Eli Lilly Rises to Global No.3 in Top 20 Pharma Rankings Driven by GLP-1 Blockbusters

Johnson & Johnson

Medical Device R&D and Manufacturer

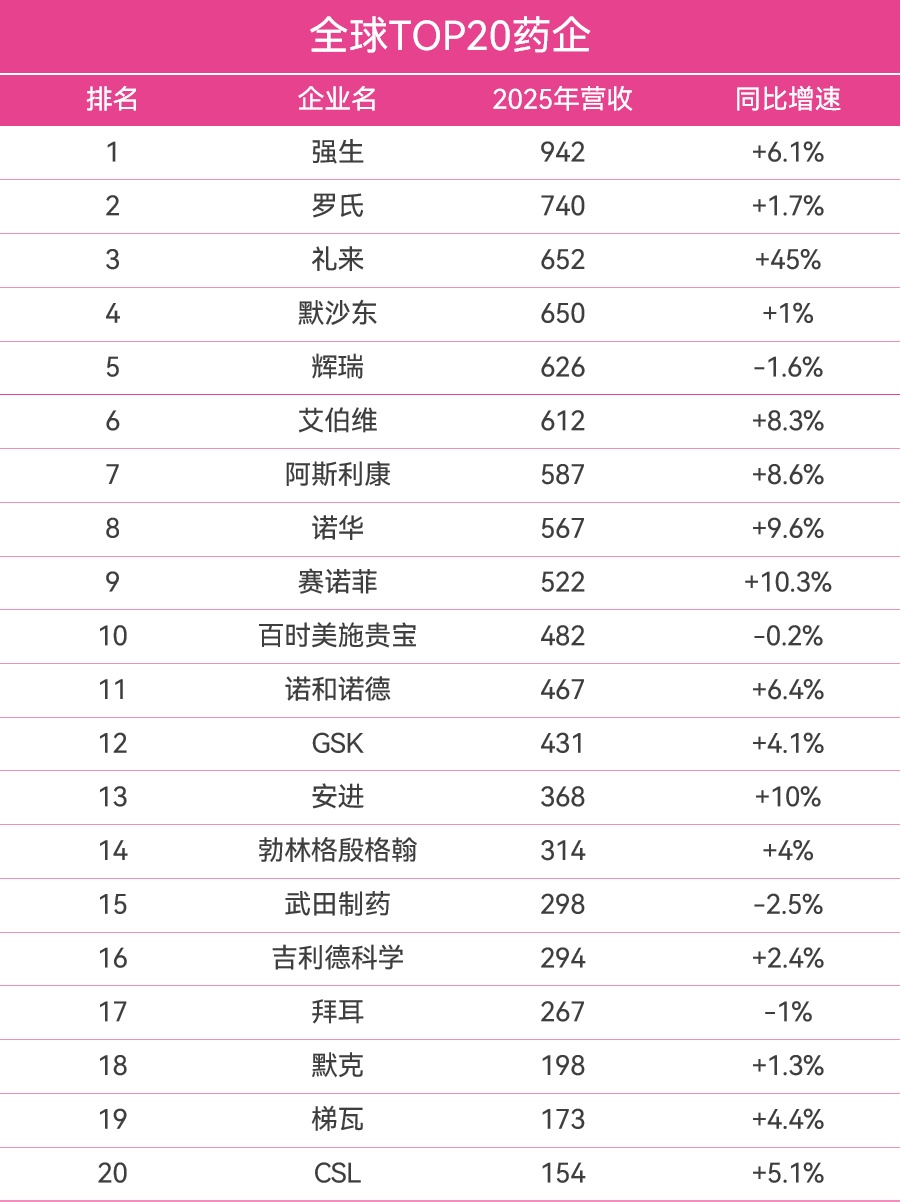

Based on the revenue situation of major pharmaceutical companies in 2025, the well-known industry media Fierce Pharma recently releasedTop 20 Global Biopharmaceutical CompaniesAs the global pharmaceutical industry enters a new cycle of innovation and iteration, this list not only visually presents the changes in the scale rankings of leading companies but also clearly outlines the deep structural transformations taking place in the global pharmaceutical industry.

GLP-1 Drugs Spark Growth

Stable Head Structure

Patent Cliff Becomes a Matter of Life and Death

The differentiation of tracks continues to intensify.

Core Performance of Leading Enterprises

Johnson & Johnson: Firmly in First Place, a Billion-Dollar Threshold in Sight

Lilly: Largest Source of Growth, Highly Concentrated Increase

Novo Nordisk: Growth Slows, Enters Adjustment Phase

Merck & Pfizer: Rebalancing After the Dividend Clearance

VectorBuilder, founded by world-renowned molecular biologist Dr. Lan Tian, is a leading gene delivery company with over 10 subsidiaries and offices worldwide. In 2023, it was promoted to a global unicorn enterprise.

Cloud舟Bio independently developed the "VectorBuilder" platform, ushering in the commercial era of personalized gene vectors; it has currently empowered more than 130 countries and regions worldwide, serving over 7,000 top research institutions and pharmaceutical companies. Its customer coverage in QS Top 100 universities has reached 90%, and its customer coverage among the global TOP30 pharmaceutical enterprises also exceeds 90%. The global citation volume of its product achievements exceeds 7,000 papers.

Cloud舟Bio's gene drug CRO and CDMO projects span multiple countries and regions, including North America, Europe, and Japan. It has successfully supported dozens of projects worldwide in conducting IIT or IND research. Among them, GMP-grade plasmids and lentiviral vectors have received formal IND approval from the U.S. FDA for use in multicenter clinical trials in the United States.

Cloud Boat Biotech is committed to systematically overcoming key technical bottlenecks in the gene delivery industry, creating irreplaceable value for the industry and the world.