Another Ophthalmic Chain Lists on China's A-Share Market: Is the Sector Entering an Era of Intensified Competition?

Bright Eye

Professional Ophthalmology Chain Medical Institution

Today, the booming “golden ophthalmology” sector welcomed another listed company as Bright Eye made its IPO on the ChiNext board.

Recently, healthcare IPOs have accelerated, with companies intensively submitting listing applications. Yesterday, VCBeat specifically published in “IPO Boom: The Healthcare Industry Is Buzzing” article. Coincidentally, several other companies have also successfully listed on the secondary market in recent days. Healthcare remains a sector highly favored by the capital markets.

In the ophthalmology sector specifically, chain operators are currently experiencing a wave of initial public offerings (IPOs). Prior to 2022, only Aier Eye Hospital, the industry leader, and Guangzheng Eye Hospital, which transitioned from manufacturing to healthcare, were listed on China’s A-share market. In March 2022, He Eye Hospital listed on the ChiNext board. Huaxia Eye Hospital is also currently in the queue awaiting its IPO. Coupled with Chaoju Eye Care, which went public on the Hong Kong Stock Exchange in 2021, and previously established players such as C-MER Eye Care, the secondary market for ophthalmology chains is becoming increasingly vibrant.

Multiple companies have gone public, securing more ample capital for business expansion. Does this also signal that the ophthalmology chain sector is beginning to experience cutthroat competition?

Overall, the “one superpower, multiple strong players” landscape in the chain ophthalmology market is becoming increasingly pronounced.

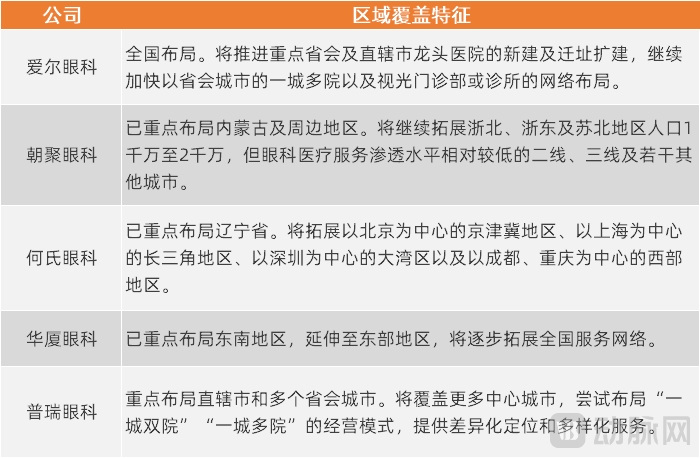

“The Leading Player”: Aier Eye Hospital has established a nationwide presence. By the end of 2021, Aier Eye Hospital (within its listed company system) operated 174 hospitals and 118 outpatient clinics across China. It has built a horizontal, tiered diagnosis and treatment network within the same cities, featuring multiple hospitals in provincial capital cities, optometry outpatient clinics (or practices), and “Ai Yan e-Stations.” This strategy has created a layout characterized by “horizontal clustering and vertical networking” in multiple provinces and regions.

“Multiple Strong Players”: Most ophthalmic chain institutions exhibit distinct regional distribution characteristics.

For example, Chaoju Eye Care is concentrated in Inner Mongolia and surrounding areas, with its business expansion primarily focused on northern Zhejiang, eastern Zhejiang, and northern Jiangsu. He Eye Hospital’s main operations are distributed across Liaoning Province, with key expansion regions including the Beijing-Tianjin-Hebei area centered on Beijing, the Yangtze River Delta region centered on Shanghai, the Greater Bay Area centered on Shenzhen, and the western region centered on Chengdu and Chongqing. Huaxia Eye Hospital’s strongholds are in southeastern provinces, while its expansion efforts are mainly directed toward eastern China.

In contrast, Bright Eye is an exception.

Bright Eye originated in Southwest China, primarily establishing its hospital network in key cities such as municipalities directly under the Central Government and provincial capitals, thereby extending its reach to surrounding areas. By the end of 2021, it had opened 23 ophthalmic hospitals and 3 ophthalmic outpatient clinics across China, distributed in nearly 20 provincial capitals and municipalities directly under the Central Government.

Key Geographic Footprints of Major Ophthalmic Chain Groups, Source: Company Prospectuses or Latest Annual Reports

The advantage of a regionally concentrated layout lies in its ability to build reputation through long-term service to patients in specific areas. Establishing multiple medical institutions within a region enables maximum market penetration, and if these institutions offer differentiated services, they can also facilitate mutual patient referrals. However, when operations are concentrated in one or a few regions, business performance is subject to objective factors such as local economic development, consumption levels, and policy changes. Overreliance on revenue from a single location can also become a constraint on corporate growth.

Correspondingly, a nationwide presence allows for the formulation of tailored business strategies based on local conditions, thereby achieving risk diversification where weaknesses in one region can be offset by strengths in another. Meanwhile, the brand influence of a national footprint exceeds that of a regional one. However, cross-regional expansion entails adapting to diverse market environments, which consequently leads to higher market costs.

