DaKang Medical Completes RMB 400 Million Series E Funding to Accelerate Expansion in China's Independent Hemodialysis Center Market

DiaCare Medical

Chain Medical Service Provider for Blood Purification

VCBeat has learned that on June 29, 2022, DiaCare Medical, a leading enterprise in the chain of independent hemodialysis centers, announced the completion of its RMB 400 million Series E financing round. This round of financing saw participation from local state-owned assets in Jiangxi and Jiangsu provinces, as well as from a well-known central enterprise’s rural revitalization fund.

The lead investor was Ganjiang Kaitou, the state-owned assets platform of Jiangxi Ganjiang New Area. It was followed by investments from China Central Enterprise Rural Industry Investment Fund Co., Ltd. (hereinafter referred to as “Central Enterprise Rural Investment Fund”) and Nanjing Gaoke Xinjun, a local state-owned enterprise in Jiangsu Province. Kaicheng Capital served as the financial advisor for this round of financing.

It is reported that this financing round represents the largest amount raised in recent years within China’s independent hemodialysis center healthcare services sector. Following this round, DiaCare Medical will pursue industry mergers and acquisitions, leveraging both organic growth and external expansion to further advance the chain-based, large-scale, and group-oriented development of independent hemodialysis centers in China.

This June, the hemodialysis sector, which had been quiet for some time, reached a turning point.

In addition to DiaCare Medical completing its RMB 400 million Series E financing, Chongqing Sunwisen successfully passed the review by the STAR Market on June 6. Subsequently, on June 10, the official website of the China Securities Regulatory Commission (CSRC) disclosed the acceptance notice for Shandong Weigao Blood Purification’s proposed overseas listing. The latter two companies are upstream enterprises primarily engaged in the production and sales of hemodialysis equipment and consumables.

Within just one month, the hemodialysis industry has sparked a minor surge in the capital market. Amid the broader trend of import substitution, and following ophthalmology, dentistry, health checkups, oncology, and medical aesthetics, will hemodialysis become the next hot investment sector?

Why Has the Hemodialysis Industry Been “Quiet” for a While? In fact, in the capital market, there are already numerous listed companies in the hemodialysis sector. More than ten A-share and Hong Kong-listed companies are associated with the hemodialysis concept, including Jafron Biomedical (hemoperfusion cartridges), Biolight Medical (dialysate), Xinhua Medical (dialyzers), Sanxin Medical (dialysate and catheters), Tianyi Medical (tubing sets), Weili Medical (catheters), as well as Hepalink, Qianhong Bio-pharma, Changshan Pharmaceutical, and Chase Sun Pharmaceutical, which are involved in heparin-related businesses. If Chongqing Sunwowa and WEGO Blood Purification successfully go public this year, the number of listed companies in the hemodialysis industry will further increase.

However, looking at the midstream dialysis medical services sector, no domestic companies have yet gone public on the U.S., Hong Kong, or A-share markets. As for the size of the dialysis services market, we will set aside the Chinese market for now and first examine the moves of foreign industry giants.

Fresenius of Europe and DaVita HealthCare of the United States are the two global giants in dialysis. The former is a company covering the entire industrial chain of dialysis equipment, consumables, and dialysis services, while the latter specializes in providing dialysis medical services. The former is known as the "King of Hemodialysis," and the latter is considered a Buffett concept stock due to its long-term holding by Berkshire Hathaway, under Warren Buffett, as its largest shareholder. In 2021, they achieved revenues of $19.941 billion and $11.619 billion, respectively, with after-tax profits of $1.38 billion and $1.212 billion.

But in March this year, Fresenius Group suddenly announced that it would spin off its Fresenius Care business and merge it with two other companies to establish an independent new company to provide kidney care services. The new company aims to target a potential market worth $170 billion.

Regarding the rationale behind this spin-off, Fresenius Group CEO Stephan Sturm explicitly stated that Fresenius had “not received sufficient valuation from the capital markets,” implying that the company aims to achieve better growth prospects through the demerger. The newly spun-off entity targets caring for and managing over 270,000 kidney disease patients by 2025, while overseeing approximately $11 billion in medical expenditures in the same year. According to Fresenius’ annual report, the company operated 4,171 dialysis centers worldwide in 2021, serving approximately 345,000 dialysis patients globally.

In the United States, a total population of 333 million is served by over 7,000 dialysis centers, catering to more than 570,000 patients. In Japan, with a population of 126 million, there are more than 4,400 dialysis facilities serving over 340,000 hemodialysis patients. Meanwhile, in China’s Taiwan region, a population of 23 million is supported by nearly 600 dialysis centers, which serve approximately 60,000 dialysis patients.

