Top VCs Enter the Arena as Companies Rush to IPO: Balding Gen-Z and Millennials Ignite a Trillion-Yuan Hair Loss Market

2.5 Billion People Suffering from Hair Loss Are Igniting a Hundred-Billion-Yuan Market.

Following the listing of Yonghe Medical, the leading hair transplant company, on the Hong Kong Stock Exchange last December (with a current market capitalization exceeding HK$5.5 billion), Barley Hair Transplant Medical (Shenzhen) Group Co., Ltd. (hereinafter referred to as “Barley Hair Transplant”) has recently submitted its prospectus to the Hong Kong Stock Exchange, positioning itself to become China’s second publicly listed hair transplant enterprise.

Founded in 2015, Barley Hair Transplant positions itself as a mid-to-high-end medical group specializing in hair disorder diagnosis and treatment. Its services span the entire lifecycle of hair care, including consultation and diagnosis, micro-needle hair transplantation, and hair stabilization and nourishment therapies, with its core competency lying in “micro-needle hair transplantation” technology. According to a report by Frost & Sullivan, Barley Hair Transplant holds the largest market share among hair disorder diagnosis and treatment service providers in China’s first-tier cities.

According to the prospectus, Barley Hair Transplant’s business primarily comprises surgical hair transplantation and non-surgical hair stabilization and care, which accounted for 79% and 21%, respectively, of its total revenue in 2021. From 2019 to 2021, Barley Hair Transplant’s total revenue reached RMB 747 million, RMB 764 million, and RMB 1.021 billion, respectively. In terms of revenue, Barley Hair Transplant held a 5.2% market share in 2021.

In addition to the continued boom in the secondary market, the primary market remains equally hot.Over the past year, multiple innovative companies—including HardCore Pharma, Keshilife, Tekelo Bio, Stemson Therapeutics, and Revela—have secured financing, with investors such as Sequoia Capital, IDG Capital, Tiantu Investment, Yuanjing Capital, CDH VGC, Maki VC, Montage Ventures, and K5 Global backing these ventures.

Behind the wave of hair transplant clinics going public and the accelerated investments by top-tier venture capital firms lies a vast, unmet market demand. According to survey data from the National Health Commission, 250 million people in China currently suffer from hair loss, with post-90s individuals accounting for 39.3% and post-80s individuals making up 37.9%.It is evident that young people's demand for hair loss treatment has experienced explosive growth, becoming a significant driving force in the hair loss market.

“Battle for the Balding Perimeter” Has Begun Amid a Vast Hair Loss Population and the Trend of Affected Individuals Getting Younger

#01

“Bald”ness Strikes Suddenly: 250 Million People with Hair Loss Fuel a Hundred-Billion-Yuan Market

“Bald”ness Comes Suddenly.

"Nowadays, an increasing number of young people are experiencing anxiety about their hair, repeatedly sparking hot topics."For instance, on Weibo, the topic “Hair Loss Among Post-90s Generation Occurs 20 Years Earlier” has garnered over 140 million views and more than 53,000 user comments. Matching this atmosphere, a flood of advertisements for hair care, hair regrowth, and hair transplantation are continuously displayed and broadcast across buses, office buildings, elevators, news feeds, and short-video platforms.

However, for most people, hair loss is actually a normal phenomenon. This is because hair grows in cycles: it undergoes a growth phase lasting 2 to 6 years, followed by a catagen (regression) phase of about 3 weeks, and finally enters the telogen (resting) phase, which lasts approximately 3 months. After this period, the hair follicle re-enters the growth phase, and the cycle repeats. Therefore, some natural hair shedding occurs in daily life, with an average daily loss of around 50 hairs, generally not exceeding 100. Hair loss within this range is considered normal.

Therefore, medical consultation, pharmacological treatment, or hair transplant surgery should only be considered if excessive hair shedding persists over a long period, with daily hair loss exceeding 100 strands.

