NuosiGe (R&G PharmaStudies) Debuts on ChiNext as a Rising Clinical CRO Backed by Legend Capital, IDG Capital, and Hillhouse

“The unfinished laboratory contained only towering piles of unopened wooden crates, yet weekly expenditures had already reached $750 million.”

In *The Billion-Dollar Molecule*, American journalist Barry Werth vividly depicts the hardships faced by the newly founded Vertex Pharmaceuticals during the capital winter of 1989. This rare bestseller in the century-long history of pharmaceutical development offers a glimpse into how time-consuming and labor-intensive new drug research and development can be.

However, from a commercial perspective, this is a long industrial chain capable of sustaining countless wealth-creation myths. From Labcorp, IQVIA, and Charles River Laboratories to WuXi AppTec and Tigermed, nearly every segment related to new drug clinical trials has the potential to spawn publicly listed companies. R&G PHARMA STUDIES CO.,LTD., which made its debut on the ChiNext board today, emerged from within this very industrial chain.

R&G PHARMA STUDIES CO.,LTD. Officially Listed on the ChiNext Board

Today, R&G PHARMA STUDIES CO.,LTD., a star domestic clinical CRO enterprise, officially listed on the capital market. Its stock opened at 78.89 yuan and subsequently surged by over 20%, reaching a market capitalization of nearly 6 billion yuan. As a leading company that has been deeply engaged in the popular CRO sector for many years, R&G PHARMA STUDIES CO.,LTD. is backed by numerous top-tier healthcare investment institutions.

R&G Pharma Studies Shares Surge at Open

R&G Pharma Studies was established in 2008. In 2018, it attracted investment from renowned firms such as Legend Capital and JF Capital. In 2019, it further secured funding from IDG Capital, Huimei Capital, Hillhouse Capital, and Shenzhen Capital Group. During this period, the company’s business scale and revenue expanded rapidly.

As a professional investment institution that has accompanied R&G Pharma Studies throughout its growth journey, Wang Junfeng, Co-Chief Investment Officer of Legend Capital, stated, “Congratulations to R&G Pharma Studies on its successful IPO! As a veteran in China’s clinical CRO sector for drug development, R&G has long provided end-to-end clinical CRO services to innovative pharmaceutical companies both domestically and internationally. With an international perspective, a renowned team of experts, and a high-quality service system, the company’s successful listing marks the starting point of a new long march. We are optimistic about R&G’s long-term development potential and look forward to its future success.”

In fact, Legend Capital has made systematic investments in the CRO/CDMO sector. In addition to R&G PHARMA STUDIES CO.,LTD., it has invested in a number of new drug R&D CRO/CDMO companies, including WuXi AppTec, WuXi Biologics, Pharmaron, Bellen (Liuhe Ningyuan) Group, Clinipace China, Saifu Pharma, Dipeptide Biologics, Xihua Testing, Duchuang Pharma, ZhiXiang Biologics, BioDuro, and Simcere Diagnostics.

As of the IPO, IDG Capital was R&G PHARMA STUDIES CO.,LTD.’s largest institutional investor. Its related investors stated, “We are deeply impressed by R&G’s highly professional core management team, many of whom are experts in the medical field and wield significant influence within the industry. The company boasts robust clinical research capabilities, extensive experience, and a leading scale in the sector. We believe that R&G will play a pivotal role in advancing the innovative drug industry in the future.”

Unlike multinational pharmaceutical companies with market capitalizations often reaching hundreds of billions of dollars, CROs have smaller market caps and lower profiles, yet they serve as key driving forces behind star pharmaceutical companies and blockbuster drugs.

According to Frost & Sullivan, global pharmaceutical R&D investment totaled $165.1 billion, $174.0 billion, and $182.4 billion in 2017, 2018, and 2019, respectively. Of these amounts, expenditures on outsourced services (i.e., CROs) were $52.5 billion, $57.9 billion, and $62.6 billion, respectively. In other words, approximately one-third of annual pharmaceutical R&D spending is allocated to the CRO industry, which is growing at a rate significantly higher than that of pharmaceutical R&D itself.

