Navigating Uncertainty in China's Medical Device Market: Seeking Certainty Amid Volatility

Editor’s Note: This article is from JD Capital, and VCBeat has obtained the right to republish it.

Under the new macroeconomic backdrop, how should private equity (PE) firms properly view each current “hot trend”? What investment logic can truly withstand market cycles?

We will share JD Capital’s research and investment insights across various industry sub-sectors on an irregular basis through “JD Capital Insights,” consistently adhering to growth-oriented industry research grounded in certainty to seize corporate growth investment opportunities.

The capital markets have once again opened a door for medical device companies. In June 2022, the Shanghai Stock Exchange released the "Guidelines for the Application of Listing and Issuance Review Rules on the STAR Market No. 7—Application of the Fifth Set of Listing Standards by Medical Device Companies" (hereinafter referred to as the "Guidelines"). This set of listing standards does not require companies to be profitable, nor does it even require them to generate revenue; however, it imposes stringent requirements on R&D capabilities and valuation levels. The favor shown toward medical device companies is closely tied to their market potential. Data shows that China's medical device market size is expected to exceed one trillion yuan by 2023. For comparison, in 2020, the global medical device industry had a market size of $477.4 billion, representing a year-on-year growth of 5.63%; meanwhile, China's medical device market size was approximately RMB 734.1 billion, with a year-on-year growth of 18.3%. In other words,The global medical device market is more than four times the size of China’s, while the growth rate of China’s medical device market is nearly four times that of the global average.Currently, China has become the world's second-largest medical device market, after the United States.

In addition to capital market policies, medical devices, as a branch of healthcare, are significantly influenced by numerous policies from national pharmaceutical authorities, particularly volume-based procurement and DRG/DIP payment reforms. Compounded by factors such as the COVID-19 pandemic and the international landscape, the medical device market has experienced considerable turbulence in recent years.

In this issue of “Jiuding Investment Insights,” we will examine the medical device sector in light of healthcare policies such as centralized procurement and DRG/DIP payment reforms, as well as recent regulatory updates for capital market listings, aiming to cut through the fog surrounding the medical device market and identify certainty amidst uncertainty.

Moderate Price Reductions in Centralized Procurement Still Impact Business Models, Market Landscape, and Market Size

In January 2017, the “13th Five-Year Plan for Deepening the Reform of the Medical and Healthcare System” issued by the State Council stated that the centralized procurement system for pharmaceuticals and high-value medical consumables should be improved.

# Centralized Volume-Based ProcurementThe so-called centralized volume-based procurement refers to a mechanism in which public medical institutions act as the primary entities for consolidated purchasing, commit to specific procurement volumes for pharmaceuticals or medical devices, and leverage group purchasing power to negotiate prices with manufacturers. The objective of this initiative is clear: to reduce the prices of pharmaceuticals and medical devices, thereby alleviating the financial burden on patients and curbing expenditures from the national medical insurance fund.

