H1 2022 Global Healthcare Industry Capital Report: Early-Stage Projects Continue to Grow, Domestic Secondary Market Poised for Recovery

I. Factors such as regional conflicts, SARS-CoV-2 variants, energy shocks, debt burdens, and economic inflation led to a decline in total domestic and overseas financing in the first half of 2022, with investors becoming increasingly cautious. However, given the continued increase in the number of financing deals and the fact that the decrease in financing volume is primarily measured against the exceptional surge seen in 2021, the healthcare industry is poised for a new turnaround in the second half of 2022.

II. In the medical device and biopharmaceutical sectors, capital continues to concentrate on high-valuation “golden tracks” such as early cancer screening, genetic testing, and cell and gene therapy (CGT) technologies. While the domestic digital health sector has cooled, newly minted unicorns in the overseas digital health market are demonstrating strong momentum.

III. Influenced by the development of private equity financing, intensified M&A trends, and the underperformance of healthcare companies listed in 2021, the number of healthcare enterprises listing on U.S. stock exchanges decreased in the first half of 2022. On the other hand, numerous domestic companies concentratedly submitted their prospectuses in late June, signaling an imminent recovery in the secondary market.

IV. Domestic investment institutions are focusing on early-stage and small-scale investments. Under policy guidance, early-stage projects centered on innovative technologies and the commercialization of scientific research outcomes are receiving priority attention. For instance, brain science and innovative small-molecule drugs have become key focus areas for Sequoia Capital China.

V. The Rise of Innovative Healthcare Forces in Asia, with Jiangsu Province Becoming a Hotbed for Domestic Capital.

VI. Top 10 Most-Funded Companies in H1 2022: Nuowei Health Leads Globally with $760 Million in Financing, While Synthetic Biology and Large-Molecule CDMO Sectors in China Attract Significant Capital Interest.

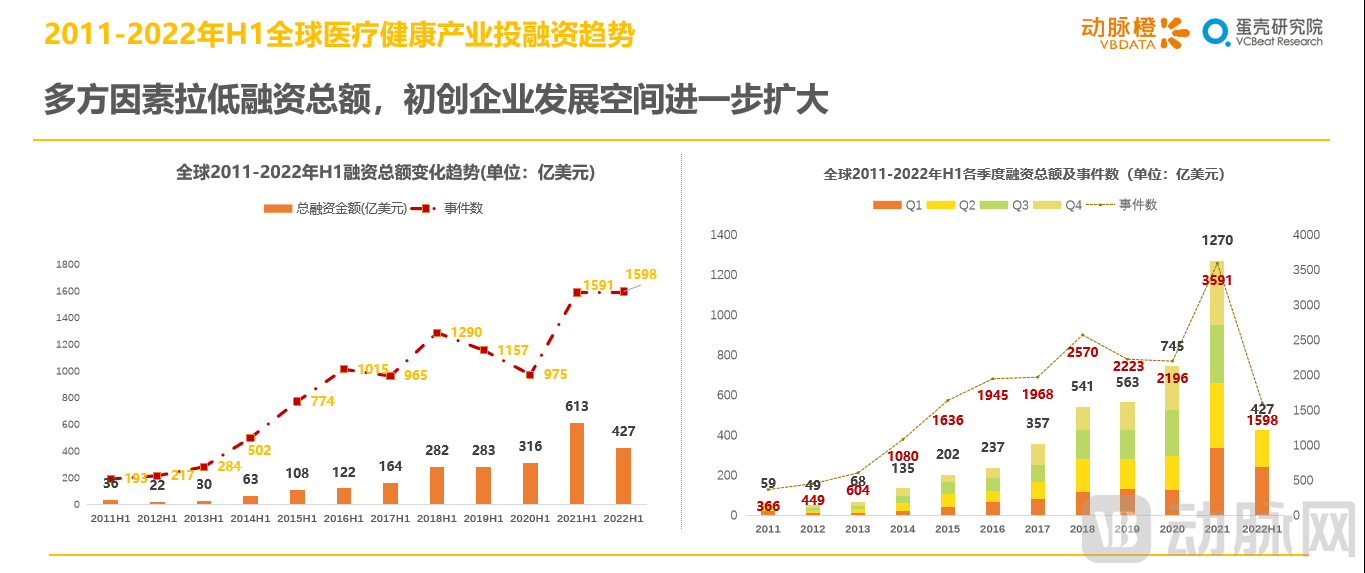

1.1 Multiple Factors Drive Down Total Financing, Further Expanding Growth Space for Startups

Affected by factors such as regional conflicts, the pandemic, energy issues, debt, and inflation, both domestic and international capital markets experienced a certain degree of volatility in the first half of 2022. Industry perspectives at home and abroad offered less-than-optimistic outlooks for the capital markets, which in turn impacted the healthcare industry during the first half of 2022—

In H1 2022, a total of 1,598 financing deals occurred in the global healthcare industry, an increase of six year-on-year. The total financing amount reached $42.7 billion (approximately RMB 277.734 billion), ranking second highest in history. This figure represents a decline of approximately 43% compared to the historical peak in H1 2021, indicating an overall cooling trend. Meanwhile, capital continued to maintain its 2021 stance toward startups in H1 2022: inclusivity further increased, with more high-potential and high-growth startups receiving financial support.