Based on the different service stages, CROs are further divided into clinical CROs and preclinical CROs.

Clinical CROs refer to professional third-party organizations that provide outsourcing services related to the preparation, conduct, and summary of clinical trials during the drug clinical trial phase. International examples include LabCorp and IQVIA, while domestic examples include Tigermed.

Preclinical CROs, as counterparts to clinical CROs, are also professional third-party service providers primarily responsible for early-stage drug development activities such as molecular discovery, bioanalysis, and safety evaluation. Representative companies include Charles River Laboratories internationally and WuXi AppTec in China.

Similar to various third-party service providers, the existence of Contract Research Organizations (CROs) has significantly helped pharmaceutical companies reduce R&D costs. These companies no longer need to build large professional development teams or tie up substantial capital in rapidly iterating life science equipment. Abroad, as CROs have gradually matured, large pharmaceutical companies only need to retain a small core of technical experts to monitor the latest trends in drug development and clinical technologies, while small biotech firms can focus more intently on their areas of expertise, achieving breakthroughs through specialized concentration.

To date, drug safety evaluation, the earliest emerging segment, has become the CRO service with the highest penetration rate, with an outsourcing rate of approximately 60%. However, since costs associated with drug safety evaluation account for a small proportion of total new drug R&D expenditures, the resulting CRO market size is relatively limited. Among various CRO services, clinical CROs represent the largest market segment. According to Frost & Sullivan data, the market size of clinical CROs exceeded $50 billion in 2020, accounting for the absolute majority of the entire CRO market.

The underlying reason is that clinical CROs correspond to the clinical trial phase of new drug development, which involves the largest capital investment and the highest risk of failure for pharmaceutical companies. Data show that more than half of the total costs of new drug development are incurred during Phase I–III clinical trials.

