H1 2022 Global Early-Stage Healthcare Investment Report: Rising Capital Tolerance for Startups, China's Early-Stage Funding Nears $900 Million

1. In the first half of 2022, the number of financing events and the total amount raised in the global healthcare industry both declined overall compared to the previous year; however, sustained growing investor interest in early-stage medical projects in China drove an increase in the overall volume of investment and financing transactions within the domestic healthcare industry.

2. Capital is actively positioning itself to invest in early-stage and small-scale ventures; the biopharmaceutical sector demonstrates significant financing advantages, followed closely by the digital health sector, although the latter lacks large-scale financing deals.

III. Sequoia China Emerges as the Most Active Investor in Early-Stage Healthcare Projects in H1, with a Focus on Biopharmaceutical Companies; Guided by Policy, Investment Firms Will Continue to Concentrate on Early-Stage Healthcare Projects

IV. Biopharmaceuticals and digital health were hotspots of global interest in 2022, with growing demand for medical data access services. Capital has been widely investing in startups in this sector, and the healthcare industry’s demand for digitalization is expected to continue rising in the future.

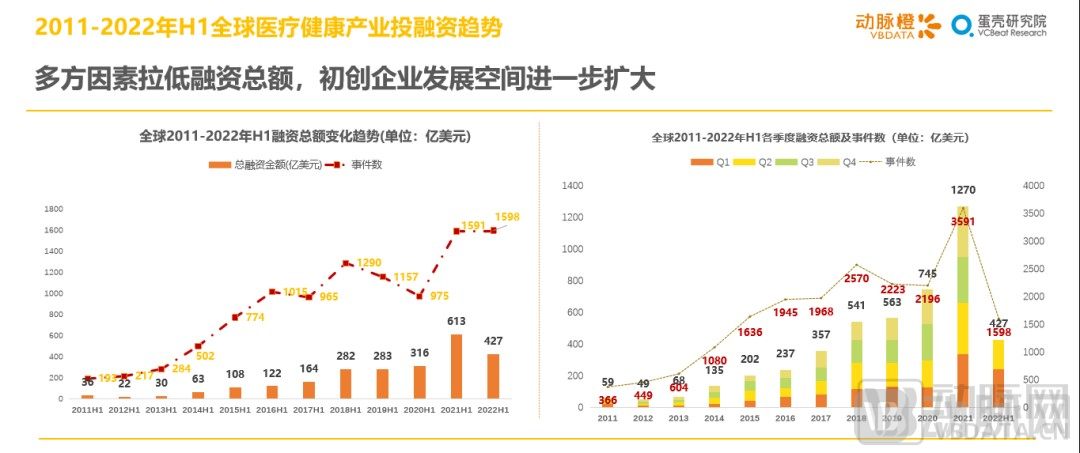

Trends in Global Healthcare Startup Financing, 2011–H1 2022

1.1 Multiple Factors Disrupt the Investment and Financing Market, with Sustained Growth in Attention Toward Startups

Affected by factors such as regional conflicts, the pandemic, energy issues, debt, and inflation, both domestic and overseas financing markets experienced a certain degree of volatility in the first half of 2022. Among them, the financing market for the healthcare industry was not as optimistic as expected.

H1 2022,A total of 1,598 financing events occurred in the global healthcare industry., an increase of 6 cases year-on-year;Total financing reached $42.7 billion(approximately RMB 277.734 billion), ranking second highest on record, representing a decline of approximately 43% from the historical peak in H1 2021, with the overall market cooling down.

However, capital’s tolerance for startups has continued to rise, sustaining the attitude it adopted toward early-stage projects in 2021. An increasing number of high-potential, high-growth startups have secured funding, enabling them to further expand and strengthen during the first half of this year.

