How Women's and Children's Hospitals Are Breaking Through the Customer Acquisition Bottleneck Amid the Surge in Medical Aesthetics and Postpartum Rehabilitation

JINXIN FERTILITY

Assisted Reproductive Technology Service Provider

In the "Statistical Bulletin on the Development of China's Health and Hygiene Undertakings in 2021" recently released by the National Health Commission, the proportion of third-child births following the implementation of the new population policy was disclosed for the first time: third children and above accounted for 14.5%.

Three-child policy, birth rate... have long become keywords closely watched by all sectors of society. In the healthcare industry, the most directly related aspect is the transformation of the maternal and child healthcare market.

When the two-child policy was introduced, both public and private institutions made substantial investments in the women’s and children’s healthcare sector, with a particular focus on obstetrics. However, the subsequent baby boom proved short-lived. In recent years, even with the implementation of the three-child policy, the declining fertility trend has not been reversed. Within women’s and children’s hospitals, obstetrics departments were the first to feel the resulting market impact.

The overall customer base has shrunk. Whether between public and private hospitals or among private hospitals themselves, efforts to attract expectant mothers and boost delivery volumes have resulted in a zero-sum game rather than mutual growth. Breaking through this patient-acquisition bottleneck has become an unavoidable challenge that the women’s and children’s healthcare sector is striving to address. However, the long-term viability of women’s and children’s hospitals depends on far more than just solving the customer acquisition problem.

In the past, private women’s and children’s hospitals relied on various customer acquisition strategies, including search engine bidding, online and offline advertising, and marketing events, resulting in high costs. With declining fertility rates, these elevated customer acquisition costs no longer guarantee proportional returns. Consequently, such hospitals are gradually shifting their investments from “new patient acquisition” to “patient retention.”

“Cut unnecessary costs, especially marketing expenses; cancel any non-essential advertising and activities.” A relevant executive at an obstetrics and gynecology institution in Southwest China stated that the hospital’s current primary objective is to reduce costs and improve efficiency.

Women’s and children’s medical services primarily consist of obstetrics and gynecology (OB-GYN) and pediatrics, with OB-GYN further divided into gynecology and obstetrics. Among these, obstetrics is the most directly affected by fertility rates; pediatrics is characterized by a declining patient volume but growing individual demand; while gynecological services remain relatively stable in terms of demand, assuming no significant changes in the disease spectrum. Distinct customer profiles necessitate differentiated market strategies.

Expanding consumer offerings such as medical aesthetics, postpartum care centers, and postnatal recovery services has become standard practice

Expanding service offerings centered on obstetrics to address women’s health needs before, during, and after pregnancy is a key strategy for coping with the decline in delivery volumes. Specifically, it has become standard practice for women’s and children’s hospitals to establish medical aesthetics centers, postpartum rehabilitation centers, and postnatal care centers.

“Service offerings must evolve from purely medical care to encompass healthcare, wellness, beauty, and confidence,” stated Duan Tao, Chief Strategy Officer of Jinxin Fertility. “While the focus of medical care is on diagnosis and treatment, we are now expanding beyond childbirth services to cover full-lifecycle health management and promotion, postpartum confinement care, postpartum rehabilitation, medical aesthetics, as well as psychological and mental health. This significantly broadens the scope and reach of our services, extending from low-frequency essential needs to include medium- and high-frequency needs that are either essential or discretionary.”

Currently, women’s and children’s healthcare institutions under New Century Healthcare, Amcare, and Meihua Medical all offer medical aesthetics and postpartum rehabilitation services. UIB Healthcare separately operates obstetrics hospitals and postpartum care centers. In 2021, the listed company Changjiang Health also mentioned in its annual report that its subsidiary, Zhengzhou Shengma Obstetrics Hospital, would expand its postpartum rehabilitation area, steadily scale up, and gradually extend into beauty-related services.

Among these consumer-oriented services, postpartum care centers and postpartum rehabilitation can attract customers by leveraging their “medical-grade” attributes; medical aesthetics, which address women’s needs for restoring their appearance after childbirth, can also be well integrated with delivery-related services.