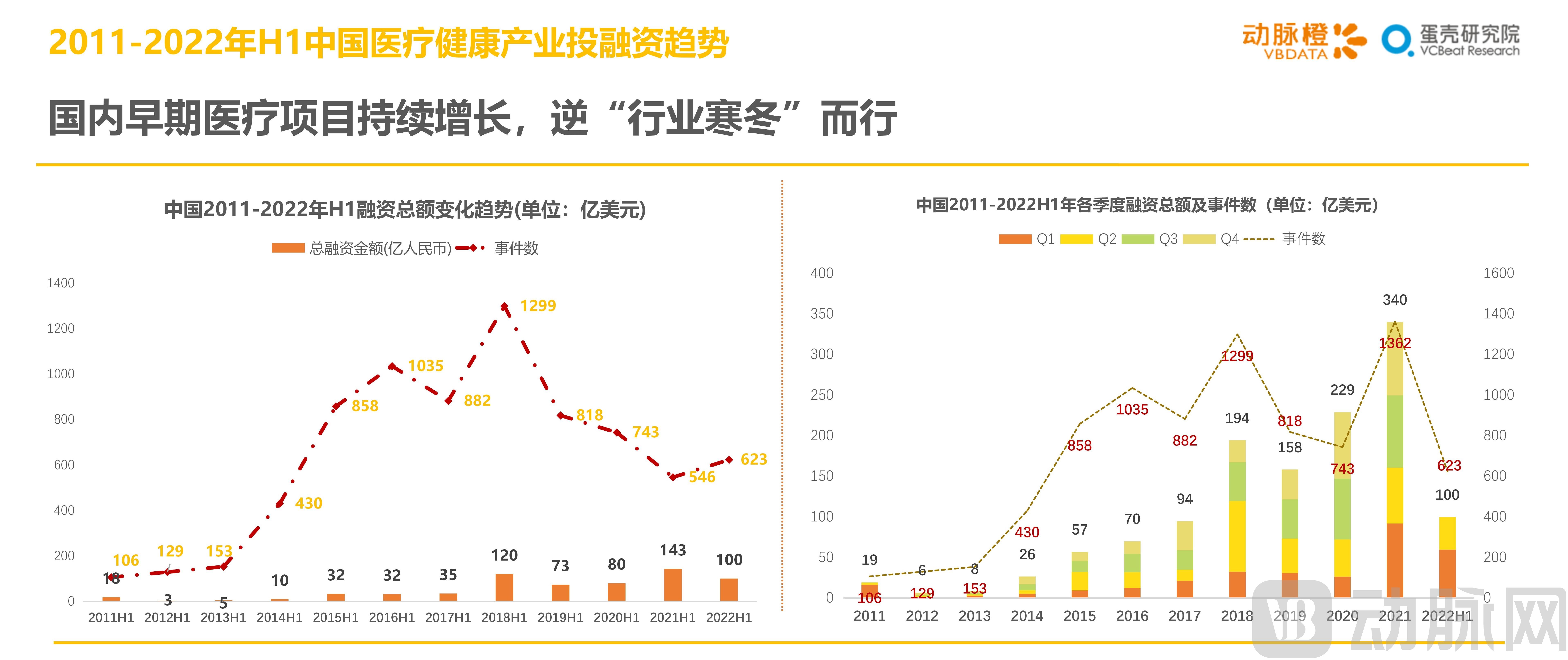

1.2 Early-stage medical projects in China continue to grow, bucking the “industry winter” trend

In H1 2022, the total investment and financing in China's healthcare industry amounted to nearly USD 10 billion (approximately RMB 64.759 billion), representing a year-on-year decline of over 40%; meanwhile, the number of domestic financing transactions reached 623, an increase of 77 compared with H1 2021.

This phenomenon is attributed to the increase in early-stage investment projects. In the first half of 2022, there were 180 early-stage financing and investment events (including seed rounds, angel rounds, and Pre-A rounds) in China’s healthcare sector, with cumulative funding reaching nearly $900 million. Both the number of financing deals and the total amount raised approached the full-year figures for 2021 (296 financing deals totaling over $1.194 billion, approximately RMB 7.76 billion).

In recent years, under the direct pressure of “performance evaluations,” research institutions and scientists have become more focused on the commercialization of scientific achievements than ever before. With substantial policy guidance, financial support, and resource linkage in China, a group of scientists has followed the trend, moving from laboratories to the marketplace. Furthermore, as the healthcare industry gradually extends into high-tech fields, innovative projects with original technologies and significant market potential are more likely to stand out in the early-stage market.