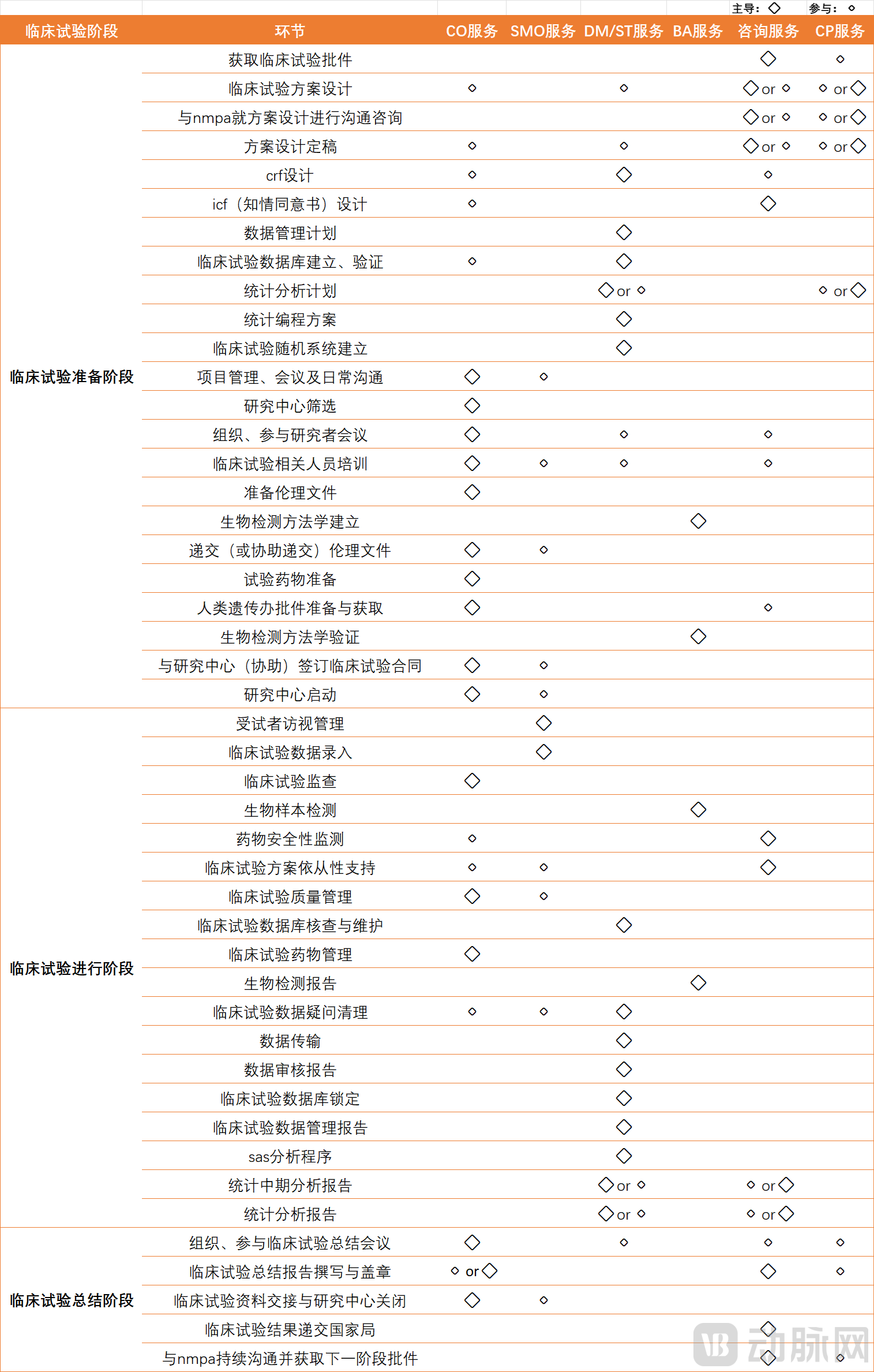

In this process, based on different business focuses, professional service providers further segment clinical CRO services into multiple business sectors: clinical trial operations (CO) services, which excel in clinical resources; site management organization (SMO) services, which specialize in medical expertise; data management and statistical analysis (DM/ST) services, which are strong in data analysis; bioanalytical (BA) services, which leverage biological expertise for biological sample testing; and consulting services, which focus on regulatory compliance. This segmentation allows them to either lead or participate in the advancement of processes within specific service stages. Wu Jie, Chairman of R&G PHARMA STUDIES CO.,LTD., stated in a media interview that the industrial trend of CROs is characterized by increasingly higher demands for professionalism and greater reliance on R&D strategy and top-level design.

Clinical CRO Processes

In particular, certain critical steps often require the collaborative efforts of at least two business modules. For instance, the design of informed consent forms is led by both the consulting service agency and the CO service team, while training for personnel involved in pediatric clinical trials is led by the CO service team, with active participation from SMO, DM/ST, and the consulting service team.

Abroad, the clinical CRO industry has reached a considerable scale after nearly 40 years of development, with leading players such as LabCorp and IQVIA typically offering users one-stop clinical CRO services. In contrast, domestic clinical CRO companies in China are relatively small yet specialized. Apart from large-scale domestic leaders like Tigermed, most start-up clinical CRO firms lack the capacity to cover a full spectrum of business lines and tend to focus on deepening their expertise in one or several specific segments.

In fact, in addition to the aforementioned capabilities in clinical resources, data analytics, and medical expertise, the focus on clinical CRO service requirements varies across different stages even after entering the clinical trial phase. For instance, Phase I clinical trials, which are conducted in healthy volunteers, have relatively lower requirements for patient enrollment and drug administration but place a significant premium on the CRO’s operational efficiency. In contrast, Phase II–III clinical trials involve complex protocol designs and stringent enrollment criteria, with the potential occurrence of serious adverse events, thereby testing the CRO’s clinical trial experience and medical prowess.

On the other hand, as foreign clinical CROs such as LabCorp and IQVIA quote relatively high prices, domestic boutique clinical CROs have entered the market by offering cost-effective services. After continuously accumulating project experience, they are also expanding their business boundaries. For example, while R&G PHARMA STUDIES CO.,LTD.’s traditional strength lies in Coordination Organization (CO) services, it has accelerated its expansion into Site Management Organization (SMO) services and Data Management/Statistical Analysis (DM/ST) services in recent years.

