Millennial and Gen-Z Pet Owners Fuel a Billion-Dollar Market: Animal IVD Emerges as the New Frontier

Mindray

Medical Device R&D Manufacturer

Reagent kits costing only tens of yuan are sold to veterinary clinics through distributors, where they are bundled with ultrasound, X-rays, and other services into annual check-up packages. By the time these reach pet owners, the price can range from 300 yuan to over 1,000 yuan.

Most older-generation pet owners would reject such high prices. For the current core demographic of pet owners—those born in the 1980s and 1990s—who are also sensitive to veterinary costs, the choice is not whether to seek treatment, but rather to select a more affordable option among the services offered by various hospitals.

Amid the surge in demand for in vitro diagnostics (IVD), established players and early-stage startups have rapidly entered the secondary market to secure their positions. Notably, Dasheng Pet Medical, a subsidiary of Sansure Biotech, generated RMB 13.84 million in revenue and RMB 2.22 million in net profit within less than a year of its establishment, achieving a net profit margin nearly on par with its parent company. Latecomers such as Jiditai and other startups have also managed to break even within a year, generating several million yuan in revenue.

Nevertheless, there is no shortage of players exiting the industry. As a rising star in IVD, is pet diagnostics a true blue ocean or a pseudo-demand?

“2021 China Pet Industry White Paper” data shows that the market size of urban dogs and cats was 249 billion yuan, a year-on-year increase of 20.6%. From 2019 to 2021, while the market share of food decreased from 61.4% to 51.5%, the market share of medical care increased from 19% to 29.2%, an increase of 10.2 percentage points.

58.06 million pet cats and 54.29 million pet dogs together underpin this multi-billion-yuan market. A rough estimate suggests that if the annual penetration rate of pet health check-ups is 8%, with an average expenditure of RMB 500 per check-up on in vitro diagnostics (IVD), the annual spending would amount to approximately RMB 4.49 billion.

The figure of RMB 4.49 billion may appear respectable, but given that there are over 30,000 pet clinics across China, if we assume that 25,000 of these veterinary hospitals can consistently provide in vitro diagnostic (IVD) services, the average annual revenue generated from IVD-based health checkup items would amount to RMB 180,000 per facility. Furthermore, as domestic veterinary hospitals are heavily concentrated in first- and second-tier cities, this level of income is merely moderate for individual medium-to-large hospitals when weighed against their high operational expenditures.

Reality is never perfectly balanced. In fact, whether in the United States, with its well-developed pet market, or in China today, corporate and chain-based business models remain mainstream in the veterinary hospital sector. In 2021, the market concentration of veterinary hospitals in China was approximately 16%. Chain hospitals such as New Ruipeng Group, Ruipai Pet Healthcare, and Chongwu International have been capturing market share backed by significant capital investment, and the revenue generated by individual hospitals through in vitro diagnostics (IVD) will, to some extent, exceed the average level.

Even more compelling is the inherent potential of the market itself. As pets age, pet owners’ health awareness and willingness to spend on medical care are increasing, which will further expand the aforementioned projections. Furthermore, excluding the check-up market, veterinary hospitals also provide certain point-of-care diagnostic services for sick pets, representing an emerging market segment.

In summary, from the perspective of veterinary hospitals, the IVD sector represents a landscape of limited current profits alongside ubiquitous opportunities.

Further Exploration of the Upstream of Pet Hospitals—IVD Suppliers.

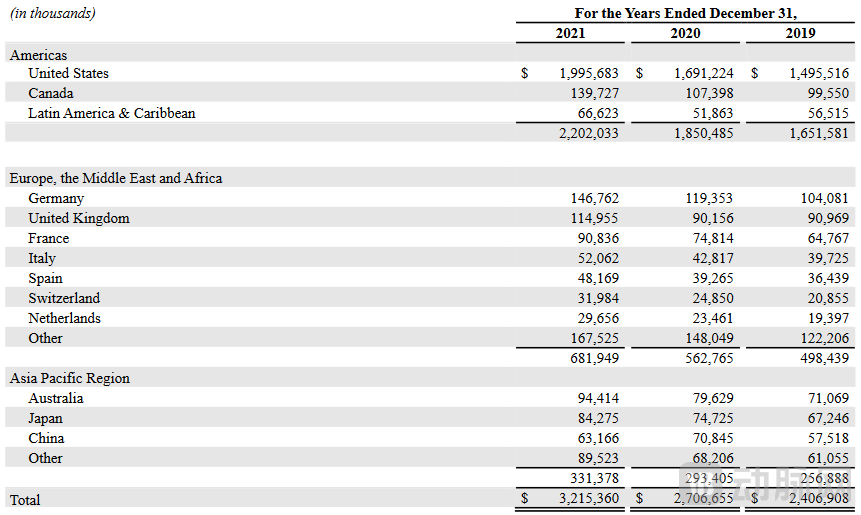

In China’s animal IVD market, IDEXX dominates as the sole major player. Over 39 years of operations, it has built a commercial empire valued at $40 billion, with annual revenue exceeding $3.2 billion. According to its 2021 annual report, the company’s revenue in the China region amounted to $63.17 million, lagging behind various European countries, slightly below the $84.28 million recorded in the Japan region, and significantly lower than the $2 billion generated in the U.S. region.

