Ophthalmic Giants Invest Over $7 Billion in MIGS: What’s Driving the Surge?

Alcon

Ophthalmic Pharmaceuticals and Medical Devices Manufacturer

Allergan

Global Pharmaceutical Manufacturer

Minimally Invasive Glaucoma Surgery (MIGS) has become a hot sector with intensive strategic investments by ophthalmic giants over the past two years.

VCBeat (WeChat ID: vcbeat) has compiled statistics showing that global ophthalmic giants have invested over RMB 5 billion in the field of minimally invasive glaucoma surgery (MIGS). The two most recent deals occurred this July: AbbVie invested $60 million in iStar Medical, a Belgian MIGS device manufacturer; subsequently, Bausch + Lomb invested in Sanoculis, an Israeli MIGS company. The two companies also established a strategic partnership, granting Bausch + Lomb exclusive distribution rights for Sanoculis products in Europe.

In 2021, another ophthalmic giant, Alcon, acquired Ivantis, a manufacturer of glaucoma stents, for $475 million; earlier, in 2015, Allergan had acquired AqueSys, a developer of MIGS products, for $300 million.

In China’s primary market, attention to minimally invasive glaucoma surgery (MIGS) is also on the rise. Several companies have secured funding in rapid succession this year, signaling that domestic capital is beginning to focus on this sector.Allergan’s XEN Gel Stent for glaucoma drainage is also accelerating its commercialization in China, with initial implantation surgeries completed at multiple hospitals across the country. Santen’s Preserflo MicroShunt for glaucoma drainage has also been implanted in China.

Why Have Glaucoma Drainage Devices, With Diameters on the Same Order of Magnitude as a Human Hair, Attracted Frequent Attention from Ophthalmic Industry Giants? What New Breakthroughs Can MIGS Bring to Glaucoma Treatment? VCBeat Has Compiled an Overview of the MIGS Landscape.

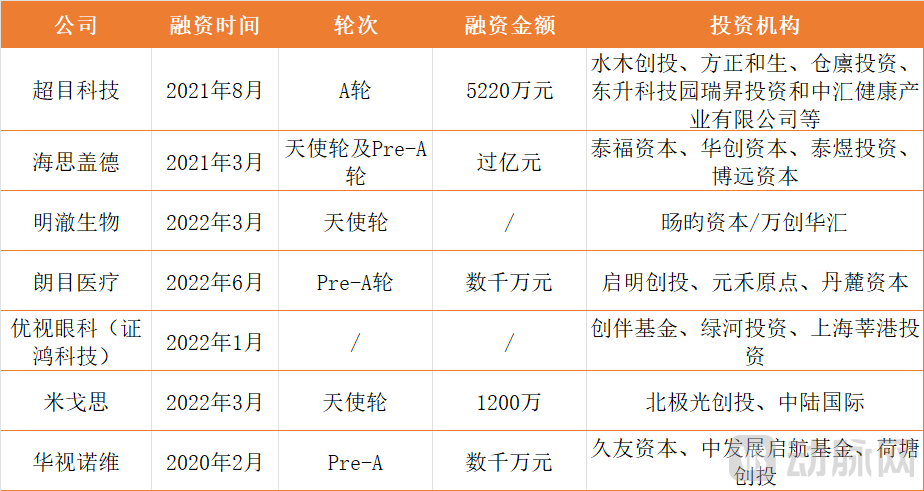

Financing Events in the Domestic MIGS Sector

Why Have Industry Giants Frequently Focused on Minimally Invasive Glaucoma Surgery Over the Years? The Fundamental Reason Is the Unmet Needs in the Field of Glaucoma Treatment.