“However, with the growing number of young people experiencing hair loss, consumer demands in the overall market have undergone a significant shift—from treating hair loss as a medical condition to enhancing physical appearance. Many individuals born in the 1980s and 1990s believe that hair loss undermines their confidence and makes it more difficult to find a partner."The head of the consumer healthcare division at a leading e-commerce platform told VCBeat."

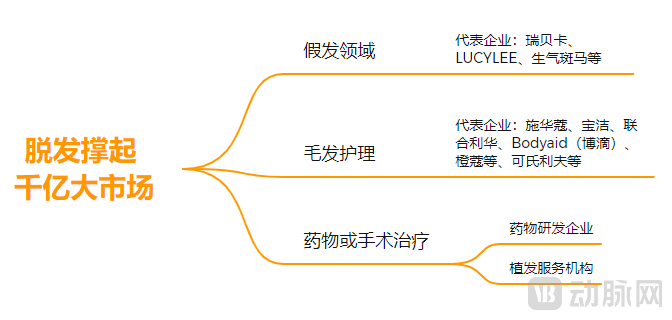

It is precisely on this basis that the demand for addressing hair loss has gradually given rise to a hundred-billion-yuan market dominated by wigs, hair care, and treatments.

Wigs and hair care belong to a relatively traditional sector. In the wig industry, China has produced Rebecca, the country’s first publicly listed wig company. Additionally, within the past year, wig accessory brand “LUCYLEE” and emerging hair and makeup brand “Shengqi Banma” have successively secured financing.

In the hair care sector, multinational FMCG brands such as Schwarzkopf, Procter & Gamble, and Unilever have established a strong presence, alongside emerging enterprises like Bodyaid (Bodi), Chengkou, and Keshilifu, all of which have launched anti-hair loss care products. Notably, Yunnan Baiyao and Tongrentang are also actively expanding into this field.

“If the market demand for hair loss is stratified, the lowest tier is the wig market, which has relatively low entry barriers and represents a typical consumer sector. The next tier up is hair care and maintenance, a field with numerous competitors and intense competition. The highest tier is the therapeutic segment, encompassing pharmacological treatments and hair transplant surgeries, which has the highest entry barriers.“A senior industry investor stated that breakthroughs in treatment are the key determinant of the hair loss market’s ceiling.”

Currently, there are four primary approaches to treating hair loss: first, adjusting one's physical condition; second, alleviating symptoms through dietary supplements; third, pharmacological treatment; and fourth, hair transplantation surgery.

“In the early stages of hair loss, the condition can be improved and reversed through pharmacological treatment and regulation of physical health; hair transplantation is often considered a last resort,” Dr. Li Mei, Standing Committee Member of the China Hair Transplant Association, previously told VCBeat.

Amidst the vast untapped potential of the hair loss treatment market, a growing number of companies are entering the fray, driving an industry boom through increasingly diverse and differentiated products and solutions.

#02

“Battle Against Baldness”: Opportunities and Challenges in Two Core Sub-sectors

"The Battle Against Baldness" Is Underway.

From the perspective of current industry development, the treatment of hair loss primarily comprises two core sub-sectors: pharmacological therapy and hair transplant surgery, corresponding to new drug R&D enterprises and hair transplant service providers, respectively.

On the pharmaceutical front, although numerous companies have entered the field, existing solutions remain scarce due to the high difficulty and risks associated with innovation.

It is worth noting that since the FDA approved two androgenetic alopecia drugs, minoxidil and finasteride, in 1988 and 1997 respectively, it was not until last month that the agency approved another new oral anti-hair loss medication, the JAK inhibitor baricitinib. This also marks the FDA’s first approval of a systemic therapy for the treatment of alopecia areata.

In terms of efficacy, finasteride is an oral medication with an average onset of action of 3–6 months, and its effectiveness rate can reach 65%–90% after one year of treatment. Minoxidil is a topical solution with an average onset of action of 6–9 months, and its effectiveness rate can reach 50%–85%. Currently, the patents for both drugs have expired, and some generic manufacturers have begun to emerge.

In the domestic market, numerous companies are involved in the finasteride sector, including Merck & Co., Xianju Pharmaceutical, Conba, and China Resources Double-Crane.

