Hillhouse-Backed Cryofocus Medtech Files for Hong Kong IPO: Can It Succeed in Both Electrophysiology and Tumor Ablation?

Cryofocus

Minimally Invasive Interventional Cryotherapy Device Developer

In July this year, Cryofocus submitted its prospectus to the Hong Kong Stock Exchange for the second time. Citigroup and Huatai International served as its joint sponsors.

This Shanghai-based company primarily focuses on the field of minimally invasive interventional cryotherapy, with its core products including bladder cryoablation devices, endoscopic anastomosis clips, and cardiac cryoablation products.

Prior to its initial public offering, Cryofocus secured investments from several prominent institutions, including Proxima Venture Partners, Hillhouse Capital, YuanSheng Venture Capital, and FutureX Capital. Specifically, YuanSheng Venture Capital held a 5.39% stake through Suzhou Xinjianyuan Phase II Venture Capital; Proxima Venture Partners held a 3.53% stake via Hangzhou Proxima and a 3.32% stake via Suzhou Proxima; and Hillhouse Capital held an 8.48% stake. Following the final round of financing before the IPO, Cryofocus’s post-money valuation was approximately RMB 2.093 billion.

Currently, among Cryofocus’s three core products, only the cryoablation device for bladder cancer has received regulatory approval. The company’s primary revenue is derived from surgical auxiliary consumables, specifically pulmonary nodule localization needles and single-port multi-channel laparoscopic access systems. Revenue from the sale of these surgical auxiliary consumables amounted to RMB 22.426 million in 2021 and RMB 6.321 million in the first four months of 2022. In 2020, 2021, and the first four months of 2022, Cryofocus reported net losses of RMB 159 million, RMB 126 million, and RMB 30 million, respectively, with these losses primarily attributable to research and development expenditures.

Cryofocus’s main competitor, MicroPort EP, is also in the final stretch toward its IPO. MicroPort EP has successfully completed registration on the STAR Market, plans to raise RMB 1.01 billion, and had a post-money valuation of RMB 4.8 billion in its previous funding round.

MicroPort EP selected the route of radiofrequency ablation combined with 3D mapping in the electrophysiology field, while also laying out cryoablation capabilities. Cryofocus opted for the cryoablation route and simultaneously deployed PFA technology; however, Cryofocus’s valuation is less than half that of MicroPort EP.

With the advent of PFA technology, interest in cryoablation for cardiac electrophysiology has waned. As Cryofocus races toward its IPO, what potential remains for cryoablation technology? VCBeat (WeChat ID: vcbeat) breaks down Cryofocus’s prospectus.

Cryofocus was established in 2013. During its first six years, the company focused exclusively on cryoablation therapy for atrial fibrillation within the field of cardiac electrophysiology.

Atrial fibrillation (AF) is one of the most common clinical arrhythmias, with approximately 10 million patients in China. Severe conditions caused by AF, such as thromboembolic events (e.g., stroke, mesenteric artery embolism, and limb artery embolism) and heart failure, impose a substantial disease burden.

The electrophysiological treatment of atrial fibrillation has long been marked by a “fire and ice” debate, pitting cryoablation against radiofrequency ablation. Cryofocus is betting on cryoablation.

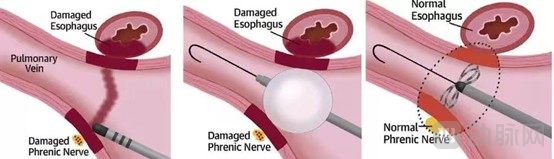

Cryogenic ablation catheters, used in conjunction with cryoablation systems, deliver ablative energy to tissues, causing a rapid temperature drop around the target site and thereby damaging or destroying abnormal cardiomyocytes in that region. In contrast, radiofrequency ablation induces necrosis of atrial tissue through elevated temperatures, forming circumferential scar tissue that helps restore regular cardiac rhythm.

Reports on the use of cryoablation for treating arrhythmias date back to the 1970s; however, it was not until 2003 that a cryoballoon catheter system suitable for pulmonary vein isolation became available.

Cryoablation was previously regarded as an innovative procedure. Its most significant advantage over radiofrequency ablation lies in its operational simplicity. Although cryoablation has been available for many years, radiofrequency ablation remains the mainstream option in terms of market performance.

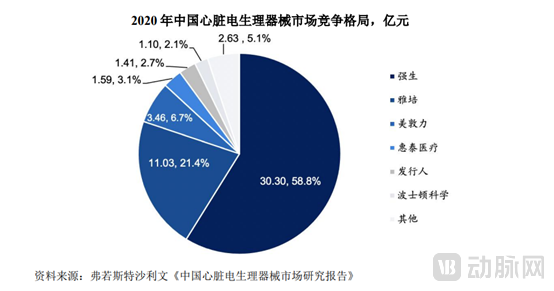

The world’s first cryoballoon system for the treatment of paroxysmal atrial fibrillation was launched by Medtronic in the United States in 2010. Medtronic’s cryoballoon ablation product is also the only one commercially available in China. However, Medtronic holds less than a 10% market share in China, with the market still dominated by Johnson & Johnson and Abbott in the field of radiofrequency ablation.