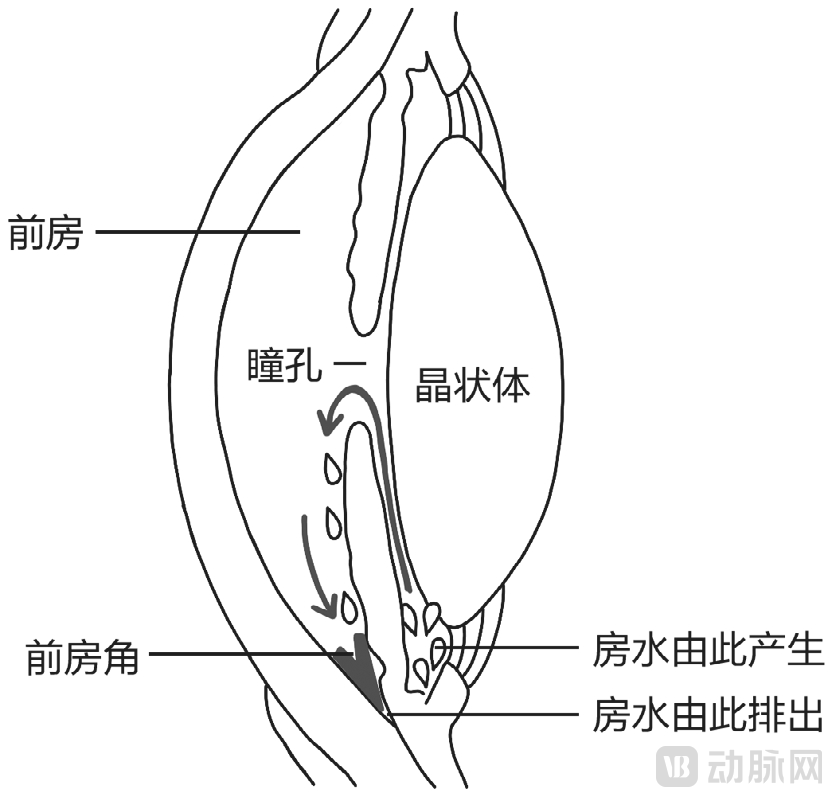

Glaucoma patients experience elevated intraocular pressure due to impaired aqueous humor circulation within the eye, which exceeds the tolerance limit of the optic nerve and results in chronic optic nerve damage.

Image source: "Glaucoma Is the Thief of Light"

Glaucoma ranks second among blinding eye diseases, following cataracts. The most significant difference between glaucoma and cataracts is that vision loss from cataracts can be restored through surgery, whereas the visual impairment caused by glaucoma is irreversible and cannot be salvaged by medication or surgical intervention.

Glaucoma affects over 100 million people worldwide. According to the Chinese Glaucoma Guidelines (2020), it is estimated that the number of glaucoma patients in China reached 21 million in 2020, with up to 5.67 million cases resulting in blindness. In China, the majority of glaucoma patients still struggle to receive early diagnosis and timely, appropriate treatment. The incidence of glaucoma gradually increases with age, and as the population ages, the prevalence of glaucoma in China is expected to continue rising.

Current glaucoma management primarily relies on pharmacotherapy, laser therapy, and surgical intervention. Lowering intraocular pressure through medication or surgery helps slow disease progression. Pharmacological treatment is typically the first-line approach; however, the escalating number of eye drops may cause side effects for patients, while daily administration poses challenges to adherence and imposes a financial burden. Invasive surgeries carry the risk of irreversible complications and generally require long-term patient management.

Compared with pharmacological and surgical treatments, MIGS has garnered attention in glaucoma management due to its advantages of being minimally invasive and safe.

Compared with traditional glaucoma surgery, MIGS offers advantages such as minimal invasiveness, reduced disruption to anatomical and physiological structures, high safety profile, shorter operative time, and faster recovery.

Its safety profile has positioned MIGS as the most promising therapeutic approach for glaucoma. According to data from iStar Medical’s official website, MIGS is the fastest-growing treatment modality for glaucoma, with a global average annual growth rate of 24% in surgical volume.

However, existing MIGS products also have disadvantages., the Chinese Glaucoma Guidelines 2020 state that current data indicate significantly lower complication rates with minimally invasive internal drainage surgery compared to traditional trabeculectomy, while its intraocular pressure-lowering efficacy is not superior to that of trabeculectomy. Furthermore, existing MIGS procedures are not suitable for patients with advanced glaucoma who require sustained intraocular pressure reduction and medication reduction.

Currently, the leading MIGS products in the U.S. market, iStent and XEN, were developed relatively early and have a decade-long history. With advancements in materials and technology, superior MIGS products are expected to emerge in the future, addressing the limitations of earlier generations.

Ophthalmic giants’ continued investment in this field reflects their bet on superior next-generation MIGS technologies. One reason for the rising interest in MIGS is the emergence of more innovative products globally in recent years.

The market prospects for MIGS are equally promising. In China, approximately 450,000 glaucoma surgeries are performed annually, the vast majority of which are conducted on patients in the middle to late stages of the disease. MIGS products are primarily indicated for early-stage patients. According to capital market estimates, the existing pool of approximately 3.7 million glaucoma patients in China represents the potential target population for MIGS procedures.

