospitals in China has shown a significant downward trend, with the average length of stay in tertiary hospitals decreasing from 10.4 days in 2015 to 9.3 days in 2020.

Furthermore, the comprehensive rollout of DRG/DIP has also accelerated bed turnover rates in public hospitals, particularly tertiary hospitals. Pilot results from regions such as Beijing, Shanghai, and Zhejiang indicate that DRG/DIP has effectively reduced the average length of stay for patients.

Total Hospitalization Expenditure for Cerebrovascular Diseases in China (100 Million Yuan)Data sourced from CEI Net

In neurology, the annual number of stroke cases is approximately 12 million. Stroke has a high mortality rate, with a one-year recurrence rate exceeding 17%. Furthermore, the incidence of nervous system tumors in China has reached 15 per 100,000 population. In particular, patients with gliomas and pituitary adenomas require prolonged hospitalization and often undergo rehabilitative therapy.

Taking Huashan Hospital, which boasts one of China’s top neurology specialties, as an example, its neurosurgical procedure volume has been growing at an annual rate of 20% in recent years. For conditions such as glioma, the typical postoperative recovery period is around 45 days; however, Huashan Hospital generally requires patients to be discharged within 10 days after surgery. How should the remaining 35 days of recovery be managed?

For acute neurological conditions, such as stroke, approximately 28 days of rehabilitation are required once vital signs have stabilized and neurological symptoms have ceased to progress. However, large tertiary hospitals typically require patients to be discharged after just seven days. Where should patients go for the remaining 20 days of care?

Given the relative scarcity of medical resources in China, and from the perspective of maximizing utility, beds in large tertiary Grade A hospitals are a scarce resource that must be allocated to where they are needed most. Consequently, these hospitals can only outsource this portion of rehabilitation care demand to external providers.

For the vast number of patients in the acute and subacute phases, their rehabilitation needs cannot be met by public hospitals.

In the future, the demand for inpatient rehabilitation among patients at public tertiary hospitals will continue to spill over.

From a business model perspective, private rehabilitation hospitals primarily serve the spillover demand for rehabilitation services from public tertiary (Grade A) hospitals.

Policy-level support is also being extended to the development of private rehabilitation hospitals. In June 2021, eight departments, including the National Health Commission and the China Disabled Persons’ Federation, jointly issued the Notice on Printing and Distributing the Opinions on Accelerating the Development of Rehabilitation Medical Services, which explicitly proposed supporting and guiding social forces to establish large-scale, chain-operated rehabilitation medical centers, and coordinating public medical institutions and socially operated medical resources within the region.

We can use Shanghai as an example to examine the business model of private rehabilitation hospitals.

As one of China’s top-tier Grade 3A hospitals, Huashan Hospital Affiliated to Fudan University is surrounded by several private rehabilitation hospitals, including Shanghai Yongci Rehabilitation Hospital, Shanghai New Start Rehabilitation Hospital, Shanghai Lanhai Rehabilitation Hospital, and Shanghai Hebin Rehabilitation Hospital. These facilities were established in the vicinity of Huashan Hospital to better accommodate the spillover demand for rehabilitation services from Huashan Hospital.

From the patient’s perspective, they would certainly prefer to trust Huashan Hospital. However, if Huashan Hospital is unable to provide postoperative rehabilitation services, most patients and their families would still be willing to seek care at a rehabilitation hospital located near Huashan, provided that Huashan physicians conduct regular visiting consultations there, medical insurance reimbursement is available, and the two institutions have established an official institutional partnership.

