Early-Stage Healthcare Investment Defies Market Winter: 121 Deals and Nearly RMB 10 Billion Raised in H1 2022

In the first half of 2022, amid the pandemic’s impact, a recurring sentiment emerged within the healthcare industry to the effect that “the sector is in decline.” This pessimism also spread to the early-stage healthcare market, which has attracted significant attention in recent years. Many industry insiders viewed the current fervor surrounding this market as mere castles in the air, lacking tangible practical value.

Is this really the case? It seems not.

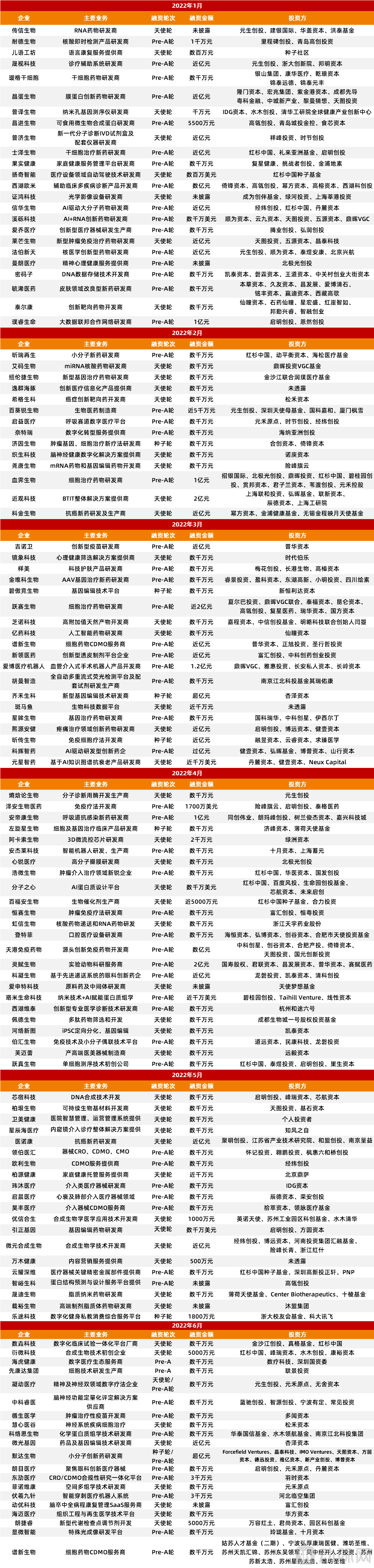

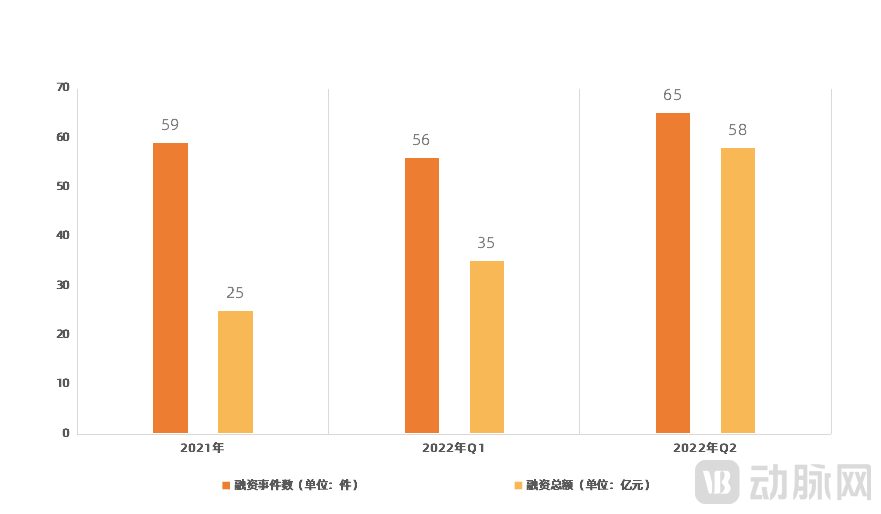

According to statistics from VCBeat’s Orange Fruit Bureau, a total of 121 early-stage investment and financing transactions occurred in China’s healthcare sector in the first half of 2022, with total funding amounting to nearly RMB 10 billion.