Regarding the aforementioned ophthalmic chains, Aier Eye Hospital’s leading position remains unshakable. Its expansion model, driven by off-balance-sheet M&A funds, has entered a virtuous cycle, with both revenue and profits demonstrating stable growth. While the other companies also reported respectable overall revenue growth, their profitability varied significantly: Bright Eye’s net profit margin lagged behind its peers.

According to the prospectus, from 2019 to 2021, Bright Eye’s gross profit margin on its core business was 42.69%, 43.28%, and 43.37%, respectively, while its net profit margin was 4.11%, 8.00%, and 5.49%, respectively. The gross profit margin on its core business was comparable to that of other listed companies, whereas its net profit margin was lower than that of comparable listed companies. It is understood that the net profit margins of several other listed companies were approximately 10%–15%.

Regarding the aforementioned gaps, at least two reasons can be found in Bright Eye’s prospectus:

First, newly established or acquired hospitals require a growth ramp-up period. For instance, hospitals such as Lanzhou Ophthalmology & Optometry, Xi’an Bright Eye, Guizhou Bright Eye, Shenyang Bright Eye, Shandong Liangkang, and Tianjin Bright Eye need time to achieve revenue growth, resulting in generally lower net profit margins that drag down the Group’s overall net profit margin.

Second, advertising and promotional expenses are relatively high. Bright Eye noted that the company adopts a nationwide layout strategy focused on provincial capital cities, resulting in a relatively dispersed regional presence. Consequently, corresponding promotional activities are required in each operational region to enhance brand penetration. Compared with the strongholds of Aier Eye Hospital, Huaxia Eye Hospital, and He’s Eye Hospital, Bright Eye’s brand influence in local markets lags behind, necessitating greater resource investment in marketing and promotion.

It is evident that expansion requires a growth cycle. When expanding across regions, greater investment in brand-building costs is necessary to enhance local influence and thereby shorten the growth cycle, resulting in higher overall costs.

Thus, from the perspective of expansion paths, a regionally concentrated layout does not yet face “involution”; however, attempting to achieve widespread nationwide coverage in the short term would mean competing not only with the national leader, Aier Eye Hospital, but also with regional leaders, making “involution” unavoidable.

Cataract surgery, refractive surgery, and optometric services are the three pillars of private ophthalmic hospitals. Among these, cataract surgery, which is covered by medical insurance, has played a key role in the rapid development of private ophthalmic hospitals. However, over the past two years, as cost-containment measures under medical insurance have become increasingly stringent, hospitals have been gradually reducing the proportion of services reimbursed by medical insurance. Although the cataract surgery sector is not characterized by intense cutthroat competition, its share of revenue across institutions has declined significantly due to payment-side pressures; for instance, Aier Eye Hospital’s revenue from cataract procedures has dropped to approximately 15%.

Refractive surgery and optometric services are both highly consumer-driven offerings. Refractive surgery targets adults, with a focus on vision correction, while optometric services cater to a broader population, encompassing not only vision correction but also the currently prominent field of myopia prevention and control in adolescents.

Currently, while ophthalmology chains emphasize consumer-oriented services, they are placing particular focus on optometry services. In recent years, demand has continued to rise for myopia prevention and control among adolescents, postoperative eyeglass dispensing following ocular surgeries, and vision rehabilitation. The service sector has responded accordingly. At present, major players such as Aier Eye Hospital, Chaoju Eye Care, and He’s Eye Hospital have established numerous independent optometry clinics, strategically located in close proximity to residential communities. Notably, He’s Eye Hospital operates as many as 55 primary eye care institutions, which are positioned for the prevention and rehabilitation of eye diseases, with optometry services as their core business. As their operational scale expands, profitability is improving year by year.

On one hand, optometry clinics can provide optometric services, screening and diagnosis of basic eye diseases, etc., thereby generating corresponding revenue. Moreover, optometric services themselves boast relatively high gross profit margins. Data from multiple medical institutions indicate that the gross profit margin for optometric services is generally above 55%.

On the other hand, optometry clinics require relatively low investment, can be widely distributed, and offer operational flexibility. They help expand the service radius of tertiary hospitals and serve as a patient source by referring screened, eligible patients to these higher-level institutions. Meanwhile, compared with commercial optometry, medical optometry possesses stronger competitiveness due to its inherent medical attributes.

Of course, setting up optometry clinics within hospitals has also become a standard practice.

Benefiting from their strategic layouts in the optometry sector, an analysis of the revenue structures of various chain hospitals reveals that the proportion of revenue from consumer-oriented services, particularly optometry services, is growing rapidly. Notably, Aier Eye Hospital’s share of revenue from optometry services has increased from approximately 15% to over 20%, while He氏 Eye Hospital’s optometry service revenue now accounts for more than 30%, surpassing the proportions contributed by refractive surgery and cataract services.

In January 2022, the National Health Commission issued the “14th Five-Year Plan for National Eye Health (2021–2025).” The targets to be achieved by 2025 include: achieving an annual coverage rate of over 90% for eye care and vision screening among children aged 0–6 years; continuously improving the overall level of eye health among children and adolescents; steadily increasing the effective coverage rate of refractive error correction; and gradually reducing the number of individuals with visual impairment caused by high myopia.

