Lunit: The AI-Powered Medical Imaging and Biomarker Company That Tripled Revenue 30x in 3 Years and Surged 30% on IPO Day

Lunit

Artificial Intelligence Software Developer

On July 21, 2022, medical artificial intelligence company Lunit (Lunit Inc.) listed on the Korea Exchange. On its first day of trading, Lunit opened at KRW 30,800 (USD 23.53) and closed at KRW 40,000 (USD 30.56), hitting the maximum single-day price increase limit of 30%. As of yesterday’s close, Lunit’s stock price continued to rise, closing at KRW 43,500 (USD 33.22).

On July 21, 2022, Lunit successfully listed on the Korea Exchange (Image source: Lunit)

Notably, Legend Capital, a domestic investment firm, led Lunit’s Series B financing round in June 2018 and made three additional investments in 2019 and 2021, continuously supporting the company’s growth.

Like most medical AI companies, Lunit initially broke into the market with deep learning-based medical imaging analysis. It later carved out a unique path by venturing into biomarker research, securing a $26 million investment in 2021 from Guardant Health, the world’s largest liquid biopsy company, and establishing its ambitious vision to “Conquer Cancer Through AI.”

Lunit’s strategic layout integrating “radiology + pathology” is uncommon both in China and internationally, yet it has garnered high recognition from top IVD companies and capital markets in China, South Korea, and the United States, achieving an average annual revenue growth of 5–7 times over the past three years.

How far can this innovative model go on the international stage? And what implications does its philosophy hold for the entire medical AI sector? VCBeat engaged in an in-depth conversation with Brandon Suh, Founder and CEO of Lunit. After nine years of entrepreneurship, how has Lunit become a world-class medical artificial intelligence company?

Centered on conquering cancer, Lunit focuses on two key areas: “diagnosis” and “treatment,” corresponding to its two products, Lunit Insight and Lunit Scope, respectively.

Lunit Insight, Lunit’s longest-developed and most mature AI imaging product, currently supports chest X-ray, chest CT, mammography, and digital breast tomosynthesis. In the medical imaging sector, Lunit’s strategic approach mirrors the early logic of Chinese AI company Yizhun Smart, aiming to promote early screening, early diagnosis, and precise diagnosis for lung cancer and breast cancer, two major global cancer types.

The value of AI lies in enhancing diagnostic accuracy and efficiency. Data from Lunit shows that this AI can help South Korea’s healthcare system improve tumor diagnosis accuracy by 20%, enable early detection of lesions in 50% of lung cancer patients and 40% of breast cancer patients, reduce unnecessary follow-up examinations by 30%, and increase diagnostic speed tenfold.

In terms of implementation, Lunit primarily adopts two models for advancement. The first involves collaborating with equipment manufacturers to embed AI directly into imaging devices such as DR and mammography systems, enabling radiologists to receive diagnostic results at the time of image acquisition. The second involves partnering with PACS vendors to integrate AI-based image analysis during the image interpretation phase.

The starting point for defining business models is the hospital. In the first business model, Lunit bundles AI with imaging equipment and sells it to hospitals with long-term AI needs. For hospitals, equipment that includes AI is a capital expenditure; although the upfront cost of buying out the AI is high, the cost amortized over a long period is low.

The second business model is an ideal one anticipated by the industry, involving revenue sharing with PACS vendors on a “per-case” payment basis. This approach is classified as an operating expense in hospital financial accounting, facilitating the calculation of current-period costs for hospitals while enabling AI companies to secure more sustainable cash flows.

From the current landscape, hospitals in various countries show a stronger preference for perpetual licensing over per-case payment models. Lunit is pursuing a dual-pronged strategy: it has established equipment partnerships with imaging giants such as GE HealthCare, Philips Healthcare, Fujifilm, and Hologic, while also collaborating with companies like GE HealthCare, Fujifilm, and Agfa on per-case payment arrangements.

