China's Domestic Medical Imaging Equipment Firms Rush to IPO: Opportunity or Disruption?

The History of China’s Medical Imaging Equipment: A Development Narrative Centered on “Domestic Substitution”From ultrasound and digital radiography (DR) to magnetic resonance imaging (MRI) and positron emission tomography/computed tomography (PET/CT), medical imaging companies have typically focused on two key strategies: capturing hospital market share from multinational corporations, and competing with domestic rivals for the private-sector and primary-care markets.

Nowadays, the coverage rate of medical imaging equipment in hospitals at all levels is gradually increasing. However, grassroots public health institutions are facing financial constraints, and domestic companies are showing signs of fatigue in their strategies. According to statistical data provided by iResearch Consulting and LeadLeo Research Institute: from 2021 to 2025, the compound annual growth rate (CAGR) of China's medical device market size is 16.2%, while the global imaging equipment industry market size growth rate is only 5.5%, with a domestic growth rate of 9.7%.

The Battle for Breakthroughs Waits for No One. On June 29, two medical imaging equipment companies, MinFound and Zhejiang Langshi Instrument Co., Ltd., simultaneously launched IPOs on the STAR Market, sounding the charge while also revealing a wealth of underlying market data.

Where Is the Future of Domestically Produced Medical Imaging Equipment? Behind Two Companies, We May Find Clues to the Next Chapter.

MinFound, the third-largest domestic CT manufacturer, and Zhejiang Langshi Instrument Co., Ltd., the second-largest domestic CBCT (Cone Beam CT) manufacturer, can be seen as a microcosm of two distinct schools in the field of medical imaging equipment.

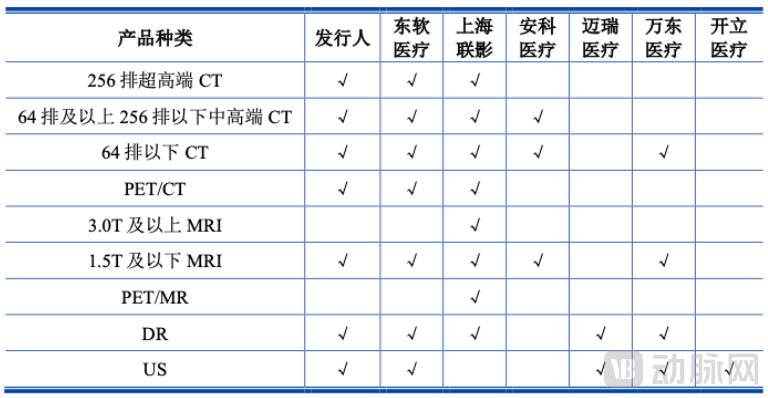

MinFound represents a major domestic manufacturer of medical equipment, having built a comprehensive product portfolio that includes CT scanners across the full range, 1.5T MRI systems, DR, ultrasound, and PET/CT. Its product breadth is comparable to that of GPS (GE Healthcare, Philips, and Siemens Healthineers), United Imaging Healthcare, and Neusoft Medical.

Product Line Layout of Imaging Companies (Source: MinFound's Prospectus))

Product Line Layout of Imaging Companies (Source: MinFound's Prospectus))

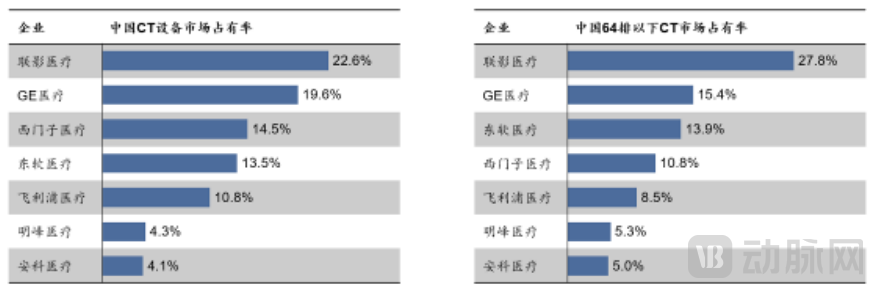

CT is MinFound’s fastest-growing and most comprehensive product line, offering 8-slice, 16-slice, 24-slice, 48-slice, 64-slice, and 256-slice models, as well as mobile CT units and the Ark CT series. Ranked by the market share of newly installed units in 2021, MinFound placed sixth among all CT manufacturers in China, third among domestic manufacturers, and third among Chinese brands in export volume.

2021 Competitive Landscape of the CT Equipment Market in China

In addition to CT, MinFound has obtained medical device registration certificates for two models of 1.5T superconducting MR systems, four DR systems, and two ultrasound devices. However, its commercialization efforts have lagged behind, failing to achieve large-scale market deployment. MinFound attributes this to constraints in production capacity and funding, which are also among the primary objectives of its current IPO.

