Biotech Success Doubles with Big Pharma Backing: Exit Rates and Valuations Surge

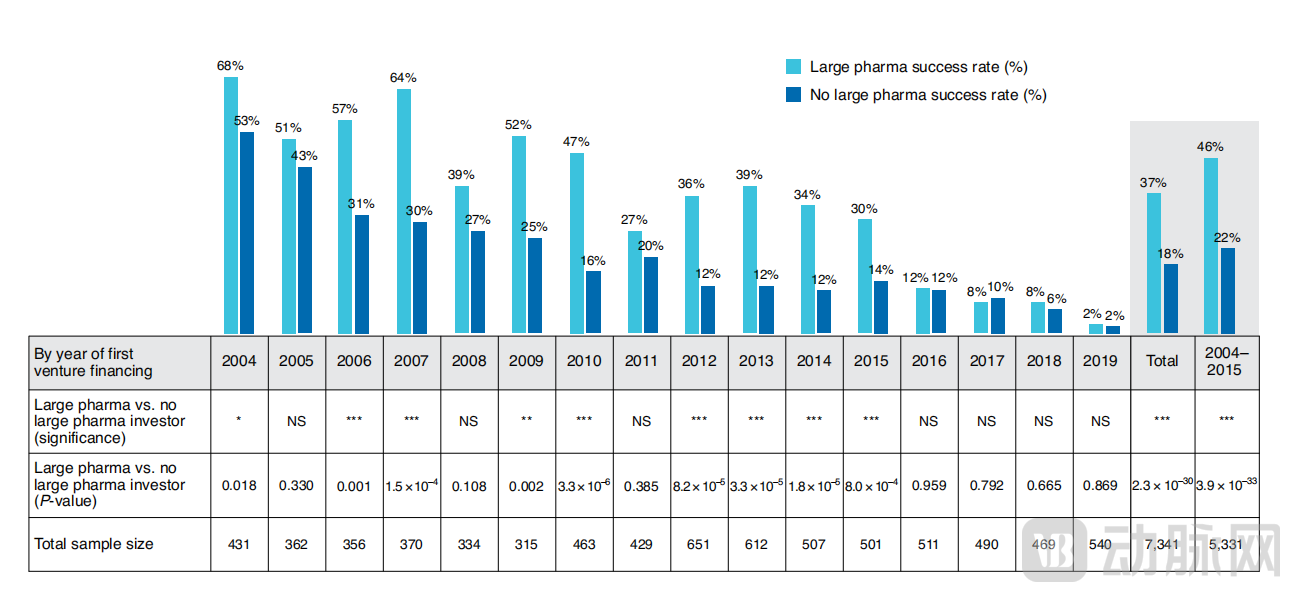

Recently, an industry report published in Nature presented a set of intriguing research data: biotech companies with investment from large pharmaceutical firms had a successful exit rate of 46%, whereas those without pharmaceutical company involvement had a successful exit rate of only 22%. In other words,The success rate of exits for biotech companies invested in by pharmaceutical firms has doubled.

Not only has the exit success rate doubled, but the market capitalization and acquisition value of biotech firms invested in by large pharmaceutical companies have seen even more striking increases—with acquisition valuations nearly doubling.

Investors focus on exit success rates and valuations; this set of data is based onA Study Based on 5,331 Sample Companies from 2004 to 2015These data can provide direct insights for currently cautious investors in the biopharmaceutical sector.

This data is equally enlightening for Biotech founders and large pharmaceutical companies. Amid the recent “double winter” in both the domestic and overseas biopharmaceutical markets, transaction volumes have declined sharply. Biotech founders are striving to turn the tide against headwinds, yet they continue to face tight cash flows; while large pharmaceutical companies hold substantial cash reserves, their pace of innovation-driven transformation remains relatively slow.

Is a startup biotech company guided by a small-scale farmer’s mindset, working in isolation, or does it integrate into the ecosystem to achieve win-win collaboration? This is a strategic question that founders must consider from the outset.

Timing: Significant dividends from early collaboration with large pharmaceutical companies

In the aforementioned report, Gina Melchner von Dydiowa and colleagues conducted multi-dimensional statistical data analysis on the impact of pharmaceutical company investments on the success rate of biotech firms, from which we can derive two key insights:

First,This report provides a comprehensive examination of the correlation between pharmaceutical companies’ participation in investment and the success rate of biotech exits:Biotech companies backed by large pharmaceutical firms have a 46% exit success rate, whereas those without pharmaceutical investment have only a 22% exit success rate.

