Domestic Players Accelerate Import Substitution in China's Emerging Sports Medicine Market

Editor’s Note: This article is from Yunhu Consulting and has been republished with permission by VCBeat.

As public emphasis on sports and health continues to grow, potential market demand in sports medicine is steadily increasing. Against the backdrop of the inclusion of orthopedic devices in centralized volume-based procurement (VBP), original profit margins for orthopedic manufacturers have declined, prompting them to seek transformation opportunities. As the only segment of orthopedic devices not yet included in VBP, sports medicine has emerged as a popular choice. Driven by both demand-side and supply-side factors, sports medicine has become the fastest-growing subsector within orthopedics. With the wider adoption of sports medicine procedures across more hospitals and cities, it is expected to maintain robust growth in the future.

In addition to its high growth rate, another defining characteristic of the sports medicine sector is import monopoly. In 2017, domestically produced products accounted for less than 2% of China’s sports medicine market, indicating substantial potential for import substitution. Currently, domestic companies such as Demei Medical, Tianxing Medical, and Kailitai have all established footholds in specific segments of the sports medicine field. The combination of rapid growth and broad opportunities for import substitution has generated significant optimism within the orthopedics industry and investment community regarding the prospects of sports medicine. In recent years, the sports medicine sector has gained considerable momentum, with active financing, investment, and merger and acquisition activities. Industrial funds and venture capital firms continue to increase their investments in this sector, aiming to identify high-quality targets in China’s future sports medicine market.

This article draws on publicly available online information and interviews with industry experts to analyze the potential of niche segments within China’s sports medicine sector and the companies involved, sharing our research findings for industry reference.

I.Overview of Sports Medicine

1. Overview of Sports Medicine

2. Sports Medicine Industry Chain

3. Macro-Policy Orientation in Sports Medicine

4. Impact of Centralized Procurement on High-Value Consumables in Sports Medicine

II. Competitive Landscape of Major Medical Devices

1. Overall Competitive Landscape

2. Equipment - Arthroscopic Surgical System

3. Consumables - Knee Joint (Ligament Area) - Interference Screw

4. Consumables - Knee Joint (Ligament Area) - Button Plate with Loop

5. Consumables - Knee Joint (Ligament Area) - Artificial Ligament

6. Consumables - Knee Joint (Meniscus Region) - Meniscus Repair System

7. Consumables - Shoulder Joint - Suture Anchors

III. Leading Companies in Sports Medicine

1. Product Lines of Leading Companies and Their Market Entry Strategies in Sports Medicine

2. Domestic Investment and Financing Events

I. Overview of the Sports Medicine Industry

1. Overview of Sports Medicine

1) Basic Concepts

Sports medicine is a comprehensive, multidisciplinary medical field that integrates basic and clinical sciences with athletic activities. It primarily focuses on the diagnosis and treatment of injuries to bones, joints, muscles, tendons, ligaments, cartilage, synovium, and other structures that are either related to or affect physical performance. This specialty is closely intertwined with orthopedics, rehabilitation medicine, kinesiology, materials science, biomechanics, and endoscopic minimally invasive techniques.

Sports medicine originated from orthopedics but focuses more on sports-related injuries. It differs from general traumatic orthopedics in terms of incidence patterns, diagnostic and therapeutic principles, and prognosis. To better manage sports injuries, sports medicine has branched off from orthopedics. Currently, at major Grade A tertiary hospitals such as Ruijin Hospital Affiliated to Shanghai Jiao Tong University School of Medicine, Shanghai Sixth People’s Hospital, and Peking University Third Hospital, the annual volume of sports medicine surgeries has reached 300–500 cases. Sports medicine is gradually separating from orthopedics to become a specialized department.

2) Development History

In 1955, sports medicine departments were successively established in physical education institutes and medical colleges across China, marking the beginning of the development of sports medicine in the country.

In 1978, the Chinese Society of Sports Medicine was established and joined the International Federation of Sports Medicine in 1980.

In 2007, with the successful bid for and subsequent preparations of the Beijing Olympic Games, the Sports Medicine Branch of the Chinese Medical Association was officially established.

In 2019, the Sports Medicine Physicians Branch of the Chinese Medical Doctor Association was established in Beijing. Subsequently, sports medicine organizations under medical associations and physician associations across various regions were successively founded, promoting the comprehensive and rapid development of sports medicine throughout China.

In 2020, major Grade A tertiary hospitals such as Ruijin Hospital, Shanghai Sixth People’s Hospital, and Beijing Third Hospital separated sports medicine from orthopedics into an independent department. Hospitals performing more than 300 surgeries annually are also considering establishing standalone sports medicine departments, while specialists in joints, trauma, and other fields have begun to practice sports medicine.

3) Market Size

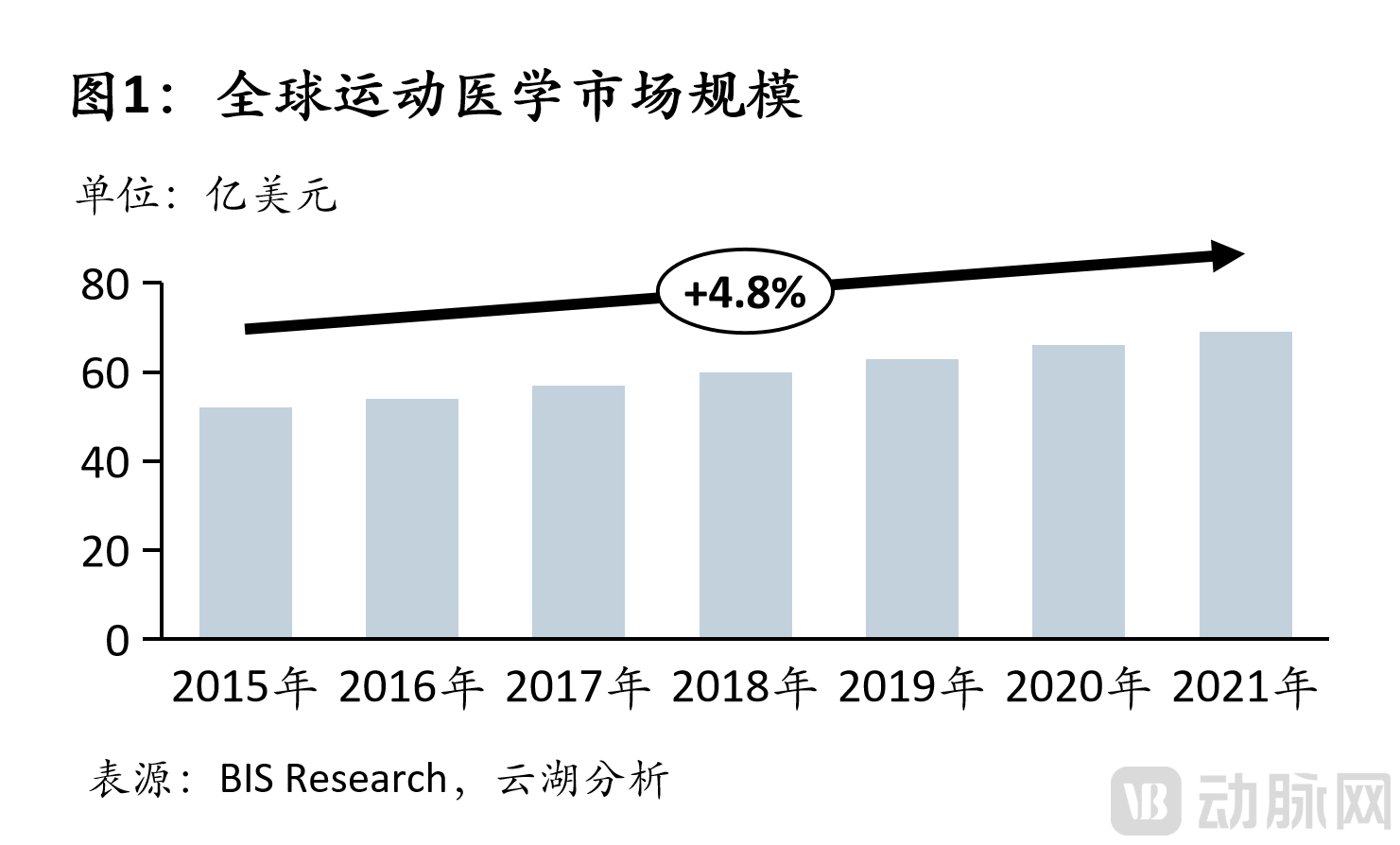

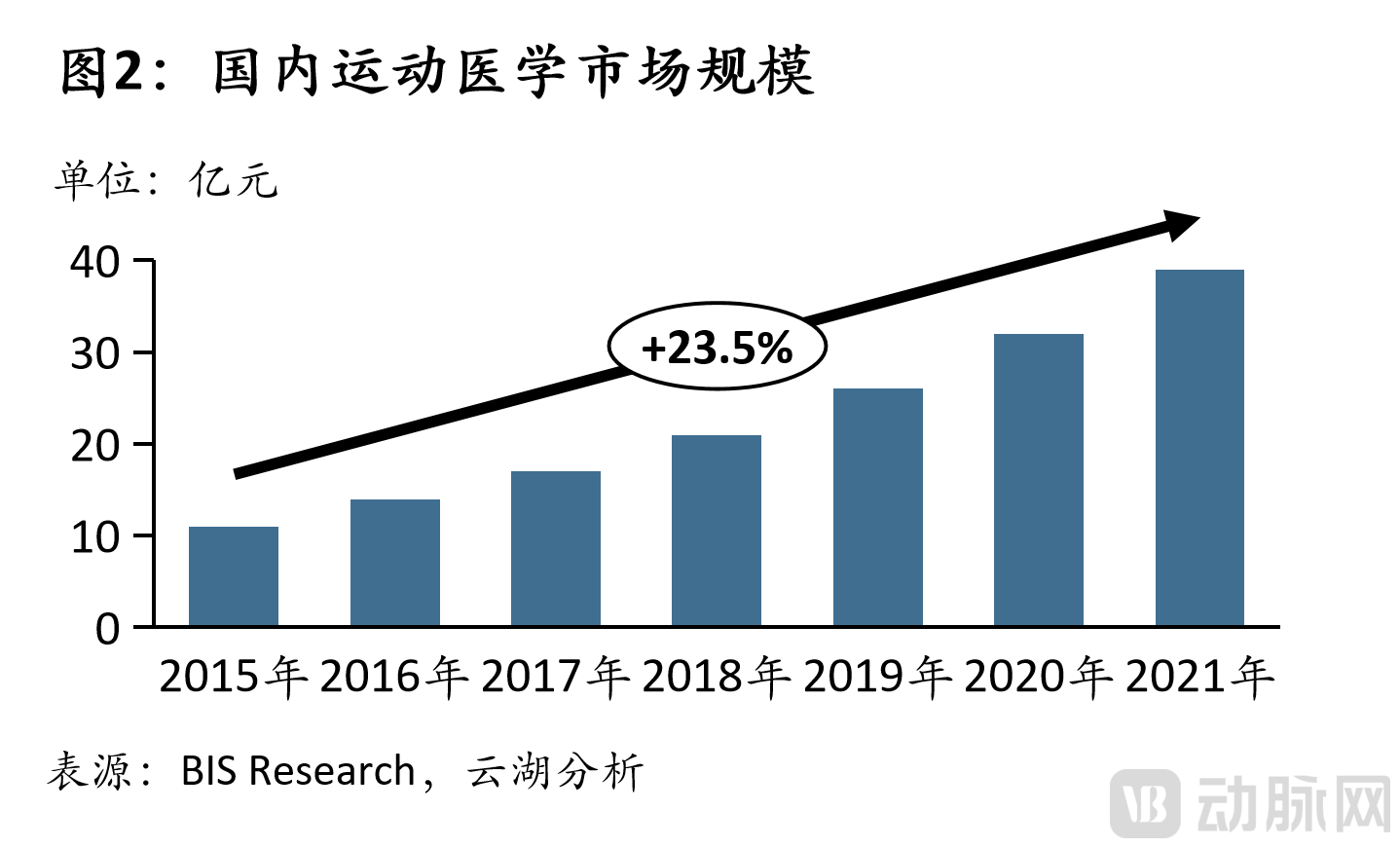

In 2021, the global sports medicine market was estimated at approximately USD 7 billion, demonstrating steady overall growth with a compound annual growth rate (CAGR) of 4.8% compared to 2015. Although China’s sports medicine market started later and remains smaller in scale, it has experienced rapid growth. In 2021, the size of China’s sports medicine market was approximately RMB 4 billion, with a CAGR exceeding 23%.

