Three Common Pitfalls for Listed Companies Diversifying into Rehabilitation Healthcare

SANXING MEDICAL ELECTRIC

Provider of Integrated Smart Power Distribution and Consumption Solutions

Following the Wenchuan earthquake, modern rehabilitation medicine in general hospitals experienced a surge in development. Subsequently, as multiple rehabilitation services were gradually included in medical insurance reimbursement, it spurred substantial investment from private capital to establish specialized rehabilitation hospitals.

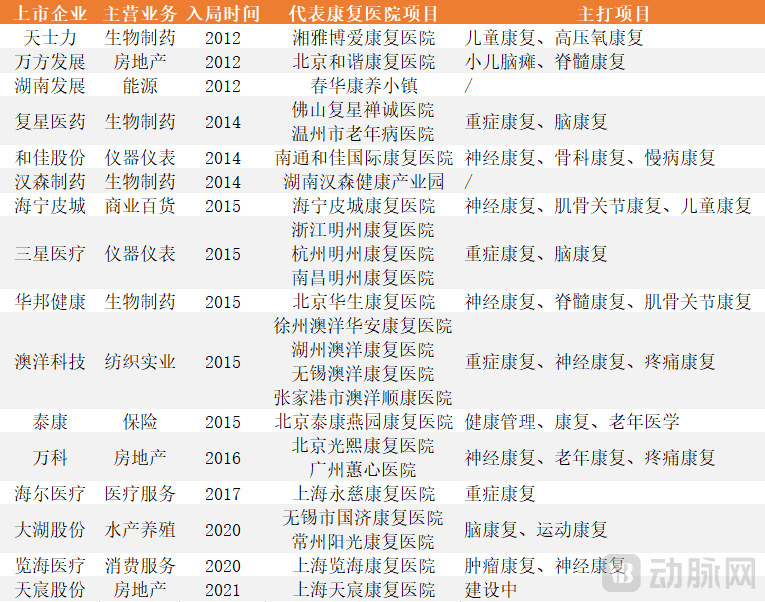

According to incomplete statistics, more than 20 listed companies have entered the rehabilitation hospital sector, many of them crossing over from unrelated industries. For instance, Haining Leather City, whose core business is leather trading; Dahu Shares, primarily engaged in aquaculture; Aoyang Technology, focused on textile fibers; and home appliance giant Haier, among others, have successively expanded into the rehabilitation medical industry, striving to capitalize on the broader health and wellness market. Samsung Electric, a controlled subsidiary under the Aux Group, directly changed its name to Samsung Medical in 2015 and acquired multiple hospitals to establish its presence in rehabilitation healthcare.

Some Listed Companies Enter the Rehabilitation Hospital Sector, Compiled by VCBeat Based on Public Information

The reason these listed companies have made such a choice is that rehabilitation is a medical field with relatively low entry barriers. According to data from a research report by Industrial Securities, the net profit margin of specialized rehabilitation hospitals ranks second only to ophthalmology, medical aesthetics, and dentistry, reaching 10.7%. In terms of investment costs, the per-bed investment for rehabilitation hospitals is only RMB 300,000–500,000, compared with RMB 500,000–1,000,000 per bed for general hospitals.

For cross-industry entrants, whether their aim is to secure real estate projects or to use rehabilitation as a springboard into the broader health and wellness sector, their entry undoubtedly reflects an optimistic outlook on the future of the rehabilitation field. However, development paces vary among these new players. What are the key pitfalls to avoid when establishing a rehabilitation hospital?

How to fully leverage various government policy incentives and subsidies to reduce costs is an issue that listed companies must take seriously.

For listed companies engaged in cross-sector rehabilitation, whether positioning rehabilitation hospitals as part of integrated medical and elderly care services or operating them on a purely commercial basis, rigorous cost control is essential. This includes actively striving to leverage favorable land policies, medical insurance policies, designated provider status for work-related injury insurance, and accreditation from the China Disabled Persons’ Federation.

Land policies vary by region and will not be discussed here. Instead, we begin with the commonalities in medical insurance policies. Listed companies often enter the market by focusing on critical care rehabilitation (represented by neurological rehabilitation), geriatric rehabilitation, and functional rehabilitation, primarily because these sectors are perceived to have higher value. However, many enterprises overlook the fact that the business model for critical care rehabilitation is built upon medical insurance coverage.