Figure 1. Early-stage financing data in the healthcare sector

If this still does not provide an intuitive sense, we can make a year-over-year comparison with the data from 2021. According to statistics, there were 59 early-stage investment and financing transactions in China’s healthcare sector in 2021, with a total funding amount of RMB 2.5 billion. This means that in the first half of 2022 alone, China’s early-stage healthcare market had already surpassed the full-year figures of the previous year.

When our understanding of the hype surrounding an emerging industry remains vague, data always provides a clearer perspective, helping us clarify the underlying logic behind its rise and determine its future trajectory. So, what story did the early-stage healthcare market tell in the first half of the year? VCBeat’s Orange Data Bureau will unfold the answer through a series of data points.

01. Who Is Starting a Business?

According to statistics, among the 121 companies that completed early-stage financing in the first half of this year, 85% had been established for less than two years, indicating that a wave of emerging entrepreneurs is accelerating their entry into the healthcare sector.

So, who exactly are they? The vast majority are scientists.

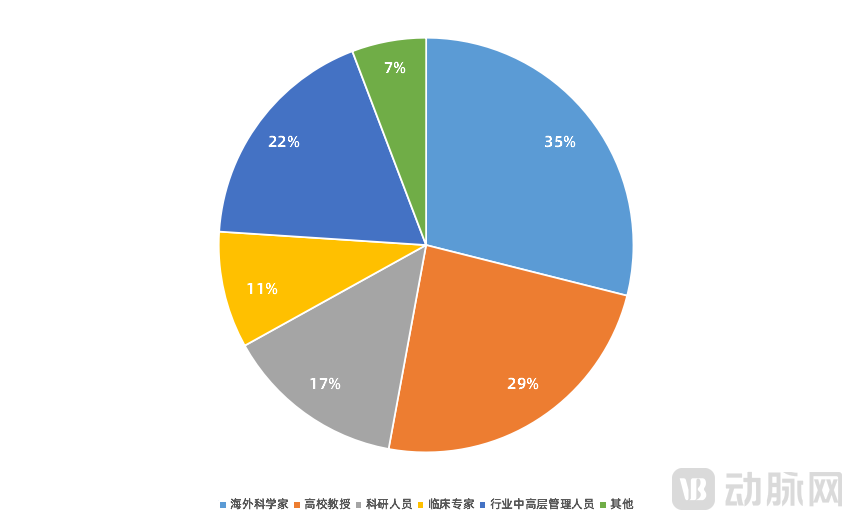

Figure 2. Profile of Founders in Early-Stage Healthcare Startups

According to statistics, among the 121 startups that completed early-stage financing in the first half of this year, 76% of the founders have a scientific background, while the remaining 23% are primarily mid-to-senior level managers from listed companies or leading healthcare enterprises who have left to start their own ventures.

A closer look at the profiles of these scientist entrepreneurs reveals that 29% are returnees who studied abroad. For instance, Lemang Biotech, which secured nearly RMB 100 million in angel financing this January, was founded by a team all hailing from the École Polytechnique Fédérale de Lausanne (EPFL), a world-leading institution in science and technology.

The remaining 71% of scientists come from domestic universities, medical centers, and research institutions. Among these, universities account for the largest share at 24%, followed by research institutions at 14%, while medical centers represent a smaller proportion at 9%.

From this series of data, we can observe two core trends in the early-stage healthcare market: first, scientists are increasingly venturing into entrepreneurship; second, a significant proportion of startups are founded by overseas-returnee scientists and university professors. There are, of course, underlying reasons for these trends.

Let’s begin with the broader trend of scientists launching startups. In recent years, under the direct pressure of “performance evaluations,” research institutions and scientists themselves have become more focused than ever on translating research findings into practical applications. As a result, a growing number of scientists have gone with the times, moving from the laboratory to the entrepreneurial arena. This is the apparent reason.

Another aspect lies beneath the surface: the development trajectory of the healthcare industry. Currently, the sector is increasingly extending into high-tech domains, which means that only innovative projects with genuine original technologies and substantial market potential are more likely to stand out in the early-stage market. This trend demands that today’s startups possess greater “hard” capabilities than in the past, thereby raising the bar for founders.