While expanding women’s consumer services can help mitigate the decline in obstetrics business, it is essential to emphasize synergy between core operations and diversified services.

Each of the aforementioned consumer service categories has a large number of specialized agencies operating within their respective niches. “For obstetrics and gynecology (OB/GYN) medical institutions, venturing into these areas is akin to developing a side business to compete with others’ core operations, especially since intense competition already exists within these niche sectors,” noted a relevant executive from an OB/GYN institution in Southwest China. He believes that although many players are moving in this direction, the extent to which they can succeed remains uncertain.

Taking medical aesthetics as an example, women’s and children’s hospitals primarily offer services such as dermatological aesthetics and anti-aging treatments. In contrast, the core competitiveness of specialized plastic surgery hospitals lies in surgical procedures, particularly complex reconstructive and cosmetic surgeries. These high-complexity services demand stringent qualifications and highly specialized personnel, areas where women’s and children’s hospitals face significant challenges in both implementation and excellence. Therefore, the expansion into medical aesthetics serves merely as a complementary extension to their core business, rather than direct competition with specialized institutions.

In Duan Tao’s view, maternal and child healthcare emphasizes clinical technical expertise and is led by hospitals and physicians, whereas postpartum care, postnatal recovery, and medical aesthetics are primarily professional consumer services focused on user experience and driven by consumers. “To integrate these two sectors, it is necessary to rebuild or restructure the management and professional service teams—ideally as independent teams or even through separate entities. The existing maternal and child healthcare and management teams should not be expected to operate under traditional models and mindsets.”

Unlocking Pediatric Potential to Meet Specialized Healthcare Needs

A decline in fertility rates leads to a reduction in the number of children; however, due to the wide age range of pediatric patients—from newborns to adolescents—the decrease in the pediatric population resulting from fewer births will manifest with a lag.

Currently, while obstetric medical resources are relatively saturated, pediatric medical resources remain scarce.

According to the Seventh National Population Census, as of November 2020, China had 254 million children aged 0–14, accounting for 18% of the total population. The number of children in both the 0–4 and 5–14 age groups increased. During the same period, there were approximately 163,400 pediatricians serving these 254 million children, resulting in an average of 0.65 pediatricians per 1,000 children. Using the national benchmark of 2.9 physicians per 1,000 population as a reference, there remains a substantial shortage of pediatricians, indicating significant room for growth in pediatric medical services.

Meanwhile, driven by policy guidance and heightened family health awareness and willingness to pay, market demand for child healthcare, health management, and specialized pediatric subspecialties has grown significantly.

“Pediatrics is a rapidly growing market and a key segment we focus on,” said Wang Yu, CEO of UIB Healthcare. From the perspective of actual business operations, medical or management services in pediatric ophthalmology, dentistry, growth and development, autism, and ADHD are experiencing rapid growth. Meanwhile, with advancements in medical technology, challenges in treating complex and severe pediatric conditions are being continuously overcome through multidisciplinary collaboration, presenting further growth opportunities for specialized children’s hospitals.

New Century Healthcare also stated in its 2021 annual report that, leveraging multidisciplinary pediatric collaboration as its competitive advantage, it would focus on the development of pediatric subspecialties and build a product and service chain centered around customers’ medical and health needs.

In fact, pediatric ophthalmology and dentistry represent blue-ocean markets that specialized chain providers in these fields are aggressively expanding. The long-term, multimodal nature of myopia control, along with dental care and orthodontics for all age groups, has created substantial market space for pediatric ophthalmology and dental services.

Therefore, amid the ongoing trend of specialization in pediatrics, there is room for growth in both medical and consumer-oriented segments. Maternal and child healthcare institutions can make strategic choices based on their existing areas of expertise and potential advantages.