2. Sports Medicine Industry Chain

From the perspective of the industrial chain, the upstream of the sports medicine industry consists of raw material suppliers, the midstream comprises manufacturers of sports medicine products and consumables, and the downstream primarily includes distributors of sports medicine products and end-user hospitals.

1) Upstream: This segment includes implantable and non-implantable consumables, with manufacturing processes serving as the core competitiveness of upstream manufacturers.

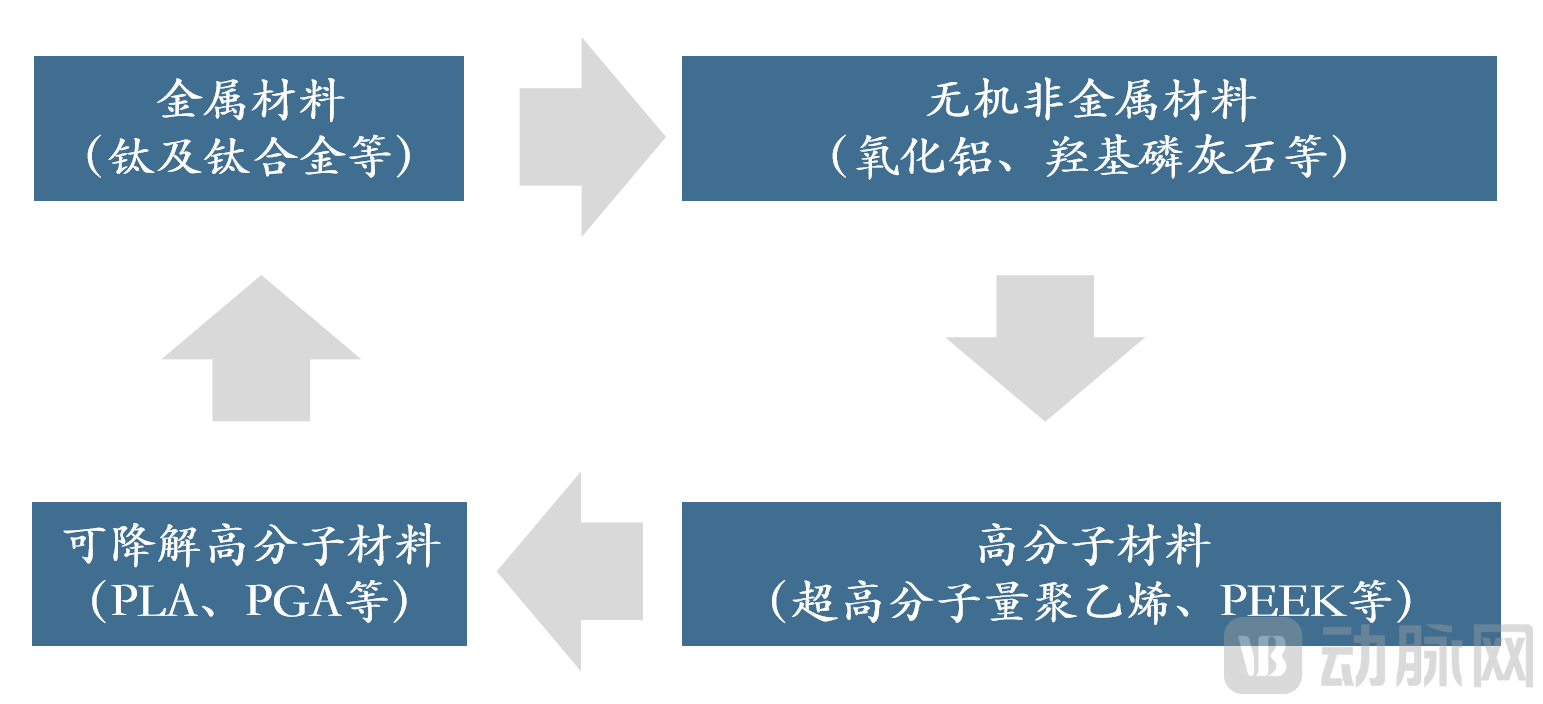

Implantable consumables have stringent requirements for strength, biocompatibility, processability, mechanical compatibility, and wear resistance. Clinically used implantable consumables have evolved from metals to inorganic non-metals, polymers, and degradable polymers, with material iterations continuing. As materials evolve, their prices gradually increase, while the number of available suppliers decreases. Implantable consumables demand high product safety; currently, there are few high-quality domestic raw material suppliers in China, and core critical materials remain predominantly imported. Taking PEEK material as an example, its upstream materials are expensive, and the domestic market is still monopolized by importers such as Victrex, giving upstream suppliers strong bargaining power.

2) Midstream: Medical device suppliers, with high-value consumables monopolized by overseas medical device manufacturers.

Among clinically used medical devices, arthroscopy systems serve as foundational equipment, while suture anchors, interference screws, button plates, and artificial ligaments are the primary implantable consumables. As the domestic sports medicine sector started relatively late, most manufacturers are still in the phase of product line development. Currently, the market is dominated by imported brands such as Smith & Nephew, Johnson & Johnson, Stryker, and Arthrex, but a trend toward substitution with domestically produced alternatives is evident. Given the large number of midstream manufacturers and the anticipated launch of commercially available domestic products in the future, the following section will focus on leading manufacturers that have already obtained relevant sports medicine qualifications in China.

3) Downstream: pharmaceutical and medical device distributors and end-user hospitals, with cost reduction and efficiency enhancement serving as the core competitiveness in the distribution segment.

Orthopedic products are relatively complex, with a wide variety of types and models, and clinicians typically have diverse needs; therefore, the distribution model currently dominates the industry. Due to the high concentration in the pharmaceutical and medical device distribution sector, the “Two-Invoice System” in the field of high-value consumables is still in its early stages compared to pharmaceuticals. As policies such as the Two-Invoice System and centralized procurement of medical devices are gradually implemented, the ability of pharmaceutical and medical device distributors to reduce costs and improve efficiency will determine their competitive advantage.

3. Macro Policy Orientation in Sports Medicine

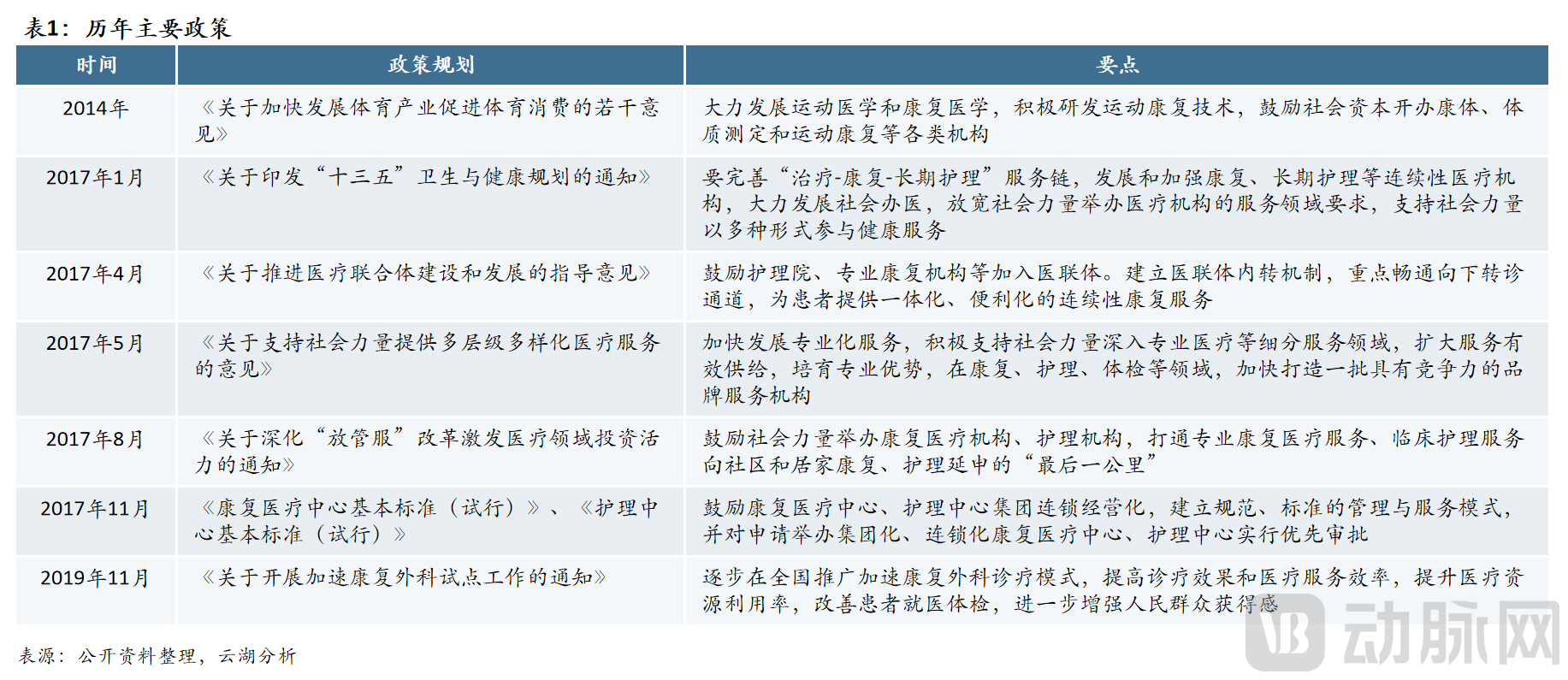

As early as 2014, the “Several Opinions on Accelerating the Development of the Sports Industry and Promoting Sports Consumption” already highlighted sports rehabilitation as a key priority: “Vigorously develop sports medicine and rehabilitation medicine, actively research and develop sports rehabilitation technologies, and encourage social capital to establish various institutions such as fitness-rehabilitation centers, physical fitness assessment facilities, and sports rehabilitation clinics.”

In recent years, relevant authorities have successively introduced policies to vigorously support the development of the sports rehabilitation industry, encouraging the establishment of group-based and chain-operated rehabilitation medical centers and nursing centers, with the aim of comprehensively building an integrated rehabilitation service chain encompassing “treatment–rehabilitation–long-term care.”

However, as the industry remains in its early stages, China’s medical insurance policies for sports rehabilitation are still underdeveloped. With only a limited number of services covered by medical insurance, patients primarily bear out-of-pocket costs. These high treatment expenses have, to some extent, suppressed patient demand and constrained market growth.

Overall, China maintains a stance of “strong encouragement” toward the development of the sports rehabilitation industry. In the future, as the medical insurance policy framework continues to improve and patient out-of-pocket costs decline, latent demand will be gradually unleashed, driving rapid growth in China’s sports rehabilitation sector.