IDEXX’s Regional Revenue Distribution, 2019–2021 (Source: IDEXX Prospectus)

IDEXX’s Regional Revenue Distribution, 2019–2021 (Source: IDEXX Prospectus)

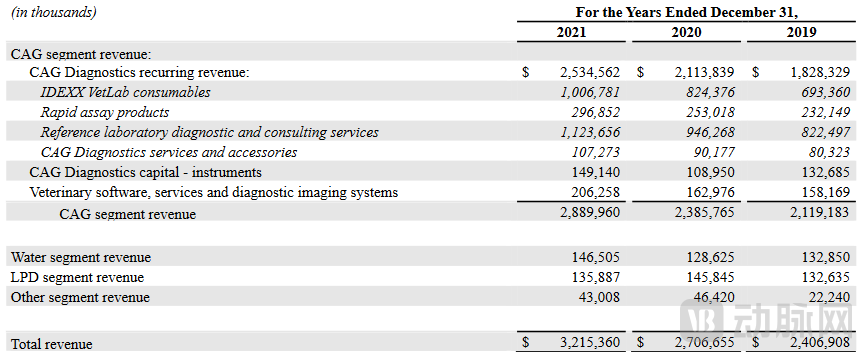

Two-thirds of IDEXX’s revenue comes from the sales of pet-related reagents and equipment, as well as rapid diagnostic and laboratory testing services. In the Chinese market, there is a significant gap between IDEXX’s pet biochemistry and immunoassay diagnostic reagents and domestically produced diagnostic reagents across various aspects.

In terms of the market, Idexx’s incremental revenue in recent years has come from developed regions rather than emerging markets. Its CAG Diagnostics Recurring Revenue, which is strongly correlated with pet diagnostics, grew rapidly due to the COVID-19 pandemic, reaching a growth rate of 20% in 2021.

IDEXX’s Revenue Distribution by Project, 2019–2021 (Source: IDEXX Prospectus)

IDEXX’s Revenue Distribution by Project, 2019–2021 (Source: IDEXX Prospectus)

Behind the data of these pioneers lie two key insights: first, China’s animal IVD market still has ample room for growth compared to developed countries; second, as with human medical devices, there is a path toward domestic substitution yet to be fully traversed.

Currently, the domestic IVD market in China is primarily composed of clinical chemistry and immunoassay diagnostic instruments and related consumables. Common test panels include clinical chemistry, liver function, renal function, coagulation, diabetes, electrolytes, and preoperative screening. The overall distribution is not significantly different from that of human medicine, with many products derived from adaptations of those used in human healthcare or animal experimentation.

However, due to the significant shortage of veterinary professionals in China, device developers must prioritize operational ease and strive to achieve automated detection as much as possible, even though the procedures are similar to those in human medicine. In this regard, most domestic devices have already implemented automated detection, simplifying operational analysis steps and enabling personnel without prior experience to master the workflow within minutes.

Beyond ease of use, the primary differences among IVD products from various companies lie in the number of test parameters and assay specificity. These instruments have low throughput requirements and modest demands for testing speed (although high-speed analyzers are theoretically superior to low-speed ones, animals in poor condition typically require hospitalization for observation in clinical practice). IDEXX’s high-end biochemistry analyzers can simultaneously detect 17 parameters, while the company has also launched an economical 10-parameter biochemistry product line. Currently, IVD products introduced by domestic companies in China mainly aim to meet basic needs.

However, due to the regulatory vacuum in the pet healthcare market and significant regional price disparities for medical services, pet owners are highly sensitive to the costs of medications, diagnostic reagents, imaging examinations, and other medical services. For instance, at a pet hospital in Hangzhou, the IDEXX premium 17-item biochemistry panel costs up to RMB 580, whereas a domestically produced biochemistry test costs only RMB 300. Given this price advantage, domestic in vitro diagnostics (IVD) can also carve out their own market niche.

Beneath the surface of apparent prosperity, dangers always lurk. For startups entering the animal IVD sector, risks stem primarily from the supply chain, followed by the business model.

To ensure diagnostic capabilities, hospitals need to achieve comprehensive test coverage; however, the diversity of pet species, examination items, and sample types results in a limited market size for any single product.

Many veterinary clinics are located in street-front retail spaces, where limited storage capacity makes it difficult to maintain large inventories. Companies must collaborate with distributors to develop effective rapid replenishment strategies, thereby controlling the logistics costs associated with small-batch, high-frequency restocking.

Another issue arising from limited testing volumes is the hindrance to corporate expansion. Without achieving economies of scale, it is difficult for a brand to break through regional constraints and expand nationwide; even the most successful domestic manufacturers can only exert influence at the provincial level.

In this context, manufacturers seeking to expand their sales scale nationwide must establish connections with leading regional distributors and set up separate sales channels in each province and city. As a result, the pace of corporate expansion is hindered, and marketing costs rise accordingly.