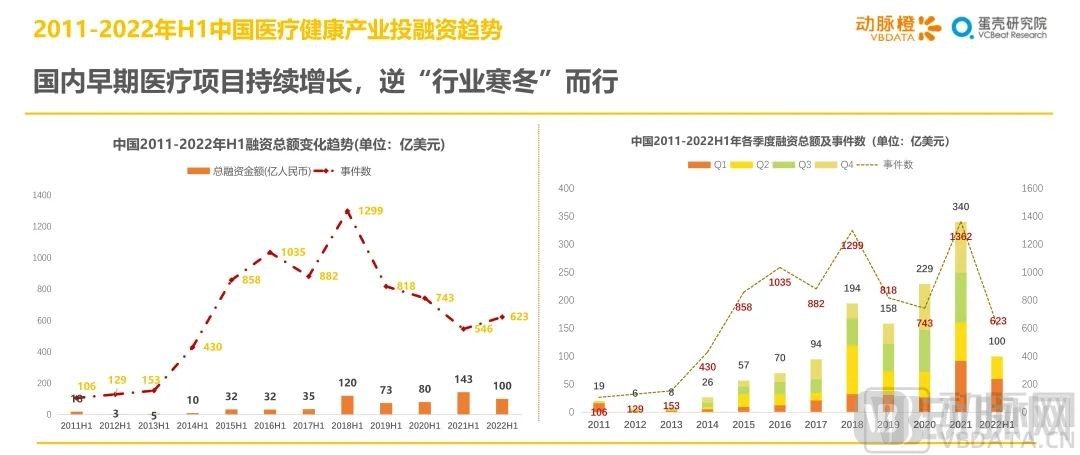

1.2 Investment and financing for early-stage medical projects in China continue to grow, bucking the “industry winter” trend

In H1 2022, the total investment and financing in China's healthcare industry amounted to nearly $10 billion.(approximately RMB 64.759 billion), a year-on-year decrease of over 40%; meanwhile, the number of domestic financing transactions reached 623, an increase of 77 compared to H1 2021.

Total investment and financing amounts saw a significant decline, yet the number of financing transactions increased. This trend is primarily attributed to a rise in early-stage healthcare project investments.

In H1 2022, a total of 180 early-stage financing events (including seed, angel, and Pre-A rounds) occurred in China’s healthcare sector, with cumulative funding reaching nearly $900 million. These figures closely approached the full-year totals for 2021, both in terms of the number of financing deals and the total amount raised.(296 financing events raised over $1.194 billion, approximately RMB 7.76 billion).

In recent years, under the direct pressure of “performance evaluations,” research institutions and scientists have focused more on translating scientific achievements into practical applications than ever before. Coupled with domestic policy guidance and support in terms of funding and resource allocation, a growing number of scientists are aligning with the times by moving from the laboratory to the marketplace.

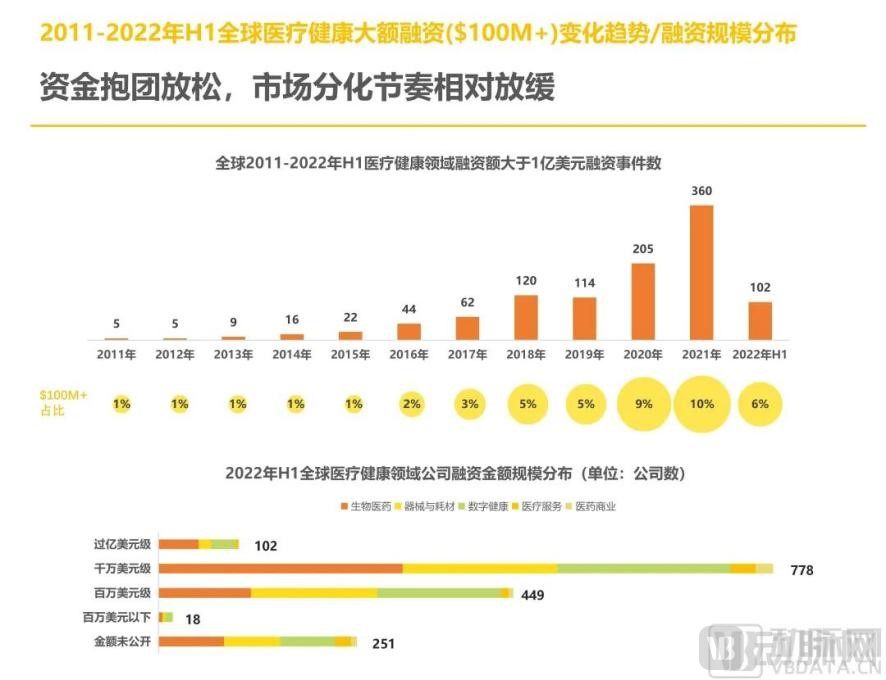

1.3 Easing of Capital Herding, with a Relatively Slower Pace of Market Divergence

The trend from Q1 2022 continued through the end of the first half of the year: in H1 2022, there were 102 global financing deals each exceeding $100 million, accounting for over 6% of the total financing amount in H1, which was lower than the same period in 2021; half of these deals originated from the biopharmaceutical sector.