According to data from the China National Renal Data System (hereinafter referred to as “CNRDS”), the number of patients with end-stage renal disease (ESRD), also known as uremia, undergoing dialysis in China was 160,000 in 2010 and reached 820,000 in 2020, representing a compound annual growth rate of 41.25% for dialysis patients over the past decade.

In the future, with the advent of an aging society, the number of dialysis patients in China is projected to exceed 3 million by 2035. Currently, however, there are only about 6,000 dialysis institutions in China, including hospital hemodialysis units and independent hemodialysis centers, indicating a substantial market gap.

In terms of cost, the average annual treatment expense for hemodialysis patients in China is approximately RMB 80,000. With 3 million potential patients, the market size exceeds RMB 200 billion; however, this still represents a substantial gap compared to Fresenius’s projected total market value of USD 170 billion.

As expected, both Weigao Blood Purification and Chongqing Sunwowa are set to list on the capital markets within the year. DiaCare Medical specializes in dialysis services and does not engage in the production or sales of dialysis products. As a pilot unit spearheaded by the former Ministry of Health for independent hemodialysis centers, it currently operates the largest number of such centers nationwide, with nearly 60 independent hemodialysis centers in operation across 15 provinces, including Jiangxi, Shandong, Yunnan, and Guizhou.

It is reported that this financing round represents the largest investment in China’s independent hemodialysis center sector in recent years. Regarding the company’s development following this funding, Chen Shaobo, Founder and Chairman of DiaCare Medical, stated that the company will pursue industry mergers and acquisitions. Through both organic growth and inorganic expansion, DiaCare Medical aims to promote the chain operation, scaling, and group-based development of independent hemodialysis centers across China.

Chen Shaobo, Chairman of DiaCare Medical

Regardless, within the RMB 100 billion hemodialysis market, each niche segment will give rise to industry leaders.

Compared to other specialized medical services such as ophthalmology, dentistry, health check-ups, oncology, medical aesthetics, and radiotherapy/chemotherapy, the national deregulation of independent hemodialysis centers occurred relatively late.

In December 2016, the former National Health and Family Planning Commission issued the “Notice on Issuing the Basic Standards and Management Specifications for Hemodialysis Centers (Trial)” (commonly referred to in the industry as “Document No. 67”), which formally recognized independent hemodialysis centers as distinct medical institutions. The notice clarified the standards and regulations for establishing such centers, permitted social capital to participate in their establishment, encouraged the development of hemodialysis centers into chain and group-based models, and established a priority approval process for applicants seeking to establish group-based or chain-operated hemodialysis centers.

Although independent hemodialysis centers were liberalized at a later stage, more than five years of development have yielded significant results: by the end of 2021, there were over 740 independently operated hemodialysis centers registered with industrial and commercial authorities in China, with more than 400 formally in operation.

However, compared with the more than 30-year development history of hemodialysis centers in developed countries such as those in Europe, the United States, and Japan, independent hemodialysis centers in China have just ushered in their first five years of development.

According to the information disclosed in Shanwaishan’s prospectus, with a foothold in the hemodialysis market, Shanwaishan aims to build an integrated “equipment + consumables + services + informatics” four-in-one full industry chain for hemodialysis, with medical services constituting its third-largest business segment.

During the reporting period, Shanwaishan had a total of 18 medical institutions, most of which were established in 2017 and 2018. In 2021, Shanwaishan transferred and deregistered one hospital and eight dialysis centers that had not commenced actual operations. Currently, nine dialysis centers are operating normally. The core operational metrics for Shanwaishan’s dialysis services are shown in the figure below:

The above data are compiled from Shanwaishan’s prospectus.

Based on the general process of investing in and establishing an independent hemodialysis center, the key stages are as follows: site selection → renovation → application for medical institution practice license → obtaining designated status under the medical insurance scheme → official opening → ramp-up period → break-even period → maturity period (profitability phase). Typically, the timeline from applying for the medical institution practice license to securing medical insurance designation and commencing formal operations takes approximately 1 to 1.5 years.

The nine centers of Shanshan Waiwai were primarily established in 2017 and 2018, based on business registration records. When accounting for the time required to obtain medical institution practice licenses and designated health insurance provider status, their official opening dates were concentrated in the second half of 2018 and the second half of 2019. Consequently, the majority of these nine centers are still in the ramp-up phase, while a few that were established earlier may have already entered the profitability stage.

Taking the profitable Tongliang Shanwaishan Dialysis Center as an example, the center was established in May 2018 with an area of 1,120 square meters. It obtained its medical practice license in September 2018 and officially commenced operations in the first half of 2019 after being included in the national health insurance program. By the end of 2021, it had achieved a net profit of RMB 1.038 million in less than three years of operation. Back-calculating from this performance, the center likely reached break-even in 2020, aligning with the standard investment model for independent hemodialysis centers.