However, it is inherently challenging for scientists to launch startups. Even with an impressive personal résumé and profound expertise in scientific research, translating a laboratory breakthrough into a market-ready product involves multiple complex stages, each of which filters out a number of scientist-entrepreneurs.

“Elimination” is determined by three key factors: first, scientific research outcomes—specifically, whether the technology possesses original innovativeness and whether the market potential is sufficiently large; second, the scientist—whether they exhibit entrepreneurial traits and possess relevant industry insights and market resources; third, the scientist’s affiliated research institution—a reputable organization with a comprehensive incubation system and market resources can often provide unexpected support to scientist-entrepreneurs in the early stages.

Having delineated the founder profile, we now address why returned overseas scientists and university professors constitute a significant proportion. This is closely tied to the three determinants mentioned above.

Let’s start with the overseas perspective. Taking the United States as an example, it began exploring the architecture and models of the medical innovation and translation ecosystem earlier than China, and has now established a relatively complete and systematic framework for translating scientific achievements into practical applications. Scientists nurtured in such an environment tend to possess strong overall competencies, which often leads to higher success rates in their entrepreneurial ventures. This constitutes an intrinsic individual factor.

There are also external environmental factors. In recent years, the exclusion of Chinese scientists by the U.S. academic community has intensified, making it more likely for them to encounter obstacles when applying for research funding and seeking approval for scientific projects. Meanwhile, China has extended olive branches to these scientists, offering substantial support through policy guidance, financial assistance, and resource connectivity. This combination of push and pull factors has naturally attracted many scientists to return to China to start businesses.

Shifting our focus to China. Compared with clinical-centric medical centers and research-led scientific institutions, universities possess greater market-oriented core competencies; consequently, their incubation benefits derived from early-stage projects are more pronounced in terms of tangible outputs.

02. What to Do When Starting a Business?

Having addressed the question of who is starting businesses, it is time to explore “what they are doing in their ventures.”

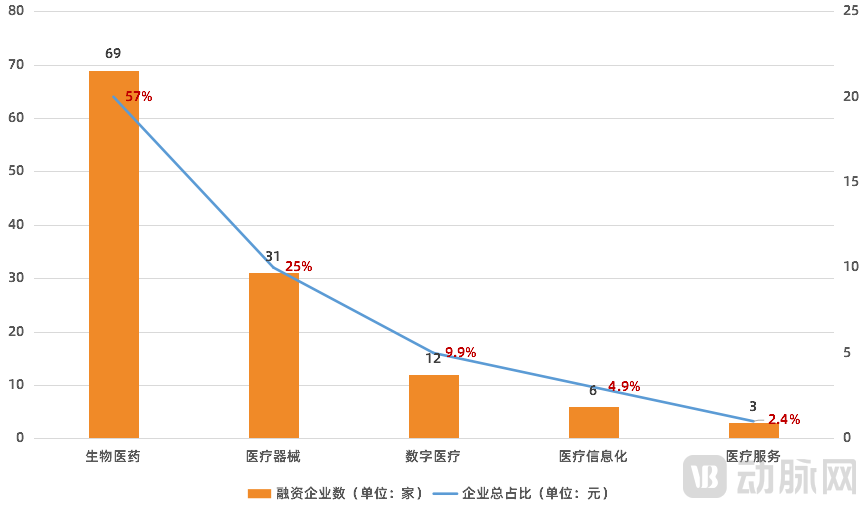

Figure 3. Breakdown of Early-Stage Financing in the Healthcare Sector

Let’s start with the big picture. According to statistics, among the 121 companies that completed early-stage financing in the first half of this year, exactly 100 were “hard tech” companies, accounting for 82.6% of the total. Of these, 69 were biopharmaceutical companies, representing 57% of the total, and 31 were medical device companies, accounting for 25.6%.

There are compelling reasons why startups are increasingly emphasizing hard-tech attributes. China’s healthcare sector has moved beyond the entrepreneurial era dominated by “domestic substitution” under traditional business models; the low-hanging fruit has largely been picked. Future opportunities will undoubtedly favor innovative enterprises that possess genuine, original technologies and effectively meet clinical needs.

Next, let us examine the specific sub-sectors. According to statistics, among the 121 companies that completed early-stage financing in the first half of this year, synthetic biology, brain science, and ophthalmology emerged as focal areas, accounting for a total of 31 companies, or 25% of the total. Among these, synthetic biology was the “biggest winner,” with 14 startups.

