Where Did the Money Go in Global Biopharma Investment During H1 2022 Amid the Capital Winter?

Core Viewpoints

1. Both the number of financing events and the total financing amount in H1 2022 declined year-on-year, yet they remained the second-highest levels since 2016. Valuable innovative projects continued to attract strong investor interest during the capital cooldown period, reflecting sustained market optimism.

II. Globally, early- to mid-stage projects remain a key focus for capital deployment, while large-scale investments exceeding $100 million have declined significantly, reflecting a more cautious market. Biologics are the most sought-after asset class, followed by R&D and manufacturing outsourcing services.

3. Each sector exhibits distinct growth patterns, including “low-hanging fruit,” evolutionary, and surge-driven models. Gene therapy and CXO sectors lead in market interest and serve as the primary drivers of investment and financing growth;

IV. Novowell Health and Xiamen Unimedicine ranked among the top 10 globally in financing amount, driven by strategic development funding. CXO and synthetic biology are prominent labels for the top 10 companies in China, with a new trend highlighting “incubation” attributes emerging.

V. Nineteen Chinese Companies Ring the Bell: Overall Listing Enthusiasm Remains Undiminished, with the A-share Market as the Primary Venue, While Interest in Overseas Listings Cools

I. Global Biopharmaceutical Investment and Financing Trends from 2016 to H1 2022

1.1 The average financing amount per transaction in H1 2022 was substantial, with valuable innovative projects remaining highly sought after even during the capital cool-down period

