Can Early-Stage Medical Startups Weather the Capital Winter as the Market Cools?

In July, although the weather across China was extremely hot, this heat did not seem to extend to the early-stage healthcare market, which is currently favored by capital.

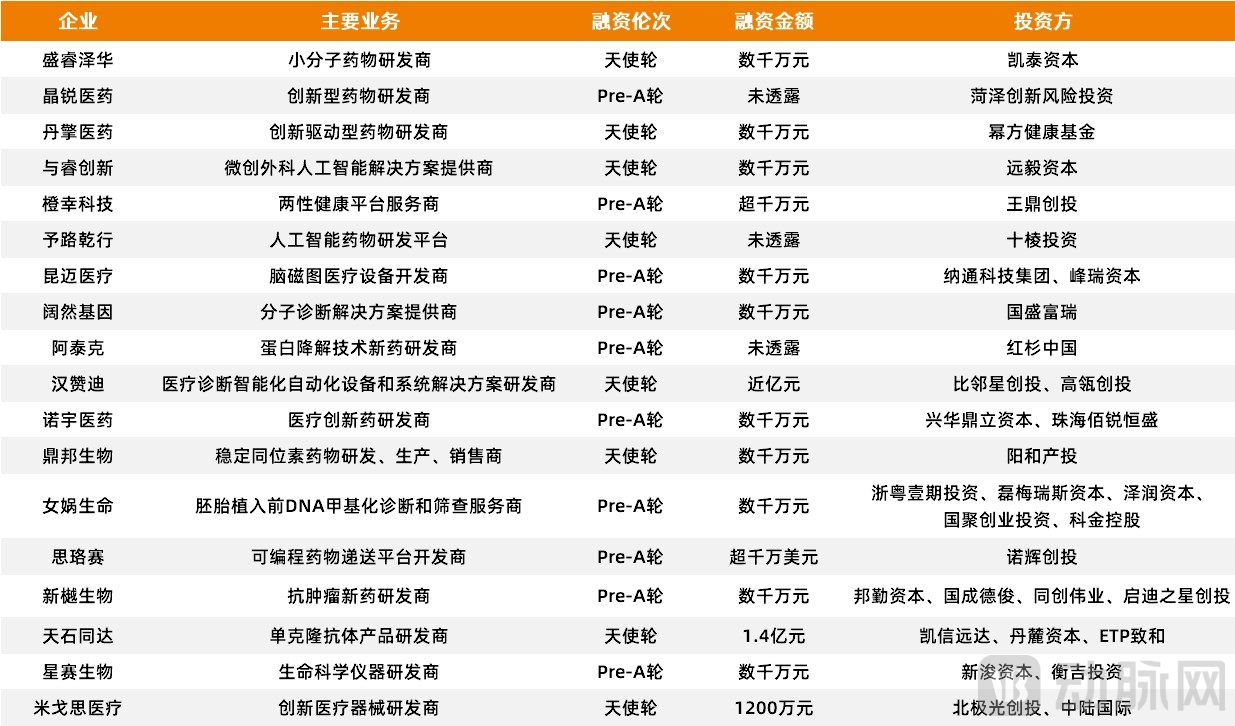

Overview of Early-Stage Healthcare Financing in July 2022

According to incomplete statistics from VCBeat’s Orange Fruit Bureau, a total of [events/transactions] occurred in China’s healthcare and medical sector in July18 casesEarly-stage investment and financing events, with a total funding amount of approximately1.3 billion yuan, representing a decline in both metrics compared to the first half of the year, which saw an average of 20 investment and financing deals per month and an average monthly total financing amount of RMB 1.5 billion.

However, investment firms are generally optimistic about the early-stage healthcare market in the second half of this year. In their mid-year reports, they have clearly stated their intention to increase investments in early-stage healthcare projects during the latter half of the year.

So, why does this gap between reality and expectations exist? Is it due to the lag effect in investment? Or have investment institutions adopted a more rational stance toward the early-stage healthcare market? On another front, how can startups “stand out” amidst the current capital winter? To address these questions, VCBeat’s Orange Fruit Bureau will examine the early-stage financing data from July to gain insights.

Two Key Features: Composite Background, Joint R&D

Data never lies. A further analysis of the 18 startups that completed early-stage financing in July reveals two notable characteristics:First, most founders possess multidisciplinary backgrounds; second, cross-platform and cross-domain collaborative R&D has become a consensus among startups.