In simple terms, the implementation of cross-regional medical insurance settlement, coupled with reforms in DRG/DIP payment methods, has led to a concentration of the rapidly growing demand for neurosurgical treatments at top-tier tertiary hospitals. In the post-pandemic era, these tertiary hospitals have shifted their operational strategies toward strengthening their dominant specialties and improving gross margins, resulting in the spillover of rehabilitation services to external providers.

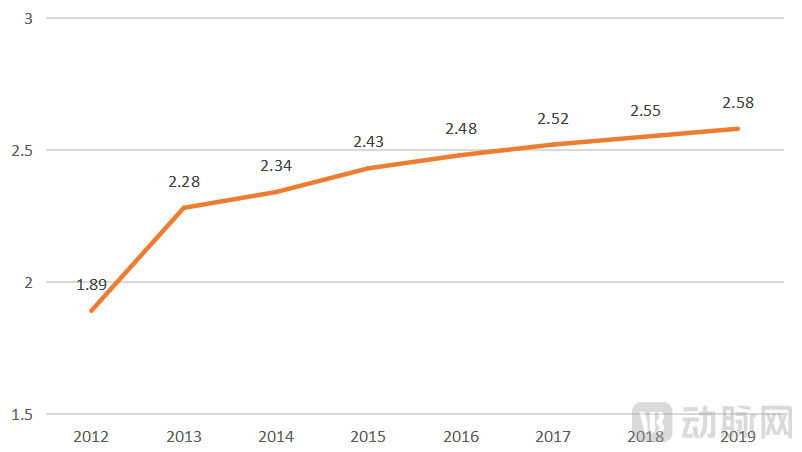

In recent years, cerebrovascular diseases, represented by stroke, have shown an explosive trend. According to the National Cerebrovascular Disease Big Data Platform, the age-standardized prevalence of stroke among individuals aged 40 and above in China rose from 1.89% in 2012 to 2.58% in 2019. This means that in 2019, the number of stroke patients aged 40 and above in China exceeded 17 million, with a one-year recurrence rate of 5.48%.

Stroke Prevalence Among Adults Aged 40 Years and Older in China, 2012–2019: Data from the National Cerebrovascular Big Data Platform

Furthermore, stroke mortality remains at a high level. According to data released by the Stroke Prevention and Control Engineering Committee of the National Health Commission, there were 17.8 million stroke patients aged 40 years and older in China in 2020, with 3.4 million new cases and 2.3 million deaths attributable to stroke that year. A 2019 survey indicated that the case fatality rate within one year after hospital discharge for stroke patients was 8.64%.

If stroke patients do not receive timely rehabilitation treatment after the acute phase, 30%–35% of them will progress toward disability and dementia. From a health insurance perspective, addressing the issue at its source can reduce subsequent healthcare expenditures.

In other words, to accommodate this spillover demand for critical care rehabilitation, facilities must be designated as medical insurance providers. Therefore, for rehabilitation hospitals, joining the national medical insurance scheme is an urgent and critical priority.

Many cross-industry enterprises have recognized this issue. For instance, Shanghai Lanhai Rehabilitation Hospital was included in the national medical insurance program by May 2022, just six months after its official opening in November 2021. In contrast, Beijing Guangxi Rehabilitation Hospital, under Vanke, was not enrolled in the medical insurance scheme until three years after commencing operations due to various reasons. Three years is sufficient time for a hospital to turn losses into profits, which is truly regrettable.

Designation as a designated institution by the Disabled Persons' Federation is also a policy benefit that can be pursued.

Taking the admission criteria for designated autism rehabilitation training institutions under Hubei Province’s Rehabilitation Assistance System for Children with Disabilities as an example, in addition to requirements concerning the institution’s nature, qualifications, and basic compliance items such as fire safety, hygiene, and general safety, functional requirements primarily mandate the availability of dedicated facilities, including assessment rooms, behavioral intervention rooms, and social functioning rooms.

For rehabilitation hospitals built in accordance with national standards, meeting the access requirements poses no difficulty. During the initial phase of hospital operations, when business volume is not yet saturated, undertaking such government-supported projects can help reduce operational costs and represents a viable option worth considering.

The same applies to designated medical institutions for work-related injury rehabilitation.