Take Weiyuan Synthetic Biology, which completed a nearly RMB 100 million angel financing round in May this year, as an example. This is a biomanufacturing company based on synthetic biology technology, committed to producing various compounds using low-carbon, energy-saving, and sustainable methods for applications in pharmaceuticals, daily chemicals, agriculture, food, feed, and materials.

In fact, emerging fields such as synthetic biology and brain science are currently attracting significant market attention, making the clustering of startups an inevitable outcome. On one hand, these emerging sectors are in their early stages, with a substantial volume of scientific research achievements being generated during this period. On the other hand, they offer vast market potential and have drawn considerable interest from the capital markets, resulting in a relatively higher success rate for commercialization.

Finally, in terms of therapeutic areas. According to statistics, among the 121 companies that completed early-stage financing in the first half of this year, a total of 38 startups focused on oncology and cardiovascular therapeutics, accounting for 31.4% of the total. Of these, 29 were oncology-focused companies, and 9 were cardiovascular-focused companies.

In fact, there are good reasons why startups are willing to focus on these areas. Currently, oncology and cardiovascular diseases both have significant clinical needs, which means that the corresponding product markets have substantial potential. As a result, they attract considerable attention from the capital market.

As a senior venture capitalist told VCBeat, “investing early” often depends less on the founders and more on the technology itself and the choice of therapeutic area—the startup’s “core strength.” If a startup operates in a field with significant unmet clinical needs and possesses proprietary, original technological achievements, it will inevitably gain faster traction in the market.

03. Who Invested in Them?

Investment remains the focal point of the early-stage healthcare market.

First, in terms of market enthusiasm, early-stage healthcare investment has become an industry consensus. Statistics show that in the first half of this year, there were as many as 121 early-stage financing deals in China’s healthcare sector, with the total financing amount approaching RMB 10 billion. Both core figures have experienced explosive growth compared to the same period last year.

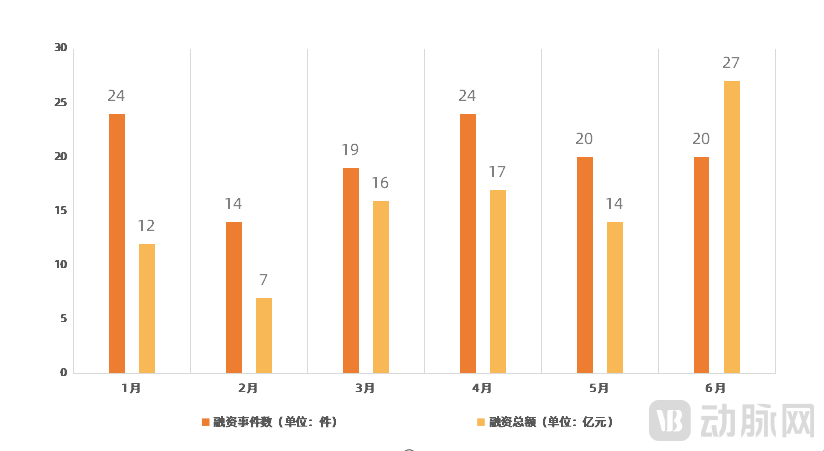

Figure 4. Monthly Early-Stage Financing in the Healthcare Sector, First Half of 2022

Breaking it down by month, although the first half of this year was continuously affected by the pandemic, the early-stage healthcare market remained stable, with approximately 20 financing events recorded each month.

In fact, the current investment fervor in the early-stage healthcare market is inevitable. In recent years, the trend toward younger listed companies in the medical sector has become increasingly pronounced. Taking 2021 as an example, among the 98 newly listed companies, 31 had been established for less than 10 years, marking a significant compression of the listing cycle compared to the traditional 15–20-year timeline in the healthcare industry.

As going public becomes increasingly “easy,” the pace of investment and financing is accelerating accordingly. Many companies have completed two or even three rounds of financing within a single year, a speed that far exceeds previous norms.