To date, Lunit Insight’s AI for chest radiography has been commercialized in 42 countries, and its AI for mammography has been commercialized in 38 countries. These figures are expected to continue growing as Lunit expands its partner network.

Revisiting Lunit SCOPE: A Pathology AI Product and Lunit’s Horizontal Expansion of Its AI Capabilities. To fully elucidate its value, we must first discuss immunotherapy and companion diagnostics.

Companion diagnostics are in vitro diagnostic technologies associated with specific drugs. By measuring the expression levels of proteins and variant genes in the human body, they can identify patient populations most likely to respond to particular drugs and therapeutic regimens, thereby reducing the risk of severe side effects from treatment, selecting safer and more effective therapeutic options, and enhancing the safety and efficacy of treatment. Consequently, the co-development of drugs and companion diagnostics is garnering increasing attention from the global pharmaceutical industry.

Data provided by the investment firm ARK Investment Management LLC further corroborates this trend: the use of companion diagnostics to measure biomarkers in Phase I clinical trials can increase the trial success rate from 8.4% to 25.9%, representing a threefold improvement. Furthermore, companion diagnostics can reduce clinical trial costs from approximately $1.2 billion to $300 million, cutting trial expenditures by three-quarters.

However, a molecular diagnostics expert told VCBeat: Although the demand for companion diagnostics is growing, the technology of using large panels for companion diagnostics is not yet mature. With the development of immunotherapy, this new therapy will gradually expand its market space in the field of tumor treatment and push tissue-based biomarkers (such as PD-L1, MSI, etc.) to the mainstream—this is precisely where Lunit's opportunity lies.

In simple terms, Lunit SCOPE is an AI-powered pathology product that represents a horizontal expansion of Lunit’s AI capabilities. Specifically, this AI performs tumor tissue identification and quantitative analysis based on histopathological images, including analysis of intratumoral tumor-infiltrating lymphocyte (TIL) density, stromal TIL density, tumor-stroma ratio (TSR), and tissue classification according to immunophenotype.

Due to the complexity of biological systems and the heterogeneity of patient diseases, the same disease may present with different pathological states in different patients, and the same drug may yield varying effects across individuals. Lunit’s AI analyzes multi-dimensional data—such as electronic health records, holographic images, and imaging data—to identify novel biomarkers from imaging, genomics, and clinical data for assessing disease progression. This capability facilitates the design of stratified clinical trials and the recruitment of the most suitable participants, thereby effectively reducing risks in clinical development. Additionally, it can guide precision medication following immunotherapy.

Lunit’s business characteristics have successfully attracted the attention of Guardant Health, the world’s largest liquid biopsy companion diagnostics company. Following Guardant Health’s investment, Lunit has successfully integrated into this industry giant’s ecosystem. In terms of its business model, Lunit can collaborate with Guardant Health to provide services for relevant research conducted by top 100 pharmaceutical companies, and it can also directly reach end consumers through Guardant Health’s hospital sales network.

Despite Lunit’s disruptive innovations in its business and commercial models, it still needs to address the industry-wide challenge of “how medical artificial intelligence can achieve profitability.”