The minoxidil market is primarily dominated by two companies: 3SBio and Zhendong Pharmaceutical, which hold approximately 70% and 20% of the market share, respectively. In this field, new innovative enterprises are also beginning to establish their presence. For instance, Hardcore Pharma, which secured lead investments from IDG Capital and Sequoia China last October, jointly established the Hardcore Pharma Research Institute with Fudan University and Sinopharm Group, launching a next-generation minoxidil enhancement combination product targeted at users suffering from hair loss.

However, both finasteride and minoxidil have certain limitations, creating an urgent market need for more innovative therapies and prompting capital to actively invest in companies developing such solutions.

For example, Tekeluo Bio, which secured tens of millions of RMB in Series A financing in April 2021, is developing TDM-105795, a “first-in-class” small-molecule candidate drug for the treatment of seborrheic alopecia. TDM-105795 is protected by global intellectual property rights.

Stemson Therapeutics, which secured $15 million in Series A financing from pharmaceutical giant AbbVie last July, is dedicated to treating hair loss by achieving hair follicle regeneration through induced pluripotent stem cell (iPSC) technology. Currently, the team is working on inducing the epithelial component of human iPSC-derived hair follicles, combining iPSC-induced human epithelial cells with dermal papilla mesenchymal cells, with the aim of generating complete human hair follicles.

Revela, which secured financing this year, aims to leverage AI technology to identify novel ingredients capable of addressing hair loss. It has recently discovered a new ingredient, ProCelinyl™, which accelerates the growth rate of dermal papilla cells by 50% per day and promotes the healthy growth of hair and hair follicles.

Notably, baricitinib, a JAK inhibitor approved by the FDA last month as a landmark development in the industry, is a novel therapy co-developed by Eli Lilly and Incyte. According to clinical trial results published in The New England Journal of Medicine, 40% of patients saw their hair loss decrease from an average of over 85% to below 20% by week 36 of treatment. In other words, nearly 40% of patients regained 80% of their hair after taking baricitinib. Of course, the subsequent performance of baricitinib remains to be tested by the market.

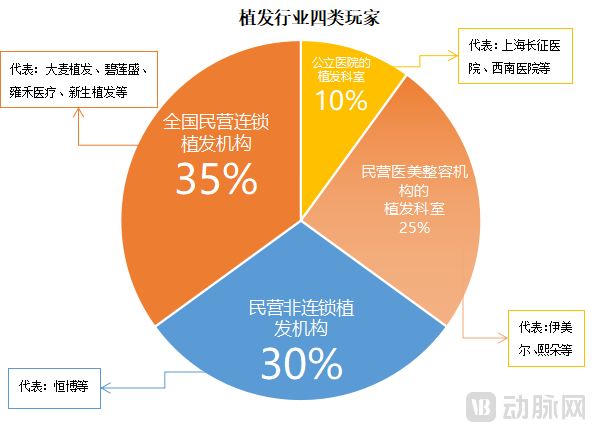

In the hair transplant sector, four types of participants have currently emerged in the industry.

Specifically, the first category includes hair transplant departments in public hospitals, such as Shanghai Changzheng Hospital and Southwest Hospital; the second comprises hair transplant departments in private medical aesthetic and plastic surgery institutions, represented by Yimeier and Xiduo; the third consists of non-chain private hair transplant institutions, exemplified by Hengbo; and the fourth encompasses nationwide chain private hair transplant institutions, including Barley Hair Transplant, Biliansheng, Yonghe Medical, and Xinsheng Hair Transplant.

According to previous research by VCBeat, large chain hair transplant institutions—including Barley Hair Transplant, Biliansheng, Yonghe Medical, and Xinsheng Hair Transplant—account for approximately 35% of China’s hair transplant market share, representing the primary force in the sector.

It is worth noting that China's hair transplant medical service market is subject to strict regulation, requiring every hair transplant service provider to obtain a valid medical license before commencing operations.

“Hair transplantation, as an important method for improving hair loss, offers good safety and high follicle survival rates, making it an increasingly popular choice among individuals experiencing hair loss.“The aforementioned investor stated.”