In the realm of high-end imaging products, MinFound will primarily focus on its ultra-high-end 512-slice CT, the QuantumEye 799 CT, and the ultra-high-end ScintCare PET/CT 750T. The QuantumEye 799 features the industry’s only 16 cm true spherical wide-body detector and quantum spectral technology, while the ScintCare PET/CT 750T achieves an ultra-high system sensitivity of 23.5 kcps/MBq (NEMA). These two products are poised to challenge the high-end imaging landscape currently dominated by GPS.

Compared with MinFound, Zhejiang Langshi Instrument Co., Ltd. has a relatively narrow product portfolio, focusing exclusively on the research, development, and sales of dental cone-beam CT systems for the field of oral healthcare.

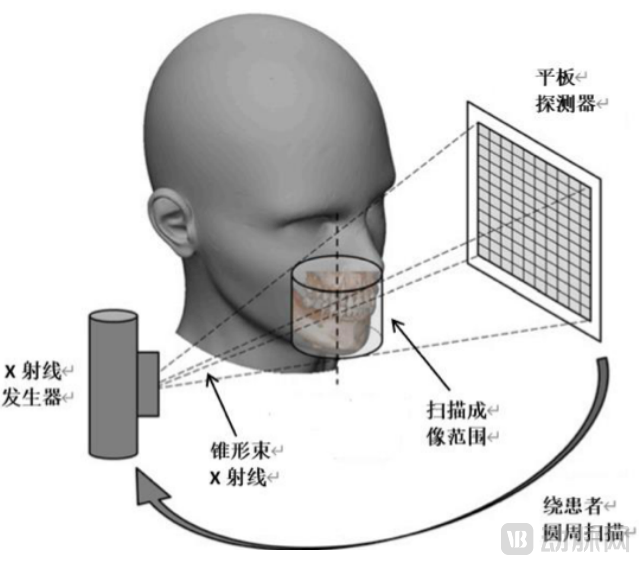

Oral Cone-Beam CT is a cone-beam CT system primarily designed for three-dimensional imaging of the oral and maxillofacial region. It is widely used across various dental specialties, including dental implantology, orthodontics, endodontics, and oral and maxillofacial surgery. Particularly in complex applications such as dental implants, oral cone-beam CT plays an irreplaceable and critical role.

Compared with traditional general-purpose spiral CT, dental cone-beam CT offers advantages such as high resolution, low radiation dose, small footprint, and low operating cost. It is a revolutionary device in the field of dental imaging and is widely used in dental medical institutions at all levels.

Principles of Cone Beam CT (Source: Langshi Instrument Prospectus)

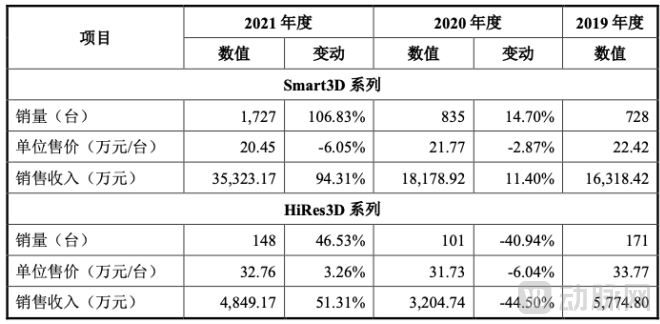

Langshi Instrument’s product lines are primarily structured to serve their respective markets, consisting mainly of the HiRes3D and Smart3D series.

The Smart3D product series is primarily positioned for primary healthcare institutions. In 2021, the unit price was RMB 204,500 per device. This model features the capability to capture all four types of X-ray images required by dental medical institutions with a single unit, enabling CBCT, panoramic, cephalometric, and intraoral imaging. For general dental medical institutions, this highly integrated four-in-one solution eliminates the need to purchase multiple imaging devices, thereby reducing procurement costs and facilitating more convenient operation for clinicians and data management for patients.

The HiRes3D series is primarily targeted at public hospitals and high-end private medical institutions, with a unit price of RMB 327,600 in 2021. Its patient population is characterized by high volume, complex conditions, and limited individual consultation time. Consequently, there are stringent requirements for CBCT equipment, including high-frequency operation and imaging, visualization of finer tissue structures, and scanning coverage of larger wound areas. These demands entail greater technical complexity, leading to a higher average unit price.

From a production line perspective, MinFound boasts a rich and well-structured portfolio. It not only maintains a CT product line that generates revenue but also explores fields such as ultrasound and MR, securing potential for future commercialization. In this regard, Zhejiang Langshi Instrument Co., Ltd. targets a relatively narrow sector; however, its product lineup is highly concentrated, which likewise limits its growth ceiling.