In the past, the underdevelopment of primary-level rehabilitation institutions led to a concentration of work-related injury rehabilitation patients in general hospitals, regardless of the severity of their conditions. Consequently, the limited rehabilitation resources available at tertiary medical institutions have become increasingly inadequate to meet the demand for work-related injury rehabilitation.

The shift in personal rehabilitation concepts has also led to an increase in the demand for work-related injury rehabilitation.

Previously, employers’ handling of work-related injury accidents was limited to reimbursement of medical expenses and monetary compensation. Injured workers, driven by considerations related to disability assessment and economic compensation, would even forgo rehabilitative treatment.

Currently, many injured workers are increasingly recognizing that functional rehabilitation and the restoration of work capacity are more important in the long term than financial compensation from employers. Coupled with policy coverage for occupational injury rehabilitation, such demands are gradually increasing.

Furthermore, due to the limited rehabilitation resources within tertiary medical institutions, patients with work-related injury rehabilitation needs after treatment are referred to qualified rehabilitation facilities for follow-up care. If rehabilitation hospitals can establish a two-way referral mechanism with higher-level medical institutions as a result, it would be beneficial for their subsequent operations.

For rehabilitation hospitals, undertaking such services can also fully utilize their idle medical resources and increase revenue.

Some rehabilitation hospitals accept medical insurance and other policy-related arrangements; data sourced from corporate websites and the China Disabled Persons' Federation.

Based on the review, the vast majority of rehabilitation hospitals have been integrated into the national medical insurance system, with only Beijing Huasheng Rehabilitation Hospital, which opened in May 2021, not yet connected for medical insurance settlement. However, there has been relatively less emphasis on obtaining designated status for work-related injury insurance and for services under the China Disabled Persons’ Federation. Tasly and Dahu Shares, as early cross-sector entrants, are among the few rehabilitation hospitals that have successfully integrated all types of policy-based designations.

It is worth noting that Xiangya Bo’ai has already validated its own business model, but has not yet succeeded in replicating this model.

For rehabilitation hospitals, securing these policy supports enables them to break even in approximately three years; otherwise, it would take more than five years, representing a significant disparity.

For a newly established rehabilitation hospital, site selection is a critical consideration, with the most crucial factor being its proximity to a general hospital.

For rehabilitation hospitals whose core business focuses on postoperative musculoskeletal rehabilitation and chronic pain management, the patient population is generally in a stable condition with limited need for urgent referrals. Consequently, proximity to general hospitals is not a critical requirement. Patients transferred from general hospitals to rehabilitation facilities are managed through dedicated coordination arrangements, making them relatively insensitive to distance.

Therefore, such rehabilitation hospitals not only have no particular requirements regarding the proximity of general hospitals but should, in fact, avoid locating near general hospitals with strong orthopedic departments.

For neurological rehabilitation services primarily serving patients covered by medical insurance, site selection must ensure the presence of at least one general hospital nearby. With support from their medical resources, patient safety needs can be met while also expanding channels for patient acquisition. Otherwise, the rehabilitation hospital would need to incur additional costs in this area.

Furthermore, site selection is closely tied to the hospital’s own positioning. Rehabilitation hospitals that adopt a mid-to-high-end strategy and rely primarily on inpatient revenue need to prioritize the creation of a therapeutic environment. In such cases, relatively remote locations with lower costs may well be a viable option. However, if the hospital’s positioning is more basic, with revenue dependent on outpatient services and patient inflow from surrounding communities, it is essential to assess the demographic characteristics of the nearby population, including population size, willingness to pay, and ability to pay.

For companies crossing over into the rehabilitation sector, there are also their own considerations. For instance, real estate developers may build rehabilitation hospitals as part of new property projects or revitalize existing vacant properties. In such cases, major site selection cannot be adjusted significantly; instead, efforts should focus on optimizing supporting facility design to reduce subsequent marketing costs.

Statistics on the Distance Between Some Rehabilitation Hospitals and Nearby General Hospitals, Data Sourced from Baidu Maps

From a purely data-driven perspective, those with a coverage radius exceeding 10 kilometers rank lower among the 21 rehabilitation hospitals included in the statistics. However, specific cases require individual analysis.