4. Impact of Centralized Procurement on High-Value Consumables in Sports Medicine

In accordance with the main objectives for the development of national healthcare security during the 14th Five-Year Plan period, by 2025, each province will have included more than five categories of high-value medical consumables in centralized procurement (including both national and provincial volume-based procurement). On January 14, 2020, the General Office of the National Health Commission issued the “Notice on the First Batch of Key Governance List for High-Value Medical Consumables.” Among the initial 18 listed items, orthopedic and cardiovascular interventional consumables accounted for a significant proportion, becoming two key categories under intensified monitoring. By 2021, large-scale centralized procurement of high-value medical consumables in China had covered nine major fields, with artificial joints and spinal implants being the key categories within orthopedics. Overall, volume-based procurement has demonstrated steady progress, characterized by an increasing number of included products, continuously refined procurement rules, and expanding geographic coverage.

As a subspecialty of orthopedics, sports medicine currently has a relatively small overall market demand and a low rate of localization, thus facing less pressure from centralized procurement. However, with the intensification of centralized procurement in orthopedics and the continuous improvement in the localization rate of related consumables, it is expected that sports medicine-related consumables will gradually be affected by centralized procurement within the next 2–3 years, with early signs already evident. For instance, in April 2021, six cities in Jiangsu Province included suture anchors in their centralized procurement lists; in November 2021, Luoyang City in Henan Province also brought suture anchors under the scope of centralized procurement. It can therefore be inferred that future centralized procurement in sports medicine will begin with high-volume basic implantable consumables, such as anchors, sutures, and titanium plates.

II. Competitive Landscape of Major Medical Devices

1. Overall Competitive Landscape

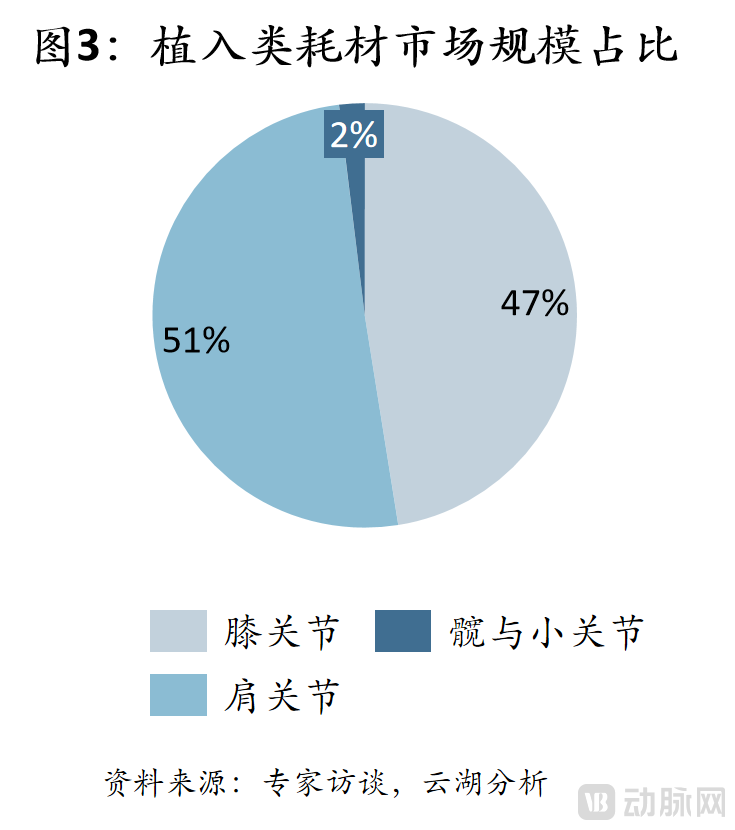

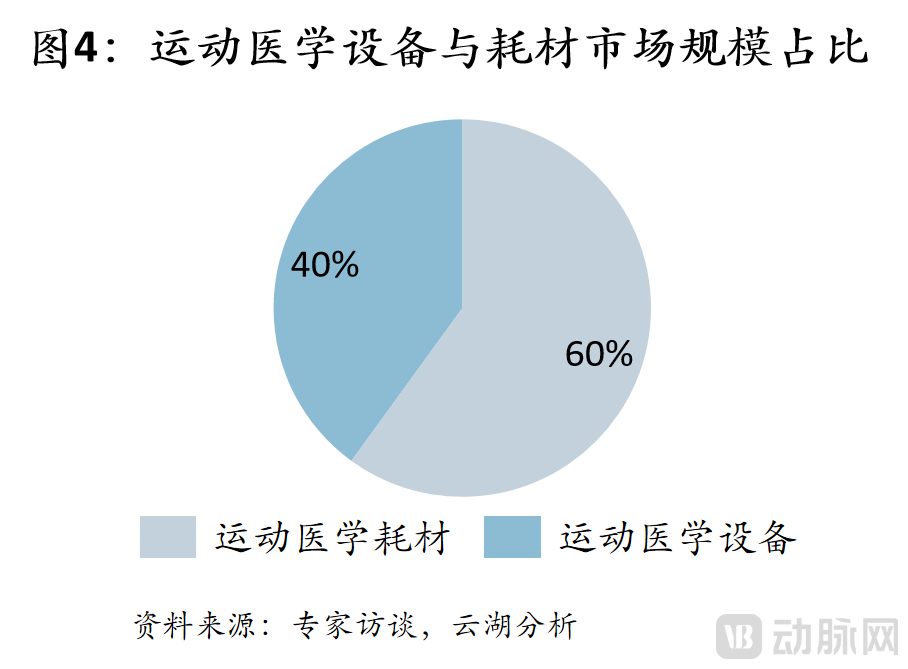

Sports medicine surgeries are primarily categorized by the site of injury into knee, shoulder, hip, and other small joints. Implants used in knee and shoulder procedures account for approximately 98% of the sports medicine market, making them the dominant procedures in this field. Knee surgeries mainly include anterior cruciate ligament (ACL) reconstruction and meniscus repair, while shoulder surgeries primarily focus on rotator cuff and labral tear repairs. Medical devices required for sports medicine surgeries are divided into equipment and consumables. Equipment, primarily arthroscopic surgery systems, constitutes about 40% of the overall market, while the remaining 60% comprises medical consumables such as suture anchors, interference screws, and titanium plates with buttons.

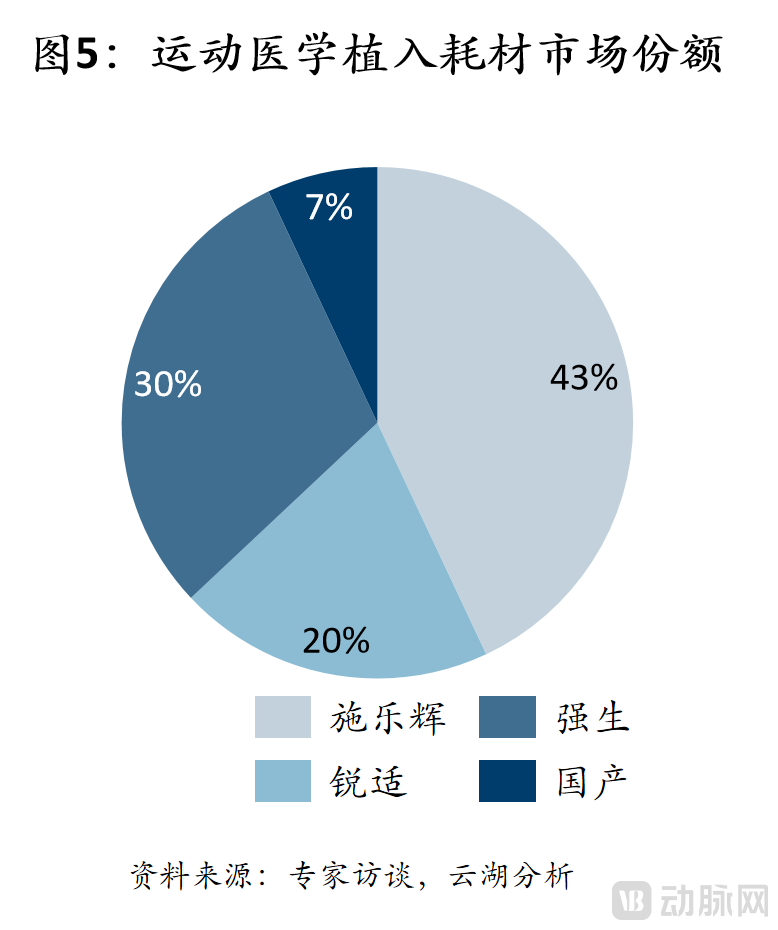

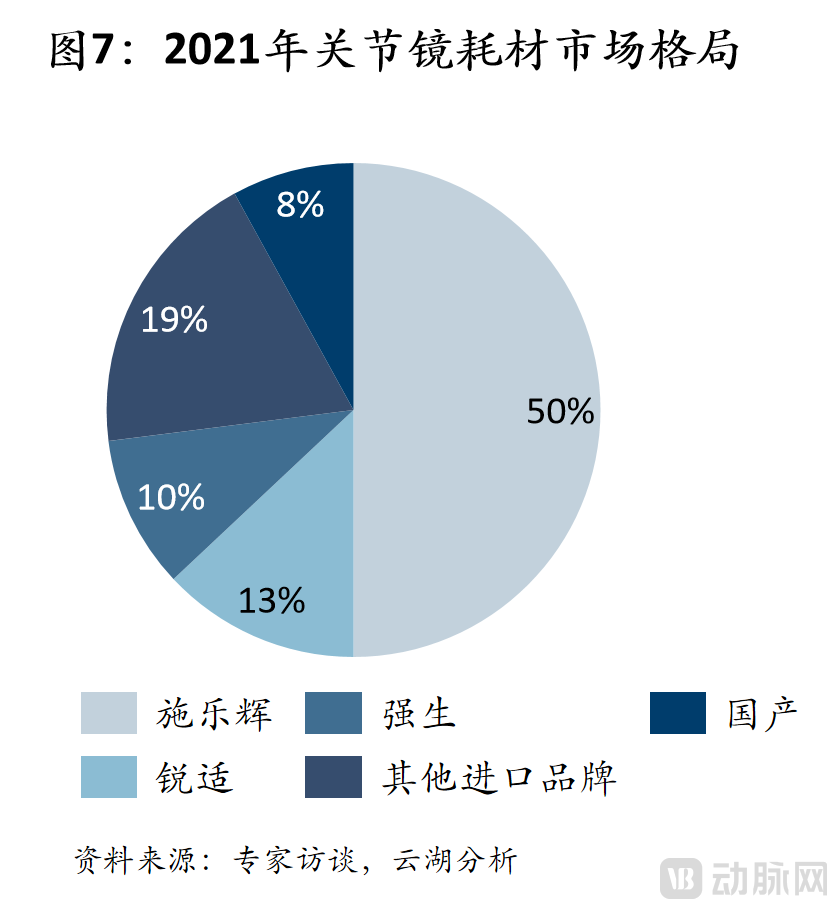

Despite the rapid development of China’s sports medicine market, the sector remains dominated by major international manufacturers such as Smith & Nephew, Johnson & Johnson, and Arthrex, owing to their longer development histories and superior product performance. Currently, Chinese domestic manufacturers hold only about 7% of the market share. Compared with imported brands, domestic companies have developed more slowly due to technical barriers, challenges in product research and development (R&D), and insufficient market insight. Notably, because sports medicine consumables are less technically challenging to develop than equipment and account for a substantial 60% of the market, many Chinese manufacturers new to the sports medicine field have entered the market by focusing on consumable products.