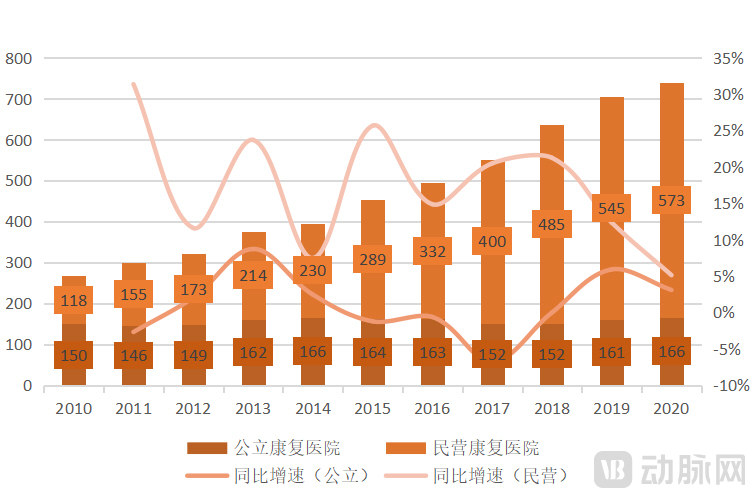

Changes in the Number of Rehabilitation Hospitals in ChinaData Source: China Health and Health Statistics Yearbook

Although the “Notice of the General Office of the National Health Commission on Launching Pilot Programs for Rehabilitation Medical Services,” issued in November 2021, required 15 provinces and municipalities to conduct rehabilitation pilot programs, guided the transformation of some primary and secondary hospitals within their jurisdictions into rehabilitation hospitals, and encouraged participation by community hospitals, numerous practical challenges have arisen in implementation.

In terms of business type, this segment of rehabilitation services falls under critical care rehabilitation. Neither secondary hospitals nor primary care institutions are well-equipped to handle it, whether in terms of technical capabilities or hardware infrastructure, while large tertiary Grade A hospitals lack the incentive to provide such services. This gap between secondary and tertiary care levels has created an ideal development environment for private rehabilitation hospitals.

In other words, this emerging rehabilitation market is a tertiary Grade A hospital-centric, spillover-driven market.

For private rehabilitation hospitals, how to effectively meet this demand has become the most critical issue.

For private rehabilitation hospitals, positioning themselves around Grade A tertiary hospitals has become a natural choice. Of course, not all Grade A tertiary hospitals are worth targeting; market size must also be taken into account.

Taking Shanghai as an example, the ideal scenario would certainly be to center operations around Huashan Hospital. However, given Shanghai’s substantial scale, it is also feasible to focus on other hospitals, such as the Sixth People’s Hospital, the Ninth People’s Hospital, as well as Zhongshan Hospital, Ruijin Hospital, Changhai Hospital, and Renji Hospital.

However, this may not necessarily be the case in non-tier-1 cities.

The gradual implementation of the policy for real-time settlement of cross-provincial medical insurance has enabled patients with subacute critical conditions, such as those with tumors or requiring neurosurgical care, to seek treatment at higher-level hospitals. According to data released by the National Health Commission, the provinces with the largest outflow of patients are Anhui, Hebei, Jiangsu, Zhejiang, and Henan, while the provinces with the largest inflow of inpatients are Shanghai, Beijing, Jiangsu, Zhejiang, and Guangdong.

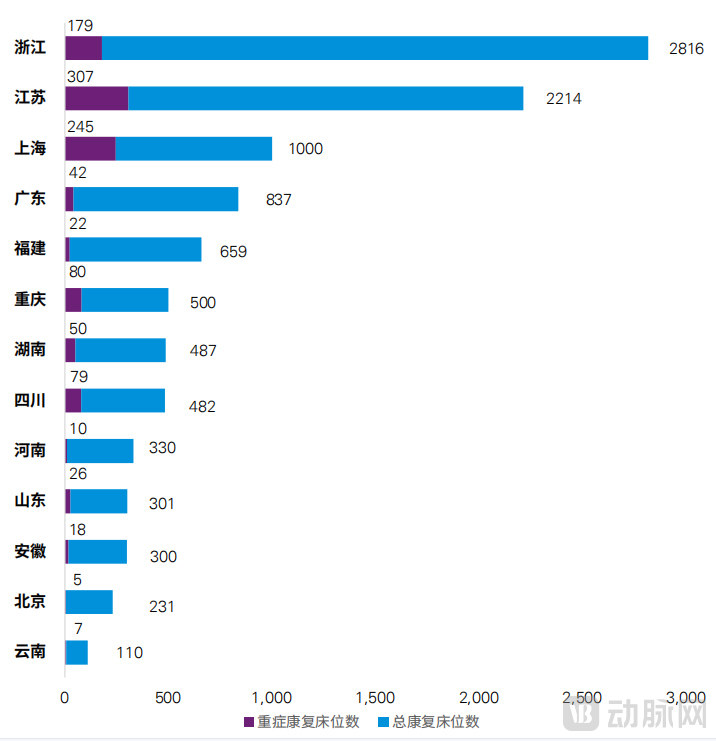

Distribution of Bed Counts Among the 31 Leading Rehabilitation Hospitals Selected by KPMG (Image source: KPMG)