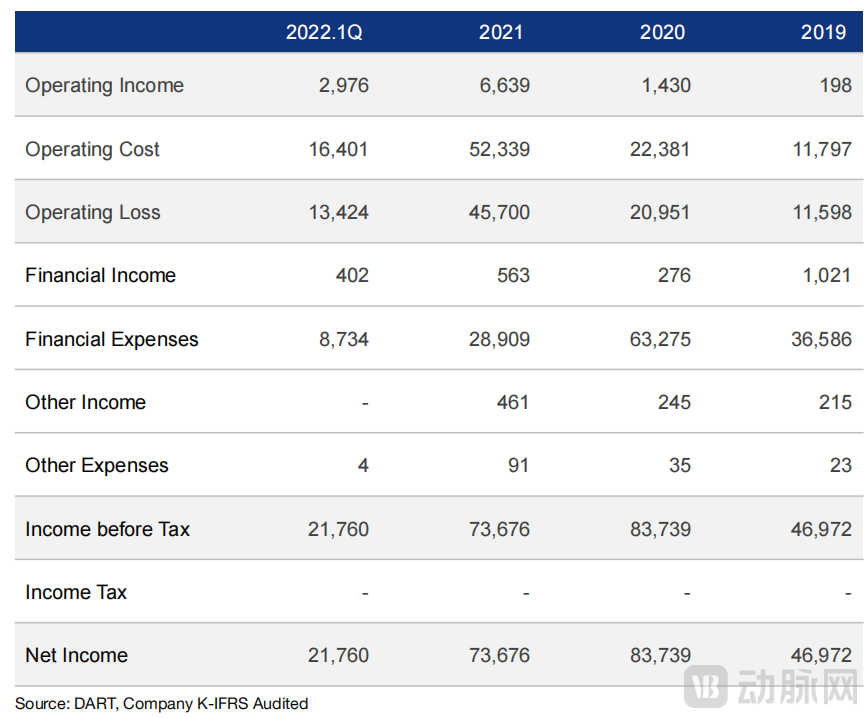

Lunit Financial Statements (Unit: Million KRW; Data Source: Lunit)

Revenue data indicates that Lunit’s business model began to gain traction after 2019. The company’s operating revenue was merely KRW 198 million (approximately USD 150,000) in 2019, but by the end of 2020, this figure had risen to KRW 1.43 billion (approximately USD 1.1 million), representing a 6.2-fold increase.

In 2021, Lunit continued its rapid expansion, generating KRW 6.639 billion (approximately USD 5.51 million) in revenue for the year, a 4.6-fold increase from 2020. Notably, in the first quarter of 2022 alone, Lunit recorded revenues of KRW 2.976 billion (USD 2.29 million). At this pace, Lunit’s annual revenue for 2022 is projected to double once again, surpassing the USD 10 million mark.

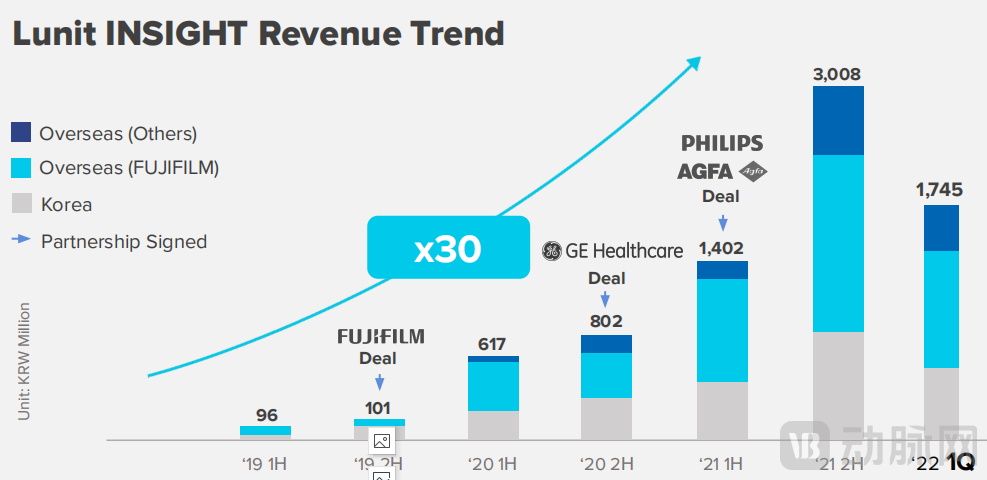

The vast majority of revenue growth was driven by Lunit Insight, a business segment that has grown nearly 30-fold over the past three years. As shown in Lunit’s revenue trend chart, the entry of Fujifilm, GE Healthcare, Philips Healthcare, and AGFA corresponded to three major inflection points in Lunit’s revenue surge. In particular, overseas revenue multiplied with the support of these partners.