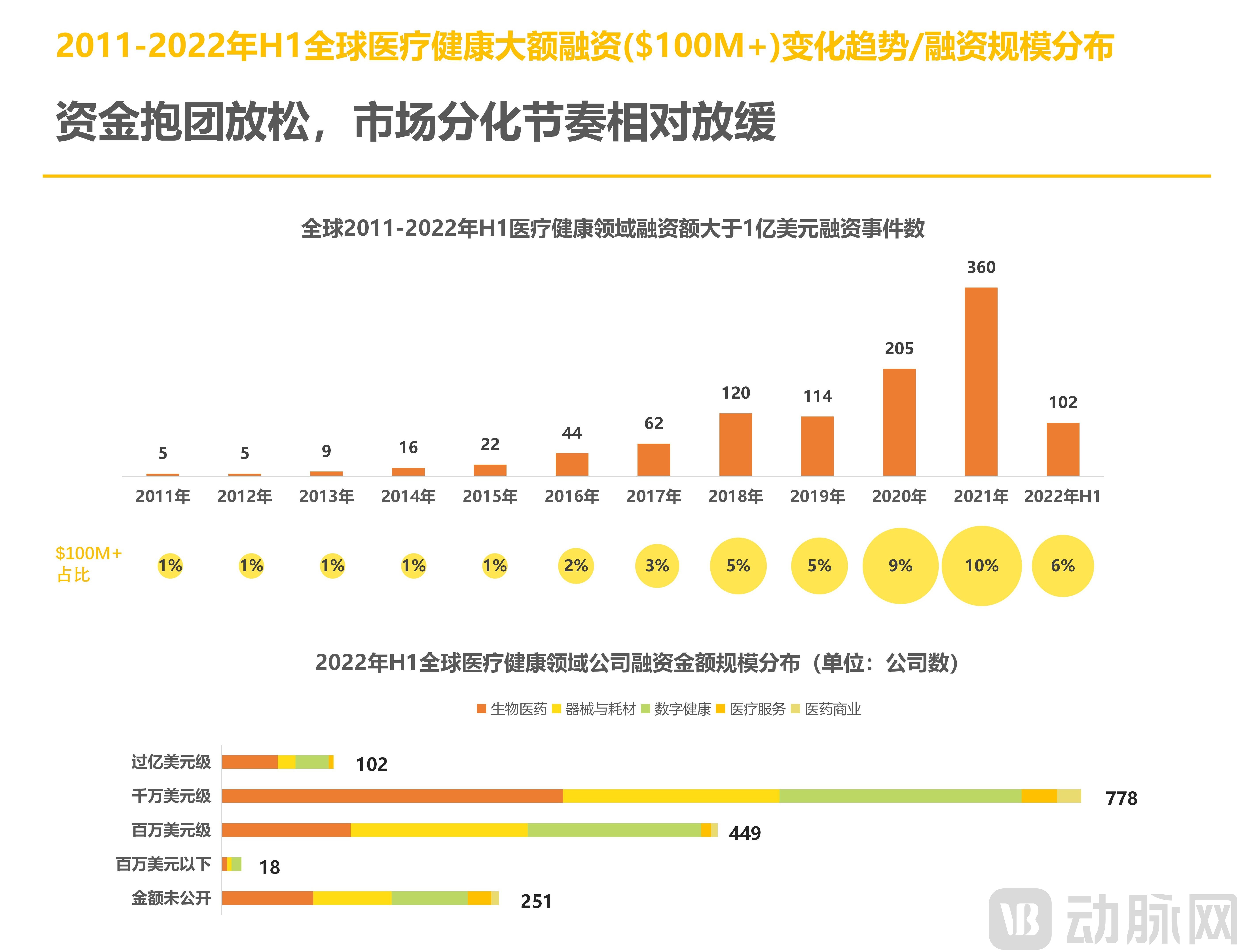

1.3 Easing of Capital Herding, Relatively Slower Pace of Market Divergence

The trend from Q1 2022 continued through the end of the first half of the year: in H1 2022, there were 102 global financing deals exceeding $100 million each, accounting for over 6% of the total financing amount in H1, which was lower than the same period in 2021; half of these deals originated from the biopharmaceutical sector.

Moreover, among the most numerous financing rounds in the tens of millions of dollars, biopharmaceutical companies accounted for the largest share, demonstrating a clear advantage and continuing to widen the gap with companies in the digital health and medical device sectors.

Similar to 2021, global economic sentiment remained weak in the first half of 2022. However, compared to the capital concentration driven by the defensive nature of the healthcare industry during 2020–2021, this trend significantly eased in H1 2022, while momentum for startups continued to rise.