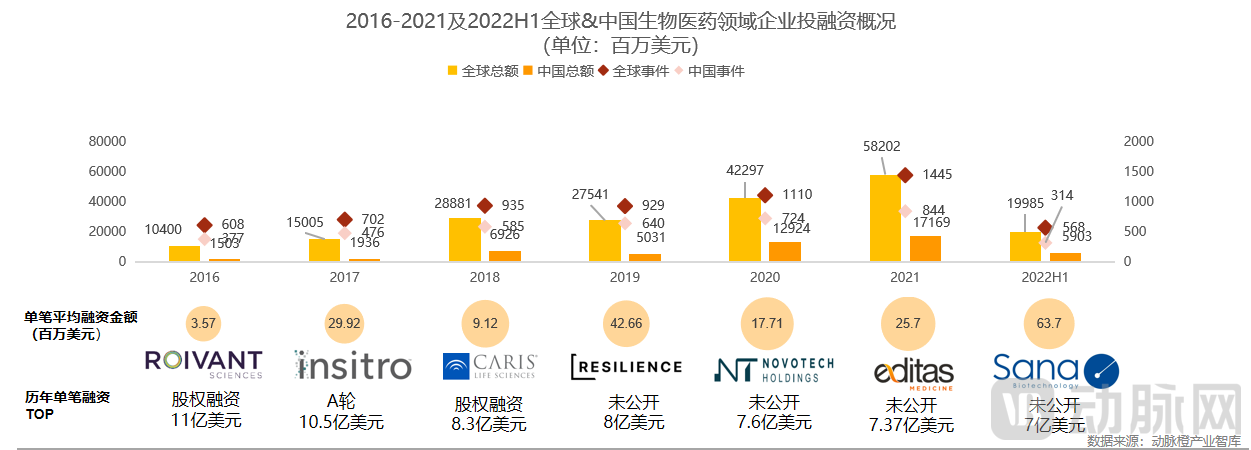

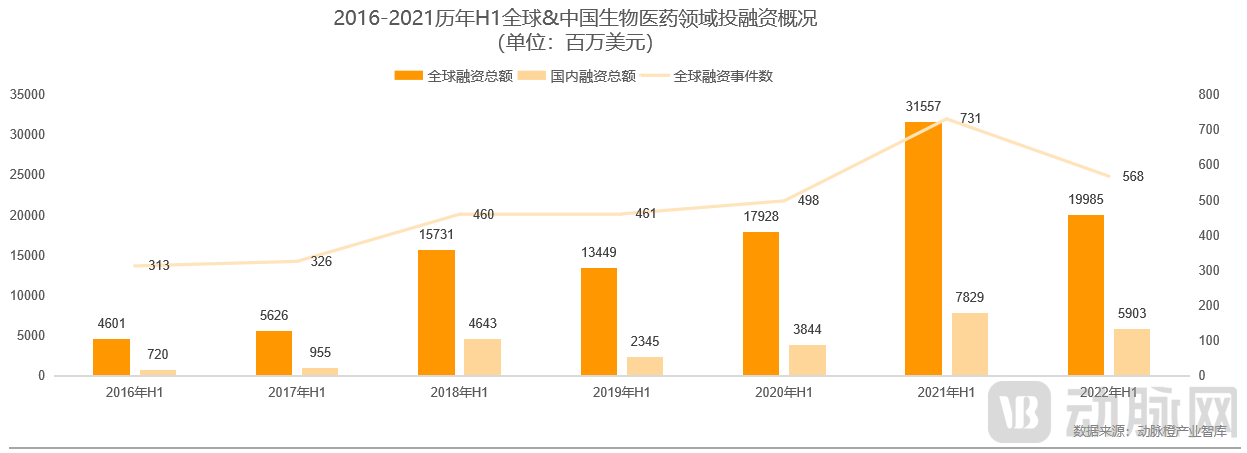

From 2016 to H1 2022, a total of 6,297 financing transactions occurred in the global primary market for biomedicine, with cumulative financing amounting to approximately $202.3 billion (approximately RMB 1.315 trillion).

From 2016 to 2021, overall investment enthusiasm in the primary market continued to rise, with a minor dip in financing activity observed only in 2019. Notably, both the number of deals and the total amount invested saw significant increases in 2020 and 2021, aligning with global trends. In the first half of 2022 (H1 2022), amid a period of capital caution both globally and in China, the average financing amount per deal remained substantial. This indicates that even during a financing downturn, high-value innovative projects continued to attract strong investor interest.

1.2 Both the number of financing events and the total financing amount in H1 2022 declined year-on-year, yet remained at the second-highest level on record, with the market maintaining an optimistic outlook

H1 2022: Domestic and Overseas Capital Cools Down; Both the Number of Financing Deals and Total Funding Amount Decline, Yet Remain the Second Highest Since 2016.

In H1 2022, there were 568 financing deals in the global primary market for biopharmaceuticals, a year-on-year decrease of 163 deals. The total financing amount reached nearly $20 billion (approximately RMB 130 billion), representing a year-on-year decline of about 37%. In China, the trend largely mirrored the global pattern, with 255 financing deals recorded in H1 2022. Although overall market enthusiasm was lower than that of the same period last year, optimism remains.

II. Hot Sectors in Global Biopharmaceutical Investment and Financing in H1 2022

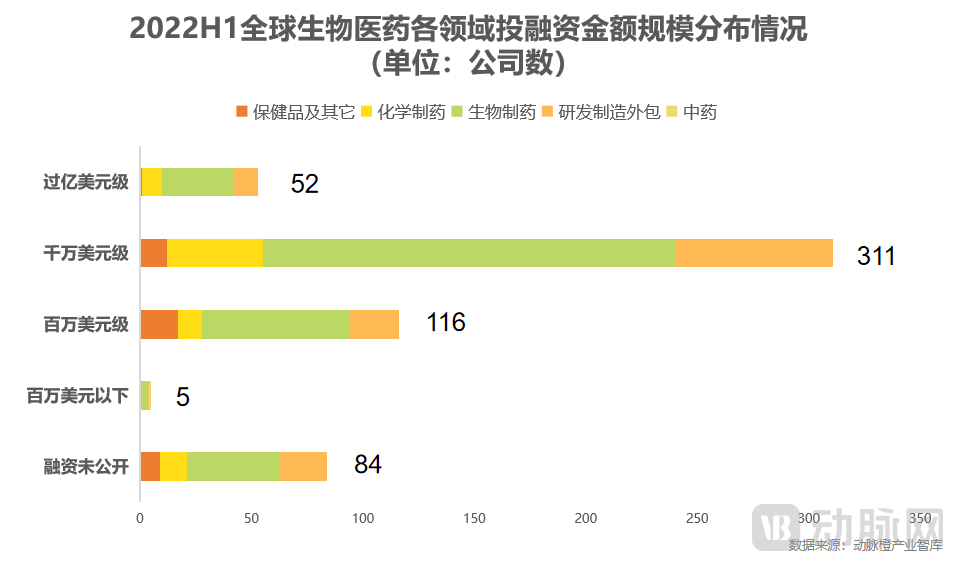

2.1 Early- to mid-stage projects remain a key focus for institutional investors; biologics are still the most sought-after, followed by R&D and manufacturing outsourcing.

In terms of funding amounts, deals in the tens of millions of dollars are the norm, followed by those in the millions. Early- to mid-stage projects remain the primary focus for most investors.