Therefore, in such an investment environment characterized by “rapid matching,” the boundaries of investment will become increasingly blurred. Investment institutions that previously focused solely on the mid-to-late stages will find it difficult to identify a suitable entry point; consequently, they will have to shift their focus to early-stage projects and cultivate them from “ground zero.”

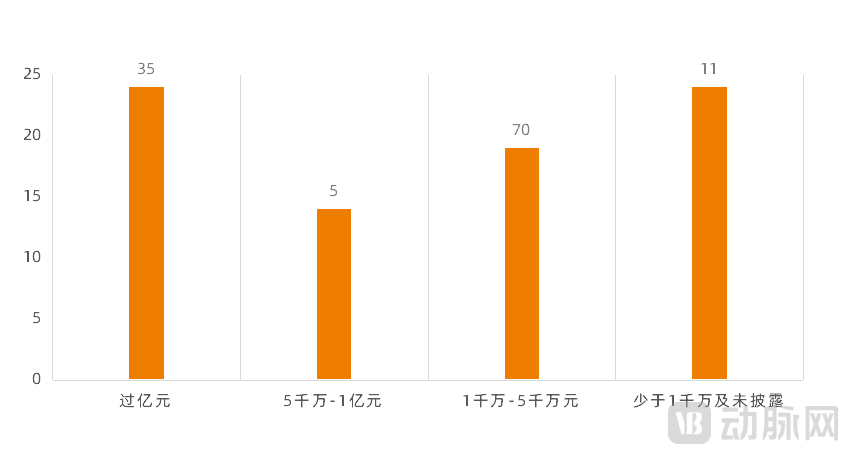

Secondly, in terms of investment amount, the overall “unit price” has risen, and the number of deals exceeding RMB 100 million has increased. Historical data shows that early-stage investments in the healthcare market were relatively “inexpensive,” mostly ranging from millions to just over ten million yuan. However, the landscape has now changed completely.

Figure 5. Distribution of Early-Stage Financing Amounts in the Healthcare Sector in the First Half of 2022

According to statistics, among the 121 healthcare companies that completed early-stage financing in the first half of this year, 35 raised over RMB 100 million each, accounting for 28.9%. Among them, NearView Technology, a BTIT overall solution provider; Yuesai Biologics, a cell therapy drug developer; and Lingfu Biotechnology, a laboratory animal research service provider, emerged as the most well-funded startups in the early-stage healthcare market during the first half of the year, with each securing RMB 200 million in early-stage financing.

In addition to the growing number of companies valued at over RMB 100 million, financing rounds in the tens of millions have become the “standard” in the early-stage healthcare investment market. Statistics show that among the 121 healthcare companies that completed early-stage financing in the first half of this year, 75 secured funding in the tens of millions, accounting for 62%.

There are clear reasons behind the “price increase” in early-stage financing, one of which is that startups are allocating a higher proportion of their resources to R&D than ever before. Currently, most healthcare startups are rooted in “hard tech,” making R&D a critical component of their early growth and accounting for a significant share of their expenditures.

This trend is clearly evident from the use of proceeds by startups that secured early-stage financing in the first half of the year. The vast majority allocated their early funding to R&D for their product pipelines or to building out their R&D teams. Although costly, focusing on R&D is indeed a sound decision, as it is the lifeline of any startup and will inevitably drive its future growth trajectory. Nevertheless, striking a balance between R&D investment and revenue generation remains a critical aspect of a startup’s growth journey.