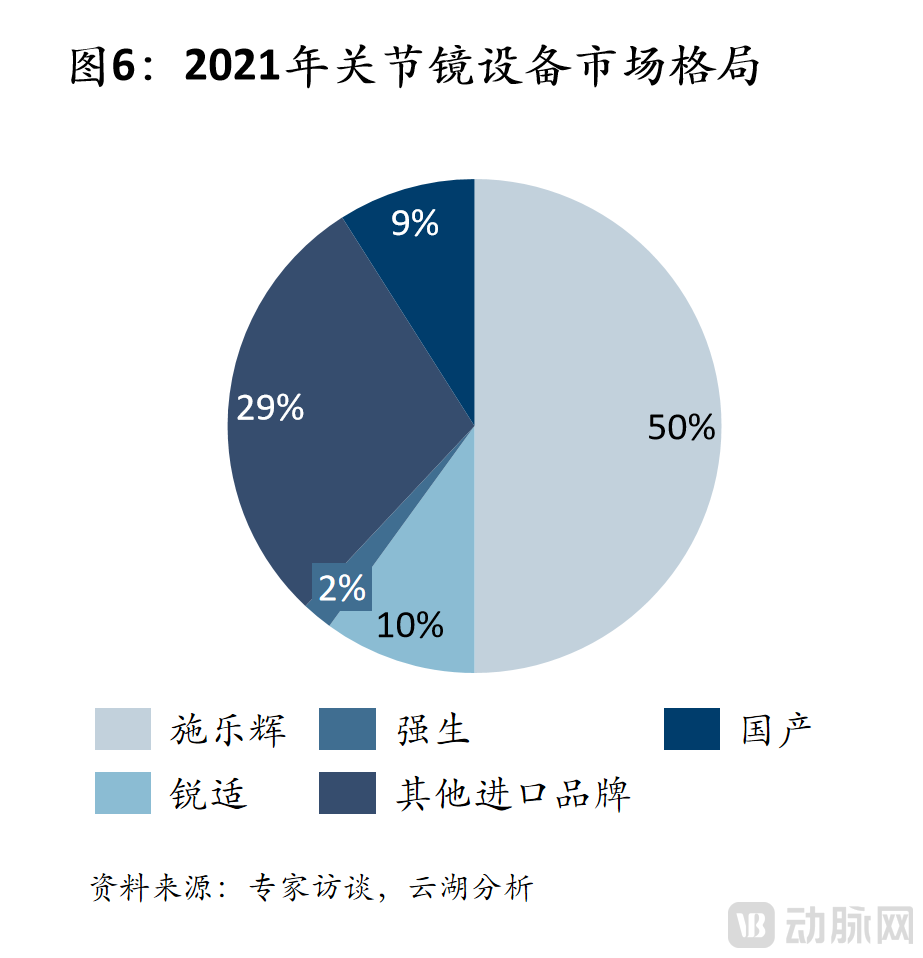

Sports medicine equipment primarily includes arthroscopic surgical systems and arthroscopic surgical consumables. Similar to the consumables market, the arthroscopic equipment and consumables sectors are dominated by imported brands. In 2021, Smith & Nephew held a market share of over 50%, followed by Arthrex, Johnson & Johnson, and other imported brands, while domestically produced brands accounted for less than 10% of the market.

This report will provide a segment-by-segment analysis based on the classification of sports medicine devices and consumables, with a primary focus on consumables required for knee and shoulder surgical procedures.

2. Equipment - Arthroscopic Surgery System

1) Arthroscopic Equipment

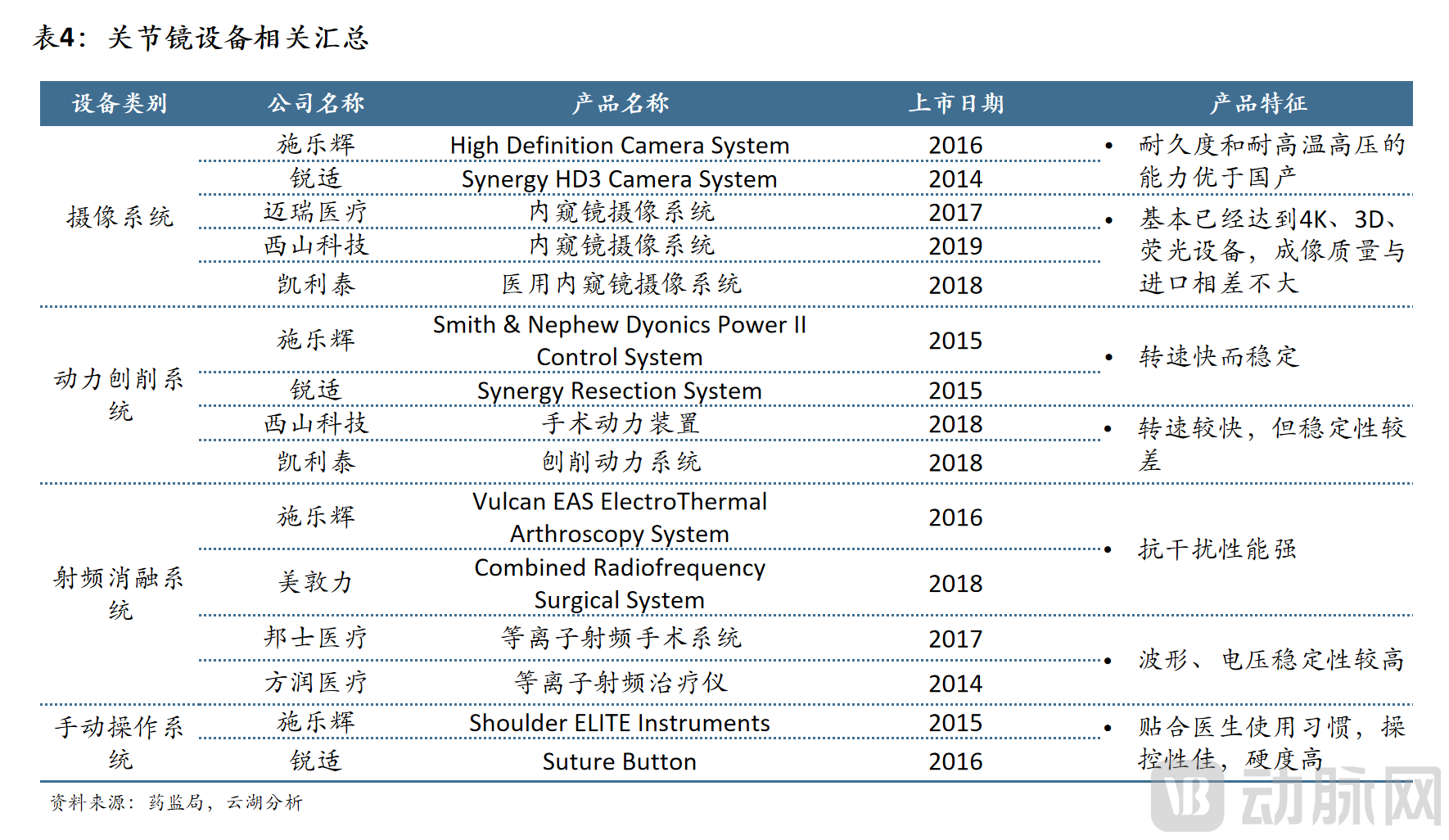

Arthroscopy systems primarily consist of digital imaging systems, xenon cold light sources, arthroscopes, motorized shaver systems, irrigation and infusion systems, plasma radiofrequency ablation units, surgical instruments, image processing systems, and surgical support stands. Due to the specialized nature of the various components and the high R&D costs involved, currently only two imported manufacturers, Smith & Nephew and Arthrex, are capable of providing complete, integrated arthroscopy systems. Domestic manufacturers remain relatively weak in offering comprehensive solutions; while some companies are developing single-function products such as cameras, motorized shavers, or plasma units, others have formed partnerships with equipment suppliers. It is common in the industry for motorized device companies to purchase imaging equipment from other manufacturers and rebrand it for sale. Although domestic manufacturers such as Kinetic Medical, Demei, and Tianxing claim to offer total solutions, industry insiders reveal that there are currently no Chinese manufacturers with fully self-developed, complete equipment suites; most operate under a rebranding and partnership sales model.

Among arthroscopy camera systems, domestic manufacturers such as Mindray Medical and Kailitai have launched devices with 4K resolution. Their imaging quality shows no significant gap compared to imported brands; however, they are slightly inferior in terms of durability and resistance to high temperature and pressure, with notable differences in image fineness and anti-reflection performance. In the field of power systems, Chinese manufacturer Xishan Technology has advanced rapidly, with its products demonstrating strong performance in key indicators such as rotational speed. Regarding radiofrequency (RF) systems, Gyrus and Smith & Nephew collectively hold over 50% of the market share. Gyrus was acquired by Smith & Nephew in 2014, after which Smith & Nephew’s product portfolio encompassed both plasma ablation and low-temperature vaporization technologies. Domestic manufacturer Fangrun Medical employs plasma ablation technology in its devices, offering superior waveform and voltage stability. The manual operation system segment is currently monopolized by imported brands, with no large-scale domestic manufacturers having emerged yet.

2) Arthroscopic Consumables

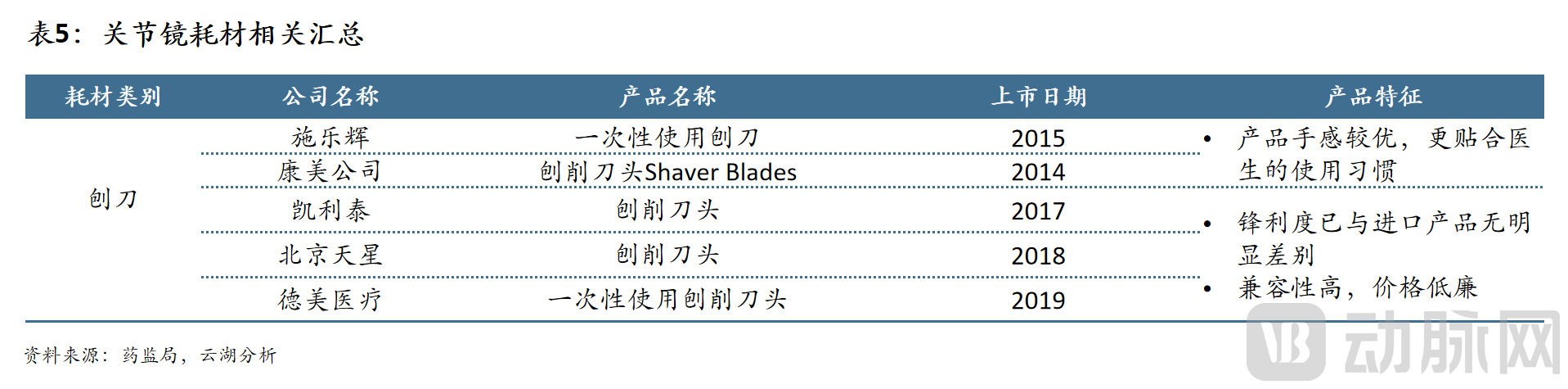

Arthroscopy consumables primarily consist of disposable shavers used in arthroscopic surgeries. Although imported brands still hold a monopolistic position in the market share of arthroscopy consumables, domestic substitution is gradually emerging. Having entered the sports medicine field earlier and achieved high equipment installation rates, imported manufacturers have established strong hospital networks that are difficult for domestic companies to displace. However, by developing consumables compatible with equipment from various imported brands, domestic manufacturers can capture market share from these incumbents and expand their own market presence. Due to the varying designs and high prices of shaver heads from imported brands, domestic manufacturers have rapidly grown by entering the market with product lines compatible with multiple imported systems and offering high cost-performance ratios. Currently, there is no significant difference in sharpness between domestic and imported shaver heads, but further improvements are needed in aspects such as product structure, maneuverability, and tactile feedback.

3) Future Development Trends

① Influenced by future bidding policies, domestic brands are more flexible and can accelerate the pace of import substitution through cross-selling and collaborative development of comprehensive solutions.

② Arthroscopic blade consumables are currently on the list for potential centralized procurement, with a certain possibility of being included in future centralized procurement programs.

③ Against the backdrop of centralized procurement for medical consumables, more manufacturers are expected to focus on equipment R&D to develop comprehensive arthroscopic surgical systems. As new players enter the market, intensified competition may further drive down the prices of arthroscopic devices.