Regarding the growing attention to MIGS in China, an industry insider calmly stated, “After 2015, with Glaukos launching the next-generation iStent inject, the U.S. MIGS market began to grow rapidly. The widespread adoption of MIGS in the United States has also drawn the attention of Chinese physicians, and MIGS is now routinely discussed at academic conferences on glaucoma in China. However, the current enthusiasm is primarily at the capital investment level. In terms of actual clinical application, there are few MIGS products approved in the Chinese market, and their utilization remains low. The field is far from reaching a boom stage and requires more data to gain acceptance among physicians.”

MIGS is widely recognized as the future of glaucoma treatment, but the more critical question is: which specific MIGS procedure will become the mainstream standard in the future?

Unlike minimally invasive procedures for cerebrovascular and cardiovascular diseases, MIGS encompasses a diverse array of surgical techniques.The ophthalmology industry defines MIGS not based on products, but by differentiating clinical treatment pathways.。

Kan Min, co-founder of Langmu Medical, told VCBeat: “MIGS can be classified into four categories based on clinical treatment pathways.”The first category is ciliary body destructive surgery,Destroying the ciliary body, the tissue that produces aqueous humor, to reduce its production; UCP (Ultrasound Cyclo Plasty), currently being promoted in China, falls into this category;The second type is subconjunctival drainage, which drains aqueous humor into the subconjunctival space, with XEN being a representative product;The third category is the pathway entering Schlemm's canal via the trabecular meshwork., with representative products including the U.S.-based iStent inject, Hydrus, and the ELT product launched by our U.S. partner;The fourth category is suprachoroidal drainage,"AbbVie's recently acquired iStar Medical is a representative of the suprachoroidal approach."

Why Are There Multiple Clinical Treatment Pathways for MIGS?

Kan Min stated that this is determined by the mechanism of aqueous humor production. After being produced by the ciliary body, aqueous humor first enters the posterior chamber, then passes through the pupil into the anterior chamber, and subsequently flows to the anterior chamber angle. The majority of aqueous humor enters Schlemm's canal via the trabecular meshwork at the anterior chamber angle, with 70%–95% of aqueous humor draining through this pathway. A small portion of aqueous humor is drained out of the eye through the suprachoroidal space.

Upon understanding the underlying principles, one can better grasp the differences and characteristics of the four MIGS pathways and their representative products.

Cyclodestructive procedures are surgeries that destroy the ciliary body responsible for aqueous humor production, thereby reducing aqueous humor formation.thereby addressing the issue of glaucoma. Taking UCP (Ultrasound Cyclo Plasty) as an example, this procedure employs high-intensity focused ultrasound technology to remodel the ciliary body structure and reduce aqueous humor production. Currently, this technique is being promoted in numerous ophthalmic hospitals, including Aier Eye Hospital.

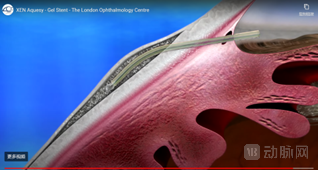

Subconjunctival drainage, a therapeutic approach derived from the gold-standard surgical treatment for glaucoma, neither destroys tissues involved in aqueous humor production nor diverts aqueous humor into the eye’s natural outflow pathways; instead, it artificially constructs an alternative egress route for aqueous humor.. Allergan’s XEN belongs to this field. The XEN received FDA approval for market launch in 2013, making subconjunctival drainage more minimally invasive. To date, over 100,000 XEN implants have been performed worldwide. In 2020, Allergan’s XEN glaucoma drainage device was approved in China, and the first surgeries have since been completed at multiple hospitals across the country.

XEN Implantation Example

The trabecular meshwork–Schlemm’s canal pathway has previously received considerable attention.Since the trabecular meshwork–Schlemm’s canal pathway is inherently the primary route for aqueous humor outflow, the representative product for this approach is the iStent series launched by Glaukos.

Glaukos, founded in 1998, is the world’s first company to bring minimally invasive glaucoma surgery (MIGS) to market. The iStent product line comprises three generations; the first-generation iStent was launched in 2012, and the next-generation iStent inject was introduced in 2018.