Medical resources in high-tier cities are siphoning patients from surrounding areas. The continuous influx of patients has further accelerated the development of specialty disciplines at large tertiary Grade A hospitals and boosted their already high bed turnover rates. These hospitals are also adjusting their service structures to allocate more resources toward their leading specialties.

This has indirectly accelerated the spillover of rehabilitation demand from top-tier tertiary hospitals.

Although private rehabilitation hospitals also aspire to achieve scaled operations and adopt a chain development model, similar to other private specialty hospitals such as those in ophthalmology and dentistry, the market distribution of rehabilitation demand is not as evenly spread as that of other specialties. Blind expansion may prolong the payback period for investments.

An industry insider told VCBeat, “In addition to super markets like Beijing and Shanghai, cities such as Nanjing, Hangzhou, Wuhan, Guangzhou, Xi’an, and Chongqing are also good options, as their large Grade A tertiary hospitals cover relatively broad regions. Meanwhile, some of these hospitals have strong neurosurgery departments—such as Tongji Hospital in Wuhan and the First Affiliated Hospital of Sun Yat-sen University in Guangzhou—which also generate significant spillover demand for rehabilitation services.”

Certainly, lower-tier cities also have a market in this area, albeit on a relatively smaller scale, including Jinan, Hefei, Suzhou, Ningbo, Nanchang, Xiamen, Fuzhou, Changsha, Harbin, Lanzhou, and Zhengzhou. In such markets, the ability to establish partnerships with the top local tertiary hospitals (Grade 3A) becomes a key factor determining whether private rehabilitation hospitals can develop successfully.

Take Wuhan Mingzhou Rehabilitation Hospital and Changsha Mingzhou Rehabilitation Hospital, recently acquired by Sanxing Medical, as examples. Due to its institutional-level partnership with Tongji Hospital in Wuhan, Wuhan Mingzhou achieves a bed occupancy rate exceeding 80%. In contrast, Changsha Mingzhou, which has not secured a collaboration with Xiangya Hospital No. 1—the largest tertiary Grade A hospital in the local area—has a bed occupancy rate of approximately 50%, highlighting a significant disparity between the two facilities.

As for lower-tier markets, greater caution is warranted. Due to limited market size, local Grade 3A hospitals themselves face underutilized capacity and are undergoing business transformation, typically focusing on maternal and child health and rehabilitation services. Competing with public Grade 3A hospitals in a small-scale market is not an advisable strategy. Furthermore, there is a high likelihood that patients in these areas will be siphoned off by higher-level hospitals, leading to further contraction in demand.

Within the specialized fields of rehabilitation medicine, critical care rehabilitation (represented by neurological disorders), geriatric rehabilitation, and functional rehabilitation have become focal points for cross-sector expansion by listed companies, owing to their relatively high value. Consequently, private rehabilitation hospitals should structure their business operations around these core services.

The primary revenue source for rehabilitation hospitals is inpatient income; therefore, bed occupancy rate becomes the key determinant of a hospital’s profitability.

According to data from the Health Statistics Yearbook, in 2019, the bed occupancy rate of rehabilitation hospitals in China was only 65.84%, while that of general hospitals during the same period was 84.83%. The key to improving bed occupancy rates lies in whether private rehabilitation hospitals possess the core competitiveness in their technical solutions to accommodate patients referred from higher-level facilities. In this context, the High Dependency Unit (HDU) serves as a critical interface for establishing collaborations with tertiary hospitals.