From the perspective of sub-sectors, biologics are the dominant field across all investment tiers, followed by R&D and manufacturing outsourcing, which demonstrates a significant advantage in attracting capital at the multi-million-dollar level.

A total of 52 financing deals exceeding $100 million were recorded, accounting for approximately 10% of the total financing amount in H1, a decline from the 99 deals seen in the same period last year.

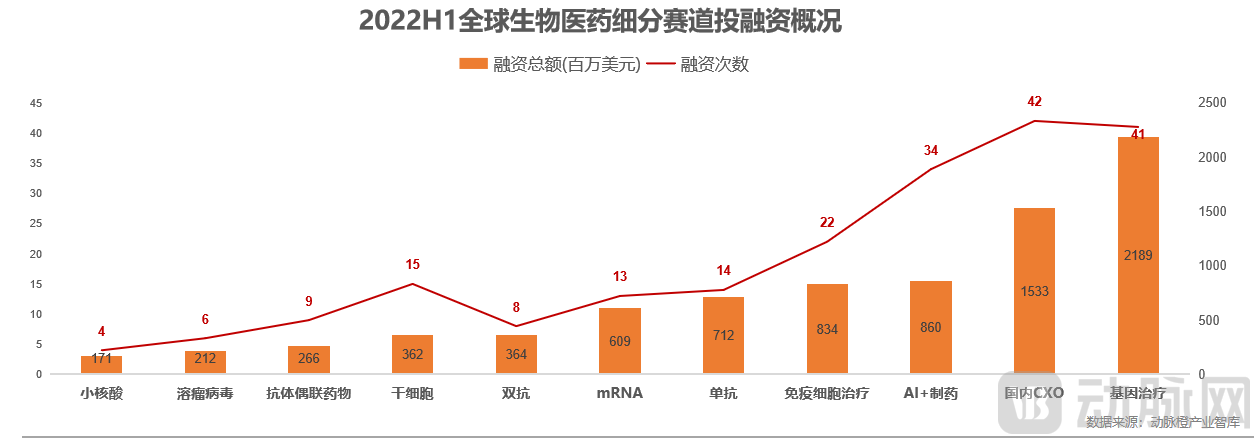

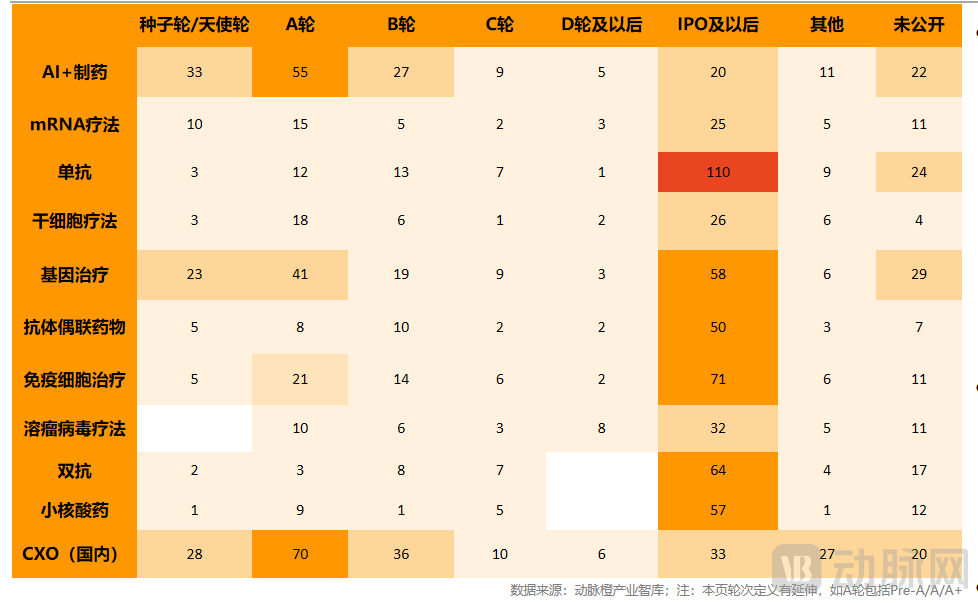

2.2 Gene Therapy and CXO Lead in Popularity, with AI+Drug Discovery, Immune Cell Therapy, Monoclonal Antibodies, and mRNA Ranking in the Second Tier

Gene therapy and CXO (in China) are the two sectors most favored by capital, while AI-driven drug discovery, immune cell therapy, monoclonal antibodies, and mRNA constitute the second tier in terms of market热度. These six sectors together form the primary drivers of growth in investment and financing.