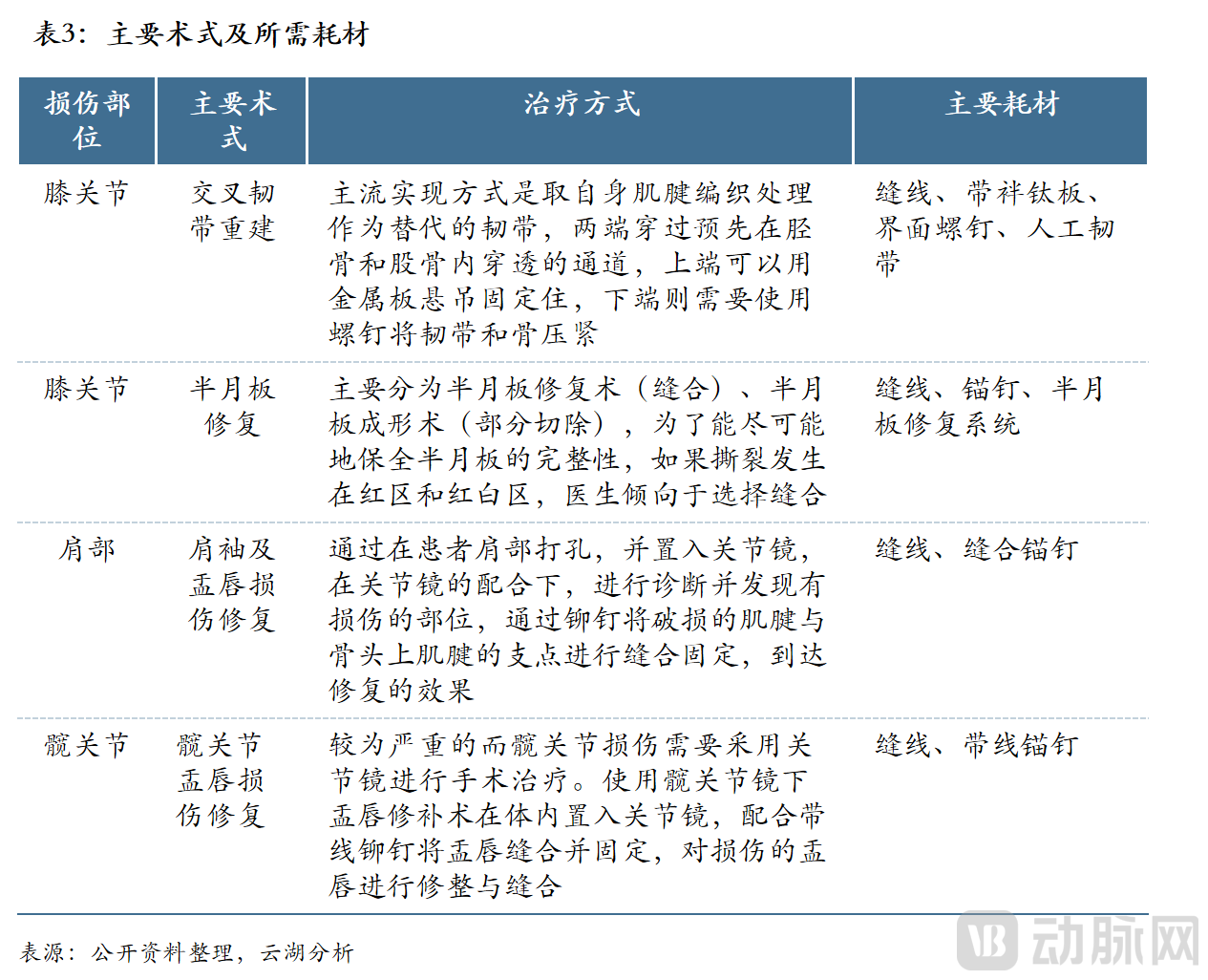

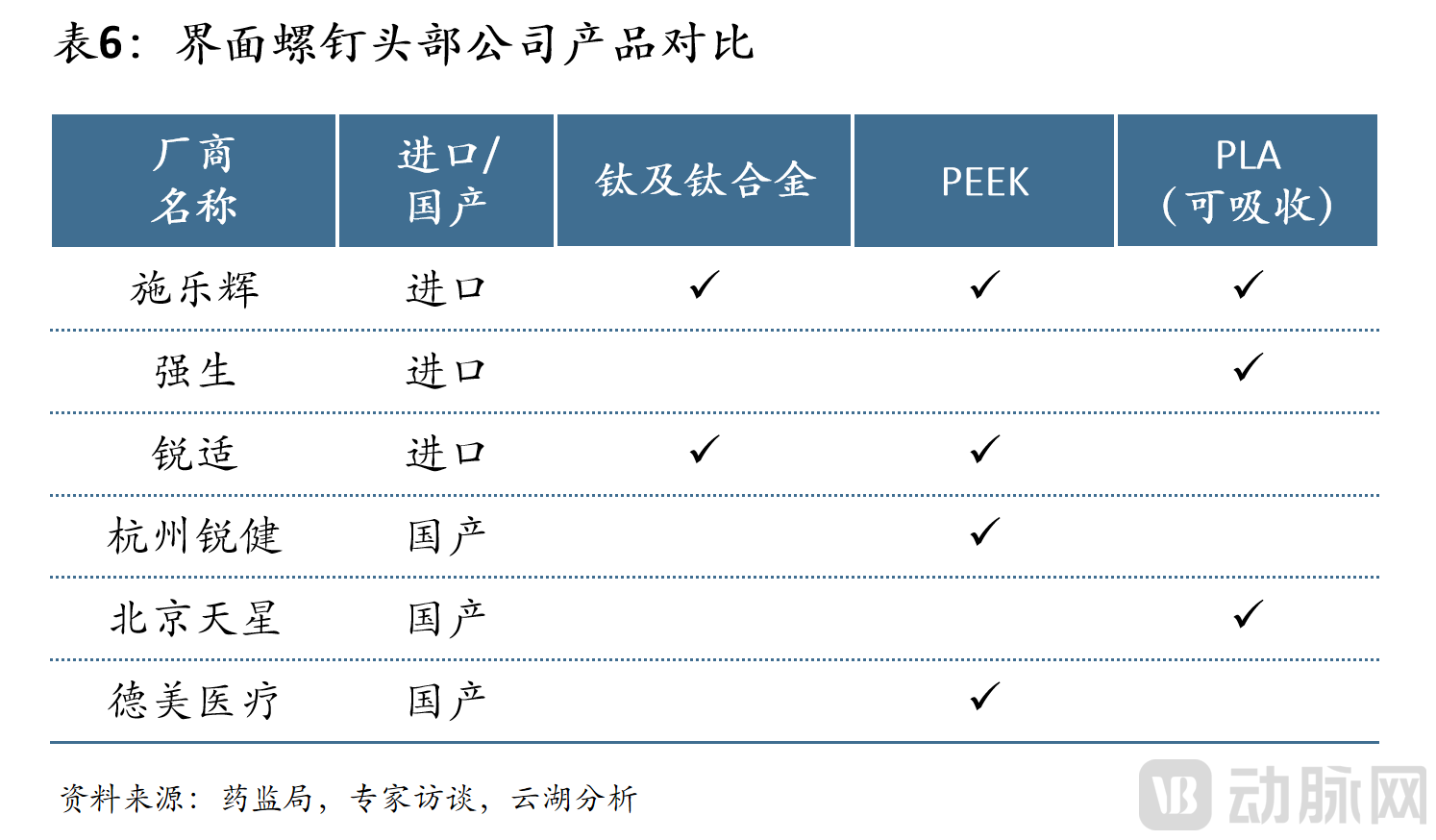

3. Consumables - Knee Joint (Ligament Area) - Interference Screw

1) Product Overview

Interference screws are commonly used consumables in knee ligament surgery, primarily serving as compression screws at the proximal femoral end. Currently, three main materials are available: metal, PEEK, and bioabsorbable materials. Among these, PEEK has replaced metal as the mainstream material. Bioabsorbable materials are less frequently used in clinical practice due to their low mechanical strength, which poses risks such as loosening and inflammation.

2) Product Comparison of Leading Companies

The domestic market for interference screws is currently dominated by imported brands, with mainstream large tertiary hospitals primarily using imported products. Key manufacturers include Smith & Nephew, Arthrex, and Johnson & Johnson, while leading domestic manufacturers include Ruijian Medical, Beijing Tianxing, and Demei Medical. Currently, there is no significant difference between domestic and imported products in terms of performance and quality. Regarding pricing, as domestic products were introduced later, their hospital listing prices are slightly higher than those of imported products in some regions; however, there is no significant difference in their ex-factory prices.

3) Future Development Trends

① The knee joint is a key surgical site in the field of sports medicine, with substantial demand for interference screw fixation at the proximal femoral end. Currently, domestic and imported manufacturers have achieved comparable levels of production technology; therefore, domestic manufacturers typically enter the market through knee implant consumables. With continuous product iterations by domestic manufacturers, interference screws are now among the implantable consumables exhibiting the most pronounced trend of import substitution in China.

② At present, interference screws are not affected by the centralized procurement policy. However, with the continuous increase in the localization rate and the gradual expansion of market share for domestically produced products, it is possible that they may be included in the centralized procurement list in the future, as they are one of the main consumables used in knee joint surgeries.

4. Consumables - Knee Joint (Ligament Area) - Loop Titanium Plate

1) Product Overview

Button plates are used in orthopedic reconstruction surgery to fix tendons and ligaments. The product consists of a metal plate with standard dimensions of 4mm x 12mm, paired with sutures. Clinically, they are commonly used for femoral-side fixation in anterior cruciate ligament (ACL) reconstruction of the knee, and are also utilized in surgeries such as acromioclavicular joint dislocation repair and distal tibiofibular syndesmosis stabilization. Depending on the product type, button plates are generally classified into fixed-loop and adjustable-loop types. Fixed-loop refers to those where the length and diameter of the suture loop in the center of the titanium plate are predetermined and unchangeable, while adjustable-loop allows the surgeon to tighten or shorten the central suture loop intraoperatively. Sutures in fixed-loop button plates are typically either braided or non-braided, whereas those in adjustable-loop button plates are usually of a wrapped design. These differ from the sutures used in suture anchors, and there are also notable differences between the central suture loop and the pull-through sutures at both ends in terms of thickness, material, and manufacturing process.

Fixed loop titanium plates require the surgeon to calculate the depth and diameter of bone tunnels based on actual needs during surgery, whereas adjustable loop titanium plates allow direct drilling of bone tunnels without the need for calculations, thereby reducing surgical difficulty. Additionally, adjustable loop titanium plates enable a greater volume of graft material within the bone tunnel, which is more beneficial for postoperative recovery; however, fixed loop titanium plates offer superior advantages in terms of fixation length.

2) Comparison of Products from Leading Companies

Currently, the market is dominated by imported manufacturers, primarily including Smith & Nephew, Johnson & Johnson, and Arthrex. The fixed-loop titanium plate was first introduced by Smith & Nephew in the 1990s and is regarded as the “gold standard” for femoral-side fixation within the industry. Subsequently, Johnson & Johnson’s launch of adjustable-loop titanium plates captured a portion of the market share previously held by Smith & Nephew’s fixed-loop products. Currently, both companies offer both fixed and adjustable product lines. Domestic manufacturers are mainly represented by Ruijian Medical, Beijing Tianxing, and Demei Medical. The first products launched by these manufacturers are typically designed for anterior cruciate ligament (ACL) reconstruction surgeries of the knee, which have high procedural volumes. Additionally, each manufacturer decides whether to introduce fixed or adjustable loop titanium plates based on its own resources.

Whether from imported or domestic manufacturers, the material and dimensions of metal plates are essentially identical; the primary difference between products lies in suture strength, with tensile strength being the main consideration for surgeons.

