Medical Sector IPO Surge Ignites Market Enthusiasm

BeBetter Med

Innovative Drug Developer

IMEIK

Developer of Biomedical Soft Tissue Repair Materials

GENRIX BIO

Developer of Novel Monoclonal Antibody Drugs

“Revenge” IPOs Are Kicking Off.

During the week of June 27 to July 3, a record-breaking 126 companies had their applications accepted for listing on the STAR Market and the ChiNext Board, with five companies successfully passing the review meetings:The recent surge in IPOs has sent a positive signal to the secondary market, which had been sluggish for some time.

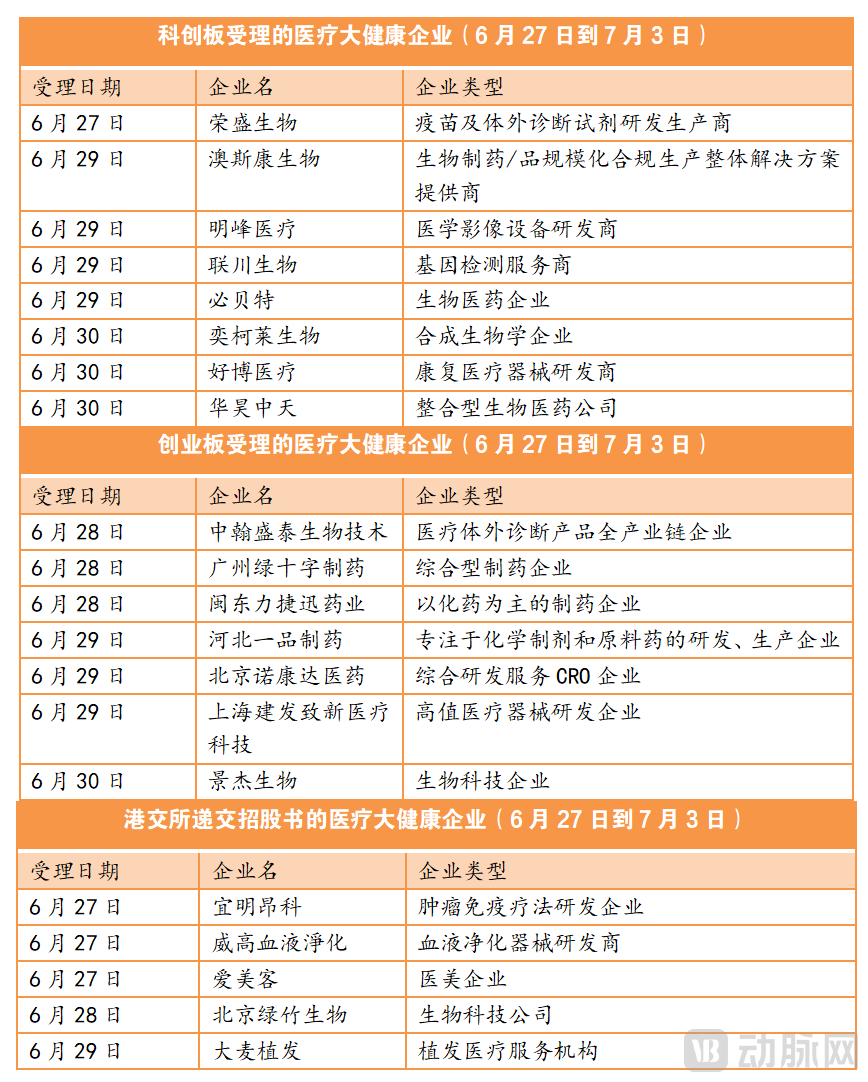

VCBeat has found that a total of 15 healthcare companies were accepted by the STAR Market and ChiNext this week, reaching a historical high. On the Hong Kong Stock Exchange side, five healthcare companies also submitted their prospectuses.

It is worth noting that from January to May this year, the STAR Market accepted only one medical and healthcare company for listing—Genetron Health. However, in June alone, it accepted 14 companies, eight of which were processed last week. This clearly indicates that the IPO processes of medical and healthcare enterprises have entered a phase of collective acceleration.