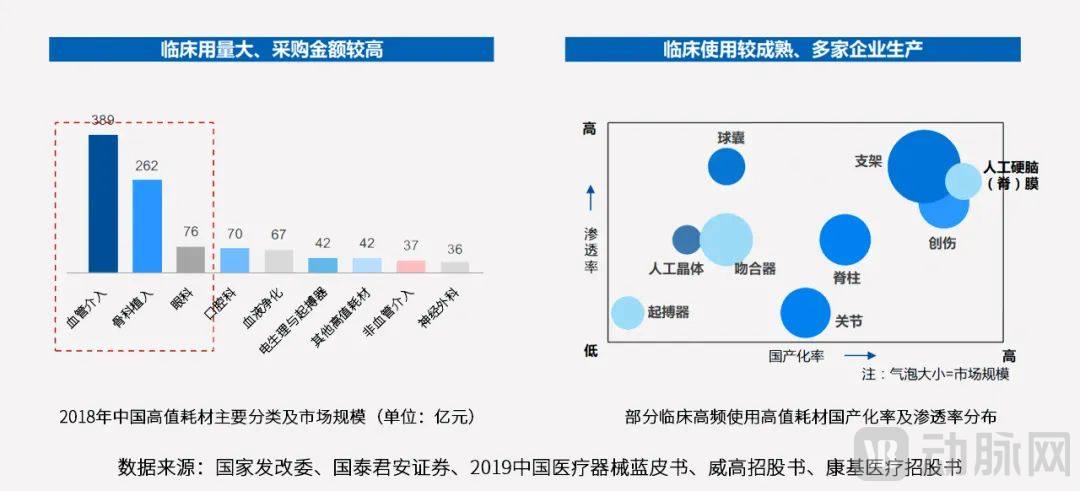

Since 2018, seven rounds of national centralized procurement have been conducted in the pharmaceutical sector, and the third round is set to be launched in the medical device sector. In addition to national-level centralized procurement, pilot programs for certain medical device categories—such as chemiluminescence in vitro diagnostic (IVD) products, drug-coated balloons, and neurointerventional devices—have already been implemented across various provinces, municipalities, and regional alliances.

In November 2020, China launched its first national centralized procurement for a medical device category: cobalt-chromium alloy drug-eluting coronary stents (i.e., cardiac stents, a type of cardiovascular interventional consumable). Twenty-six stent products from 11 companies competed in an ungrouped bidding process, with 10 products ultimately selected. The average price of stents dropped from approximately RMB 13,000 to around RMB 700. Compared with 2019, the average price reduction for identical products from the same manufacturers reached 93%.

In September 2021, the National Healthcare Security Administration (NHSA) launched another round of centralized procurement for orthopedic consumables, specifically artificial joints. The average price of hip implants dropped from RMB 35,000 to approximately RMB 7,000, while the average price of knee implants fell from RMB 32,000 to around RMB 5,000, representing an average price reduction of 82%.

In July 2022, the “Announcement on the Centralized Volume-Based Procurement of Orthopedic Spinal Consumables Organized by the State” was released, making spinal consumables the third category of high-value medical consumables to undergo national centralized procurement, following coronary stents and artificial joints.

According to the State Council Information Office, the average price reduction for the first six batches of centralized drug procurement was 53%. When combined with the price reductions achieved through centralized procurement of coronary stents and artificial joints, it appears that the magnitude of price cuts for medical devices is significantly greater than that for pharmaceuticals.However, based on our observations, the centralized procurement of medical devices is generally more moderate than that of pharmaceuticals.

From the perspective of application scenarios,For most medical devices, there is an unavoidable step between manufacturers and end patients: accompanying services.,Including providing compliant intraoperative support services, assisting with instrument assembly, offering necessary guidance on instrument use, and conducting surgical procedure training.

After the first round of national centralized procurement eliminated intermediary profit margins in the distribution of coronary stents, there were instances where accompanying services were lacking, thereby affecting the use of medical devices. Drawing on this experience,During the centralized procurement of artificial joints, ancillary services became an independent pricing unit.. From the results of centralized procurement, the average price reduction for artificial joints was 11 percentage points lower than that for coronary stents, which may be the main reason.

Moreover, unlike coronary stents, the volume-based procurement of artificial joints and spinal implants has established multiple candidate selection rules (including a “revival” mechanism). The signal conveyed is:Winning bids is no longer solely based on the lowest price, but has become more rational.

Despite the moderate price reductions, volume-based procurement will still impact the business models, market landscape, and market size of the affected products.

From a business model perspective, winning or losing bids directly impacts the company’s overall brand promotion and market sales in the future. This is because, beyond the products included in centralized volume-based procurement (VBP), other products can also expand their market coverage through the hospital access channels established by VBP. Consequently, the sales model for relevant product categories, which previously relied primarily on agency distribution, will undergo significant changes following the implementation of VBP.

From the perspective of market structure, volume-based procurement will bring about localized adjustments to the market landscape of relevant products, rather than a disruptive reshuffling.

In the centralized procurement of artificial joints that has already been implemented, enterprises are grouped into separate units for competitive bidding within the same product system category, based on medical institutions’ procurement requirements (i.e., sample hospitals declare their volumes based on historical annual procurement data prior to centralized procurement, referred to as “volume declaration”), enterprises’ supply capabilities, and product materials (such as type and material).

In the upcoming centralized procurement of spinal consumables, factors such as medical institutions’ demand, enterprises’ willingness and capacity to supply, and the completeness of product portfolios are comprehensively considered, with enterprises grouped into separate units for competitive bidding.

This approach largely respects the existing market landscape, avoids extreme scenarios driven by price, and ensures the industry’s supply capacity (e.g., preventing situations where small enterprises win bids with low prices but fail to guarantee supply).