However, MinFound faces a market landscape dominated by the “GPS” trio (GE Healthcare, Philips, and Siemens Healthineers) externally, while contending with fierce competition from domestic rivals such as United Imaging and Neusoft internally. Despite having a comprehensive product portfolio, MinFound still relies on its sales capabilities and platform infrastructure to convert technological advantages into profitability. From this perspective, there remain significant hurdles for MinFound to overcome in achieving successful commercialization of its products.

In contrast, the CBCT market in which Zhejiang Langshi Instrument Co., Ltd. operates faces limited competition. Apart from some overseas companies, Meiya Optoelectronic is the only domestically listed company that directly competes with it, and their market shares are relatively close, thereby facilitating easier product commercialization.

Further Analysis of Financial Data. Despite MinFound’s extensive product portfolio, its profitability remains unoptimistic.

According to the prospectus data of MinFound, the company’s operating revenues in 2019, 2020, and 2021 were RMB 211 million, RMB 300 million, and RMB 352 million, respectively, while the net profits were -RMB 213 million, -RMB 231 million, and -RMB 207 million, respectively.

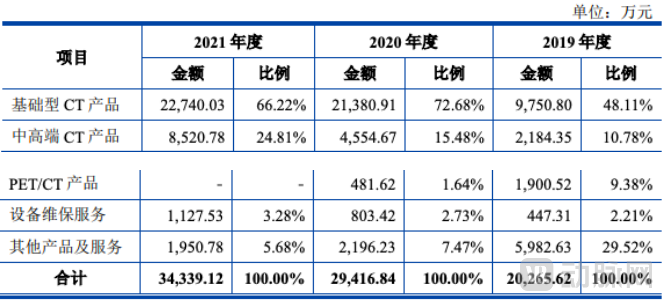

Notably, over 90% of MinFound’s revenue is derived from CT scanners, indicating an extreme reliance on the cash flow generated by the CT boom.

Revenue Composition of MinFound (Source: MinFound Prospectus)

Langshi Instrument faces an even more severe revenue concentration than MinFound. During the reporting period, Langshi Instrument’s primary sources of revenue were dental cone-beam CT products and software products, with dental cone-beam CT products accounting for 99.89%, 99.99%, and 99.98% of annual revenue, respectively. The company’s development is closely tied to industry prospects.

Sales Data for Various Devices from Langshi Instruments

The difference lies in profitability. From 2019 to 2021, Zhejiang Langshi Instrument Co., Ltd. reported operating revenues of RMB 221 million, RMB 219 million, and RMB 410 million, respectively, placing it on par with MinFound in terms of scale. However, its net profits for the same period were RMB 20 million, RMB 18 million, and RMB 64 million, respectively, maintaining consistent profitability throughout.

Ultimately, gross profit margin and R&D investment can explain the differences between the two companies.

Comparison of Gross Profit Margins Between Two Companies. In 2021, MinFound's gross profit margin was 18.15%, while Zhejiang Langshi Instrument Co., Ltd.'s gross profit margin was 41.33%.

A significant portion of the cost disparity stems from procurement costs for components. MinFound’s CT systems are predominantly spiral CTs, with core components such as X-ray tubes and high-voltage generators primarily sourced through external procurement, resulting in higher costs. In contrast, Zhejiang Langshi Instrument Co., Ltd.’s cone-beam CT systems benefit from lower core component costs. Their imaging method employs conical X-rays emitted by an X-ray generator without requiring rotation, thereby eliminating the need for core components such as slip rings and high-voltage generators. This reduces both unit price and overall costs, enabling the company to maintain higher gross margins and achieve greater profitability.

On the other hand, the influencing factors are attributed to R&D costs. From 2019 to 2021, the R&D expenses of Zhejiang Langshi Instrument Co., Ltd. were RMB 20.9591 million, RMB 23.6376 million, and RMB 36.2850 million, respectively, while those of MinFound were RMB 81.6740 million, RMB 75.8239 million, and RMB 91.7355 million, respectively, which were 3–4 times those of Zhejiang Langshi Instrument Co., Ltd.

Relying solely on data, we can draw a rough conclusion: MinFound has indeed made substantial investments in R&D and successfully developed a series of cutting-edge technologies. However, in the highly competitive “red ocean” market for CT scanners, hospitals are not yet willing to pay for MinFound’s high-end CT systems. In contrast, although Zhejiang Langshi Instrument Co., Ltd. has invested less in R&D, its outcomes better align with market demands under conditions of weaker competition, enabling rapid adoption by hospitals and ultimately achieving profitability.

Different developmental logic choices have guided two medical imaging equipment companies onto divergent paths, resulting in significant differences in the core factors influencing their future development.

MinFound’s growth inflection point lies in its strategic layout across multiple niche imaging segments. Its ScintCare PET/CT received NMPA approval in 2021, and the associated revenue was not included in the prospectus.