ICU refers to the Intensive Care Unit. HDU stands for High Dependency Unit, which translates to "High Dependency Ward" in Chinese. The HDU serves as a transitional medical unit between the ICU and general wards, primarily catering to patients who have stabilized after ICU treatment and no longer require intensive monitoring, but still need a higher level of dependent monitoring and nursing care.

Within the High Dependency Unit (HDU), physicians with ICU backgrounds, rehabilitation specialists and therapists with early rehabilitation experience, and a nursing team with critical care expertise collaborate as a critical care rehabilitation team. Leveraging specialized monitoring, nursing, and rehabilitation equipment and facilities, this team enables rehabilitation treatment even for patients in a minimally conscious state, significantly reducing complications associated with prolonged bed rest, such as declined cardiopulmonary function, muscle atrophy, and joint contractures.

According to data from the 2018 article “Establishment of High Dependency Units” published in the Chinese PLA Journal of Hospital Administration, the bed occupancy rate of HDUs in a rehabilitation hospital ranged from 81.25% to 100%, ICU bed turnover increased by 53.33%, 89.26% of patients were transferred to general wards after showing improvement and recovery, and patient and family satisfaction reached 97.13%.

In recent years, an increasing number of private rehabilitation hospitals have successfully implemented the “ICU + HDU + General Ward” operational model, establishing a complete treatment continuum that facilitates stratified patient management and care. The ICU serves as a liaison for referrals from tertiary hospitals; after a brief period of observation in the ICU, patients are transferred to the High-Dependency Unit (HDU), where rehabilitation interventions are initiated to accelerate their recovery and transition to general wards.

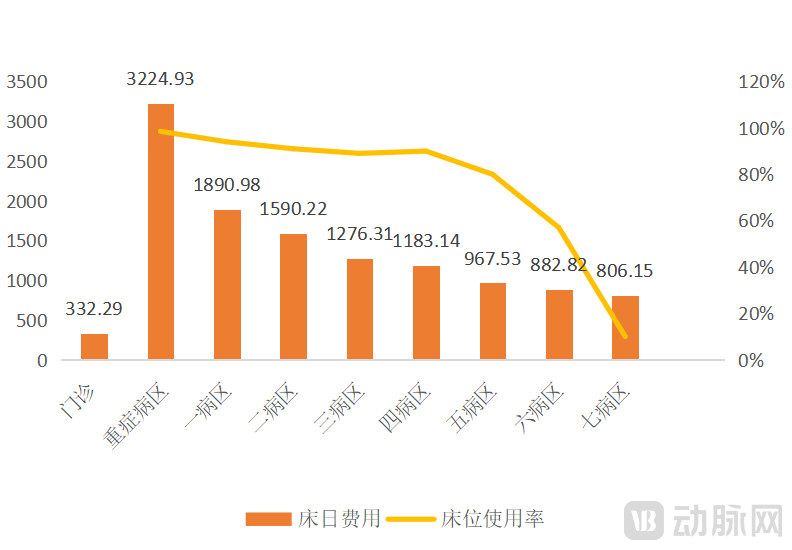

Nanjing Mingzhou Rehabilitation Hospital: Daily Bed Costs and Bed Occupancy Rates by Ward (Data Source: Corporate Announcements)

Furthermore, HDU wards are equipped with fewer devices than ICUs and place greater emphasis on the integration of rehabilitation equipment, such as bedside electric standing beds, pedal exercisers, and medium-frequency therapeutic apparatus. These devices occupy additional space, thus requiring larger ward areas compared to ICUs. Overall, however, HDUs entail significantly lower investment than ICUs while improving patient cure rates, thereby enhancing brand reputation and patient acquisition capabilities.

From a revenue perspective, critically ill patients requiring High Dependency Unit (HDU) care generally have longer recovery periods, which helps improve bed occupancy rates in rehabilitation hospitals. Data from Nanjing Mingzhou Rehabilitation Hospital also shows that the per-bed-day costs and bed occupancy rates in the intensive care unit are significantly higher than those in general wards.