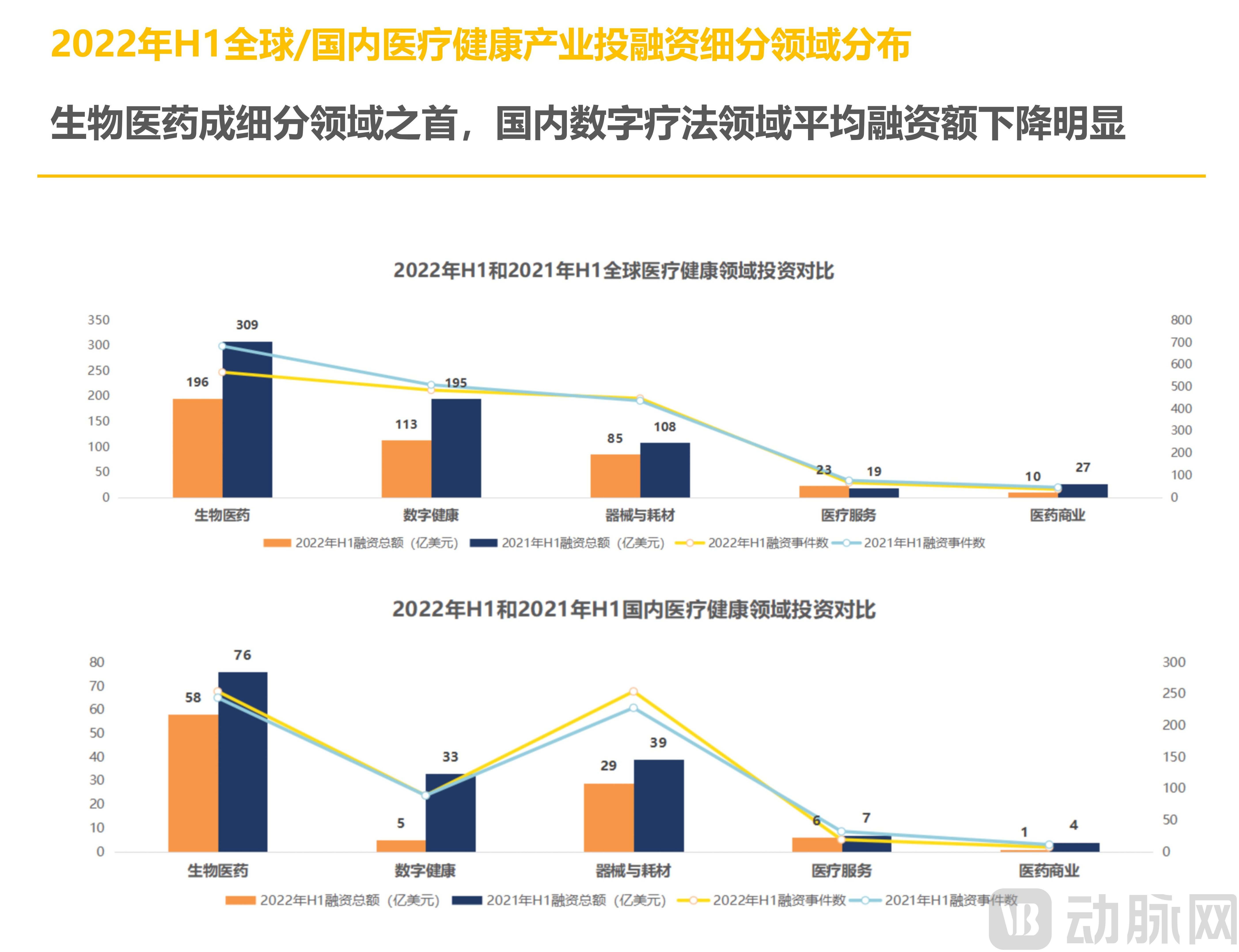

2.1 Biopharmaceuticals Lead Among Subsectors, While Average Financing in China’s Digital Therapeutics Sector Declines Significantly

In H1 2022, the global biopharmaceutical sector led all subsectors with 565 transactions totaling $19.63 billion (approximately RMB 131.605 billion). The digital health and medical device sectors followed closely, with 484 and 447 transactions, respectively. Compared with H1 2021, both the total financing amount and the number of financing events across all global sectors declined to varying degrees in the current period, with the digital health sector experiencing the most pronounced drop, as its total financing amount decreased by 42% quarter-on-quarter.

An analysis of the overall financing landscape across various sectors in China reveals that a significant decline in digital health financing is partly attributable to a decrease in the average financing amount within this sector. In the first half of 2021, eight digital health companies secured financing rounds exceeding USD 100 million, and eleven companies advanced beyond Series D. In contrast, no such large-scale financing deals exceeding USD 100 million occurred in China’s digital health sector in 2022; funding was primarily concentrated at the million-dollar level. Only two companies, Yitu Healthcare and Zhiyun Health, progressed beyond Series D (with Zhiyun Health listing on the stock market in early July 2022). Financing rounds were predominantly focused on early stages. This indicates that amid the “capital winter,” while investment institutions have actively maintained their presence in the sector, they have adopted a more wait-and-see approach.

2.2 Policy Support and Capital Frenzy: CGT Gains Momentum as the Industry Enters the “Fast Lane”

In H1 2022, the global cell and gene therapy sector witnessed 96 transactions, with cumulative financing amounting to $3.836 billion.

Specifically, in the first half of 2022, domestic companies in the cell and gene therapy sector completed 53 transactions, with cumulative financing reaching $841 million. In comparison, while the number of transactions in China was higher than that abroad, the total transaction value was significantly lower.

In January 2022, the “14th Five-Year Plan for the Development of the Pharmaceutical Industry” proposed prioritizing the development of industrialized manufacturing technologies for novel biologics, such as cell therapy and gene therapy drugs. Meanwhile, in the first half of the year, the cell and gene therapy sector attracted top-tier investment firms including Sequoia Capital, Hillhouse Capital, Matrix Partners China, Qiming Venture Partners, OrbiMed, and RA Capital. This indicates that, supported by policy, technology, capital, and downstream markets, the cell and gene therapy industry is entering a “fast lane.”