Although Xiangya Boai Rehabilitation Hospital is statistically located at a considerable distance from Xiangya Hospital, it was established through a collaborative partnership with Central South University. Beyond establishing a referral mechanism, Xiangya Hospital assumes comprehensive management of Xiangya Boai’s entire medical system and oversees its personnel. Furthermore, the two institutions share research and educational resources, and even their professional title promotion systems are integrated under unified management.

"While many rehabilitation hospitals are seeking to establish referral mechanisms with large general hospitals, Xiangya Bo’ai’s strategy of deeply integrating with Xiangya Hospital from its inception can be described as far-sighted."

The presence of Xiangya Bo'ai has somewhat impacted the local development of its competitors. For instance, Changsha Mingzhou Rehabilitation Hospital, under Sanxing Medical, chose to collaborate with the Second Xiangya Hospital of Central South University. In terms of location, Changsha Mingzhou is too far from the Second Xiangya Hospital and must also face competition from local rehabilitation hospitals that are closer to the Second Xiangya Hospital, such as Hunan Provincial Rehabilitation Hospital and Changsha Traditional Chinese Medicine Rehabilitation Hospital.

Although the location of Changsha Mingzhou is somewhat remote, the overall site selection strategy for the Mingzhou-affiliated rehabilitation hospitals has proven quite effective. While establishing collaborative mechanisms with local large-scale tertiary Grade A general hospitals, these facilities have ensured that their locations remain within a reasonable proximity to their partner institutions.

Furthermore, an interesting observation can be drawn from these statistics: large general hospitals in high-tier cities are key battlegrounds for competition. For instance, there are five rehabilitation hospitals located near the West Campus of Huashan Hospital, which underscores the significant spillover effect of top-tier (Grade A tertiary) hospitals on severe-case rehabilitation services.

In the future, Beijing Tiantan Hospital, Capital Medical University, also a leading representative of neurosurgery in China, may become a key market that private rehabilitation hospitals seek to capture.

Wealthy listed companies venturing into the rehabilitation hospital sector are not driven by the profitability of individual facilities, but rather aim to validate this business model for large-scale expansion. Consequently, they spare no effort in developing pilot projects, though their approach can sometimes appear overly aggressive.

In terms of equipment procurement, medical devices in rehabilitation hospitals differ from those in general hospitals, allowing for flexible choices based on the hospital’s operational strategy, business model, and the focus of its medical and technical teams.

For listed companies venturing into the healthcare sector, failing to make trade-offs based on projections and instead adopting bundled solutions will ultimately lead to equipment idleness, resulting in resource waste and delaying the break-even point.

Taking expensive MR and CT equipment as an example, the number of patients undergoing MR examinations is typically around 2% of the combined total of inpatients and outpatients, while the number of patients undergoing CT examinations is approximately 5% of that same combined total. The configuration of such equipment should be determined based on actual calculations tailored to the specific circumstances of each institution.

The root cause of this phenomenon lies in how listed companies position rehabilitation hospitals.

From the perspective of a sound business model, critical care rehabilitation backed by medical insurance has been proven to be a viable pathway. However, this is an arduous route that requires refined operational management to control costs, meet industry net profit margin standards, and ultimately achieve profitability.

Some cross-industry entrants prefer to position themselves in the mid-to-high-end segment, making substantial investments in infrastructure development, bed planning, equipment procurement, and staffing standards. However, post-launch operations often rely solely on reimbursement from the basic medical insurance system. The gradual, steady-payment nature of such insurance coverage delays the break-even point.

Positioning in the mid-to-high-end market is inherently sound. Beyond conventional elements such as luxury wards, imported equipment, and externally hired experts, high-end rehabilitation services also require appropriate hospital scale, service offerings, pricing structures, marketing strategies, and staffing systems.

In practical terms, there is no viable payment pathway for the high-end model; the small number of patients with out-of-pocket payment capacity is insufficient to sustain such a service system. Therefore, for publicly listed companies entering the rehabilitation sector from other industries, blindly pursuing a high-end strategy is not a rational choice from an operational perspective.

Furthermore, under the model of real estate developers diversifying into rehabilitation services, there is a tendency for rehabilitation care to become overly nursing-oriented. At present, for most real estate companies, whether developing senior living properties or incorporating rehabilitation hospitals as medical support for elderly care beds to establish so-called integrated healthcare and eldercare service systems, rehabilitation hospitals play an indispensable role.