Overall, the strategy for women’s and children’s healthcare has shifted toward expanding services around women’s health while continuously subdividing specialties with pediatrics at the core. This reflects a focus on deepening engagement within existing patient bases, as the previous strategy of constantly “acquiring new customers” for each specialty is no longer suited to the current market environment.

In 2021, the "Decision of the Central Committee of the Communist Party of China and the State Council on Optimizing Fertility Policies to Promote Long-Term Balanced Population Development" stated that a couple may have up to three children. The opening of the three-child policy has once again brought benefits to the field of women's and children's health. Since then, the national and local governments have successively introduced supporting measures such as special individual income tax deductions, housing subsidies, or childcare allowances to encourage childbirth.

“The three-child policy will not trigger a V-shaped rebound as the two-child policy did, but rather lead to an L-shaped gradual recovery,” Duan Tao noted. Since 2022, through data exchanges with obstetrics departments in hospitals across various regions, he has found that compared with the first quarter of 2021, both delivery volumes and the number of prenatal registration cards issued in the first quarter of 2022 continued to decline. However, the declines were mostly in single-digit percentages, with only a few cities experiencing drops exceeding 10%. “This represents a narrowing of the decline compared with the 10–20% drops seen in previous years.”

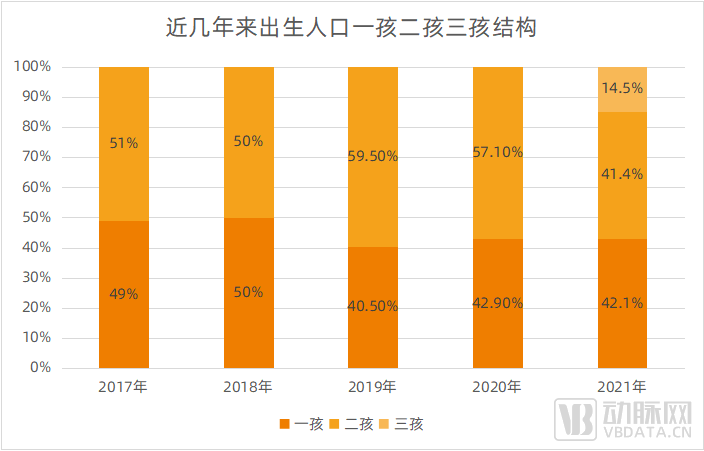

Recently, the "Statistical Bulletin on the Development of China's Health and Hygiene Undertakings in 2021," released by the National Health Commission, showed that among the 10.62 million births in 2021, second children accounted for 41.4%, and third or higher-order children accounted for 14.5%.

Proportion of First, Second, and Third Children Among Live Births in Recent Years. Data source: Official Website of the National Health Commission (Note: Data for the proportion of second children from 2017 to 2020 refers to the proportion of second children and above).

It is evident that the impact of population policies will be long-term. Combined with the previously observed proportion of second children, it can be seen that second and third children already account for a significant share, which can serve as a reference for guiding strategic shifts in the maternal and child healthcare market.

First, a high proportion of second and third children means that the field of women's and children's health has a higher percentage of "repeat customers," especially in obstetrics. Childbirth is no longer a "one-time" business, and reputation is becoming increasingly important.

“Customers will become more sophisticated, evolving from first-time mothers with little knowledge to experienced mothers of two or three children. This means that healthcare institutions must truly strengthen their core competencies by improving medical quality and patient satisfaction in order to prevail in competition,” said Wang Yu. He noted that during periods of rapid market growth, the focus should be on increasing visibility and capturing market share to quickly boost performance; however, when the market stabilizes or even declines, competition hinges on substantive capabilities.

Meanwhile, in first- and second-tier cities, fertility decisions are closely tied to household financial conditions; families choosing to have a second or third child typically possess strong purchasing power, which constitutes a natural advantage for the mid-to-high-end maternal and child healthcare sector. Hospitals positioned in this segment must therefore adapt to the objective market environment by prioritizing service quality and building a strong reputation.

Secondly, it is necessary to build competitive barriers through medical technology capabilities and discipline development.