The localized changes lie in the fact that volume-based procurement (VBP) entails a certain elimination rate, and companies with historically higher market shares and a stronger willingness to reduce prices will be prioritized in gaining relevant market share. According to the VBP rules for spinal consumables, leading companies with comprehensive product components are also expected to gain greater advantages.

Regarding the impact of centralized procurement on market size, we believe that the situation varies across different product categories.

For product categories with high market penetration, it is difficult to offset price reductions through volume growth, making a contraction in market size inevitable. However, for less mature product categories, centralized procurement can rapidly drive volume expansion, compensating for losses from price cuts and leading to overall market growth.

Innovation and Global Expansion Will Be the Themes of Future Development, with Real Demand and Willingness to Pay as Key Factors

As centralized procurement becomes normalized, which subsectors will be included in the national centralized procurement scope next?

The "Reform Plan for the Governance of High-Value Medical Consumables" issued by the General Office of the State Council in July 2019 pointed out that centralized procurement should be explored by category for high-value medical consumables that are widely used in clinical practice, involve high procurement amounts, have mature clinical application, and are produced by multiple manufacturers.

In light of this plan and the volume-based procurement programs already implemented, the industry generally believes that,The higher the proportion of a category in medical insurance expenditures and the higher its domestic production rate, the greater the likelihood of it being included in centralized procurement.。

In addition to centralized procurement, another key policy facing Chinese pharmaceutical companies is DRG/DIP payment.

By the end of 2021, the National Healthcare Security Administration launched the Three-Year Action Plan for DRG/DIP Payment Method Reform. By the end of 2024, all pooling regions across China will have fully implemented DRG/DIP payment reforms. By the end of 2025, DRG/DIP payment methods will cover all eligible medical institutions providing inpatient services.

DRG and DIP payment refer to Diagnosis-Related Groups (DRG)-based payment and Disease-Specific Points-Based Payment, respectively. In the past, China’s basic medical insurance payment methods primarily included fee-for-service, per-unit-of-service payment, capitation, and single-disease payment.

Similar to centralized procurement, the implementation of DRG/DIP payment aims to improve the efficiency of medical insurance fund utilization and curb unreasonable growth in healthcare costs.

For Chinese medical device companies, as niche sectors such as coronary stents and artificial joints gradually shift into red ocean markets, and with the normalization of centralized procurement and the implementation of DRG/DIP payment models, their profit margins in the domestic market will gradually shrink. In this context, how should they respond?

On the one hand, medical device companies can achieve high premiums and profit margins for certain products by driving product innovation in categories not subject to centralized procurement.。

For example, in the 2020 national centralized volume-based procurement of coronary stents, Lepu Medical’s cobalt-chromium alloy sirolimus-eluting stent system was selected. Lepu Medical stated that with the implementation of the national organized centralized volume-based procurement of coronary stents, revenue from its traditional metal drug-eluting stent business declined significantly; however, the company’s portfolio of innovative interventional products (including bioresorbable stents, drug-coated balloons, and cutting balloons) achieved a year-on-year revenue growth of 827.36% in 2021.

Sinomed’s BuMA coronary drug-eluting stent, made of stainless steel, was not included in the national volume-based procurement program. The company has also stated publicly that stent consumables require a variety of specifications to meet the clinical needs of patients with lesions at different anatomical sites. As the volume of clinical procedures increases, there remains significant market potential for products outside the volume-based procurement framework.

It should be noted that medical devices constitute a multidisciplinary field, encompassing optics, physics, biochemistry, precision mechanics, and computer hardware and software. Innovation in this sector relies on advancements in these disciplines; therefore, achieving breakthrough innovations from scratch (0 to 1) is highly challenging, with most efforts focused on incremental innovations or minor improvements based on existing products. This reality requires greater patience from practitioners, investors, and regulators, who must respect the inherent laws of these disciplines and maintain a rational perspective on development cycles.

Generally speaking, incremental innovation in medical devices proceeds from the following aspects:

● Innovations in precision or sensitivity, such as enhancing the sensitivity of diagnostic reagents.

● Innovation in simplicity to streamline processes and reduce time.

● Innovation in business models, such as developing innovative products for home or commercial use based on hospital-oriented products.

We believe that companies should not innovate for the sake of innovation. When making investment value judgments, we do not focus on the merits of individual technologies. Only technological advancements that meet real-world needs demonstrate willingness to pay and thus hold true value.