First, let’s discuss the founder profile.. Through observations of 18 startups, we found that their founding teams are mostly not limited to R&D in a single field, but ratherPossessing a Multidisciplinary Background。

For example, having completed a tens-of-millions-yuan angel round of financingMigosi Medical, Professor Li Jiwei, the founder, not only has a background in materials science from the Chinese Academy of Sciences but also possesses over ten years of experience in marketing, sales, and investment mergers and acquisitions at foreign enterprises and domestic listed companies.

In addition, there is the company that completed an angel round of financing amounting to nearly 100 million yuan this month.Hanzandi, its founding team is not only dedicated to scientific research, with over a decade of experience in life science product development and a background in biology, but also proficient in market-oriented operations, possessing deep expertise in life science marketing management and innovative business models.

In fact, the diversification of founder identities is becoming a “prerequisite” for startups. This is because research and development (R&D) differs fundamentally from entrepreneurship, with the most critical distinction lying inR&D is idealistic, while entrepreneurship is grounded in reality. R&D investment can be made regardless of cost, but this is not feasible for startups, as entrepreneurship operates within a fully market-driven framework.。

Therefore, if founders possess only R&D capabilities but lack accurate market insights, even the most advanced technologies will face numerous limitations during commercialization.

Therefore, we have observed that many startup teams are consciously recruiting partners with market operation experience; meanwhile, these startups are also employing various strategies to compensate for their weaknesses in commercialization capabilities.

Having outlined the founder profile, we now turn our focus to the R&D model.. Through an analysis of 18 startups, we found that“Joint R&D” Is Becoming a Common Trait Among Startups in the Healthcare Sector。

Having completed a Pre-A financing round of tens of millionsNuoyu Pharmaas an example. It is reported that during the R&D phase, Nuoyu Pharma not only co-established a Nuclear Medicine Clinical Translation Center with Jiangnan University and its affiliated hospital, but also collaborated with multiple leading medical R&D institutions and universities both domestically and internationally, jointly focusing on cutting-edge radiopharmaceutical development and innovative drug screening. Currently, two of Nuoyu Pharma’s research achievements have entered the global first-in-class cohort of innovative drugs.

In addition, there are those selected by Sequoia.ArtekTo fully leverage the potential of ATTEC’s core technology, Artek has actively established extensive R&D partnerships with leading global pharmaceutical and biotech companies. In 2020, it formed a strategic partnership with an internationally leading pharmaceutical company to jointly develop novel molecular glue therapies.

In a sense, the “joint R&D” model not only reduces the R&D risks for startups but also breaks through the limitations of individual R&D efforts. Cross-platform and cross-disciplinary collaborative partnerships not only maximize each party’s strengths but also compensate for their respective weaknesses.

Founder of AitekDing YuProfessorstated, “By collaborating with internationally leading pharma and biotech companies, we will advance drug development targeting high-value targets, leverage complementary strengths, and fully unlock Artek’s potential in ATTEC and protein degradation drug R&D.”

"The 'Changes' and 'Constants' in the Investment Sector"

Beyond the founder’s profile and R&D model, the specific subsector to which an early-stage medical startup belongs is also a focal point, as it, to some extent, foreshadows the future trajectory of the healthcare market.

According to statistics from VBInsight, among the 18 companies that completed early-stage financing in July, biopharmaceutical companies accounted for the lion’s share, with 10 firms representing 56% of the total. Medical device companies followed closely, with 5 firms accounting for 28%. The remaining three companies all belong to the digital health sector, which has garnered significant attention in recent years.

In fact, this segmentation has become a consensus in the early-stage healthcare market, which can be broadly categorized into three key areas: first, prioritizing hard-tech startups; second, showing a stronger preference for biopharmaceutical companies; and third, increasingly focusing on digital health startups with emerging vitality and significant market potential.This is regarded as the “constant” in investment direction.。

So, what has changed?What has changed is the application scenario of the startup's core product.。

According to statistics from VCBeat’s Orange Fruit Bureau, among the 18 startups that completed early-stage financing in July, seven focused on oncology therapeutics, accounting for 39% of the total and making it the subsector most closely watched by investors.