Taking Barley Hair Transplant as an example, its prospectus shows that the company's total revenue in 2019, 2020, and 2021 was RMB 747 million, RMB 764 million, and RMB 1.021 billion, respectively, showing a trend of continuous annual growth.

Additionally, the number of hair transplant patients at Barley Hair Transplant increased from approximately 23,800 at the end of 2019 to approximately 32,700 at the end of 2021. From 2019 to 2021, the average transaction value per paying patient for hair transplant services at Barley Hair Transplant was approximately RMB 30,000, RMB 25,800, and RMB 24,700, respectively.

However, behind the continuous growth in revenue, the hair transplant industry has also begun to fall into a situation of "increasing revenue without increasing profits."

The prospectus of Barley Hair Transplant Medical (Shenzhen) Group Co., Ltd. shows that its gross profit margins from 2019 to 2021 were 79.8%, 75.9%, and 70.9%, respectively, showing a year-on-year declining trend. In contrast, Yonghe Medical, which released its first annual report after listing in April this year, achieved a revenue of RMB 2.169 billion in 2021, a year-on-year increase of 32.4%. However, its net profit margin dropped significantly by 26.3% year-on-year, reaching RMB 118 million.

A key factor behind this is the high marketing expenses: Due to severe homogenization among hair transplant clinics, intensive advertising campaigns and progressive consumer inducement have become common marketing strategies to better acquire customers. According to the prospectus, Barley Hair Transplant Medical (Shenzhen) Group Co., Ltd.’s marketing and distribution expenses from 2019 to 2021 were RMB 500 million, RMB 399 million, and RMB 520 million, respectively, accounting for approximately half of its revenue.

How Should the Entire Industry Respond to Challenges? And How Will Future Trends Evolve?

#03

Continued “Baldness Breakthrough”: The Evolution of Three Major Trends in the Hair Loss Market

In the quest to break through in the RMB 100 billion hair loss market, three major trends have begun to emerge.

First, in the private hair transplant sector, the integrated model of "treatment, maintenance, and transplantation" is becoming mainstream.As a low-frequency service, hair transplantation requires continuous customer acquisition through marketing efforts, compelling hair transplant clinics to invest heavily in expanding their customer base. Consequently, how to re-engage and activate the existing customer base has become a critical issue for these clinics to address.

Currently, leading hair transplant chains are increasingly attempting to drive consumer spending and expand their overall profitability by diversifying into ancillary services.

Second, technological innovation must be prioritized in both pharmaceutical treatments and hair transplantation.An analysis of the current financial data from hair transplant institutions reveals that R&D expenditures account for only 1%–3% of revenue, a disproportionately low share that has led these service providers to become overly reliant on marketing. Furthermore, against the backdrop of a rapidly growing population suffering from hair loss, the currently available anti-hair-loss medications remain limited, underscoring an urgent need for more innovative drugs and therapies.

Third, the global market is rising rapidly, making international expansion a new option.High prevalence of hair loss and strong purchasing power overseas have driven rapid growth in the volume of hair transplant procedures. Compared with China, people in Europe and the United States tend to experience onset of hair loss at a younger age, and the prevalence of hair loss across all age groups is significantly higher than among Asians. The substantial overseas demand for hair loss treatment, coupled with strong ability to pay, has propelled the volume of hair transplant surgeries abroad into a period of rapid growth in recent years.

According to data from the International Society of Hair Restoration Surgery, the volume of hair transplant procedures in North America, South America, Europe, and Africa grew significantly between 2012 and 2019, with compound annual growth rates (CAGR) of 9.1%, 21.6%, 10.2%, and 27.1%, respectively, indicating promising market prospects for the overseas hair loss treatment industry.

Amid this evolving trend, the hair loss market is poised to remain in a growth phase. It is crucial, however, that the industry steers toward more positive development, continuously delivering superior hair regrowth experiences and outcomes for patients.

After all, for the vast majority of people, regaining thick hair is a “top priority” concerning both health and appearance.