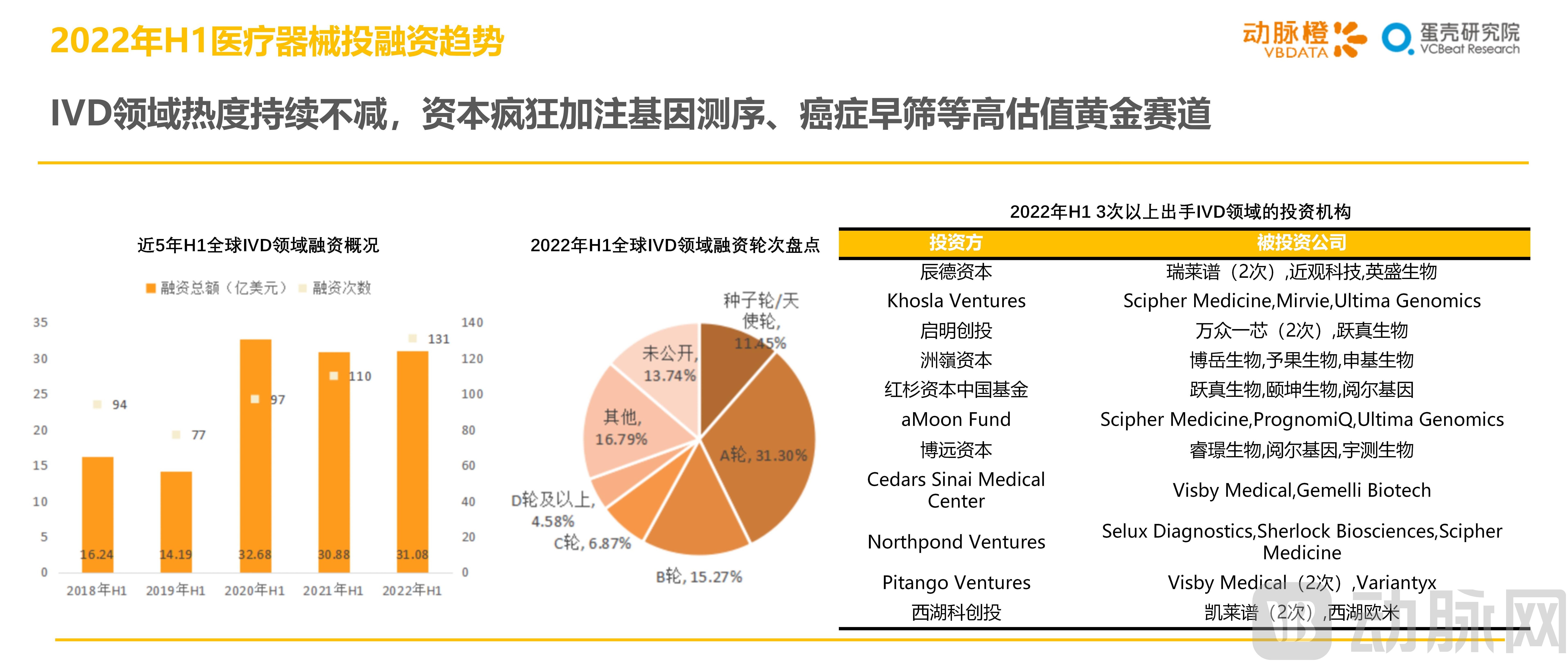

2.3 The IVD Sector Remains Highly Attractive, with Capital Aggressively Betting on High-Valuation Golden Tracks Such as Gene Sequencing and Early Cancer Screening

While total financing across the entire healthcare sector declined in H1 2022, investment enthusiasm in the IVD (In Vitro Diagnostics) segment remained robust. The total financing amount was essentially flat compared to H1 2021, with the number of financing deals increasing by 21. The average deal size decreased slightly, and financing rounds were predominantly concentrated at Series A.

The sustained fervor in IVD sector financing is primarily driven by two factors. On one hand, the fluctuating and recurring nature of the COVID-19 pandemic has led to FDA and NMPA approvals for multiple COVID-19 antigen self-test products, creating new application scenarios for the IVD industry. On the other hand, capital continues to focus on high-valuation “golden tracks” such as gene sequencing and early cancer screening. For instance, Yuezhen Biotechnology, dedicated to developing single-cell sequencing technology, received additional investments from both Qiming Venture Partners and Sequoia Capital China; Yingsheng Biology, deeply entrenched in the clinical mass spectrometry market, completed a C-round financing worth hundreds of millions of RMB under the joint lead investment of Chende Capital and Hillhouse Investment; and Aorui Biology, which launched a five-cancer early screening product, secured over RMB 100 million in Series B financing in January 2022.