In terms of product pricing, adjustable loop titanium plates generally cost between RMB 12,000 and 13,000, while fixed loop titanium plates are typically priced below RMB 10,000. Overall, there is no significant price difference between domestically manufactured products and those from imported brands, with some domestic products even priced higher than their imported counterparts.

3) Future Development Trends

① Since some manufacturers outsource the procurement of sutures, certain domestic companies in China may focus on developing suture manufacturing in the future.

② The application of loop titanium plates in the knee joint is currently relatively mature, but their use in certain surgical procedures for the shoulder and ankle joints remains limited. As these specific procedures gradually gain market acceptance, demand is expected to increase.

③ Since domestic manufacturers currently focus primarily on knee joint products and the R&D barriers for titanium plates are not high, the trend of domestic substitution will gradually begin with anterior cruciate ligament (ACL) reconstruction surgery of the knee.

5. Consumables - Knee Joint (Ligament Area) - Artificial Ligament

1) Product Overview

In the field of sports medicine, anterior cruciate ligament (ACL) injury is one of the common knee joint disorders. Arthroscopic ACL reconstruction can restore motor function through ligament reconstruction. The ligament materials used in surgery can be divided into three types: autografts, allografts, and artificial ligaments. Currently, autografts are the mainstream treatment method in China, with an estimated market share of nearly 90%, according to industry experts.

Autologous ligaments are harvested from the patient’s own tissues, offering excellent biocompatibility and eliminating concerns regarding immune rejection or disease transmission. For patients with sufficient autologous tendons, this is currently the preferred treatment option; however, vigorous exercise is contraindicated in the immediate postoperative period, a recovery period of up to one year is required, and the expected level of functional activity after reconstruction is relatively modest.

Allogeneic ligaments are harvested from cadavers, and currently, only a few domestic companies, such as Beijing Yunkang, have been approved to supply them. Although allogeneic ligament products themselves have a high safety profile, their scarcity drives prices higher than those of autologous ligaments. Patients still require a recovery period of six months to one year, and there are potential risks such as rejection reactions.

Artificial ligaments are non-absorbable implantable consumables whose internal structure resembles that of normal human ligament fibers. Artificial ligaments typically require only about three months for recovery, but their penetration rate in China is far lower than that of autologous ligaments, mainly due to the following reasons: ①The price is on the high side., excluding medical insurance coverage, the cost of artificial ligaments exceeds RMB 30,000, whereas the expense for autologous ligaments can be reduced to RMB 10,000–20,000. Currently, in clinical practice, artificial ligaments are primarily recommended for patients who have a strong need for early rehabilitation and possess higher payment capacity; ②Insufficient Market Education and Promotion;③High technical proficiency is required of clinicians., therefore, the use of artificial ligaments is still limited to large tertiary hospitals at this stage, with a lower penetration rate compared to other consumables such as sutures and anchors.

2) Comparison of Leading Companies

As early as October 2003, LARS obtained the Medical Device Registration Certificate issued by the National Medical Products Administration (NMPA). Since its entry into the Chinese market, LARS products have consistently maintained a leading position in terms of product technology. From 2003 to 2007, Cosmo served as the registered agent for LARS. In 2013, the domestic agency for LARS was changed to Wanjie Tianyuan, and in 2016, the domestic registration agent for LARS was changed to Jietong Kangnuo.

Given the substantial profit margins associated with artificial ligaments, multiple companies in China—including device manufacturers such as Ligament and distributors like Wanjie Tianyuan—are accelerating the research and development (R&D) of artificial ligament products. As artificial ligaments impose specific requirements on suture properties such as strength, tensile force, toughness, and durability, as well as on weaving techniques and cleaning processes, most domestic players currently involved in this field are leading implantable consumables manufacturers in the sports medicine sector. It is understood that Ligament’s artificial ligament product has completed clinical trials, making it the fastest-moving company in terms of R&D progress in China. Upon successful product development, it is expected to gain a pricing advantage.

3) Future Development Trends

① Influenced by multiple factors, including pricing and market education, the volume of artificial ligament usage has consistently lagged significantly behind that of autologous ligaments. Looking ahead, as sports participation becomes more widespread and market education deepens, the use of artificial ligaments is expected to continue rising. On the other hand, if domestically commercialized products achieve success in China, competition within the artificial ligament sector will intensify. Price competition will benefit patients and may further promote the clinical adoption of artificial ligaments.

② Currently, no domestically developed artificial ligament products are on the market in China; whether the overall domestic sales volume of artificial ligaments can fully meet the expectations of centralized procurement in the short term remains to be seen.

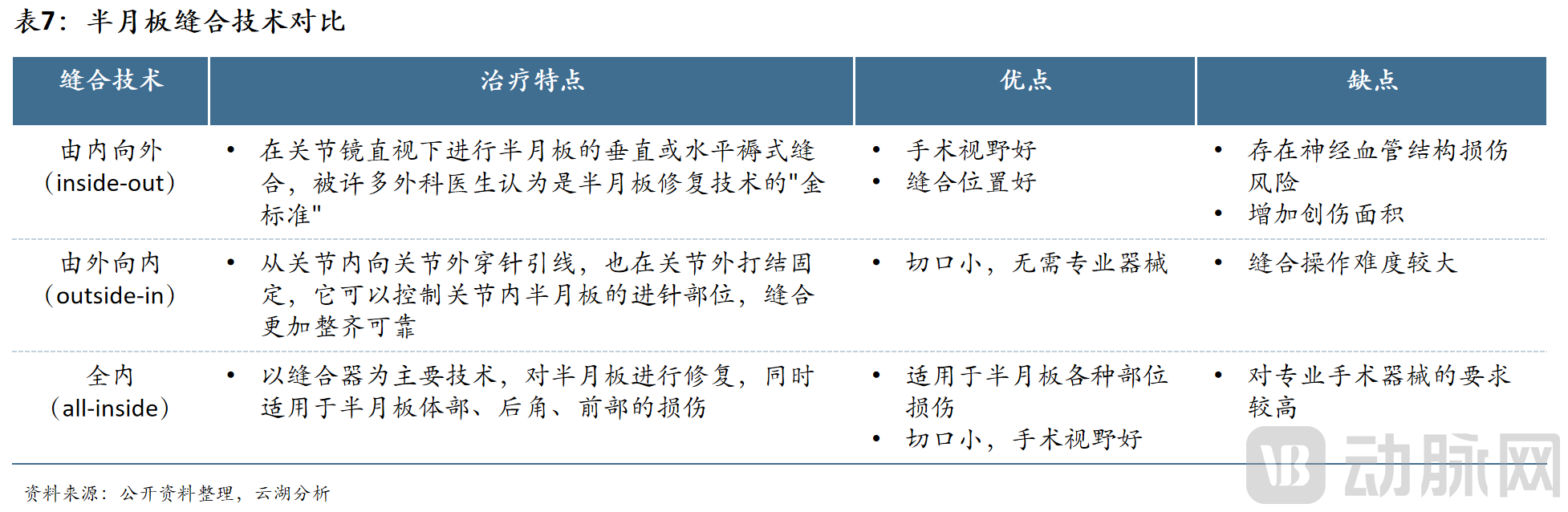

6. Consumables - Knee Joint (Meniscus Region) - Meniscus Repair System

1) Product Overview

The objective of meniscal repair surgery is to preserve the meniscal structure as much as possible, thereby maximizing the meniscus’s protective function for the knee joint. The meniscal repair system is the primary consumable used in all-inside meniscal repair procedures; each system contains a set of implants, including anchors and sutures.

Based on the direction of suture placement, meniscal repair techniques are primarily categorized into three types: outside-in, inside-out, and all-inside. Currently, considering factors such as applicability to the injury site, surgical complexity, extent of tissue trauma, and operative risk, the all-inside meniscal suture technique is regarded as the most ideal approach for meniscal repair.

2) Comparison of Leading Manufacturers

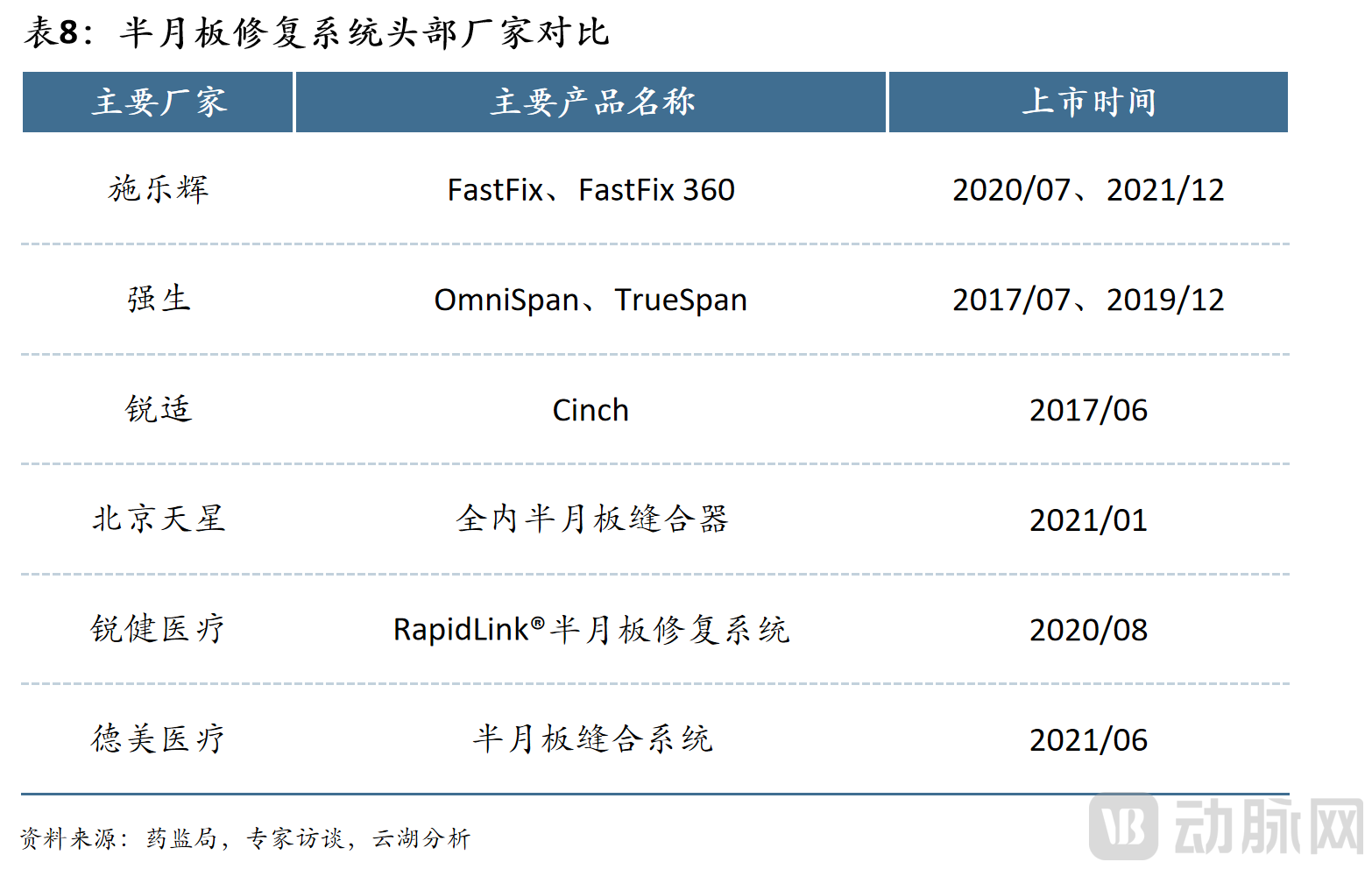

Differences among products from various manufacturers are mainly reflected in implant size, operability, product design, and deployment mechanism. Operability primarily refers to the difficulty of handling during suturing in surgical procedures. Product design is mainly manifested in the external form; for instance, Smith & Nephew’s products are predominantly pen-shaped, while Johnson & Johnson’s are mostly gun-shaped. Deployment mechanisms are categorized into active and passive deployment. Currently, second-generation products launched by international manufacturers, such as Smith & Nephew’s FastFix 360 and Johnson & Johnson’s TrueSpan, feature active deployment. Similarly, the first-generation products from domestic manufacturers are predominantly based on active deployment. In terms of market applicability, active-deployment meniscus repair systems have become the mainstream, as they facilitate easier manipulation of implants by surgeons.