The HDU ward, serving as a “buffer zone” between ICU and general wards, has become a key direction for the future development of critical care rehabilitation. For private rehabilitation hospitals, the establishment of an HDU ward will be a decisive factor in turning losses into profits.

Furthermore, some private rehabilitation hospitals have focused their specialized strengths on intelligent technologies. For instance, Shanghai Yongci Rehabilitation Hospital has implemented an Intelligent IoT Rehabilitation Hub through its collaboration with Fourier Intelligence. Within this IoT-enabled rehabilitation hub, a single therapist can manage 20 patients simultaneously during physical therapy sessions, facilitating a transition in rehabilitation care from labor-intensive to technology-intensive models and addressing the dual pain points faced by both patients and therapists.

From an operational perspective, compared to general hospitals, the single-hospital model of rehabilitation hospitals is asset-light and labor-intensive, with relatively low initial investment.

Taking Hangzhou Mingzhou Rehabilitation Hospital as an example, a 400-bed rehabilitation hospital with an operational area of approximately 20,000 square meters has purchased around 1,000 units/sets of medical equipment, including hyperbaric oxygen chambers, B-mode and color Doppler ultrasound systems, ventilators, patient monitors, EEG acquisition and testing devices, anesthesia machines, and electric operating tables, with a book value of approximately RMB 10 million. The annual site rental cost is about RMB 5 million. At maturity, the medical and nursing team comprises approximately 250 staff members, with annual labor costs of around RMB 40 million, accounting for 20–25% of revenue.

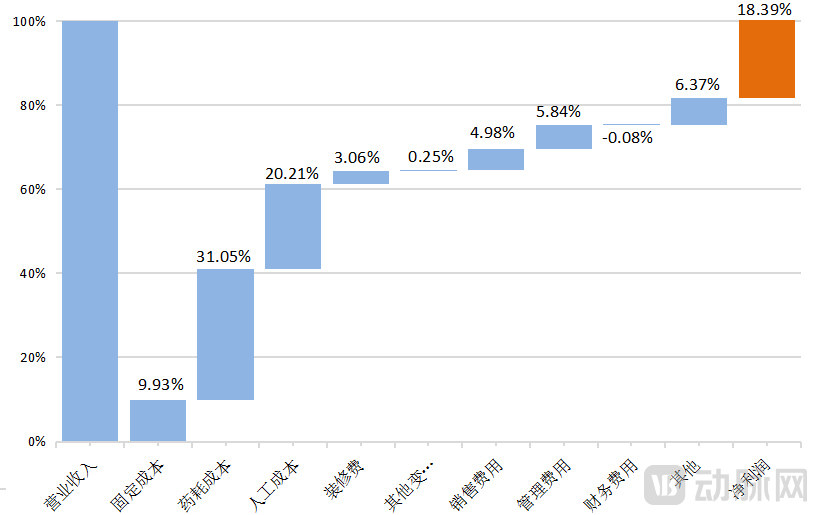

Breakdown of Revenue and Costs at Hangzhou Mingzhou Rehabilitation Hospital in 2020Data sourced from corporate announcements

Due to the nature of rehabilitation medical care, the daily revenue per bed in rehabilitation hospitals is limited. In 2020, the primary costs for Hangzhou Mingzhou Rehabilitation Hospital were pharmaceuticals and consumables (accounting for 31.50%) and labor (accounting for 20.21%). These two factors are also critical in rehabilitation operations and will directly impact profit margins.

Hangzhou Mingzhou Rehabilitation was established relatively early, operates with greater maturity, and maintains a relatively high net profit margin. Currently, the industry average stands at approximately 12%–16%.

From a business structure perspective, the most profitable services at rehabilitation hospitals are High Dependency Units (HDU), neurosurgery, and neurology. From the standpoint of rehabilitation hospitals, although the Intensive Care Unit (ICU) operates at a loss, it must be maintained as it serves as a channel for accepting patient transfers from tertiary hospitals.