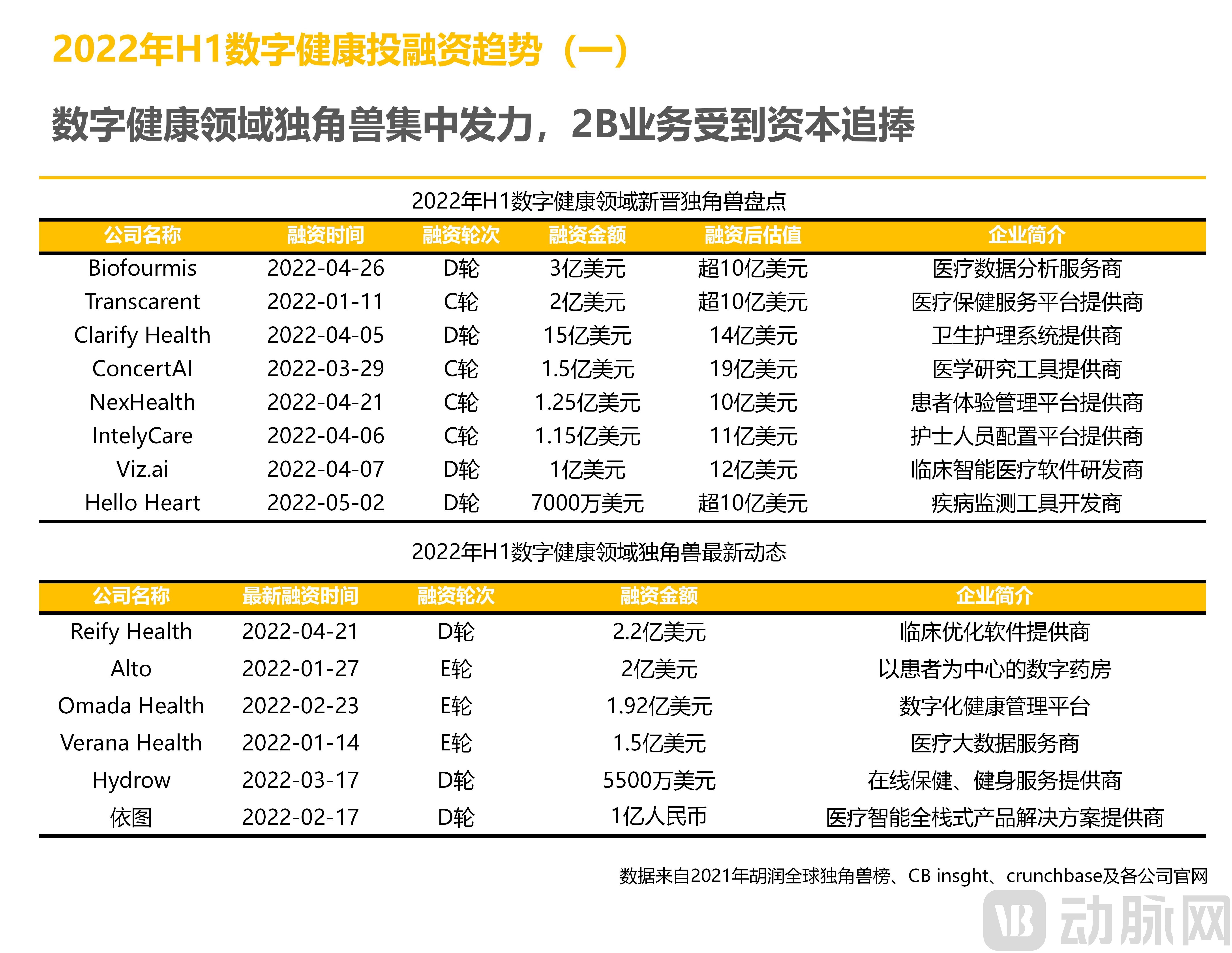

2.4 Unicorns in the Digital Health Sector Intensify Efforts, with B2B Businesses Garnering Strong Investor Interest

From its inception to the present, the “unicorn” concept has evolved such that its once-emphasized characteristic of “rarity” became commonplace by 2022. Following 2021—a record-breaking year for unicorns—the development of unicorn companies entered a new phase. Specifically, in the digital health sector, eight new unicorns emerged globally in the first half of 2022.

Trends such as APIs (Application Programming Interfaces), the expansion of virtual care, and the decentralization of health data will continue to drive demand for digitalization in the healthcare industry.

However, current digital health unicorns primarily cater to enterprise-side demands; there remains significant growth potential for businesses targeting end-consumer needs in the future.

2.5 Rising Demand for Medical Data Access Services Drives Capital Toward Startups

The U.S. 21st Century Cures Act requires providers to enable patients to easily and digitally access their medical records through application programming interfaces (APIs). Influenced by this, in addition to companies that have already become digital health unicorns, the relevant provisions of the Act have also prompted some emerging healthcare IT enterprises in the United States to enter the data access services market.

Meanwhile, the FHIR (Fast Healthcare Interoperability Resources) standard, as a non-mandatory guideline, has been incorporated into the business development plans of some startups due to its role in facilitating the secure exchange of health information.

Given the continued use of various health applications that collect and share health data by enterprises, the demand for health data will continue to rise in the future. This trend has also attracted the attention of various investors in the United States, who are adopting a "broad net" approach to bet on startups.