Next, let’s examine R&G PHARMA STUDIES CO.,LTD.’s competitiveness in the clinical CRO market.

As a company built on delivering professional services, service capability is arguably the most critical factor in assessing operational performance and potential. For clinical CROs, clients’ willingness to repurchase and the value of signed but not yet executed orders often reflect the quality of past service delivery, while core employee retention rates can indicate whether the company can sustain high-level service capabilities in the future. Established a few years later than peers such as Tigermed and Boji Medicine, R&G PHARMA STUDIES CO.,LTD. has emerged as a dark horse in China’s clinical CRO industry, rapidly building competitive advantages through its strong core team and professional expertise.

The institution offers a comprehensive, full-spectrum suite of clinical CRO services, including CO, SMO, DM/ST, BA, and consulting services. This end-to-end service capability is critical for maximizing client reach. Its therapeutic coverage spans oncology, cardiovascular disease, endocrinology, respiratory disorders, and other areas. The company collaborates with renowned medical institutions in China, such as Xiangya Hospital, Peking Union Medical College Hospital, Beijing Anzhen Hospital, and West China Hospital of Sichuan University. To date, it has supported over 3,300 clinical trial projects for approximately 750 clients both domestically and internationally. The experience and capabilities accumulated through these engagements have laid a solid foundation for R&G PHARMA STUDIES CO.,LTD. to further enhance its service delivery.

Key Account Repurchase.According to the prospectus, CO services were R&G PHARMA STUDIES CO.,LTD.’s primary revenue source during the reporting period, consistently accounting for more than 50% of total revenue. SMO services ranked second, contributing nearly 20% of revenue. Although customers with annual order values below RMB 1 million constituted the majority in number among the company’s cumulative base of 750 clients, R&G PHARMA STUDIES CO.,LTD. secured several key repeat purchases from major clients with annual per-customer spending exceeding RMB 20 million.

According to the prospectus, in 2017, R&G Pharma Studies entered into a collaboration with Henlius Biotech to provide services related to the Phase III clinical trial of the latter’s investigational drug, RG01W-2211. Two years later, Henlius Biotech awarded R&G Pharma Studies the contract for the Phase III clinical trial of another investigational drug, RG01W-2732. Through these two projects, R&G Pharma Studies generated nearly RMB 130 million in revenue between 2019 and 2021. In addition, over the past two years, R&G Pharma Studies also secured SMO (Site Management Organization) and DM/ST (Data Management/Statistical Analysis) orders from Henlius Biotech, generating more than RMB 10 million in revenue.

In addition to Henlius, Kelun Pharmaceutical has also been procuring CRO services from R&G PHARMA STUDIES CO.,LTD. for several consecutive years. Since 2019, R&G PHARMA STUDIES CO.,LTD. has successively secured some small-value orders from Kelun Pharmaceutical. By 2021, the company had won two clinical operations (CO) service contracts from Kelun Pharmaceutical, namely RG01-04560 and RG01-04810, generating over RMB 23 million in revenue.

Regarding subsequent orders.According to the prospectus, R&G PHARMA STUDIES CO.,LTD. recorded advances from customers or contract liabilities of RMB 139 million, RMB 116 million, and RMB 150 million in 2019, 2020, and 2021, respectively. Given that its revenues during the same period were RMB 423 million, RMB 484 million, and RMB 608 million, respectively, it is evident that the contracts signed in advance by customers were sufficient to generate a subsequent quarter’s worth of business volume for the company.

Core Personnel.For clinical CROs, business development talent is undoubtedly the most critical resource. Each clinical CRO has its own insights into how to retain and efficiently leverage such talent amid fierce market competition. Over the past 14 years, R&G PHARMA STUDIES CO.,LTD. has attracted top industry professionals from organizations such as Pfizer, Novartis, Johnson & Johnson, Takeda, and the U.S. FDA. These experts bring extensive experience in clinical development and regulatory review, with many having participated in the formulation of multiple national and industry standards. This enables them to better understand the pain points pharmaceutical companies face in clinical trials and propose targeted solutions.