The meniscus repair systems developed by domestic manufacturers are primarily based on secondary R&D of Smith & Nephew’s products. In terms of overall operability, there is little difference between domestic and imported brands; the main disparity lies in the smoothness of system actuation.

In terms of product materials, both domestic and imported manufacturers currently rely primarily on PEEK material.

In terms of product pricing, Johnson & Johnson has the highest hospital procurement price among imported manufacturers. Arthrex is slightly lower in price than other manufacturers due to its overall inferior operability and lack of a second-generation active-triggering product. The prices of domestic manufacturers show no significant difference from those of imported manufacturers and are generally comparable to the prices of Smith & Nephew’s latest-generation products.

3) Competitive Landscape of Meniscus Repair Systems

The domestic meniscus repair system market is dominated by three imported manufacturers: Smith & Nephew, Johnson & Johnson, and Arthrex, while the overall market share of domestic manufacturers remains relatively small, with key players including Beijing Tianxing, Ruijian Medical, and Demei Medical.

Domestic manufacturers hold a relatively low market share, primarily for the following reasons: ① As domestic manufacturers entered the field of meniscus repair systems later than their imported counterparts, thereforeImported manufacturers have a better first-mover advantage; ② Most importers are comprehensive medical device manufacturers or specialized orthopedic manufacturers, with a long history of overall development and stronger R&D capabilities in their respective professional fields, whoseThe product has also undergone market validation in the large European and American sports medicine markets, thereby gaining greater recognition from hospitals and surgeons.

4) Development Trends

Although domestic manufacturers entered the market later, their products currently show no significant differences from imported ones in terms of performance and price. In the future, as domestic products continue to iterate, and given that imported manufacturers may face dual pressures from centralized procurement and medical insurance cost containment, domestic manufacturers are expected to follow the development trajectory of other high-value orthopedic consumables, expand their market share, and gradually achieve import substitution.

7. Consumables - Shoulder Joint - Suture Anchors

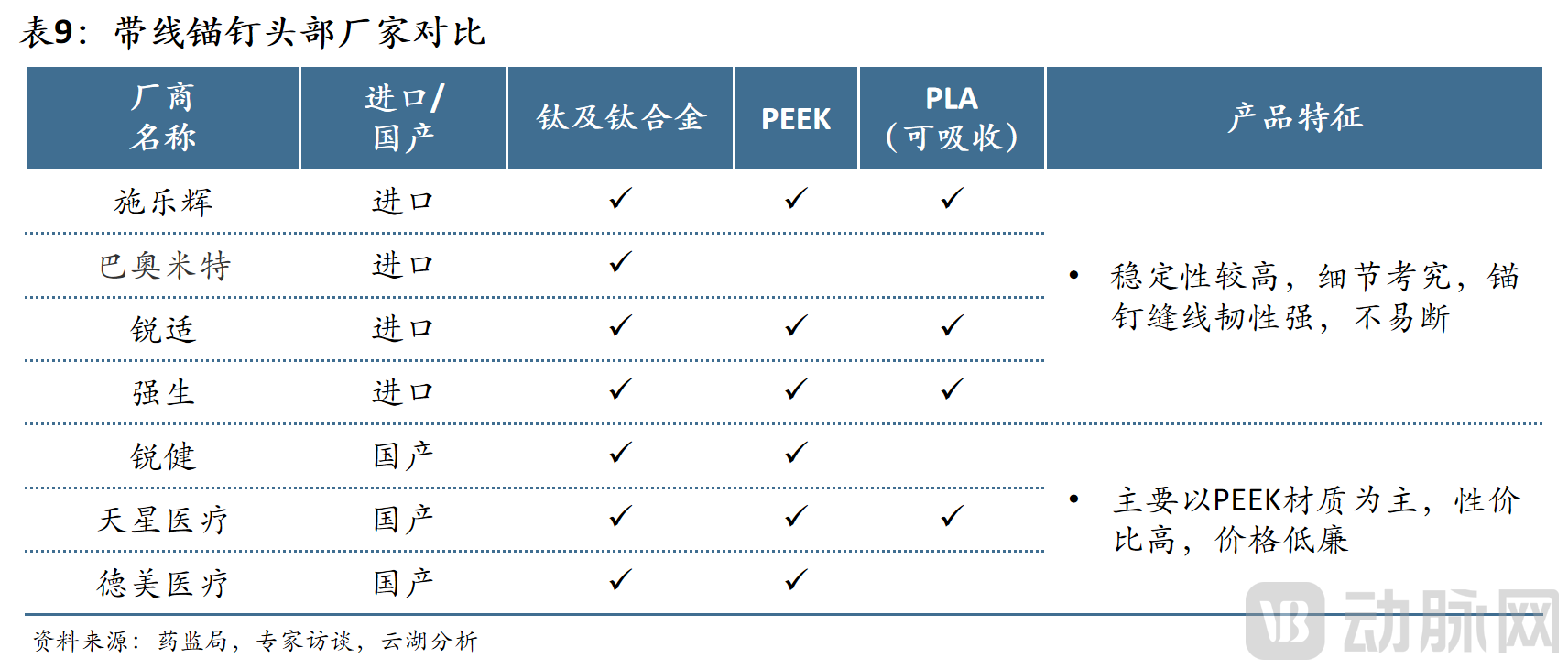

1) Product Overview

Suture anchors secure soft tissue to the bone surface by passing sutures through the tissue via a needle and tying knots to anchor the tissue to the implant. Currently, anchor materials are primarily titanium alloy, PEEK (polyether ether ketone), and absorbable polylactic acid, while the suture component is predominantly made of ultra-high-molecular-weight polyethylene. Among these, absorbable anchors are the most expensive, followed by PEEK anchors, with metal anchors being the most affordable, priced at only half that of PEEK anchors. Currently, suture anchors available on the market are mainly made of PEEK.

Currently, there are four foreign manufacturers of suture anchors: Smith & Nephew, Arthrex, Johnson & Johnson, and Biomet. With the exception of Biomet, the other three companies offer multiple material series. Although numerous domestic enterprises have successfully registered and obtained approval for their products, industry insiders reveal that only Ruijian, Tianxing Medical, and Demei Medical have achieved mass production and secured a certain volume of orders.

2) Comparison of Products from Leading Companies

Suture anchors have relatively low technical barriers in terms of anchor body design, and Chinese manufacturers have already achieved product development. Currently, domestically produced suture anchors are mainly made of PEEK material, with prices generally about 20% lower than imported anchors, offering high cost-performance ratio. However, there is still a significant gap compared to imported products in terms of anchor body stability and attention to detail.

3) Future Development Trends

① Currently, the suture braiding technology for suture anchors is highly advanced. Braiding machines are manufactured by only a few companies in the United States and Germany. Most domestic sports medicine manufacturers currently rely on external procurement; however, driven by cost considerations, Chinese manufacturers are gradually shifting toward independent research and development.

② In the future, domestic manufacturers will place greater emphasis on optimizing anchor shape, leveraging their communication advantages to rapidly address customer needs and update products, thereby making them better suited to Chinese medical practices and achieving genuine import substitution.

③ Currently, Jiangsu’s medical insurance program has included suture anchors in its centralized procurement list, while Henan has added them to its key regulatory oversight list. In the future, the inclusion of suture anchors in medical insurance coverage lists is expected to become a major trend.

III. Leading Companies in Sports Medicine

1. Product Lines of Leading Companies and Their Modes of Entry into the Sports Medicine Field

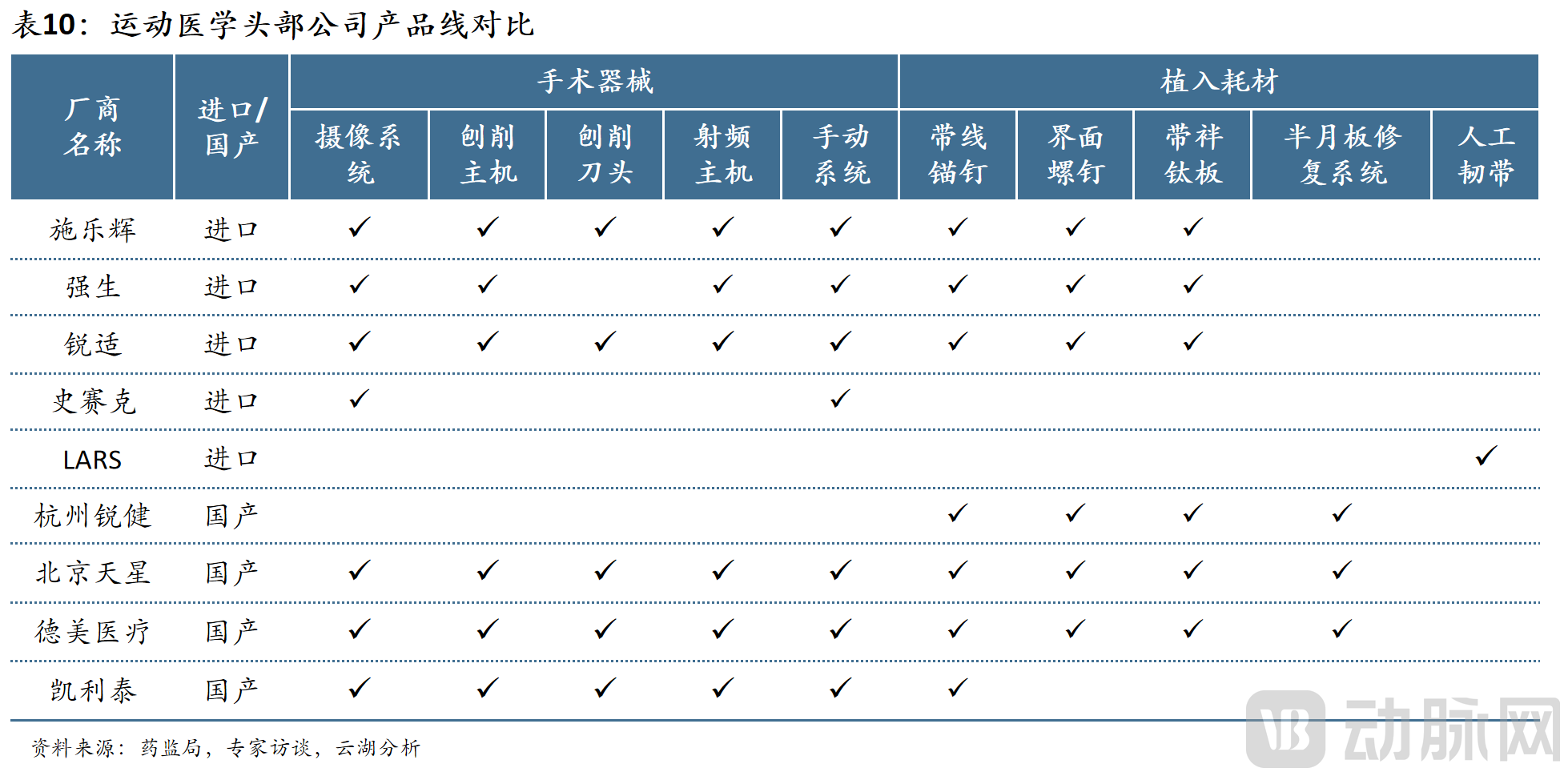

Comparison of Product Lines Among Leading Sports Medicine Companies (Including Only Registered and Marketed Products)

Overall, there are several primary pathways to enter the field of sports medicine:

1) Business Development for the Orthopedics Company

As a leading enterprise in the spine sector, KellyMed has entered the sports medicine field through independent R&D and investments in companies such as Ligament, engaging in the research, development, and production of various products. Similarly, influenced by volume-based procurement (VBP) in orthopedics, traditional orthopedic leaders Weigao Orthopaedics and Double Medical have also shifted their focus to sports medicine in recent years; while their product applications have been approved, large-scale sales have not yet commenced.