On the other hand,Similar to many other industries, expanding overseas presents a significant opportunity for the medical device sector.。

It has been more than 20 years since China joined the World Trade Organization (WTO), and its pace of opening up will not slow down. As overseas giants continue to enter the Chinese market, domestic enterprises also need to expand globally. Moreover, as previously mentioned, the global medical device market is more than four times the size of China’s, offering new growth opportunities for Chinese companies.

It is understood that many Chinese enterprises are currently planning to establish international platforms. Building on the global markets initially opened through the export of epidemic prevention supplies, these companies aim to further expand their overseas market channels by setting up overseas branches or pooling domestic corporate resources to venture abroad collectively.

Furthermore, many enterprises have prioritized countries and regions along the “Belt and Road” for overseas market expansion, while some companies in niche sectors with high technical barriers have chosen to collaborate with firms in developed countries and regions, such as those in Europe and the United States, on R&D and sales channel development.

New Listing Rules Benefit “Hard Tech” Companies; Investment Value Requires Comprehensive Assessment Based on Multiple Factors

Having analyzed the industry fundamentals, we now turn our attention back to the rules of the capital market.

In early 2019, the Shanghai Stock Exchange issued the Notice on Soliciting Public Comments on Supporting Business Rules for the Establishment of the STAR Market and the Pilot Registration-Based IPO System, clarifying that an issuer applying for an initial public offering and listing must meet at least one of the five listing criteria.

Among these, the fifth listing standard of the STAR Market refers to “an estimated market capitalization of no less than RMB 4 billion; core business or products must be approved by relevant national authorities; there must be substantial market potential; and phased achievements must have been attained. Pharmaceutical companies must have at least one core product approved to enter Phase II clinical trials, while other enterprises aligned with the positioning of the STAR Market must demonstrate clear technological advantages and meet corresponding conditions.”

In the three years since the launch of the STAR Market in July 2019, companies listing under Criterion 5 have been predominantly innovative biopharmaceutical firms, with no successful cases among medical device enterprises. This is largely due to the lack of clear operational guidelines for medical device companies applying under Criterion 5, which has posed significant challenges for both corporate filings and substantive regulatory review.

Given this uncertainty, many unprofitable medical device companies have chosen to list in Hong Kong or pivoted to listing under the second set of criteria of the STAR Market.

Until March 2022, MicroPort EP, a medical device company under MicroPort Scientific Corporation specializing in electrophysiology interventional diagnosis, treatment, and ablation therapy, successfully “broke new ground” by becoming the first medical device company to have its IPO application approved under the fifth set of listing criteria on the STAR Market.

With practical cases and reference templates in place, the Shanghai Stock Exchange has accordingly introduced the aforementioned Guidelines.

We believe that the Guidelines are, on the whole, favorable to the medical device and investment industries. Medical device companies that are not yet profitable but possess strong scientific and technological innovation attributes now have a legal basis for listing on the STAR Market, thereby enhancing the certainty of their IPOs.

We also anticipate that the new policy will attract a cohort of unprofitable medical device companies to list on the STAR Market, though not in a clustered manner.

Based on the relevant provisions of the Guidelines, detailed requirements have been established for medical device companies applying to list under the fifth set of listing criteria of the STAR Market:

For example, core technology products should fall within the scope encouraged and supported by the national strategy for technological innovation in medical devices and related industrial policies; the research and development of core technology products should have achieved phased results; the main business or products should have significant market potential; and there should be clear technological advantages.

These provisions, combined with the market capitalization requirements under Listing Standard 5, have excluded many medical device companies.

Medical device companies that meet the fifth set of listing requirements for the STAR Market have mostly already listed on the Hong Kong Stock Exchange (HKEX) or are in the queue for listing. We have observed that since the HKEX opened its doors to pre-profit biotechnology companies in 2018, more than 50 such companies have gone public on the exchange, among which only slightly over ten are medical device enterprises.

The STAR Market also sets an implicit threshold for enterprises.:If a company reports negative net profit excluding non-recurring items for two consecutive years and its operating revenue is below RMB 100 million, it will face the risk of delisting. When reviewing IPO applications, the STAR Market uses this “profitability timeline” to back-calculate the company’s current business capabilities. If it is determined that the company will be at risk of delisting in two years, its IPO application will not be approved.