The Battle Between Cryoablation and Radiofrequency Ablation Continues, but Market Focus Has Shifted to Pulsed Field Ablation (PFA) Technology Beyond the “Ice and Fire” Duel. The market share of cryoablation may also be eroded by pulsed field ablation (PFA) technology. As technological paradigms shift, electrophysiology companies worldwide are actively deploying PFA technologies, including Medtronic, the former leader in cryoablation.

Even without PFA being commercially available, the proportion of cryoablation procedures remains significantly lower than that of radiofrequency ablation, based on current surgical volumes.According to Cryofocus’s prospectus, a total of 81,900 atrial fibrillation ablation procedures were performed in China in 2020, including 9,800 cryoablation cases and 72,100 radiofrequency ablation cases. The number of cryoablation procedures for atrial fibrillation in China increased from 2,300 in 2016 to 9,800 in 2020. The proportion of cryoablation among all atrial fibrillation ablation procedures rose from 7.0% in 2016 to 12.0% in 2020, and is projected to reach 27.6% by 2030.

The global market growth rate for cryoablation in atrial fibrillation is lower than that of the domestic market.According to Cryofocus’s prospectus, the global market size for atrial fibrillation cryoablation catheters increased from USD 726.6 million in 2016 to USD 1,201.3 million in 2020, representing a compound annual growth rate (CAGR) of 21.2%, and is projected to reach USD 7,735.0 million by 2030. In China, the market size for atrial fibrillation cryoablation catheters grew from RMB 48.4 million in 2016 to RMB 255.0 million in 2020, with a CAGR of 51.5%.

Why is the market share of cryoballoons relatively low? In terms of advantages, compared with radiofrequency ablation, cryoablation enables simultaneous treatment of all target sites in a single procedure, making the surgery simple and efficient and, to some extent, shortening operative time. However, current indications for cryoablation are limited; the design of cryoballoons targets only the pulmonary vein ostia, and they are primarily used for atrial fibrillation ablation, particularly for paroxysmal atrial fibrillation.

The performance of cryoballoons in China, coupled with the emergence of pulsed field ablation (PFA) technology, has cooled the domestic cryoballoon market. Most companies that had deployed cryoballoon products have since diversified into other product lines, and Cryofocus is no exception.

Based on Cryofocus’s product pipeline, the company has also entered the pulsed field ablation (PFA) space. Meanwhile, Cryofocus diversified its previously single-product portfolio through an acquisition in 2020. At the end of 2020, Cryofocus completed a strategic integration with Shengjie Kang, which specializes in tumor cryoablation and endoscopic/laparoscopic minimally invasive procedures. This integration repositioned Cryofocus as a minimally invasive cryoablation therapy platform.

Cryofocus and Shengjie Kang share the commonality of possessing cryotechnology platforms. Cryofocus’s cryoablation technology is applied in cardiac electrophysiological ablation, whereas Shengjie Kang is the earliest company in China to develop cryoablation technology for intraluminal tumors. Its core product, the “Transnatural Orifice Tumor Cryoablation System,” enables non-invasive tumor treatment via natural human body passages such as the esophagus, stomach, colorectum, bladder, and cervix. In addition, Shengjie Kang offers medical consumable products, including a multi-channel laparoscopic surgical access system and pulmonary nodule localization needles.

The integration of the two companies has expanded the potential applications of cryoablation technology.

Another major market segment with the greatest potential for cryoablation technology is the tumor interventional ablation market.

Tumor ablation primarily includes thermal ablation (radiofrequency ablation/microwave ablation), cryoablation, and emerging techniques such as combined cryo-thermal ablation and irreversible electroporation ablation. Cryoablation achieves focused ablation of the target site by performing freeze-thaw cycles in the vicinity of the lesion.

Cryoablation can be used to treat pain and other symptoms associated with the spread of abnormal tissue. When the risks of surgical tumor resection are prohibitively high, cryoablation balloons can be employed to alleviate cancer-related symptoms and may also serve as part of a comprehensive multimodal treatment regimen. Therefore, cryoablation is beneficial for patients who are not candidates for surgical tumor removal.

Compared with other ablation modalities, cryoablation offers multiple advantages, such as the use of local anesthesia, reduced pain, and preservation of tumor immunogenicity. Furthermore, the frozen zone created by cryoablation has well-defined boundaries and uniform temperature, thereby facilitating monitoring of the ablation site.

Tumor cryoablation products marketed in China are categorized into two types: percutaneous and transnatural orifice.

Currently, products commercialized in China utilize cryoablation catheters inserted percutaneously into the body to freeze and thaw target tissues, a procedure that involves making incisions in the skin. Key players in the percutaneous cryoablation market include Siemens, Haieria, Boston Scientific, Guided Medical, and IceCure Medical. The indications for these companies’ products are broad, covering breast, prostate, kidney, and liver cancers, among others.