Previously, private healthcare providers in the obstetrics and pediatrics sector primarily competed on service quality. Compared with the overcrowded conditions in public hospitals, private hospitals were highly favored by expectant and new mothers for their spacious environments and patient-centered care. Currently, however, as overall delivery volumes decline, public hospitals have also seen a reduction in patient load and are striving to attract expectant and new mothers by enhancing service quality and meeting personalized needs through options such as premium wards. Consequently, the service advantage of private hospitals has weakened, placing them on an equal footing with public institutions.

Meanwhile, given the higher proportion of second and third births and the corresponding increase in maternal age, expectant mothers place greater emphasis on delivery safety when selecting a hospital. These factors collectively indicate that high-quality service alone is no longer sufficient; it is essential to further prioritize enhancements in medical technology, academic proficiency, and related capabilities.

“In the end, public hospitals will also need to attract patients by improving services and building their brands, while private hospitals must enhance their management and technical capabilities.” Duan Tao believes that in the future, the true core competency of women’s and children’s hospitals will not lie in hardware and services, but in medical technology.

It is undeniable that in recent years, there have been frequent reports of maternity hospitals facing wage arrears and closures. Nor can it be denied that during the period of rapid market expansion, the industry witnessed numerous instances of irregular medical practices, overtreatment, and non-compliant advertising, some of which persist to this day. However, these issues represent only one facet of the industry.

“Market changes driven by fertility rates are both a challenge and an opportunity, enabling healthcare institutions to shift their focus from ‘volume’ to ‘quality,’ with more time and energy dedicated to the latter, while the market undergoes structural adjustments within its existing stock,” Duan Tao admitted.

The landscape of the maternal and child healthcare market is undergoing significant changes, with survival space being squeezed for non-compliant, small-scale, and fragmented medical institutions. Meanwhile, new entities continue to emerge. According to data from Qichacha, over 50 obstetric hospital operating entities and more than 230 maternal and child health hospital operating entities have been registered in the past year.

Expanding women’s and children’s medical institutions remains a growth strategy for some healthcare service groups.

In January 2022, after more than three years of preparation, Xuzhou Xingchen Women’s and Children’s Hospital opened its doors as one of the institutions under Fosun Health’s “Xingchen Initiative.” As Fosun Health’s specialized medical brand project focused on women’s and children’s health, the “Xingchen Initiative” aims to build a comprehensive health management system covering women’s entire life cycle—from growth and development, through reproductive years, to aging. It also provides scientific, professional, and personalized health management services for children and adolescents, including health check-ups, growth and development assessments, condition screening, and disease treatment.

In December 2021, construction commenced on Foshan New Century Huanhu Women’s and Children’s Hospital, a subsidiary of New Century Healthcare. As the first specialized hospital established by New Century Healthcare in the Guangdong-Hong Kong-Macao Greater Bay Area, it is designed as a fully digitalized smart hospital. With a total investment of RMB 500 million and a planned capacity of 200 beds, the hospital is positioned to provide high-end medical services, aiming to alleviate the local supply-demand imbalance in the premium healthcare sector.

Integrating women’s and children’s healthcare institutions remains a development strategy for some capital investors or industry players.

In June 2022, Alps Capital announced the completion of its controlling investment in Meihua Medical. Following the transaction, Alps Capital will accelerate Meihua Medical’s expansion from maternal and child health services to comprehensive health care for women across their entire life cycle, as well as family health services.

In October 2021, JINXIN FERTILITY acquired Jinxin Women and Children’s Hospital to integrate with its existing assisted reproductive technology services, implementing a full-lifecycle fertility service strategy.

Overall, two major service ecosystems are taking shape in the women’s and children’s healthcare sector: one characterized by regional expansion and service layering, and the other by industrial chain synergy spanning from assisted reproductive technology (ART) to maternity care and then to pediatrics. In the future, such integrated groups will become the backbone of the market; meanwhile, within the broader healthcare system, the value of private women’s and children’s medical services remains significant.