On July 29, 2022, the “No. 25 Disclosure Compilation Rules for Information Disclosure by Companies Offering Securities to the Public—Guidelines on the Content and Format of Prospectuses for Companies Engaged in Pharmaceutical and Medical Device Businesses” was promulgated and came into effect. The document explicitly stipulates that companies planning to publicly offer securities, if they anticipate the persistence of unprofitable status or a continued expansion of accumulated uncovered losses, shall analyze the likelihood of triggering delisting conditions and fully disclose the associated risks.

Overall, we believe that the Guidelines are beneficial to the development of “hard tech” enterprises but will not significantly impact investment institutions’ decision-making. Whether a company is worthy of investment ultimately depends on an assessment of its fundamentals and intrinsic value, based on its technological sophistication, market position, industry potential, development stage, and associated risks.。

As the economy develops and medical demands upgrade, coupled with the implementation of Hong Kong Stock Exchange Chapter 18A and the registration-based IPO system in China’s A-share market, the Chinese medical device industry, much like the innovative drug sector, has entered a new development cycle—characterized by abundant capital, the continuous emergence of new technologies and companies, and a vibrant, flourishing landscape.

From the perspective of individual niche segments, we focus on the increase in market concentration.。For example, following the implementation of China’s national volume-based procurement (VBP) for spinal orthopedic products, we anticipate that industry consolidation will further intensify, with leading domestic manufacturers poised to capture greater market share. Consequently, within the orthopedics sector, we place greater emphasis on companies with core competitive advantages, characterized by comprehensive product pipelines, strong R&D capabilities, and established brand recognition.

From an innovation perspective, we believe that certain new types of high-value-added low-cost consumables also present promising investment opportunities.。For example, according to our research, absorbable knotless medical sutures have a low absolute unit price but high consumption volume, and they are covered by medical insurance reimbursement, making them highly popular in clinical practice.

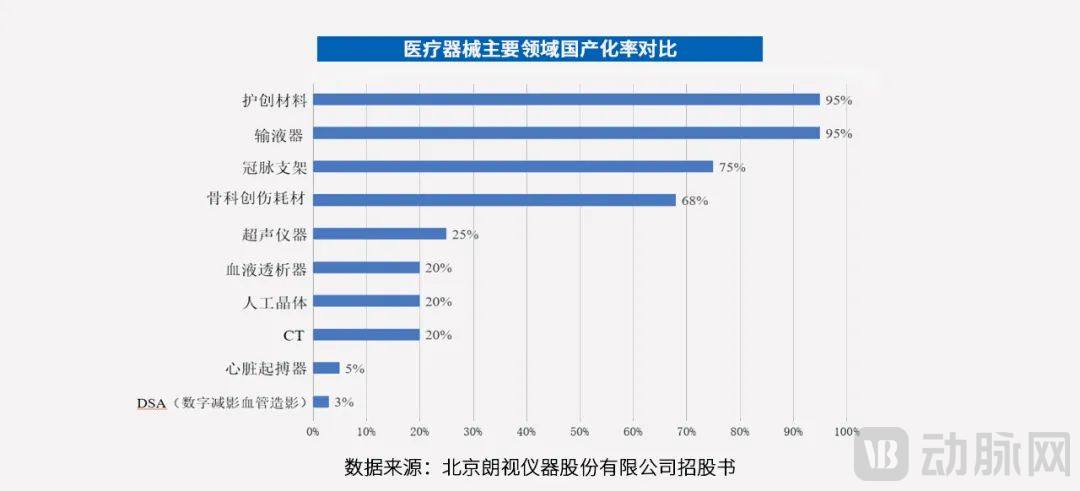

From the perspective of long-term growth potential, the domestic production rate may serve as a criterion for assessment.We believe that a 20% domestic production rate represents an inflection point. Beyond this threshold, the localization of medical devices accelerates, leading to the emergence of publicly listed companies. Consequently, in the primary market, niche segments with domestic production rates between 20% and 50%—such as neurointerventional, cardiac intervention, oncology intervention, orthopedic sports medicine, and surgical staplers—present significant investment opportunities.

As an important branch of medical devices, IVD is also a niche sector we have long focused on.We have already elaborated on this in our article, “In Vitro Diagnostics Enters a Golden Age of Development: Who Is Breaking Through, and How Will the Landscape Evolve?”