In the first half of the year, China’s gene therapy sector saw a succession of breakthroughs, with Investigational New Drug (IND) applications for gene therapy products from Longxin Biopharma, Hongji Biopharma, Jiayin Biopharma, and Bendao Gene being approved in turn, marking new milestones. Interest in gene therapy is expected to remain strong.

2.3 Fruit-Picking, Evolutionary, and Surge Models: Divergent Growth Landscapes Across Different Tracks

Monoclonal antibodies, immune cell therapies, gene therapies, small nucleic acids, and antibody-drug conjugates have all reaped the initial rewards. In particular, for monoclonal antibodies and bispecific antibodies, the mature stage (IPO and beyond) has become the overwhelmingly dominant trend. However, in the fields of gene therapy and immune cell therapy—sectors characterized by high demands for continuous technological innovation and substantial growth potential—early- to mid-stage projects continue to attract significant interest, with clear trends in technological evolution.

AI+Drug Discovery, as an ITBT cross-disciplinary technology sector, is showing a trend of divergent growth. A small number of companies have reached the late stages of maturity, while the majority are still in the proof-of-concept and early product development phases, warranting close attention and high expectations.

As China’s biopharmaceutical industry reaches a critical threshold for scaling, the domestic CXO sector is experiencing explosive growth, with a substantial accumulation of Series A financings; industry consolidation and vertical specialization are emerging as future trends.

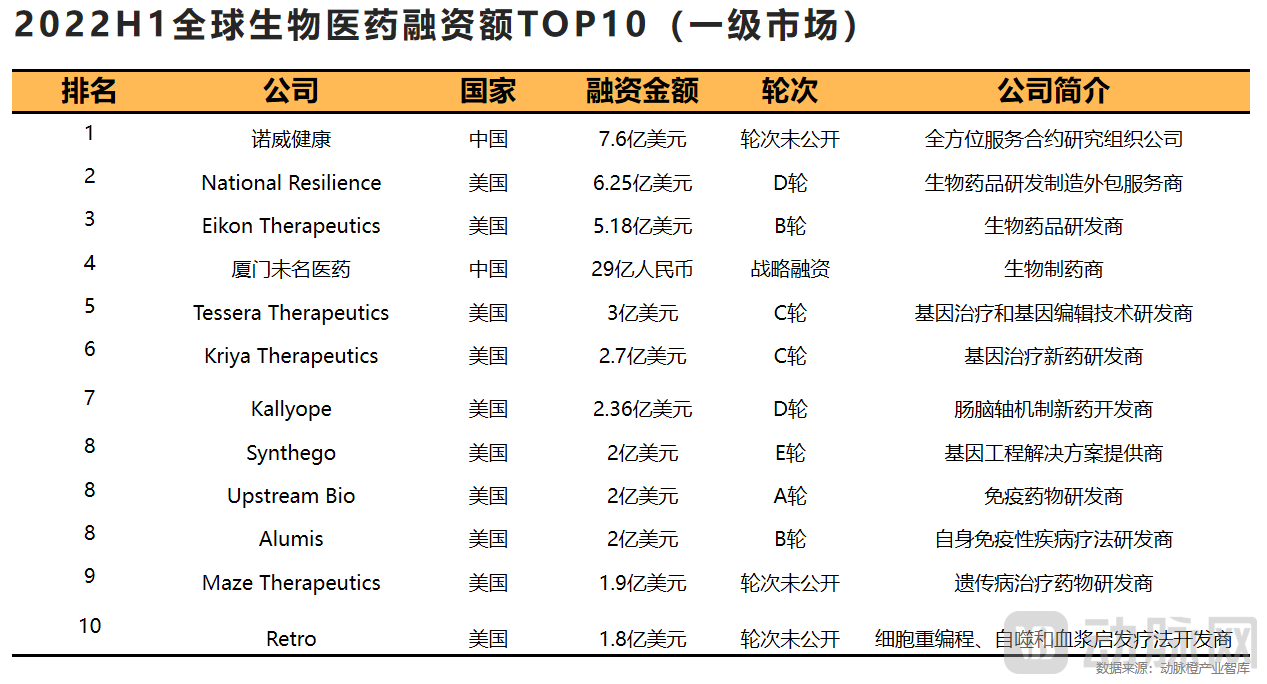

III. Top 10 Global Biopharmaceutical Companies in Financing and Investment in H1 2022

3.1 NovWell Health and Xiamen Unimed Pharmaceuticals made the list thanks to strategic development financing; gene therapy and immunotherapy are the two sectors where foreign listed companies are relatively concentrated.