Figure 1 | Comparison of Success Rates Between Startups with and without Investment from Large Pharmaceutical Companies

Light blue: Success rate of biotech companies with pharmaceutical investment; Dark blue: Success rate of biotech companies without pharmaceutical investment

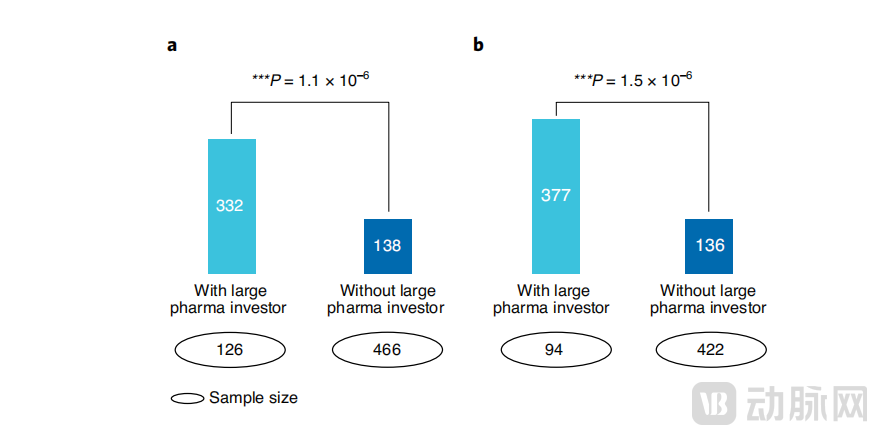

Biotechs backed by large pharmaceutical companies have seen astonishing increases in market capitalization and acquisition value, with acquisition valuations nearly doubling.The median market capitalization of newly listed startups increased from $138 million to $332 million, while the median acquisition value rose from $136 million to $377 million.

Figure 2 | Median market capitalization and acquisition value of startups with and without large pharmaceutical company investors. a, Market capitalization; b, Acquisition value.

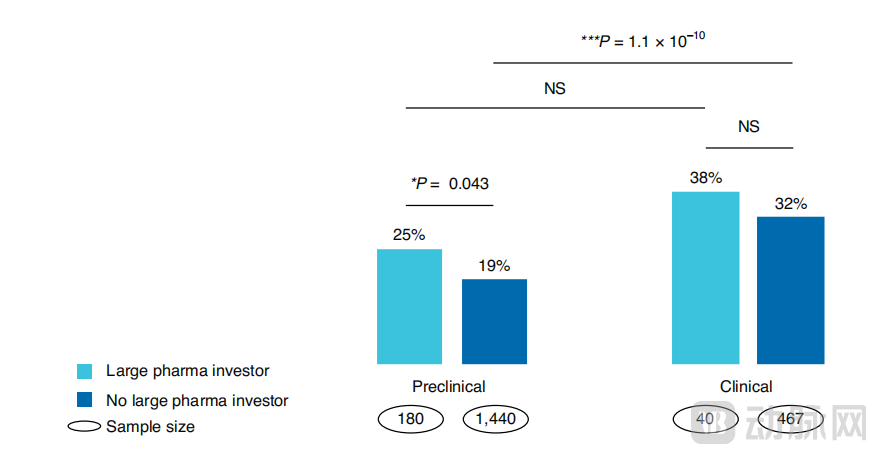

Second, regarding the timing of investments, early-stage (clinical or pre-clinical) investments offer substantial dividends. Betting on potential Biotech companies early yields favorable returns.

Nowadays, large pharmaceutical companies and Biotech entrepreneurs generally believe that investment from big pharma becomes particularly important only when a Biotech company approaches its exit stage. In fact, securing pharmaceutical investment during clinical development (or even earlier) is a mutually beneficial exploration for both parties.

Statistical data indicate that the success rates of companies still in the preclinical stage increase when large pharmaceutical companies are involved. Without the participation of large pharmaceutical companies, the success rate is 19%; with their involvement, it rises to 25%. A similar trend is observed among clinical-stage companies: the success rate increases from 32% without investment from large pharmaceutical companies to 38% with such investment. Although the difference is not statistically significant due to the small sample size, this disparity provides some inspiration for startups.

Figure 3 | Startup success rates (IPO or acquisition) by development stage in the first round of venture financing

Left: Preclinical Stage Right: Clinical Stage Light Blue: Backed by Large Pharmaceutical Companies Dark Blue: Not Backed by Large Pharmaceutical Companies

Biotech is a quintessential growth investment sector, offering substantial appreciation potential.Identifying high-potential companies and investing during the preclinical or clinical stages, while participating in optimizing the clinical validation process, offers the opportunity to achieve high returns after clinical validation with relatively small investments. Once a biotech company enters the Proof of Concept (POC) stage, it may face a situation where risks remain significant despite already elevated valuations. In the mid-to-late clinical stages, although certainty increases, severe valuation bubbles in recent years may lead to declining returns; thus, “high investment” at this stage does not necessarily guarantee “high returns.”

Some Chinese pharmaceutical companies with a keen sense of industry trends recognized the benefits of early-stage investment long ago and have concentrated their efforts on “nurturing-style” investments.

On April 25, 2022, Sino Biopharmaceutical Limited issued an announcement stating that its subsidiary, Chia Tai Tianqing, had entered into an exclusive license and transfer agreement with Anyuan Pharmaceutical for the development and commercialization rights of AP025 and AP026, novel biologics for the treatment of non-alcoholic steatohepatitis (NASH) and type 2 diabetes mellitus (T2DM), in China and certain Asian regions.