Lunit Insight Revenue Growth Trend (Source: Lunit)

The revenue growth over the past two years cannot be attributed without acknowledging the contribution of Lunit SCOPE. In 2019 and 2020, Lunit INSIGHT accounted for 99.5% and 99.2% of total revenue, respectively. However, following the investment by Guardant Health, the Lunit SCOPE segment has rapidly risen. The revenue share of Lunit INSIGHT dropped to 66.4% in 2021 and further declined to 58.6% in Q1 2022. Thus, Lunit SCOPE has become the second growth curve for Lunit and is expected to surpass Lunit INSIGHT in revenue contribution by the end of this year.

Leapfrog growth naturally comes with its costs.

A company’s leadership team defines its corporate culture. Since its inception, Lunit has maintained a high level of investment in research and development, with more than 100 papers published in top-tier journals in the field of radiology alone. Following the integration of its AI pathology solutions, Lunit’s annual operating costs in recent years have remained at the level of tens of billions of Korean won, with an upward trend.

Lunit’s leading academic research achievements have both formed its competitive moat and become its sweet burden.

In the short term, Lunit will rely on AI-based image interpretation and experimental applications of Lunit Scope as its revenue sources, making it temporarily difficult to fully convert R&D investments into profitability. However, in the long run, high-quality AI enables the large-scale deployment of Lunit Insight; collaborations between Lunit Scope and major pharmaceutical companies will open new opportunities for Lunit, while precision medication services targeted at consumers will also become a key driver of revenue generation.

Brandon Suh provided data to substantiate Lunit’s growth potential. In 2021, Lunit completed 200 transactions through the sale of imaging AI integrated with medical devices. However, global annual sales of XR equipment reach 70,000 units, with Lunit’s partners accounting for 50% of this market. Therefore, considering only the single channel of selling imaging AI bundled with devices, Lunit has nearly a hundredfold room for growth.

Lunit Scope also holds significant potential. As a precision medication service for patients following immunotherapy, if it subsequently obtains FDA review and approval, it could be sold at a price of $1,500 per person. Assuming there are 4.8 million patients worldwide receiving immunotherapy annually, this would represent a $7.5 billion market.

This figure does not account for collaborations involving AI in clinical trials and major pharmaceutical companies. Lunit has roughly estimated that it faces a massive market exceeding $22 billion.

Unlike domestic AI companies, Lunit has forgone certain key elements in its sales strategy. For instance, rather than prioritizing control over distribution channels as many Chinese AI firms do, Lunit leans more toward promoting its AI products through partnerships.

This mindset is shaped by Lunit’s market position. With thousands of hospitals in China and a constant influx of competing enterprises, AI companies must establish close collaborative relationships with hospitals and build strong brand recognition to stand out in the intensely competitive landscape and win hospital partnerships.

In contrast, Lunit faces a limited domestic market in South Korea and must expand globally to sell its products worldwide, thereby gradually recouping its substantial upfront investments. Furthermore, varying regulatory requirements across different countries prevent Lunit from adopting the strategy employed by Chinese AI companies, which typically secure adoption through hospital-by-hospital penetration within their home market. Under these circumstances, relinquishing some degree of bargaining power while dedicating itself wholeheartedly to technological R&D may well be the key factor enabling this South Korean company to stand out among numerous competitors.

Although facing different markets, Lunit’s development journey is equally worthy of study by domestic medical AI companies. After all, Lunit’s revenue leap period was largely consistent with that of Airdoc, Infervision, Shukun Technology, and Pulse Medical Imaging Technology, yet it secured a first-mover advantage in the international market.

Chinese AI companies have already established varying degrees of overseas presence, yet none are willing to place complete trust in partners to drive implementation, as Lunit has done. With competition among domestic AI firms at the product level becoming increasingly indistinguishable, the time has come to make critical choices about what to relinquish and what to retain in order to break into the vast global market.