To date, the iStent has been implanted in 800,000 to 1 million cases. In terms of sales revenue, the iStent series has also seen continuous growth. According to Glaukos’s 2021 annual report, iStent technology accounted for 79% of sales revenue.In 2021, Glaukos reported revenue of $294 million, with estimated iStent sales of approximately $230 million.。

The suprachoroidal space as a therapeutic approach is also based on the natural anatomy of aqueous humor outflow.Although the suprachoroidal space accounts for only 5%–30% of aqueous humor outflow, establishing a drainage pathway through this space could potentially achieve drainage efficacy significantly exceeding 30%. Consequently, at least three companies worldwide have established a presence in this field. The most representative product in this area previously was Cypass, launched by Alcon following its acquisition in 2016. However, CyPass was recalled two years after its market launch due to excessive loss of corneal endothelial cells.

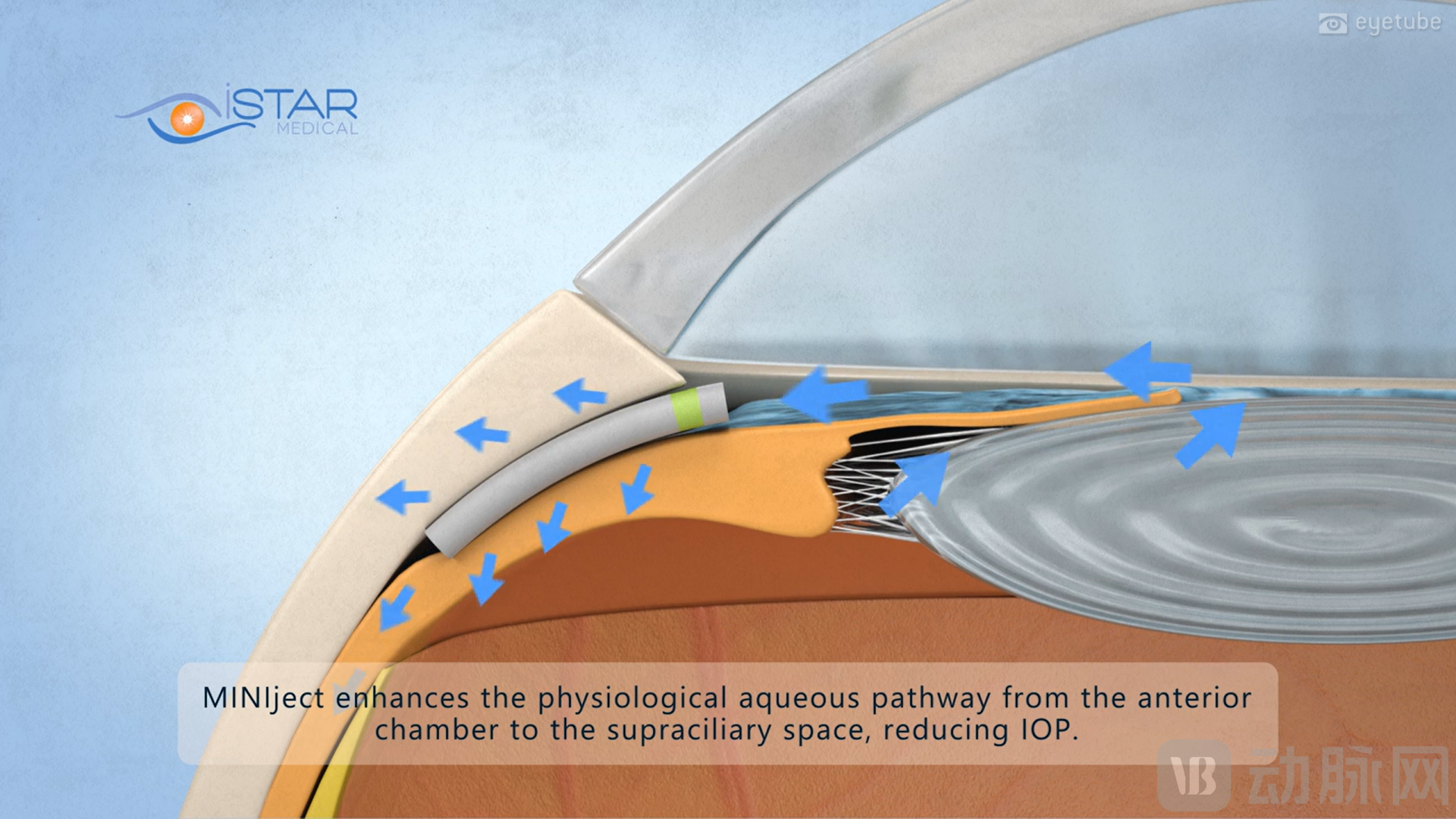

Nevertheless, this approach remains highly favored by industry giants. MINIject, developed by iStar Medical—which received a RMB 300 million investment from AbbVie—utilizes the suprachoroidal delivery route.