From a revenue perspective, based on the average annual revenue per patient for Shanwaishan from 2018 to 2021, the average annual revenue per patient exceeded RMB 100,000, reaching over RMB 110,000 in certain years (e.g., 2020). If the remaining eight centers of Shanwaishan can each achieve an average annual net profit of RMB 1 million over the next two years, the nine centers combined would generate more than RMB 9 million in net profit, corresponding to a net profit margin of 10%. This would make a significant contribution to Shanwaishan’s overall profitability.

According to Chen Shaobo, after nearly a decade of development, DiaCare Medical has initially achieved the commercialization of independent hemodialysis centers in China, with the group achieving overall profitability as early as 2019.

Investment firms that have conducted research on hemodialysis medical services told the author that, compared to hospitals, individual independent dialysis centers generally cover an area of 1,000–1,500 square meters, with an initial capital investment of approximately RMB 4.5 million. If the location is well-chosen, market competition is not overly intense, and medical insurance reimbursement rates are favorable, these centers can typically break even within one year after obtaining medical insurance designation. After two years, net profits can reach RMB 800,000–1,000,000, with a typical payback period of five and a half years.

“Of course, for medical services, setting aside the aforementioned metrics, dialysis centers ultimately compete on operational capabilities,” said the investor.

However, in reality, investors in the hemodialysis sector often grapple with whether to invest in pure dialysis services or in the entire hemodialysis industry chain.

As there are no publicly listed companies in China that, like DaVita HealthCare in the United States, focus exclusively on healthcare services, a direct comparison of their business models is not yet feasible. Nevertheless, this article attempts to compare the fiscal 2021 financial data of DaVita and Fresenius.

Data sourced from Hithink iFinD

Data sourced from Hithink iFinD

As can be seen from the table above, despite having over $8 billion less in revenue, DaVita’s pre-tax profit, after-tax profit, and net cash flow from operating activities were only marginally lower than those of Fresenius. Focusing solely on dialysis services, Fresenius’s 2021 annual report shows that dialysis services and dialysis products accounted for 79% and 21% of its business, respectively. Its dialysis service revenue reached $15.753 billion, significantly higher than DaVita’s; however, its profitability was not substantially stronger than that of DaVita.

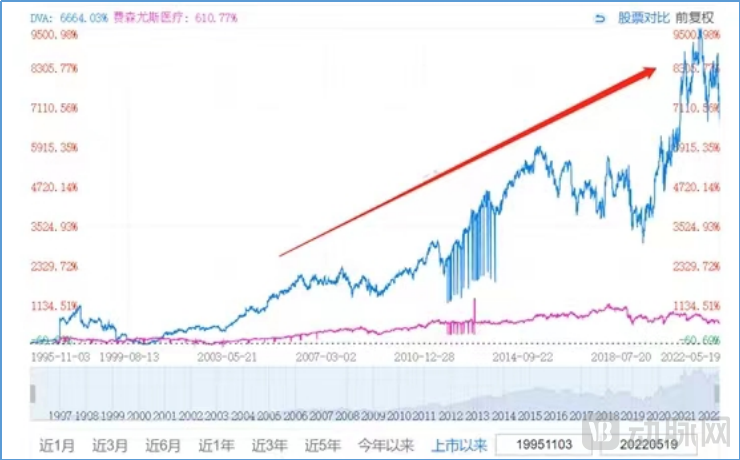

Furthermore, as shown in the chart below depicting the stock price trends of DaVita and Fresenius, both companies went public in 1995 and 1996, respectively. Since their IPOs, DaVita has consistently outperformed Fresenius in terms of stock performance, which explains why Fresenius decided to spin off its healthcare services segment.

DaVita and Fresenius: Stock Price Trends Since Their IPOs

Therefore, in its prospectus, Shanshan Waiwai also revealed its reluctance to divest from dialysis centers. In its annual report, the company stated that, based on a comprehensive assessment of the current state and trends of industry development as well as its future strategic plans, it would use its own funds to establish a chain of hemodialysis centers. This initiative aims to further promote the community-based and chained development of hemodialysis centers, fully leveraging the advantages of integrated full-industry-chain operations and end-to-end informatized health management.

At DiaCare Medical’s Series E financing press conference on June 29, although the company did not disclose its capital market plans, it is expected to accelerate its IPO process following the completion of this funding round.

Perhaps in the near future, China’s hemodialysis sector will also see the emergence of giants spanning different segments, akin to DaVita and Fresenius. After all, compared with the several decades of development in overseas markets, China’s hemodialysis industry—encompassing upstream manufacturing and midstream medical services—has only been evolving for a mere ten to several years.

Seizing the tailwinds of import substitution and tapping into the future pool of 3 million potential hemodialysis patients in China, market opportunities are immense across both manufacturing and service sectors.

As the saying goes, the hemodialysis sector, a market worth hundreds of billions, is still in its ascendant phase.