Moreover, among the most numerous financing rounds in the tens of millions of dollars, biopharmaceutical companies accounted for the largest share and demonstrated a clear advantage, further widening the gap with companies in the digital health and medical device sectors.

Similar to 2021, the global economic sentiment remained weak in the first half of 2022. However, compared to the capital clustering driven by the defensive nature of the healthcare industry in 2020–2021, this phenomenon significantly eased in H1 2022, while the momentum of startups continued to rise.

Top Healthcare Early-Stage Investment and Financing Tracks in H1 2022 Globally

2.1 Capital Actively Positions in Early-Stage and Small-Scale Investments, with High Interest in Biopharmaceuticals and Healthcare Informatics

In H1 2022, tags such as biopharmaceuticals, healthcare IT, IVD, and R&D and manufacturing outsourcing garnered significant attention. In terms of financing rounds, public funding in H1 2022 was concentrated primarily in the early stages, particularly Series A.

Specifically, these companies are all in high-barrier innovative tracks within the healthcare sector, such as the artificial heart track, where the first fully magnetically levitated VAD approved by the NMPA was obtained.Tongxin Medical, deeply cultivating deep brain stimulation in the invasive brain-computer interface sectorJingyu Medicaland securing the highest single-round financing amount record in the rehabilitation robotics sectorFourier Intelligence。

It is evident that, despite the overall decline in global healthcare financing activity in 2022, investment firms have actively pursued early-stage and small-scale investments while continuing to focus on high-potential, long-term growth sectors.

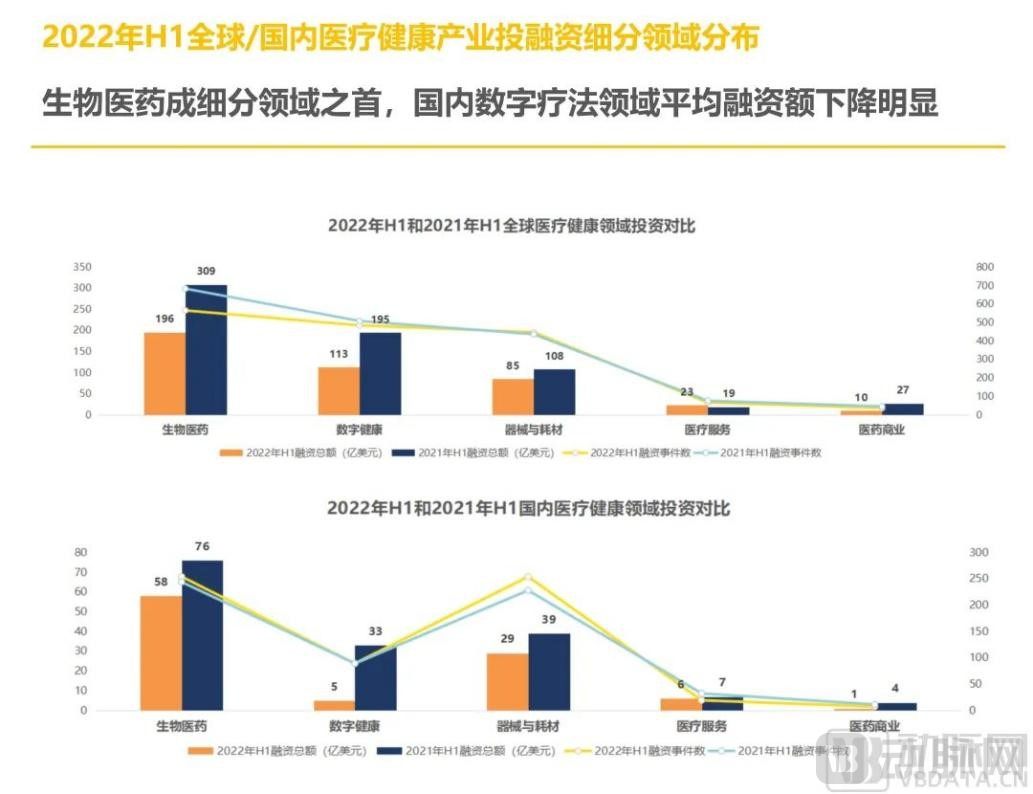

2.2 Financing in the Digital Health Sector Declines Significantly, with Investment Rounds Concentrated in Early Stages

Compared with the first half of 2021 (H1 2021), both the total global funding amount and the number of financing deals across all sectors have declined to varying degrees this year, with the digital health sector being particularly affected, registering a 42% quarter-on-quarter decrease in total funding.