However, real estate developers have yet to develop mature expertise in leveraging it effectively. Due to factors such as the low willingness of elderly patients to pay and the relatively low pricing of rehabilitation services, some established rehabilitation hospitals primarily offer basic care services, including physical therapy, tuina (Chinese therapeutic massage), and assisted exercise. As a result, fully equipped rehabilitation hospitals are being utilized merely as nursing homes, which not only prolongs the time required to break even but also diminishes the hospitals’ brand value.

In July 2022, Lanhai Medical issued an announcement regarding the termination of its stock listing and delisting, becoming the first among the many listed companies that had entered the rehabilitation industry to collapse.

Perhaps we can learn some lessons from its failure.

What left the deepest impression about Lanhai Medical was its establishment of Shanghai Lanhai Clinic and Yihe Lanhai Clinic in the most expensive luxury districts of Pudong and Puxi in Shanghai. From a communication perspective, Lanhai achieved excellent promotional results. However, from an operational standpoint, Lujiazui is one of the areas with the highest rents in China; even with a high-end medical positioning, it can only result in expenditures exceeding revenues.

When operating revenue fails to match capital input, the asset-heavy model is doomed to fail.

Lanhai Medical’s annual report notes that the construction cycle for medical projects undertaken by listed companies typically spans three to five years. Due to the impact of the pandemic, project timelines are expected to face further delays. Moreover, as most of the company’s projects are developed through self-construction, a considerable period is required to achieve profitability after completion. This entire process places significant strain on the company’s cash flow.

In other words, Lanhai had intended to pursue an aggressive, high-profile strategy to achieve rapid scale-up, but the reality is that the inherently slow nature of the healthcare industry precludes quick monetization, ultimately forcing it to make a dismal exit.

Winning Bid Prices for Selected Rehabilitation Hospital Construction Projects in China in Recent Years, Data Sourced from Caizhao.com

Data on winning bids for the construction of rehabilitation hospitals in China in recent years, sourced from procurement and bidding websites, show that despite regional variations in construction costs, the per-square-meter cost of Lanhai Rehabilitation Hospital far exceeds the national average for its peers. The path to premium positioning is by no means easy.

From a business model perspective, Lanhai positions itself as “specialty-focused with general support,” specializing in critical care rehabilitation with an emphasis on neurological and orthopedic rehabilitation. This approach is sound; however, it also incorporates “new rehabilitation” services—characterized by weaker medical attributes and stronger consumer-oriented features—into its business portfolio, including mild rehabilitation offerings such as treatment for neck, shoulder, and lower back conditions, spinal disorders, and sports injuries.

Light rehabilitation is a typical sub-sector of consumer healthcare that does not rely on medical insurance, whereas severe rehabilitation is dominated by medical insurance coverage. Balancing light and severe rehabilitation services within one’s own service system poses a significant test of operational capability.

The failure of Lanhai Medical has made it clear that without core competencies serving as a moat, relying solely on a high-end strategy can easily inflict fatal damage on a company when compounded by the impact of the pandemic.

Rehabilitation therapy differs from conventional treatment, characterized by its gradual, long-term, and dynamic nature.

Slow: The rehabilitation process is characterized by its prolonged duration. The average length of stay in general hospitals is 11 days, whereas in rehabilitation hospitals, it approaches one month. For some patients, the rehabilitation process may even extend over several months.

Common: The rehabilitation therapy process involves a high frequency of sessions, with some interventions required on a daily basis, which differs significantly from the treatment approaches in general hospitals.

Change: Rehabilitation is a constantly evolving, dynamic process. Therapists adjust the training regimen in real time based on the patient’s physical condition.

These three characteristics imply that, for rehabilitation hospitals to establish their core competitiveness, it is essential to conduct regional healthcare market research based on regional medical planning, clarify the scale and demand of the rehabilitation market, and thereby determine the hospital’s construction scale, professional positioning, discipline configuration, and policy benefits. Meanwhile, it is also necessary to improve the assessment and treatment service system centered on disease types.

For listed companies, having access to financing channels is merely an advantage; the top priority in building rehabilitation hospitals lies in transforming this advantage into core competitive strengths in rehabilitation. As for the development of the rehabilitation industry, the hope is not for another Lanhai Medical to emerge, but rather for more listed companies that are steady, grounded, and deeply committed to cultivating the rehabilitation sector.