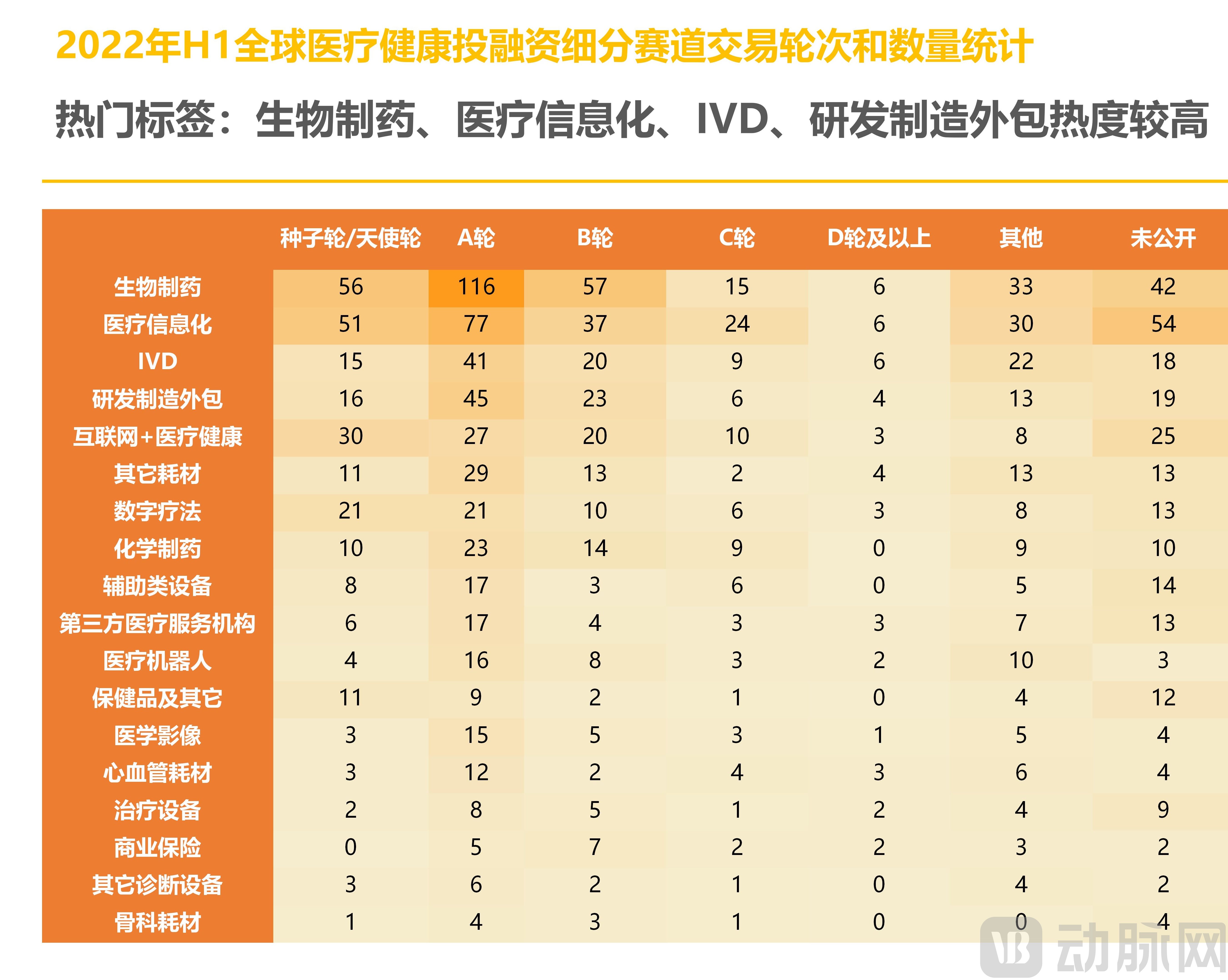

2.6 Trending Tags: Biopharmaceuticals, Healthcare Informatics, IVD, and R&D and Manufacturing Outsourcing Are Highly Popular

In H1 2022, tags such as biopharmaceuticals, healthcare IT, IVD, and R&D and manufacturing outsourcing garnered significant attention.

In terms of funding rounds, public financing in the first half of 2022 was concentrated primarily in early stages, especially Series A. Few companies advanced to Series D and beyond. Specifically, these enterprises were all positioned in high-barrier innovative segments within the healthcare sector. Examples include Tongxin Medical, which received the National Medical Products Administration’s first approval for a fully magnetically levitated ventricular assist device (VAD) in the artificial heart segment; Jingyu Medical, which has been deeply engaged in deep brain stimulation within the invasive brain-computer interface segment; and Fourier Intelligence, which set the record for the largest single-round financing amount in the rehabilitation robotics segment.

It is evident that in 2022, amid the overall decline in global healthcare financing and the ensuing “capital winter,” investment institutions actively pursued early-stage and small-scale investments while continuing to focus on high-potential sectors with substantial long-term growth prospects.

3.1 Sequoia Capital China Fund made 35 investments cumulatively, becoming the most active investment institution in the first half of the year

In H1 2022, the most active institution in the global healthcare and medical sector was Sequoia Capital China, which made a total of 35 investments during the first half of the year, primarily targeting biopharmaceutical companies. Notably, NeuroXess, a developer of invasive brain-computer interfaces, and Xinrui Regenerative Medicine, a small-molecule new drug developer, each received two rounds of additional funding from Sequoia Capital China within the six-month period.

Qiming Venture Partners ranked second with 28 investments in the first half of 2022. Notably, Qiming Venture Partners led 17 of these 28 financing rounds.

In the first half of 2022, 52 early-stage biopharmaceutical companies secured financing from the top 10 most active investment firms, indicating a tendency for investors to concentrate their investments in early-stage biopharmaceutical enterprises.

3.2 Local Policy Guidance Encourages Early-Stage and Small-Scale Investments, with Investment Institutions Concentrating Efforts on Early-Stage Healthcare Projects

In H1 2022, the most active institution in China's healthcare and medical sector was Sequoia Capital China Fund, which made a record-breaking total of 35 investments throughout the year, primarily targeting biopharmaceutical companies.

The top 10 investment institutions in China all favor the fields of biomedicine and medical devices, with most investments occurring around Series A. By analyzing specific financing events and market conditions in China during the first half of the year, we find that the primary reason for this trend is policy-related.

Driven by policy guidance from local governments in recent years encouraging investment institutions to invest early and in small-scale ventures, investment firms have focused on early-stage projects in the first half of the year. For instance, the “Several Measures to Promote the Sustained High-Quality Development of Venture Capital and Private Equity in Shenzhen,” issued by the Shenzhen Municipal Local Financial Supervision and Administration Bureau on April 7, 2022, explicitly outlined incentives for investment institutions that invest in seed-stage and start-up technology innovation enterprises in Shenzhen.