In addition to the secondary market warming up, the primary market is also heating up.On June 29, following the release of a notice on the official website of the Ministry of Industry and Information Technology to remove the “asterisk” marker from the Communication Itinerary Card, the VC/PE community instantly erupted. Li Linlin (a pseudonym), a frontline investor based in Shanghai, couldn’t help but joke with VCBeat, “In the second half of the year, we will engage in rebound project sourcing, rebound due diligence, and rebound capital deployment.”

Undoubtedly, market enthusiasm for the healthcare and wellness industry is being reignited.

Every day, healthcare companies are rushing to go public.

Considerations Behind the June IPO Surge

Data never lies.

Throughout June, IPOs in the healthcare and wellness sector are showing signs of recovery.According to statistics from VCBeat, the number of companies that have had their IPO applications accepted or have submitted prospectuses on the ChiNext Board, the STAR Market, and the Hong Kong Stock Exchange reached 29, exceeding half of the total for the previous five months combined, with an average of one healthcare and wellness company rushing to go public each day.

In terms of distribution across various sub-sectors, 24 biopharmaceutical companies, four medical device companies, and only one healthcare service company are sprinting toward an IPO in June.

Among these companies are “heavyweight players” such as GENRIX BIO, BeBetter Med, and Imeik, with valuations reaching tens of billions, or even hundreds of billions, of yuan.: In terms of fundraising scale, GENRIX BIO plans to raise RMB 3.98 billion, exceeding 3.97 times its total assets; BeBetter Med plans to raise RMB 2 billion; the fundraising amount for Imeik has not yet been determined, but when it listed on the A-share market, it originally planned to raise RMB 1.935 billion and ultimately raised RMB 3.435 billion, representing an oversubscription of 78%.

“Confidence in the industry has returned overnight.” Li Mingzhe (a pseudonym), a healthcare investor, told VCBeat that his firm is currently actively pushing its portfolio companies to accelerate their IPO bids. “Now is a favorable timing; we must seize this window of opportunity.”

In Li Mingzhe’s view,There are three reasons for the current surge in IPO activity.

First, after experiencing a downturn, market confidence is being rebuilt as a series of positive developments are released. In the second half of 2021, the rate of A-share listed pharmaceutical companies breaking their IPO issue price within the first month of trading was excessively high. Coupled with the recurrent COVID-19 outbreaks in the first half of this year, many companies lacked confidence and consequently postponed their initial public offerings (IPOs) in the first half of 2022.

“Last year, pharmaceutical companies frequently saw their IPOs break the issue price, so we advised our portfolio companies to adopt a wait-and-see approach, even if they had already passed the stock exchange’s listing hearing,” said Li Mingzhe, a healthcare industry investor.Valuation inversion affects not only investment returns but also a company’s financing capacity and market recognition.“If a pharmaceutical company’s market capitalization drops to half its IPO value just three months after listing, how will the market perceive its worth? Skepticism would undoubtedly be rampant, causing significant and unnecessary distress for R&D-driven enterprises.”

Second, since the STAR Market raised its listing requirements for pharmaceutical companies, the threshold for initial public offerings (IPOs) has been rising steadily.

Third, R&D-focused biopharmaceutical companies are in urgent need of cash flow. After a six-month hiatus in their IPO processes, R&D-driven biopharmaceutical enterprises generally have no revenue or only minimal revenue, operating at a loss. Their on-hand cash reserves can typically sustain operations for only six to nine months. Taking BeBetter Med as an example, its prospectus disclosed that its net losses after deducting non-recurring items amounted to RMB 30.64 million, RMB 64.89 million, and RMB 145 million in 2019, 2020, and 2021, respectively. Consequently, the company requires continuous financing to advance its R&D and clinical progress.

Furthermore, as we move into July, companies listed on the Hong Kong or A-share markets are required to disclose their financial reports for the corresponding period, which entails including financial data for the first half of the current year. In contrast, in June, financial data need only be reported up to December 31, 2021. Therefore, the surge in pharmaceutical companies submitting IPO prospectuses is also driven by the desire to remain within the validity period of their financial statements, thereby saving time and effort.

It is evident that, under the influence of a series of factors, the pharmaceutical industry is showing signs of emerging from its winter slump. Moreover, the market sentiment in the secondary market often affects the investment climate in the primary market.