At the time of signing the agreement, AP025 was still undergoing Phase I clinical trials in China, while AP026 was still conducting Phase I clinical trials abroad and planned to submit an Investigational New Drug (IND) application in China in 2022.

Furthermore, many of the innovative drugs that Chia Tai Tianqing focuses on are still in the preclinical stage.

Collaborating at the clinical stage offers a high cost-effectiveness ratio for both biotech firms and pharmaceutical companies.

Statistical data has, to some extent, validated the rationale behind this approach; as mentioned above, when large pharmaceutical companies are involved, the success rate of biotech firms still in clinical or preclinical stages increases by approximately 6%.

For biotech companies, it is no longer the case that they can survive by going it alone and enduring for a few years, as was possible in previous years.The biopharmaceutical industry is subject to rapid and dramatic changes, where time and cash flow are critical; a difference of just one year can determine survival or failure. This 6% increase in success rate is sufficient to address many challenges encountered during the clinical phase.Access to superior R&D resources and platforms largely mitigates the risk of new products failing during clinical development due to corporate cash flow disruptions.

For large pharmaceutical companies, the transition to high-quality innovative enterprises should be made sooner rather than later. As the tide of the times moves forward, those who break through will thrive, while others will fall behind and be eliminated.

“The Era of Coopetition”: Banding Together for Warmth, Advancing at Double Speed

For China’s pharmaceutical industry, domestic business development (BD) collaborations are undergoing a major transformation. Large pharmaceutical companies are actively partnering with biotech firms that possess innovative strengths, leveraging their own advantages in cash flow and commercialization capabilities, thereby gradually shaping a comprehensive landscape of “coopetition.”

In late November 2021, Hengrui Medicine announced a collaboration with CStone Pharmaceuticals. Under the agreement, Hengrui will pay an upfront fee and R&D milestone payments totaling up to approximately RMB 1.3 billion, plus tiered royalties in the double-digit percentages of annual net sales after product launch. Through this deal, Hengrui has in-licensed the anti-CTLA-4 monoclonal antibody CS1002, securing exclusive rights for its development, registration, manufacturing, and commercialization in the Greater China region.

In the first half of 2022, CSPC Pharmaceutical Group completed the acquisition of 100% equity interest in Zhuhai Zhifan from an independent third party. Zhuhai Zhifan holds RMB 94.4529 million in registered capital of Mingkang Biopharma (of which RMB 32.8665 million remains unpaid), accounting for approximately 51% of Mingkang Biopharma’s total registered capital as of the date of this announcement.

This has become a landmark event in the acquisition of biotech companies by large traditional pharmaceutical enterprises in China, possibly signaling the imminent onset of a wave of acquisitions by traditional pharmaceutical companies.

Mergers and acquisitions of overseas biotech firms by large pharmaceutical companies are commonplace, whereas successful acquisitions of biotech companies by domestic large pharmaceutical firms are rare, particularly in the innovative drug sector.

The pharmaceutical markets in Europe and the United States matured early, characterized by highly specialized division of labor among pharmaceutical companies and the long-established formation of monopolistic structures. Most biotech founders anticipate that while independently innovating and developing a single pipeline product is not difficult, it is challenging to build a fully integrated, large-scale pharmaceutical company relying solely on internal resources. Consequently, many biotechs seek to leverage the strengths of traditional large pharmaceutical companies from their inception, aiming to sell and monetize their assets as soon as specific pipelines reach the clinical stage.

Many founders of biotech companies in China come from scientific research backgrounds. Although their product pipelines were initially narrow, they often harbored grand visions of becoming integrated pharmaceutical enterprises covering the entire industry chain—R&D, manufacturing, and sales—through horizontal and vertical expansion, thereby securing a foothold in specific therapeutic categories. Currently, most Chinese biotechs prefer to “license out assets rather than sell themselves,” opting to sell rights to innovative drugs while resisting acquisition.

Founders of domestic biotech companies urgently need to shift their mindset.In mature pharmaceutical markets such as those in Europe and the United States, the majority of biotech companies end up being acquired by large pharmaceutical firms. This exit pathway is, in fact, just the tip of the iceberg of industrial division of labor and collaborative models, and it represents an inevitable trend as the market matures. Consequently, this has become the predetermined development path for most biotech companies from their inception.

Mergers and acquisitions do not mark the end; rather, it is possessing innovative technology that fails to truly impact the market that leads to obsolescence.

References:

1.Melchner von Dydiowa G, van Deventer S, Couto DS. How large pharma impacts biotechnology startup success. Nat Biotechnol. 2021 Mar;39(3):266-269. doi: 10.1038/s41587-021-00821-x. PMID: 33589817.

2.https://mp.weixin.qq.com/s/TF5WOXBDB5VDdqsyCMAVZA

3.https://zhuanlan.zhihu.com/p/546843581