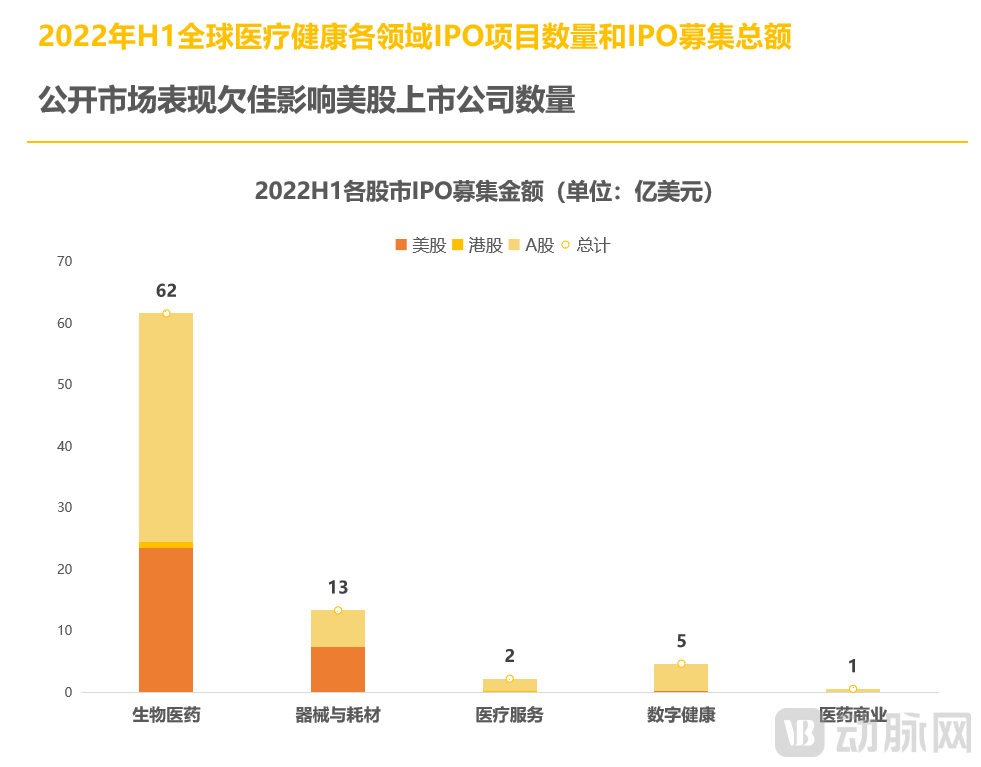

4.1 Weak Public Market Performance Affects the Number of U.S.-Listed Companies

According to the VCBeat Orange Database, in the first half of 2022, a total of 59 healthcare companies were listed on the A-share, U.S., and Hong Kong stock markets, raising over $8.668 billion. Both the number of listings and the amount raised saw a significant year-on-year decline compared to the first half of 2021. Moreover, unlike previous years when U.S.-listed companies accounted for “half the market,” the gap in the number of companies listed on the A-share and U.S. stock markets narrowed in 2022.

The post-IPO performance of healthcare companies that went public in 2021 influenced the IPO landscape in 2022: The biopharmaceutical sector set a record in 2021, with preclinical/Phase I companies accounting for half of the listings; however, their average stock price performance after listing declined significantly compared to the previous two years. Meanwhile, the post-IPO performance of digital health and medical device companies (particularly those in the IVD sector) also fell short of expectations.

4.2 In June, as many as 126 new companies had their applications accepted, signaling an imminent recovery in China’s secondary market

In H1 2022, the number of Chinese companies listing on the three major stock exchanges declined. In addition to the slowdown in U.S. listings by Chinese concept stocks in the second half of 2021 due to regulatory and policy changes, some healthcare companies in Beijing and Shanghai suspended operations to comply with epidemic prevention measures, leading to setbacks in both domestic financing and IPOs.

Nevertheless, the sluggish performance of China’s domestic secondary market is expected to break through in the second half of the year. In just three days from June 27 to June 29, five healthcare companies filed their prospectuses with the Hong Kong Stock Exchange; the number of new applicants accepted by the STAR Market and the ChiNext Board reached a record high of 126, with five companies successfully passing the listing committee review.

The IPO processes of healthcare companies collectively entered an acceleration phase in the latter half of the first half of 2022, with pharmaceutical companies demonstrating particularly strong performance. Moreover, the sentiment in the secondary market often influences the investment climate in the primary market.

5.1 The US Leads Globally as Asia’s Medical Innovation Forces Rise

In H1 2022, the five countries with the highest number of global healthcare financing events were the United States, China, the United Kingdom, Israel, and India.

In H1 2022, the United States led globally with 676 financing deals totaling $25.53 billion (RMB 171.156 billion), followed closely by China. Together, the U.S. and China accounted for 83% of the total global financing amount and 82% of all financing deals.

Moreover, the power of medical innovation in Asia is on the rise. In particular, Israel and India have seen a significant surge in healthcare financing, ranking among the top five hotspots.

From the perspective of investment hotspots, biopharmaceuticals and digital health were the areas of global focus in the first half of 2022.

5.2 Jiangsu Overtakes Shanghai in Number of Financing Events, Becoming a Hotbed for Domestic Capital

In 2022, the five regions in China with the highest concentration of healthcare investment and financing activities were Jiangsu, Shanghai, Beijing, Guangdong, and Zhejiang, in descending order.

Leveraging the spillover benefits from Suzhou’s biopharmaceutical industry hub, Jiangsu surpassed Shanghai for the first time to become the most active region in primary market healthcare investment, with 132 financing deals and nearly $1.7 billion (RMB 7.017 billion) raised. This outpaced second-ranked Shanghai, which recorded 125 financing deals and raised over $2.9 billion (RMB 12.899 billion).

Overall, healthcare financing in H1 2022 remained concentrated in Beijing, Shanghai, and Guangzhou—regions characterized by a solidified healthcare industry foundation and the aggregation of innovative resources. These areas accounted for 54% of all financing deals nationwide.

6.1 TPG’s NovuHealth Completes $760 Million Financing, Ranking First in the First Half of 2022

6.2 Eight Biopharmaceutical Companies Make the List; High Prosperity in the CXO Sector Continues