Furthermore, R&G Pharma Studies has built a stable and expanding business execution team through an attractive compensation system and career growth opportunities. Regarding the compensation structure, in terms of salary income, R&G’s average employee compensation over the past three years was lower than that of Tigermed, the leading domestic CRO, but slightly higher than that of Boji Medicine, a peer in the same industry. In addition to regular annual and ad hoc salary adjustments, R&G has also established an employee stock ownership platform to provide equity incentives for certain sales personnel.

Certainly, the accumulation of project experience is key to optimizing service capabilities for clinical CROs, and this holds true for practitioners as well. When choosing a platform, core business personnel consider not only income but also growth potential.

This pertains to personnel efficiency. According to the prospectus, R&G PHARMA STUDIES CO.,LTD. had 1,876 employees on its roster in 2021. Excluding 29 sales personnel and 96 staff in management and business support departments, all remaining employees were engaged in core business lines. Based on the service of 1,754 various clinical trial projects and the generation of RMB 608 million in revenue in 2021, R&G was able to assign at least one dedicated staff member to each project. The average revenue per business employee was approximately RMB 340,000, with both figures showing a slight increase during the reporting period.

As mentioned at the beginning of the article, clinical CROs constitute the largest outsourcing market in the pharmaceutical industry, and with the continuous expansion of downstream demand for new drug development, the clinical CRO sector remains on a rapid growth trajectory.

It is generally believed that the total size of the CRO industry can be estimated by multiplying the total R&D investment in the pharmaceutical industry by the outsourcing penetration rate. Pharmaceutical companies are further divided into large pharmaceutical enterprises and small-to-medium-sized biotech firms; the former’s R&D spending depends on drug sales revenue, while the latter’s depends on the amount of financing raised.

In recent years, China’s pharmaceutical industry has been gradually transitioning from the production and sales of generic drugs to innovative drugs. As the sector evolves from low-end imitation to research and development (R&D) innovation, investment in pharmaceutical R&D has continued to grow, with a growth rate far exceeding the global average. Meanwhile, multinational pharmaceutical companies have increased drug exports to China to tap into the Chinese market and have successively established R&D centers in the country, thereby generating substantial demand for clinical trials of imported drugs.

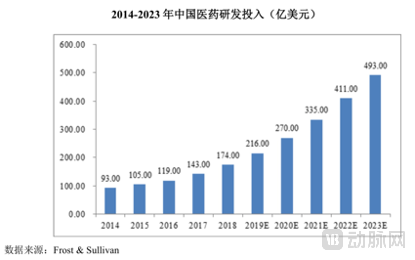

According to Frost & Sullivan’s statistics and projections, China’s pharmaceutical R&D expenditure was $9.3 billion in 2014 and grew to $17.4 billion in 2018, representing a compound annual growth rate (CAGR) of approximately 17.0%. From 2018 to 2023, China’s pharmaceutical R&D expenditure is projected to grow at a CAGR of 23.1%, reaching $49.3 billion. During this period, the growth rate of China’s pharmaceutical R&D expenditure was approximately five times the global average.

As a result, China’s clinical CRO industry has achieved substantial growth, giving rise to leading firms such as Tigermed, Boji Medicine, Primis, and R&G Pharma Studies. According to Frost & Sullivan’s projections, the potential for outsourced drug R&D in China will increase from 34.7% in 2019 to 46.7% in 2023, with the corresponding clinical CRO market size expanding from USD 3.2 billion to USD 13.3 billion.

For R&G PHARMA STUDIES CO.,LTD., listing on the capital market has undoubtedly elevated its business operations to a new and higher starting point. The same holds true for China’s clinical CRO industry: emerging demands continue to pour in, and the new regulatory framework imposes stricter requirements on quality and efficiency, thereby offering better growth opportunities for professional teams deeply entrenched in this field. We also look forward to the continuously expanding clinical CRO market fostering star enterprises with international influence.