For private rehabilitation hospitals, local healthcare security administrations impose varying requirements, necessitating the design of business structures tailored to these regulations. For instance, the Shanghai Healthcare Security Administration requires private rehabilitation hospitals that accept referrals from large tertiary Grade A hospitals to establish certain public-welfare rehabilitation programs, such as pediatric cerebral palsy rehabilitation. In contrast, Wuhan has no such requirement, allowing private rehabilitation hospitals to structure their services around a “golden combination” of ICU (Intensive Care Unit), HDU (High Dependency Unit), and neurological rehabilitation departments.

Although neurorehabilitation is the core business, strategic preparations should be made in advance for expanding into new service lines.

Currently, some private rehabilitation hospitals are entering the elderly care sector by leveraging their advantages in rehabilitation technology to create an integrated model of medical care and eldercare. Other rehabilitation hospitals are adopting a “specialty-focused plus general services” model, expanding into the treatment of other diseases to increase revenue from pharmaceuticals and medical consumables. Additionally, some institutions tailor their services to local conditions; for example, offering occupational injury rehabilitation in heavy industrial cities and specializing in rheumatic disease rehabilitation in coastal regions.

Gu Lian Medical Rehabilitation Business Structure | Source: Official Corporate Website

From the perspective of chain development, some industry insiders believe that there may still be a bonus period of about five years in the future. After that, policies in various regions will gradually align with Shanghai's approach, ranging from strict cost control to requirements for departmental setup, and enterprises need to adapt in advance. Since the profit margin of a single hospital is not high, it is necessary to pursue a path of scale expansion.

As previously analyzed, rehabilitation services are subject to certain geographical constraints. Consequently, many private rehabilitation hospitals have abandoned the traditional model of broad, nationwide expansion in favor of a chain-development strategy that focuses on increasing market share within their existing operational regions, or alternatively, they opt to expand their existing facilities.

Taking the five rehabilitation hospitals acquired by Sanxing Medical in its 2022 announcement as an example, each has a total bed capacity of over 200. Most are in a phase of rapid development, having already reached break-even, with rising bed utilization rates and improving profitability. Notably, three of these hospitals have plans to expand their bed capacity in the future.

For some private rehabilitation hospitals, expanding into other regions without the support of local public hospitals will pose many challenges. Take Hunan Development, a listed company, as an example. Although its core business is hydropower, it invested in Xiangya Boai Rehabilitation Hospital through its subsidiary. After achieving success, it began investing in four additional rehabilitation hospitals located in Changde, Hengyang, Xiangxi, and Wuhan, starting from 2015.

However, the other four entities performed poorly after losing support from the First Affiliated Hospital of Xiangya. Annual reports show that they sustained continuous losses and were ultimately transferred in 2019. Geographic expansion often tests not so much the capabilities of private rehabilitation hospitals themselves as their access to upstream medical resources.

For private rehabilitation hospitals, it is essential to assess their own strengths, integrate local medical resources, and establish clinical pathways for rehabilitation in areas where they hold a competitive advantage. These should be developed into core service lines and promoted among local tertiary general hospitals to establish stable referral mechanisms. Although fostering such collaborations takes time, positive reputation spreads rapidly among physicians.

Therefore, marketing efforts targeted at physicians are equally important. Organizing academic conferences is a common approach; for instance, showcasing novel treatment modalities at such events can enhance the overall reputation of private hospitals within the local medical community. Over time, private rehabilitation hospitals can establish a certain level of academic standing, which not only facilitates the creation of formal referral channels with tertiary (Grade 3A) hospitals but also supports their own business expansion.

In addition to the aforementioned factors, talent is another critical component; both business expansion and service replication require skilled personnel. Currently, there is a significant shortage of rehabilitation professionals in China. The ability to effectively build a talent team is crucial to the development of private rehabilitation hospitals. Whether through external recruitment, internal training, or multi-party collaborations, private rehabilitation hospitals need to make greater efforts in building their talent pipelines.

Demographic trends dictate that China will face a persistent shortage of rehabilitation services relative to demand for the foreseeable future, ushering private rehabilitation medical institutions into a golden age of development over the coming years. To establish a profitable rehabilitation hospital, it is essential to adopt the right operational model and avoid homogenization and marginalization, thereby enabling sustainable growth amidst the rising tide of the rehabilitation sector.