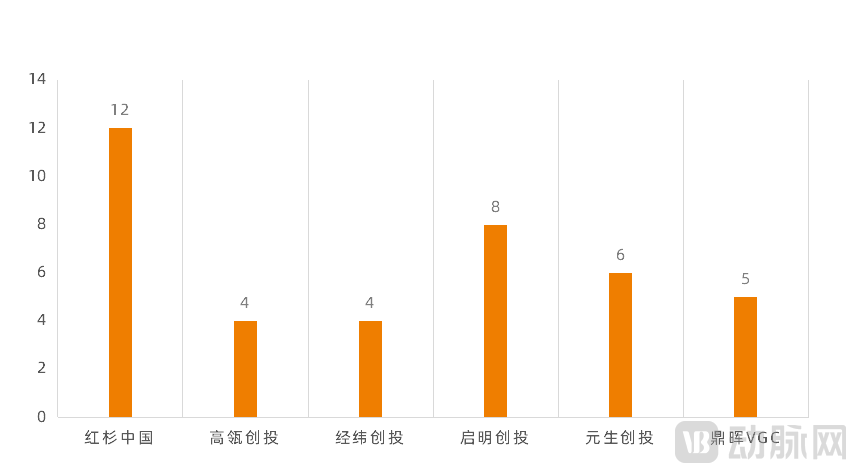

Finally, from the perspective of investment institutions, top-tier firms have successively entered the market with high transaction efficiency, while research universities and institutes have begun establishing their own “proprietary capital pools.” Statistics show that among the 121 early-stage financing deals completed in the first half of this year, a total of 177 investment institutions participated, including prominent firms such as Sequoia Capital, Hillhouse Ventures, Matrix Partners China, Yisheng Capital, CDH VGC, and Qiming Venture Partners.

Figure 6. Number of Early-Stage Healthcare Investment Deals by Investment Institutions in the First Half of 2022

Among them, Sequoia has been the most active, completing 12 early-stage financing deals in the healthcare sector in the first half of this year, demonstrating keen insight and strong execution capabilities.

In fact, as one of China’s top investment firms, Sequoia had already begun making moves in early-stage investing as early as 2018. In that year, it pioneered the launch of Sequoia China Seed Fund, and over the past three years, it has connected with more than 13,000 entrepreneurs, invested in over 170 early-stage companies, many of which have progressed to the growth stage, with several becoming unicorns valued at over $1 billion.

In addition to the influx of leading investment firms, the early-stage healthcare market has seen the emergence of angel investment institutions “endorsed” by research universities and institutes. Taking NearSight Technology, mentioned earlier, as an example, its investor lineup includes the Shanghai Industrial Technology Research Institute. Another case is Shengshi Technology, whose investors include the Zhejiang University Innovation Institute, a fund dedicated to incubating outstanding research teams and scientific achievements at Zhejiang University. Additionally, Uxin Hesheng counts Tsinghua X-Med among its investors, a specialized investment institution for the commercialization of scientific and technological achievements established under the Tsinghua Industrial Technology Research Institute.

In fact, such early-stage financing models are already highly mature in developed countries led by the United States, and practical outcomes have demonstrated their significant advantages in incubating early-stage medical projects.

First, it provides scientists with more investment options, reducing the cost of blindly seeking out investment firms. Second, it enables “precision investment,” meaning that these investment institutions can provide startups with market-oriented resources that synergize with their own business operations. Finally, it effectively “protects” scientists. Due to their unique characteristics, early-stage projects are not well-suited for excessive public exposure. In this relatively closed investment environment, scientists can quickly build trust with investors while safeguarding the “privacy” of their startup projects.

04. Where did they land?

For startups, in addition to building a core team and securing early-stage financing, there is another critical task: selecting a location for establishment.

This is critically important. If the supportive policies offered by a region, along with its corresponding upstream and downstream resources, align with the development trajectory of startups, they will provide substantial momentum for these enterprises during their early growth stages.

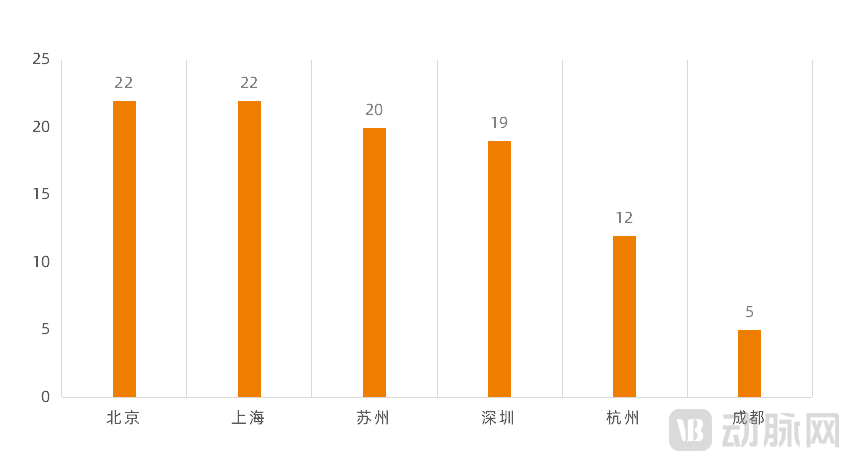

Figure 7. Implementation Status of Early-Stage Investments in the Healthcare Sector During the First Half of 2022

According to statistics, among the 121 healthcare companies that completed early-stage financing in the first half of this year, their locations were primarily concentrated in four cities: Beijing, Shanghai, Shenzhen, and Suzhou. A total of 83 companies were based in these cities, accounting for 68.6% of the total. Among them, Shanghai and Beijing each hosted 22 startups, while Suzhou and Shenzhen hosted 20 and 19 companies, respectively.