In response to this situation, VC/PE firms have also begun engaging in retaliatory business travel.

VC/PE firms begin to review deals with a vengeance,

Whoever stops will be eliminated by the market.

Affected by the recurring COVID-19 outbreaks in the first half of the year, venture capital (VC) and private equity (PE) firms in Beijing and Shanghai found it difficult to conduct offline project sourcing and due diligence. With the removal of the “asterisk” marker from the Communication Itinerary Card, the prolonged period of remote work has officially come to an end.

“The first half of the year was consumed by various online meetings, while the second half involved flying across China for a frenzy of project evaluations.“Investor Li Linlin told VCBeat that with the resumption of free movement, investment processes such as market research, due diligence on projects, and reporting for decision-making will continue to operate, and may even be busier than last year. ‘Whoever stops will be eliminated by the market. Although many projects have been followed up online, offline visits and discussions are still necessary.’”

For VC/PE firms, investment decisions hinge not only on the sector but also significantly on the people involved. Therefore, building stronger relationships and gaining deeper insights into founding teams requires repeated offline interactions and engagements.

Of course, in Li Linlin’s view,Beyond deepening our understanding of potential projects, the more pressing need behind staying busy is to keep abreast of the latest developments in specific niche sectors.“Taking the consumer healthcare sector, which I closely monitor, as an example, although our firm primarily invests in upstream technologies and materials, it is still essential to gain a clear understanding of the evolving demands of downstream institutions and consumers. These changes will, to some extent, influence market expansion and business decisions for upstream projects in the near term, thereby affecting corporate valuations.”

Additionally,For VC/PE firms, another more critical task offline is fundraising.In the investment community, as the capital providers for venture capital (VC) and private equity (PE) firms, limited partners (LPs) also need to stay informed about recent developments within these firms. Moreover, when it comes to confidential financial audit reports, offline review is often a more secure approach.

“Of course, another important thing is to offer mutual encouragement,” Li Linlin said with a smile. There are stories to share, whether for VC/PE firms or healthcare and wellness enterprises.

After all, VC/PE firms undoubtedly faced significant challenges in the first half of the year. According to a data report from Zero2IPO Research, the pace of listings for Chinese enterprises both domestically and overseas slowed in the first quarter of this year due to the international situation. The stock prices of listed Chinese concept shares suffered setbacks, the progress of companies planning to list in the U.S. was delayed, and the overseas listing performance of Chinese enterprises hit a historical low. The return multiples for VC/PE-backed Chinese enterprises listing overseas dropped to their lowest point in nearly a decade.

Medical and healthcare enterprises have also encountered numerous setbacks. Taking Shanghai as an example, under the impact of the pandemic in the first half of the year, many medical and healthcare companies experienced months of work and production stoppages, and their market activities were significantly affected.

“Reuniting with old friends can shift everyone’s mindset,” said Li Linlin.

It is not difficult to find that,After months of working from home, VC/PE firms will accelerate their pace in the second half of the year to make up for their absence in the first half, thereby driving a resurgence in heat in the primary market of the healthcare and wellness industry.

Three Major Sub-Sectors to Draw Attention,

Roll Up Your Sleeves and Go All Out in the Second Half of the Year

Following the rebound in both primary and secondary markets, the entire healthcare and wellness industry has also felt the “warmth” of summer.

The founder of a late-stage dental health company told VCBeat that he had received invitations from two mainstream venture capital firms in the past two days for initial discussions and due diligence. “We planned to launch a new round of financing at the end of last year, but due to special circumstances in the first half of this year, we postponed it until now. This is also a good time for fundraising.”

Beyond financing, market expansion is also a top priority in the company’s plan for the second half of the year.“We will consider market expansion, such as cross-regional mergers and acquisitions, with a focus on South China, including Shenzhen and Guangzhou. This is because South China was not significantly affected by the pandemic, so multi-location operations can help diversify risks,” said the founder of a Shanghai-based chain medical service provider. He added that as confidence recovers, the company aims to fully offset the losses incurred in the first half of the year.