Completion CountTens of millions of yuan in angel round financingDanqing PharmaceuticalsAs an example, this is an innovation-driven pharmaceutical R&D company based in China with a global outlook, dedicated to developing first-in-class (FIC) targeted therapies for tumors in the era of precision oncology 2.0. Currently, Danqing Pharma has five first-in-class new drug candidates in development and has filed multiple PCT international patent applications.

In addition to tumors,Ophthalmology, Assisted Reproductive TechnologyNiche sectors with strong current market demand have also become the focus of the early-stage healthcare financing market in July, accounting for 4 out of 18 startups, or 22%.

Let's start with ophthalmology.. having completed a RMB 12 million angel financing roundMigosi MedicalTake, for example, this innovative medical device company, which specializes in minimally invasive ophthalmic procedures and is built upon a foundation of living cationic polymerization biomaterial technology.

Currently, Migos Medical’s first product in its pipeline is a minimally invasive surgical device for glaucoma. Upon completion of process and sterilization validation at its GMP-certified facility, the product will enter the registration testing phase. In addition to the glaucoma segment, Migos Medical will also focus on implantable collamer lens (ICL) products in the optometry field. Notably, within less than a year, Migos Medical has successfully completed two rounds of early-stage financing, fully demonstrating investor confidence in the minimally invasive ophthalmic device sector.

On Assisted Reproductive TechnologySince the introduction of the “three-child policy,” market enthusiasm in the assisted reproduction sector has remained exceptionally high over the past year, with many startups in the field successfully securing financing by capitalizing on this policy-driven momentum.

Nüwa LifeNüwa Life, a typical representative in the field, has completed three rounds of early-stage financing within just one year after the introduction of the “Three-Child Policy” on July 20, 2021, demonstrating remarkably rapid growth momentum with its next-generation assisted reproductive technologies.

The early investment fervor in these two niche sectors also reveals a new trend: investment firms are increasingly focusing on high-value subsectors that boast substantial market demand yet remain relatively “young.”

The “Flourishing Diversity” of Investment Institutions

For investment institutions, there was no "leader" in the early-stage healthcare market in July.

According to statistics from VBInsight, among the 18 early-stage financing deals in the healthcare sector completed in July,A total of 32 investment institutions participated., having completed only one round of early-stage financing.

Among these investment institutions, there are not onlySequoia, Hillhouseincluding leading institutions, as well as those that have long focused on early-stage projectsAurora Venture Capital, Proxima Ventures, and TusStaretc. In addition, there are local government support funds—affiliated with the Xuzhou Municipal State-owned Assets Supervision and Administration Commission (SASAC)Guosheng Furui。

The diversification of investment institutions also indirectly confirms the high level of interest in the early-stage healthcare market. Currently,“Investment institutions chase after scientists,” “Investment institutions camp out at university gates,” “Investment institutions scramble to sign up scientists”Phrases like these continue to emerge in the market; while slightly exaggerated, they are largely accurate.

An investor with years of experience in early-stage project investment told Chengguo Bureau, “Before the pandemic, there were very few investment institutions focusing on early-stage healthcare projects. Most investors largely overlooked early-stage ventures, perceiving them as offering limited returns, requiring substantial effort, and carrying high risks. However, just in the past year or two,”I suddenly felt that the number of competitors had increased.“, those who previously avoided early-stage investments have now started to invest in early-stage ventures; research institutes and local governments are also establishing their own early-stage funds, making this market suddenly vibrant.”

So, why is capital choosing to double down on early-stage healthcare projects at this moment? There must be reasons. Through conversations with multiple investors, we have summarized the following three key factors:

First, the low-hanging fruit in the healthcare sector has largely been harvested; future opportunities will inevitably lie with innovative enterprises that possess proprietary original technologies and can meet clinical needs.

Second, the frenetic acceleration of the secondary market is exerting mounting pressure on the primary market, blurring investment boundaries. Investment institutions that previously focused solely on mid-to-late stages are finding it increasingly difficult to identify suitable entry points at those stages, forcing them to shift their focus to early-stage projects.

Third, early-stage healthcare projects are entering a period of significant opportunity. Currently, governments, research institutions, publicly listed companies, and investment banks are closely focusing on startup ventures in the medical sector, making it easier than ever for these startups to grow and unlock substantial market value.

Of course, these selected startups must themselves possess certain “hard” strengths, which places a premium on investment institutions’ core capabilities in screening and nurturing early-stage ventures.