3.2 CXO and synthetic biology are prominent sector labels among the top 10 companies; Duoma Pharma and Ruishi Biologics are the only two Series A companies on the list, drawing attention to their “incubation” attributes.

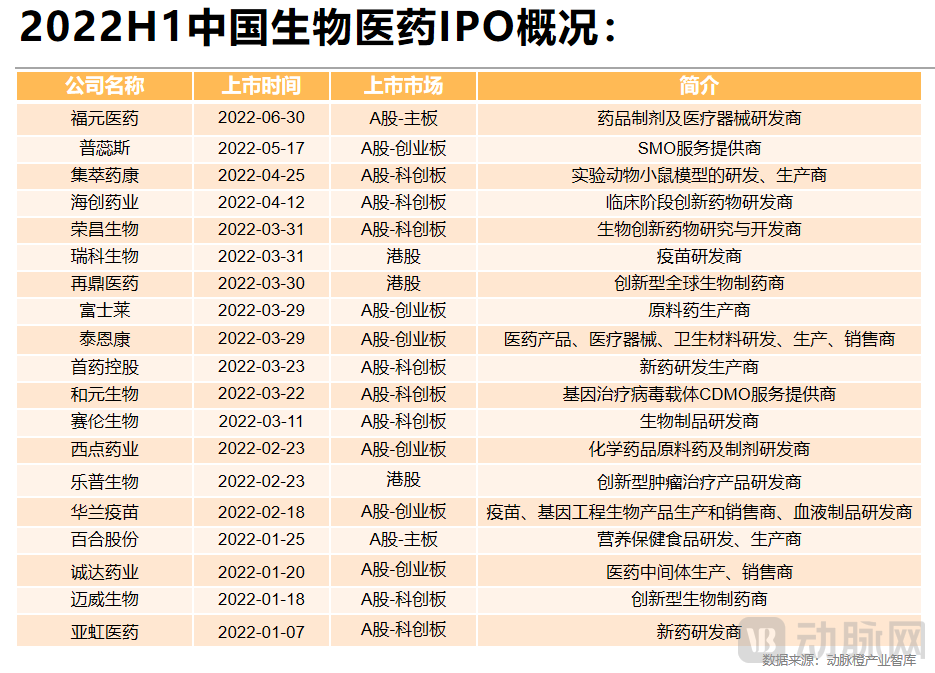

IV. Chinese Biopharmaceutical Companies with IPOs in H1 2022

19 Companies Ring the Bell: Listing Enthusiasm Remains Strong, with A-Shares as the Primary Venue

In the first half of 2022, 19 domestic biopharmaceutical companies went public in China, basically on par with the 20 listings during the same period last year, indicating that overall enthusiasm for IPOs remained undiminished.

The STAR Market has become the primary venue for listings of innovative enterprises, with eight companies; the ChiNext Board follows closely with six. The pace of Hong Kong stock listings has slowed. Influenced by the combined effects of the international political and economic environment, enthusiasm for overseas listings is significantly lower than in the same period last year.

The secondary market has successively welcomed the first CGT CDMO stock—Obio Technology, the first domestically produced 9-valent HPV vaccine stock—Reco Biotech, and the first PROTAC stock—Haisco Pharmaceutical.

Data Definition Rules

*To facilitate statistical analysis, we adhere to the following principles when processing investment and financing data:

1. The financing events covered in this report include only those from the angel round up to, but not including, the initial public offering (IPO); they exclude IPOs, private placements, donations, mergers and acquisitions, and other such transactions;

2. Consolidate angel round, seed round, and seed VC into the angel round; consolidate all rounds containing “A” into Series A; consolidate all rounds containing “B” into Series B; consolidate all rounds containing “C” into Series C; and consolidate rounds above Series C but below IPO into Series D and beyond;

3. All monetary amounts in the charts and tables of this report are denominated in U.S. dollars, calculated based on an exchange rate of 6.5 CNY to 1 USD;

4. The data in this report is current as of June 30, 2022. Any data released after June 30, 2022, is excluded from the statistical scope of this report and will be dynamically updated on VCBeat’s Investment and Financing channel;

5. Standardize financing amounts in the millions, tens of millions, or hundreds of millions to 1 million, 10 million, or 100 million, respectively;

6. The financing events included in the chart are limited to those with disclosed amounts; events without disclosed amounts are excluded.