“The Plan” has once again made myopia prevention and control a focal point. For children and adolescents who are already myopic, it is essential to emphasize the implementation of scientific optometric examinations. Furthermore, efforts should be made to enhance early diagnosis and prevention capabilities, strengthen evidence-based correction measures, and thereby slow the progression of myopia.

Meanwhile, myopia prevention and control is not merely a top-down national strategy, but a massive undertaking requiring participation from all sectors of society. As the end consumers, parents—who constitute the primary demand side—are demonstrating growing awareness of myopia prevention and control, along with an increasing willingness and ability to pay for related services.

Currently, there is a diverse array of myopia control strategies available, including medical devices and pharmaceuticals such as orthokeratology lenses and low-concentration atropine, as well as digital therapeutics with strong innovative momentum, to meet the varying needs for myopia prevention and control.

Myopia prevention and control has even become a niche sector favored by capital. Recently, Future Vision, a pediatric ophthalmology chain, just secured Series B financing. Its core business includes myopia prevention and control for children and adolescents, correction of refractive errors (myopia, hyperopia, astigmatism), and amblyopia training.

It is evident that optometry services, represented by myopia prevention and control, are not subject to “involution”; on the contrary, they hold immense potential and constitute a blue ocean market.

Private hospitals must prioritize brand building in their patient acquisition strategies. In the short term, advertising and promotion serve as one approach to brand building; in the long term, strengthening internal capabilities, enhancing clinical diagnostic and treatment expertise, and earning stronger patient word-of-mouth constitute another vital approach.

In terms of short-term investment, as mentioned earlier, Bright Eye incurs high advertising and promotion expenses. To compete with public ophthalmic medical institutions and other private ophthalmic medical institutions, it needs to continuously invest in advertising and promotion. From 2019 to 2021, these expenses reached RMB 134 million, RMB 139 million, and RMB 179 million respectively, accounting for 11.27%, 10.24%, and 10.49% of its main business revenue.

According to the China Health and Health Statistical Yearbook, the number of non-public ophthalmic hospitals in China increased from 485 in 2016 to 1,005 in 2020. It is a fact that the industry has seen an increase in participants, rapid growth in service supply, and intensified competition. In reality, promotional efforts by various institutions through online and offline media do significantly influence consumer decisions. However, has competition become so “involutary” that it now requires more than 10% of operating revenue to be spent on promotion and advertising?

Looking at the advertising and promotional expenses of other institutions: Aier Eye Hospital, Huaxia Eye Hospital, and He Shi Eye Hospital have advertising and promotional expense ratios of only around 3%-5%, with an average of about 4%.

In light of this, Bright Eye has also provided the aforementioned explanation regarding its substantial advertising expenditures, attributing them to the need for significant investment in a decentralized regional layout and enhanced brand penetration.

In terms of long-term brand building, companies need to earn better patient reputation by enhancing their diagnostic and treatment capabilities. The R&D investment of each company can, to some extent, reflect the emphasis placed on improving these capabilities.

Data shows that Huaxia Eye Hospital and He’s Eye Hospital each invest millions to tens of millions of yuan annually in R&D, accounting for less than 1% of their operating revenue. Bright Eye Hospital Group has left its R&D investment column blank for the past three years, although it has established three research institutions under its umbrella. Aier Eye Hospital allocates the highest amount and proportion of funds to R&D, with annual investments exceeding 100 million yuan over the past three years, representing approximately 1.5% of its operating revenue.

R&D investment does not yield immediate results and requires sustained commitment over many years; however, the core competitiveness built through such efforts is more robust. The R&D spending ratios of several companies also seem to reflect the reality that “even the most talented individuals remain highly diligent.”

Overall, in terms of brand influence, advertising investment can serve as the most direct means of business penetration, but it should not become a channel for involutionary customer acquisition; enhancing diagnostic and treatment technical capabilities is the fundamental way to build brand influence.

As the “windows to the soul,” visual needs are ever-present. However, against the backdrop of a systemic shift in the healthcare service model from disease treatment to health promotion, public demand for eye care has increasingly focused on extending from therapeutic interventions to preventive care and rehabilitation.

For common diseases, although the emphasis on prevention and rehabilitation has been advocated for many years, public attention to preventive and rehabilitative measures remains low in the absence of symptomatic manifestations. Consequently, health management services centered on prevention have yet to establish sustainable business models. In contrast, eye health services are closely tied to visual quality and directly impact various aspects of daily life. Therefore, the extension of ophthalmic care from treatment toward prevention and rehabilitation represents a more pressing and essential need compared to that for general diseases.

In this context, although several ophthalmology chains have entered the harvest phase of their business operations and listed on secondary markets, industry-wide “involution” has not fully materialized; rather, it is confined to specific dimensions of direct competition. Looking ahead, the ophthalmic medical services market will remain highly accommodating to sufficiently outstanding participants.