Major Companies

■ Kaitai Medical

Established in 2005, the company was listed on the ChiNext Board (Stock Code: 300326) in June 2012. Its orthopedic product portfolio has evolved from a single spinal product at inception to a comprehensive line of high-value orthopedic medical consumables covering multiple fields, including orthopedic trauma, spine, and minimally invasive joint procedures. Furthermore, leveraging its arthroscopic surgery series as an entry point, the company is prioritizing the development of minimally invasive orthopedic products in the sports medicine sector. In April 2021, the company announced a capital increase in Ligetai. Upon completion of the capital injection, the company will hold a 6.178% equity stake in Ligetai. Founded in 2014, Ligetai is a high-tech enterprise specializing in the R&D, production, and sales of sports medicine devices and biomedical materials. It primarily provides integrated solutions for the sports medicine industry, with key products including arthroscopy systems, shaver systems, and shoulder and knee arthroscopes.

2) In-house development by startups

The domestic companies with the highest current market share include Hangzhou Ruijian, Beijing Tianxing, and Demei Medical, all of which are emerging startups. In addition to the leading companies, Yunyi Medical is also a self-developing enterprise; its multiple products were successfully approved for launch in 2020, and it is currently still in an expansion phase.

Major Companies

■ Ruijian Medical

Founded in 2010, the company’s R&D, operations, marketing, and sales management teams comprise more than 80% of personnel from globally renowned medical device companies such as Johnson & Johnson, Smith & Nephew, and Medtronic. The company currently offers a comprehensive product portfolio in the field of sports medicine, including solutions for the shoulder, knee, clavicle, biceps, hip and ankle, patellofemoral joint, elbow, and wrist, covering categories such as devices, instruments, consumables, implants, and biologics. In August 2021, the company secured nearly RMB 100 million in Series A+ financing from investors including Vertex Ventures and Yida Capital.

■ Beijing Tianxing

Founded in 2017, the company has obtained NMPA (National Medical Products Administration) approval for the market launch of over 100 products, including PEEK internal and external row suture anchors, metal suture anchors, all-suture anchors, fixation loop plates, adjustable loop plates, PEEK sheathed interference screws, all-inside meniscus repair systems, double-needle meniscus devices, powered shaver systems, shaver blades, burrs, knee/shoulder arthroscopic surgical instruments, and multifunctional shoulder joint fixation braces. In January 2022, the company secured hundreds of millions of RMB in Series B financing from investors such as Aubo Capital and 3W Partner.

■ Demei Medical

Established in 2015, the company focuses on two core areas of sports medicine: new materials and minimally invasive technologies. Its product portfolio covers commonly used clinical consumables, various surgical instruments, and arthroscopic equipment, meeting the needs for both arthroscopic and open surgeries for common and frequently occurring sports medicine conditions affecting the shoulder, knee, and other joints. The company’s core products include more than ten sports medicine items such as independently developed ultra-high-molecular-weight polyethylene sutures, suture anchors in various models and materials, button plates with loops, and meniscal repair systems. The company’s revenue was approximately RMB 3 million in 2017 and RMB 20 million in 2018. In February 2021, Demei Medical announced the completion of a financing round totaling nearly RMB 150 million, led by CDH Investments, with participation from Qiming Venture Partners and Boying Capital.

3) Mergers and Acquisitions

Johnson & Johnson, a global leader in sports medicine, acquired Depuy in 1998 and Synthes in 2011 to bolster its sports medicine product portfolio. Similarly, Smith & Nephew has enhanced its competitiveness through continuous in-house R&D and external acquisitions; in 2014, the company acquired ArthroCare, enriching its product lines in radiofrequency ablation and shoulder joint treatment.

Major Companies

■ Smith & Nephew

Since entering China in 1993, the company has established offices in five cities: Shanghai, Beijing, Guangzhou, Chengdu, and Shenyang. In 2014, Smith & Nephew acquired JESS Medical, expanding into plasma radiofrequency devices and increasing its market share in the radiofrequency equipment sector to over 50%. Currently, the company operates two factories in China producing orthopedic and advanced wound care products for both the Chinese and global markets, with an overall market share of approximately 50% in China.

■ DePuy Synthes (Johnson & Johnson)

Founded in 1886, Johnson & Johnson is one of the most comprehensive and widely diversified healthcare companies in the world, with operations spanning three major sectors: medical devices, pharmaceuticals, and consumer health. Headquartered in New Brunswick, New Jersey, USA, the company operates more than 260 subsidiaries across 60 countries and regions, employing over 130,000 people worldwide. In 2020, its global revenue reached $82.6 billion, with global R&D investment amounting to $12.2 billion. Johnson & Johnson’s orthopedics business is conducted through its subsidiary DePuy Synthes (formed by the merger of the acquired Depuy and Synthes), which provides solutions in joint reconstruction, trauma, spine, sports medicine, craniomaxillofacial surgery, as well as power tools and biomaterials. Holding a dominant position in the global orthopedics market, it commands approximately 20% market share in China.

■ LARS

Founded in 1992 and headquartered in France, the company is a specialized medical device research and manufacturer focusing on synthetic ligaments for orthopedic surgery. In 1998, the company intensified its R&D efforts, committing to the development of a bioactive ligament that allows human fibroblasts to adhere to and grow into the implanted synthetic ligament fibers. In 2004, its synthetic ligament became the only product of its kind approved by the French Ministry of Health. Around 2018–2019, rumors circulated that the French company’s founder intended to sell LARS, causing significant stir within the industry. Many domestic companies, including orthopedic manufacturers and distributors, engaged in acquisition negotiations with LARS. It is reported that LARS was acquired by Huajie Ruizhong in 2021.

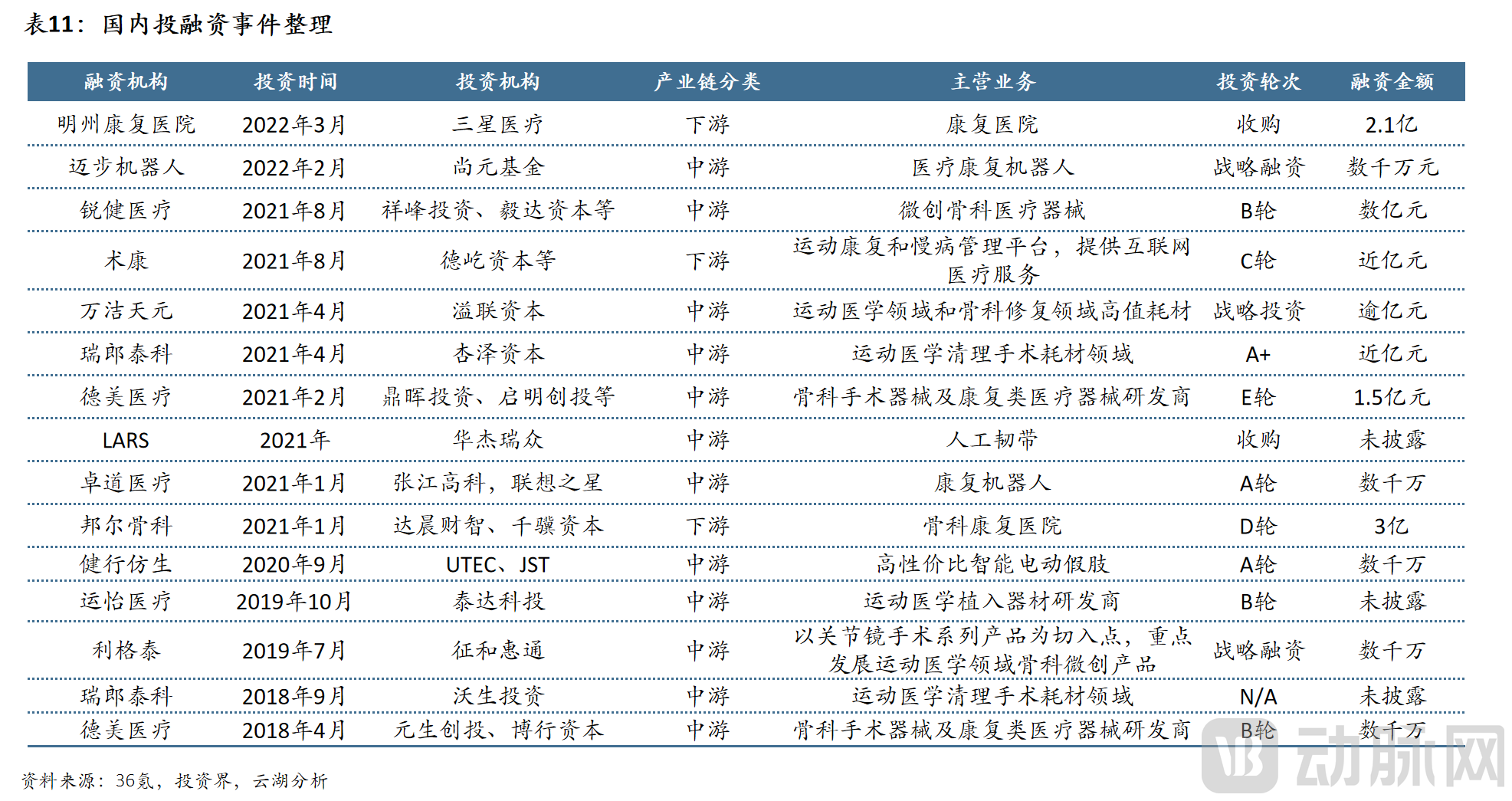

2. Domestic Investment and Financing Events

Overall, investment activities in China’s orthopedic consumables sector have been frequent in recent years. Both traditional comprehensive orthopedic manufacturers and emerging medical consumables companies are actively laying out their product pipelines. This trend is primarily driven by domestic manufacturers’ gradual shift from traditional orthopedic consumables with low technical barriers to the research and development of high-value consumables characterized by high technical barriers and low localization rates, including surgical robots, artificial joints, and arthroscopic equipment.

As the market share of sports medicine within China’s orthopedics sector gradually increases, and as related products gain broader acceptance among surgeons and patients, domestic manufacturers will intensify their strategic investments in the sports medicine field. Consequently, the process of import substitution for high-value consumables in sports medicine is expected to accelerate steadily. Regarding industry consolidation, as China’s sports medicine market matures, leading enterprises—mirroring trends in international markets—will increasingly pursue mergers and acquisitions to expand their product portfolios.

References:

1. “Sports Medicine Special Report (I) – Market Status and Prospects in the Implant Sector,” “Sports Medicine Special Report (II) – Industry Chain Market Research Analysis,” Beituo Capital

2. “The Rising Red Sun—One of the Studies on Sports Medicine: Industry Overview,” Guojin Securities

3. “2021 White Paper on the Chinese Orthopedic Device Industry,” LeadLeo Research Institute

4. “Sports Rehabilitation Poised for Rapid Growth: Key Work Points of the Healthy China Action 2022 Released,” ife

5. “A Comprehensive Review of Medical Consumables: Which Consumables Will Join the Centralized Procurement in 2022,” Medical Device Innovation Network

6. “Special Report on Orthopedic Sports Medicine in the Pharmaceutical Industry: The Industry Is in Its Ascendant Phase, and Domestic Substitution Begins,” Southwest Securities

7. "Interpretation of the All-Inside Technique for Meniscal Repair," Dr. Wan, Huashan Hospital Affiliated to Fudan University