Before establishing a stable and continuous customer base, veterinary hospitals are generally unwilling to purchase IVD instruments at their own expense. Therefore, domestic manufacturers in China typically choose to place testing equipment directly in hospitals, generating revenue through the subsequent sale of reagents and consumables.

In such a market, the pet IVD industry has primarily given rise to two business models. The first involves partnering with distributors, delegating sales responsibilities to them, and relying on these distributors to deploy equipment in veterinary clinics. The second entails collaborating with corporate partners, where the partner bears the cost of equipment placement, enabling non-IVD companies to enter the market through OEM/ODM arrangements.

Under the OEM model, IVD companies enjoy faster capital turnover, allowing them to focus on product R&D and operate with an asset-light structure. If their products fail to gain market acceptance, the risks borne by the company remain relatively controllable, making this model particularly favorable for startups.

In contrast, the direct deployment of equipment in veterinary hospitals requires a substantial initial investment. With each unit costing between RMB 20,000 and 50,000, scaling up would likely necessitate millions of yuan in upfront sales expenditures.

For an emerging market like animal IVD, deploying a large number of instruments enables companies to capture market share early. As the volume of IVD testing in veterinary clinics reaches scale, these companies will generate recurring revenue, yielding higher profit margins than the previous model.

In the early stages of the market, no single approach holds an absolute advantage. Therefore, most startups adopt both business models in parallel, aiming to secure greater cash flow while maximizing revenue with minimal initial realization.

Since the outbreak of the COVID-19 pandemic, nucleic acid testing has been widely recognized as an effective method for detecting SARS-CoV-2. Today, the trend of molecular diagnostics is also sweeping into the animal in vitro diagnostics (IVD) sector, with companies such as Mindray Animal Medical, Qingdao Jiditai, Shanghai Jiling, and Cayudi actively entering and establishing their presence in this market.

There are two primary reasons for the surge of interest in molecular diagnostics for pets: First, antibody and antigen tests have a window period; they can only detect infections after clinical symptoms appear, typically during the middle to late stages of the disease. Furthermore, the clinical concordance rate of the commonly used colloidal gold technology caps at 70%. In contrast, molecular testing can detect pathogens in the early stages of infection and achieves a clinical concordance rate of up to 95%.

Secondly, IDEXX is currently promoting biochemical and immunoassay testing projects more vigorously in China, while its efforts in molecular diagnostics are relatively limited. For domestic enterprises, establishing a presence in molecular diagnostics presents a valuable opportunity to overtake competitors on the curve.

PCR fluorescence technology is currently the most classic and mature technique in nucleic acid testing, offering highly stable performance. However, to excel in animal IVD, efforts must extend beyond diagnostic technologies alone.

Conventional molecular diagnostic reagents typically require cold-chain transportation; however, for animal IVD products characterized by small-scale operations and dispersed demand, this model incurs high costs and poses a significant risk of reagent damage. To address this challenge, Qingdao Jiditai employs a combination of lyophilized microsphere technology and microfluidics, which substantially reduces logistics costs while ensuring the stability of reagent performance.

In terms of detection systems, taking Mindray Animal Medical’s Vetgenies 8 real-time fluorescence quantitative PCR instrument as an example, this device employs a nucleic acid extraction-free technology and offers testing for 25 types of pathogens, including viruses, bacteria, and parasites. It can diagnose respiratory, gastrointestinal, and systemic diseases, basically meeting the various IVD diagnostic needs currently received by veterinary hospitals.

Despite the rapid development of molecular diagnostics, Liu Sen, head of Qingdao Jiditai, believes that the core future application scenario for pet IVD lies within pet owners’ homes, transforming it into a home healthcare product. Currently, Qingdao Jiditai has completed the R&D of nucleic acid colorimetric detection technology and possesses China’s only lyophilized microsphere product.

According to Liu Sen, the entire set of GidiTech’s metal bath equipment is priced under RMB 1,000. If successfully promoted, it has the potential to significantly disrupt the existing animal IVD market.

Whether in medical imaging equipment or animal IVD, the current field of animal medical devices is largely in a regulatory vacuum under government oversight. There are no regulatory guidelines to constrain the safety and efficacy of products, nor are there standardized diagnostic pathways to regulate diagnoses conducted by pet hospitals.

Markets lacking checks and balances are inevitably prone to chaos.

Taking animal molecular diagnostics as an example, the development of combined testing is relatively lagging at this stage. The majority of companies’ diagnostic products focus on single-item tests, ruling out animal diseases one by one. In this context, veterinary hospitals are motivated to promote as many test kits as possible to patients in order to maximize profits.

For animal IVD companies, there is currently no effective shortcut to resolve the aforementioned issues; they can only strive to optimize their products and capture the market through word-of-mouth.

However, with the rapid development of the veterinary medical market, the arrival of regulatory regulations and industry standards is only a matter of time.

Therefore, animal IVD companies must also prepare for future development. By standardizing products and initiating clinical trials early on, they can obtain regulatory approvals as soon as new regulations are implemented, thereby capturing a larger market share.