In addition to the proactive strategic positioning by enterprises,Which niche sectors will investment firms focus on in the second half of the year?According to VCBeat’s multi-faceted research, venture capital (VC) and private equity (PE) firms have reached a broad consensus on the following three key subsectors within healthcare.

First, frontier biotechnology sectors such as synthetic biology, cell therapy, gene therapy, and nucleic acid drugs.This is because frontier technologies, once their path to industrialization is proven, often possess tremendous market explosive potential and can deliver high returns. However, they also carry greater investment risks, posing a stricter test on the professional expertise and risk appetite of investment institutions.

Moreover, policy support has served as a key catalyst driving the surge of frontier technologies in the capital markets. In November 2021, the Beijing Municipal Committee of the Communist Party of China and the Beijing Municipal People’s Government issued the “Beijing Plan for Building an International Science and Technology Innovation Center during the 14th Five-Year Plan Period,” which aims to promote research and development of cutting-edge biotechnologies in key areas such as novel antibody technologies, gene editing, novel cell therapies, and stem cells and regenerative medicine.

Taking synthetic biology as an example, one of its significant contributions is providing technological innovation solutions under the overarching goal of carbon neutrality. Furthermore, by efficiently engineering cellular pathways, synthetic biology holds broad application prospects in new drug development, cell engineering, and high-end biomanufacturing.

In the field of gene therapy, the evolving trend is a gradual shift from rare diseases to common diseases. This is because, as gene therapy technology matures—particularly with advancements in vector technology—breakthroughs are being made in addressing tissue and organ targeting during delivery, as well as improving vector safety. Subsequently, as treatment costs decrease, more patients will benefit, leading to a larger market.

Second, in the field of innovative medical devices, the cardiovascular sector remains a key focus, while aesthetic medicine and ophthalmology, with their consumer-oriented attributes, will continue to be favored.In detail, within the cardiovascular sector, new technologies and products such as ventricular assist devices (VADs), pulsed field ablation (PFA), and intravascular lithotripsy balloons will continue to attract attention in the primary market, while enthusiasm in the medical aesthetics industry will concentrate on upstream technologies and materials.

A senior investor in the medical aesthetics industry previously told VCBeat that collagen and botulinum toxin will be the next investment hotspots in the sector. Advances in collagen technology are driving injectable fillers into a new era of regenerative medicine. As an irreplaceable product category, botulinum toxin remains a strong investment opportunity, particularly for newly approved products and novel bioengineered botulinum toxins.

Turning to ophthalmology, the sector’s momentum stems not only from technological advancements but, more importantly, from policy support. Early this year, China’s 14th Five-Year Plan for National Eye Health emphasized the need for early detection and treatment of eye diseases, focusing on myopia in adolescents, cataracts in the elderly, and other ocular conditions affecting younger populations. Notably, the ophthalmology sector comprises numerous subsegments, including optical coherence tomography (OCT) devices and orthokeratology lenses, all of which present significant opportunities.

Third, in the field of digital health, digital therapeutics and insurtech will become hotspots.The surge in interest in digital therapeutics (DTx) is driven, on one hand, by the continued promotion from regulatory bodies such as the U.S. Food and Drug Administration (FDA), and on the other, by DTx’s significant potential to improve healthcare accessibility.

Despite the numerous challenges faced by some insurtech companies in the first half of the year, many investors have stated that insurtech will remain a key focus in the second half, given its significance to payers in the healthcare and wellness industry. Straddling both the insurance and healthcare sectors, insurtech has assumed a leading position in the market. Data from the China Banking and Insurance Regulatory Commission (CBIRC) shows that the health insurance segment within insurtech achieved an annualized growth rate of 31.4% over the past five years, with its market size doubling. The continuously expanding market offers greater potential for growth, thereby driving sustained financing for insurtech enterprises.

“With the recovery of primary and secondary markets, the easing impact of the international external environment, and effective pandemic control, financing, investment activities, and IPOs in the pharmaceutical industry will become more frequent in the second half of the year. Barring any unexpected developments, the entire industry is sure to usher in a period of significant dividends,” said Li Mingzhe, an investor in the pharmaceutical industry.

When VCBeat asked what further preparations were needed, Li Mingzhe replied:

“Don’t overthink it—roll up your sleeves and go all out!”