The key distinction between Cryofocus and its competitors lies in the approach: while products from Siemens and Boston Scientific are delivered via percutaneous intervention, Cryofocus’s cryoballoon is administered through natural orifices. The cryoballoon can be inserted via a resectoscope or cystoscope sheath, thereby preventing bladder wall injury and reducing the risk of tumor dissemination.

Although Cryofocus’s cryoballoon ablation system for bladder cancer is an exclusive product, the incidence of bladder cancer in China increased from 77,100 cases in 2016 to 85,700 cases in 2020, indicating that the patient population remains relatively small. Market adoption of this product is expected to accelerate after more indications are approved.

The third major application scenario of cryoablation is respiratory intervention.Currently, interventional cryoablation for the respiratory system includes two categories: spray cryotherapy and bronchoscopic cryoballoon ablation. The currently approved products for respiratory interventional cryoablation are from Erbe and Beijing Kulang. Through bronchoscopy, cryoprobes can be used to remove foreign bodies, mucus plugs, necrotic tissue, and benign and malignant tumors, as well as to perform biopsies.

According to Frost & Sullivan, the global market size for interventional cryotherapy catheters for respiratory diseases has steadily grown from USD 2.5 million in 2016 to USD 4.5 million in 2020, representing a compound annual growth rate (CAGR) of 16.4%, and is projected to grow rapidly to USD 2,032.3 million by 2030. The market size for interventional cryotherapy catheters for respiratory diseases in China has also shown an upward trend. According to Frost & Sullivan, it increased from RMB 0.9 million in 2016 to RMB 2.1 million in 2020, with a CAGR of 24.4%. With the development of new technologies, this market is expected to expand further. According to Frost & Sullivan, the market size for interventional cryotherapy catheters for respiratory diseases in China is expected to reach RMB 109.8 million by 2025.

Cryofocus has also applied cryoablation to renal denervation (RDN). MicroPort EP has likewise entered this sector, but it adopts a radiofrequency ablation approach, as does Medtronic, the leader in the RDN field. Whether cryoablation can deliver superior outcomes in RDN remains to be validated by further clinical data.

Although cryoablation has a wide range of application scenarios, similar to the field of cardiac electrophysiology, its application in other areas also faces competition from multiple energy sources. Cryoablation technology needs to identify the disease indications and products that best leverage its advantages.

Recently, Cryofocus and MicroPort EP successively launched their initial public offerings (IPOs), highlighting the strong momentum in the cardiac electrophysiology sector. Previously, Huitai Medical, another player in the cardiac electrophysiology track, successfully listed on the STAR Market. The IPOs of these three companies are expected to inject greater confidence into the cardiac electrophysiology market.

In the primary market, several electrophysiology companies secured financing over the past year, including Jinjiang Electronics, Xuanyu Medical, Antike, Xinuopu, Aikemai, and Zhouling Medical, each raising over RMB 100 million.

The electrophysiology atrial fibrillation ablation market is characterized by rapid growth and a high proportion of imports, leaving significant room for the development of domestic enterprises. However, the dominant positions of industry leaders such as Johnson & Johnson and Abbott remain unshakable. According to a research report by Frost & Sullivan, the market share of domestically produced electrophysiology medical devices in China was only 9.6% in 2020, with a localization rate of less than 10%, indicating a clear advantage held by imported manufacturers.

Medtronic and Boston Scientific are also strengthening their presence in the electrophysiology field, channeling substantial revenue into cardiac electrophysiology. The pulsed field ablation products of Medtronic and Boston Scientific are expected to receive regulatory approval in China.

Therefore, domestic enterprises face equally significant challenges. Only by building a complete “system + equipment + consumables” solution can Chinese electrophysiology manufacturers achieve sufficient competitiveness in their product portfolios.

Cryofocus’s presence in another赛道—tumor ablation—is equally promising. According to data from Frost & Sullivan’s analysis report, the market size of China’s tumor ablation industry (calculated based on hospital charging prices) increased from RMB 1.88 billion in 2016 to RMB 3.92 billion in 2021. The tumor ablation industry still has broad room for growth in the future.

Currently, China performs approximately 300,000 tumor ablation procedures annually. Thermal ablation, primarily utilizing microwave and radiofrequency technologies, accounts for 80% of the entire ablation market, while cryoablation comprises approximately 10%. The localization rate for microwave ablation devices is relatively high. In the primary market, companies such as Haijieya, Nanjing Yigao, and Ruidi Biology have secured substantial financing, suggesting that this sector is poised to produce more publicly listed enterprises.

The application of cryoablation technology reveals that market acceptance of a technology is subject to various uncertainties. Successful commercialization requires seizing the optimal timing window, and in the rapidly evolving medical market, it is essential to ensure that products do not suddenly fall behind.

References:

A Comprehensive Overview of the Tumor Ablation Market — Siyu MedTech

Cryofocus Medtech Prospectus