In H1 2022, China's digital health sector saw financing deals primarily at the million-dollar level, with no mega-rounds exceeding $100 million; moreover, funding rounds were concentrated in the early stages.

It is evident that amid the capital winter, while investment institutions have actively positioned themselves and maintained follow-up in this sector, they are more inclined to adopt a wait-and-see attitude.

Analysis of Active Healthcare Investment Institutions in H1 2022

3.1 Sequoia China Emerges as the Most Active Investor, with Capital “Aggressively” Shifting Toward Early-Stage Ventures

H1 2022,Sequoia China has made a total of 35 investments, becoming the most active investment institution in the global healthcare sector. Furthermore, in terms of investment rounds, demonstrating a bias toward pre-Series A.

Sequoia China’s investment portfolio is dominated by biopharmaceutical companies. Notably, NeuroXess, a developer of invasive brain-computer interfaces, and Xinrui Regenerative Medicine, a small-molecule novel drug developer, each received additional investments from Sequoia China twice within six months.

Qiming Venture Partners made 28 investments in the first half of 2022, ranking second globally. Notably, Qiming Venture Partners led 17 of these 28 financing rounds.

Notably, in the first half of 2022, 52 early-stage biopharmaceutical companies secured financing from the top 10 most active investment firms, indicating a trend among investors to increasingly focus on early-stage biopharmaceutical enterprises.

3.2 Local Policies Guide Early-Stage and Small-Scale Investments, with Investment Institutions Concentrating Efforts on Early-Stage Healthcare Projects

The top 10 most active investment firms in China all favor the biopharmaceutical, medical device, and consumables sectors, with their investments primarily concentrated around the Series A stage.

In H1 2022, investment institutions increasingly focused on early-stage healthcare projects. Based on the financing market conditions and specific funding events in China during the first half of the year, the primary driver behind this trend was policy support.

In recent years, local governments have guided investment institutions to invest in early-stage and small-scale enterprises through policy measures. For example, the Shenzhen Municipal Local Financial Supervision Administration directly mentioned incentive measures for investment institutions investing in seed-stage and start-up technological innovation enterprises in Shenzhen in its "Several Measures on Promoting the Sustainable High-Quality Development of Venture Capital and Private Equity in Shenzhen," released on April 7, 2022.

Analysis of Hot Trends in Global Healthcare Investment and Financing in 2022

4.1 Biopharmaceuticals and Digital Health Are Global Hotspots, with Cell and Gene Therapy Entering the “Fast Lane”

From the perspective of investment hotspots, biopharmaceuticals and digital health were the areas of global common interest in the first half of 2022.

In China, the 14th Five-Year Plan for the Development of the Pharmaceutical Industry, released in January 2022, proposed prioritizing the development of industrialized manufacturing technologies for novel biologics, including cell and gene therapies. Meanwhile, during the first half of the year, the cell and gene therapy sector attracted investment from top-tier firms such as Sequoia Capital, Hillhouse Capital, Matrix Partners China, Qiming Venture Partners, OrbiMed, and RA Capital.

It is evident that, supported by policies, technology, capital, and downstream markets, the cell and gene therapy industry is entering a “fast track.”

Furthermore, the healthcare industry is gradually expanding into high-tech domains, with innovative projects featuring proprietary technologies and substantial market potential more likely to stand out in the early-stage market.

4.2 Surge in Demand for Medical Data Access Services Drives Capital Influx into Startups

The U.S. 21st Century Cures Act requires providers to enable patients to easily and digitally access their medical records through application programming interfaces (APIs). The relevant provisions of the Act have prompted some emerging health informatics companies in the United States to enter the data access services market.

Meanwhile, the FHIR (Fast Healthcare Interoperability Resources) standard, as a non-mandatory guideline, has been incorporated into the business development plans of some startups due to its role in facilitating the secure exchange of health information.

It is evident that trends such as APIs (Application Programming Interfaces), the expansion of virtual care, and the decentralization of health data will continue to drive the demand for digitalization in the healthcare industry.

However, the current digital health sector primarily caters to enterprise needs, while business models targeting end-consumer demands still hold significant growth potential.