QuantumEye, a 256-slice ultra-high-end CT system, is MinFound’s key product for entering the high-end CT market and holds significant growth potential amid the broader trend of domestic substitution. The device received approval in 2020 through the green channel for innovative medical devices, and it is expected to substantially elevate MinFound’s revenue scale in subsequent financial reports.

Beyond its high-end equipment, the profit outlook for MinFound’s DR and ultrasound product lines is less optimistic. Although DR and ultrasound systems boast high gross margins and MinFound has obtained approval for a few products, these two niche segments are highly fragmented, limiting the market share that any single product can capture.

Furthermore, to capture the high-end ultrasound market from GPS and vie for the mid-to-low-end market against Mindray, Sonoscape, and Shantou Institute of Ultrasonic Instruments, MinFound must identify a flagship technology as its brand core and cultivate it over many years to create the possibility of profitability. This path appears somewhat protracted, and the returns are not particularly attractive. The same logic applies to DR.

Building an Ecosystem: It has become a consensus among leading medical imaging companies to shift from hardware-supported revenue to a model supported by both software and hardware. However, MinFound’s ecosystem construction is relatively weak, lacking the conditions for software profitability. If it can strengthen its digital transformation in the future, MinFound may be able to create new growth points.

Langshi Instrument is expected to remain profitable in the coming years by leveraging its cone-beam CT (CBCT) technology; therefore, its product portfolio is unlikely to undergo significant changes in the short term. To identify new growth drivers, Langshi Instrument is moving closer to CBCT-guided radiotherapy and dual-source, dual-detector CBCT solutions.

Cone-beam CT offers advantages such as superior image quality, lower radiation dose, and reduced cost in imaging high-density tissues or organs. Beyond its applications in dental diagnosis and treatment, it is also utilized in the field of precision radiotherapy. Pre-treatment cone-beam CT scans generate three-dimensional reconstructed images of the lesion area, enabling the assessment of positional errors of the tumor in three dimensions, thereby further enhancing the accuracy of radiotherapy.

Furthermore, there is also significant potential for the application of cone-beam CT (CBCT) in otolaryngology and orthopedics. Currently, specialized digital imaging diagnostic equipment for otolaryngology has not yet been widely adopted in the market; hospitals still predominantly use general-purpose spiral CT scanners for otolaryngological imaging examinations. Due to its high-resolution capability, CBCT can clearly visualize the subtle anatomical structures of the ear, nose, and throat, thereby improving the rationality of preoperative planning, the precision of intraoperative procedures, and the accuracy of postoperative follow-up assessments. According to the prospectus, Zhejiang Langshi Instrument Co., Ltd. is about to launch a dual-source, dual-detector CBCT system designed specifically for the field of otolaryngology, taking an early lead in this emerging market.

Since there are no domestic pioneers to validate the feasibility of the track that Zhejiang Langshi Instrument Co., Ltd. is entering, we cannot currently determine whether the company can successfully turn it into a new revenue stream. However, compared with MinFound, Zhejiang Langshi Instrument Co., Ltd. has ample cash flow to support its exploratory efforts. With more opportunities for trial and error, the company may be able to identify other high-value, low-competition scenarios, such as cone-beam CT.

In addition to MinFound and Zhejiang Langshi Instrument Co., Ltd., domestic medical imaging companies such as Neusoft Medical, United Imaging Healthcare, and Shantou Institute of Ultrasonic Instruments have also filed prospectuses in the past year. As numerous enterprises seek transformation, losses have become the norm.

Ultimately, the development of medical imaging equipment is inherently R&D-intensive, capital-heavy, and reliant on brand reputation. To maintain the competitiveness of their product lines, Chinese medical imaging companies such as Neusoft Medical and MinFound, which benchmark against the “GPS” giants (GE Healthcare, Philips, and Siemens Healthineers), sustain high levels of R&D investment annually. Although these companies generate substantial revenue, they struggle to achieve profitability. Even United Imaging Healthcare, which was on the verge of going public, devoted nearly a decade to continuous investment before finally turning profitable in 2021.

In contrast, companies such as Zhejiang Langshi Instrument Co., Ltd. and Shantou Ultrasonic Electronics have opted for a narrower product scope. While their growth ceiling is visibly limited, they have managed to sustain long-term profitability and continuous innovation in the market.

Sustained high investment does not necessarily yield technological outputs that surpass industry standards, nor do technologically advanced startups always gain market recognition. Against this backdrop, traditional medical imaging equipment companies must develop clearer strategic plans and layouts for the future before blindly pursuing “high-end, precision, and cutting-edge” technologies.

As competition in the medical imaging equipment sector reaches a fever pitch, companies of all sizes are expanding their product lines to seek new growth drivers. In this context, businesses may wish to consider specialized, niche segments such as cone-beam CT (CBCT). In a crowded marketplace, being a big fish in a small pond may prove more advantageous than being a small fish in a large one.