Among these, two cities deserve special mention: Suzhou and Shenzhen. Let us begin with Suzhou. As a highly representative region in China’s medical industry landscape, Suzhou serves as a model for regional industrial development in the biopharmaceutical sector, whether in terms of policy direction, the construction of its overall ecosystem, or its corresponding industrial resources.

It is precisely for this reason that many startups in the healthcare sector are keen to establish their operations here. Statistics show that among the 20 healthcare companies that completed early-stage financing and settled in Suzhou in the first half of this year, 14 were biopharmaceutical firms and 6 were medical device companies. All are deep-tech enterprises with strong growth potential.

Having discussed Suzhou, we now turn to Shenzhen. As a rising star in China’s medical industry landscape, Shenzhen has demonstrated remarkably rapid growth in the early-stage medical market in recent years. This momentum is directly reflected in its data: statistics show that 19 early-stage medical companies completed early-round financing and established operations in Shenzhen during the first half of this year, with their scale basically on par with core regions such as Beijing, Shanghai, and Suzhou. Looking ahead, Shenzhen will further leverage its scientific research advantages and deeply tap into industrial resources, undoubtedly unlocking greater potential in the early-stage medical market.

Having discussed the four core regions, we now turn our attention to several standout areas. First is Hangzhou. As a national representative city for digitalization, Hangzhou has not only attracted numerous leading digital health companies but also incubated multiple digital health startups in the medical sector in recent years. Statistics show that among the 12 healthcare companies that completed early-stage financing and established operations in Hangzhou during the first half of this year, four were digital health enterprises.

Take Purui Life Sciences, which completed a RMB 100 million Pre-A financing round in January this year, as an example. It is an innovative enterprise that combines a global innovation vision with the ability to localize and digitally transform technologies in China. The company is committed to building a big data federation cooperation network covering the entire health lifecycle. By leveraging digital technology innovation and the deep application of artificial intelligence, it aims to lead the transformation of clinical research operations for biopharmaceuticals and medical devices, pharmaceutical commercial operations, and digital health service models.

Two other cities worth watching are Chengdu and Anhui. Although the overall data from the early-stage healthcare market in the first half of the year does not show significant benefits, from a future perspective, there is a high probability that Chengdu and Anhui will become another incubator for early-stage healthcare companies. Especially in Chengdu, the momentum of moving forward in the early-stage healthcare market is already very clear.

05. Final Thoughts

The early-stage healthcare market is akin to "traffic stars" in the entertainment industry, generating significant market buzz. However, unlike such celebrities, its current performance metrics remain relatively strong. In the second half of this year, as pandemic-related factors wane and the market gradually reopens, the early-stage healthcare investment sector may usher in a true period of explosive growth.

However, from a rational perspective, China’s early-stage medical market is still in its infancy and faces a variety of pressing issues that need to be addressed.

From the perspective of scientists, the core challenges they currently face are how to achieve technological innovation and how to become qualified entrepreneurs. From the standpoint of research institutions and universities, the key difficulty they must overcome is providing appropriate support during the process of innovating and commercializing scientific achievements.

Next are investment institutions, for whom the core challenges to be addressed urgently are how to reach and screen early-stage healthcare projects, and how to support their growth more effectively. Finally, for local governments, the key variables in future investment attraction will lie in introducing more targeted policies and establishing a robust incubation ecosystem for early-stage projects.

Innovation and translation of scientific research achievements in the medical field have never been a one-sided endeavor; they invariably require multi-party participation. In the current landscape, every stakeholder along this industry chain should engage in more rational reflection: Where should I position myself? What can I contribute? And where do my core competencies lie?