What features of MINIject stood out in the diverse MIGS landscape to attract AbbVie’s interest?

Kan Min stated, “I speculate that this is primarily based on the favorable clinical results of MINIject to date. Independent two-year clinical data for MINIject® show that intraocular pressure (IOP) was significantly reduced to <15 mmHg in most patients, with a low incidence of complications and a favorable safety profile regarding endothelial cell density over the two-year period.”

MINIject Product Sample Image

MIGS: Amidst Fierce Competition, Which Products Will Prevail? What Are the Future Development Trends?

Kan Min explained, “Experts abroad have previously analyzed what constitutes an ideal MIGS product, identifying three most critical criteria: sufficient intraocular pressure (IOP) reduction, sustained IOP-lowering effect, and a sufficiently minimally invasive surgical procedure. However, balancing these three aspects is often challenging; typically, a highly minimally invasive approach fails to achieve adequate and sustained IOP reduction. Nevertheless, we believe that in the near future, through the collective efforts of the entire industry, it will be possible to develop superior products that simultaneously meet all three criteria.”

For domestic companies, the research and development of MIGS products faces more challenges. The challenges mainly stem from the differences in disease types between Chinese patients and American patients, as well as the differences in medical environments.

Glaucoma is primarily classified into three major categories: primary glaucoma, secondary glaucoma, and congenital glaucoma. Primary glaucoma includes two subtypes: primary open-angle glaucoma and primary angle-closure glaucoma.Primary open-angle glaucoma (POAG) and primary angle-closure glaucoma (PACG) account for over 90% of the patient population.

Globally, two-thirds of glaucoma patients have open-angle glaucoma, which is the most common type; however, angle-closure glaucoma carries a higher risk of blindness. In Europe and North America, open-angle glaucoma is the predominant form, accounting for 74% of all glaucoma cases.

In contrast to Europe and the United States, angle-closure glaucoma is the predominant type in China and Southeast Asia, accounting for 87% of glaucoma patients.Although the proportion of angle-closure glaucoma has significantly decreased in recent years due to improved early diagnosis, the growing prevalence of myopia, and the earlier performance of cataract surgery when viewed from a long-term development perspective, the treatment demand for patients with angle-closure glaucoma in China remains substantial and cannot be overlooked.

Moreover, due to the insidious onset of primary open-angle glaucoma, there may be no symptoms in the early stages. Patients in China are often diagnosed at moderate to advanced stages., whereas most MIGS products developed by European and American companies are only suitable for patients with early-stage or mild disease.

Divergent patient demographics and clinical needs have led to a differentiation in how Chinese and U.S. companies address glaucoma. In addition to open-angle glaucoma, MIGS products from Chinese manufacturers also target angle-closure glaucoma and patients with moderate-to-advanced disease.

Taking Langmu Medical as an example, the company has independently developed AqueFish™, an innovative stent product for glaucoma treatment with original Chinese intellectual property. This product not only significantly improves the success rate of glaucoma surgery but also stands out as one of the few stents internationally suitable for both angle-closure and open-angle glaucoma. Meanwhile, Langmu Medical continues to deepen its expertise in other ophthalmic fields, having established a pipeline of multiple innovative ophthalmic products that are expected to receive regulatory approval and launch in the coming years.

Another Chinese company, HiSight Medical, has developed a relatively comprehensive portfolio of minimally invasive glaucoma surgery (MIGS) products, addressing both the early-to-mid and late stages of glaucoma progression. Specifically, for open-angle glaucoma, HiSight Medical has developed the MicroCOGO implantable stent, which features an outer diameter of less than 300 micrometers and an internal lumen with a minimum diameter of approximately 30–40 micrometers.

Mingche Biologics’ product architecture is directly derived from the XEN platform. However, unlike the XEN’s uniform-diameter drainage tube, Mingche Biologics employs a tapered inner diameter design to effectively enhance drainage efficiency. This design also enables directional drainage and prevents backflow, thereby mitigating postoperative complications associated with excessively low intraocular pressure. The device’s outer wall features a fixation structure that facilitates intraoperative positioning, improves the success rate of primary implantation, and prevents postoperative migration.

Although MIGS is gaining momentum in China, entrepreneurs who have been deeply rooted in this field for years remain most concerned with solving the challenges of glaucoma treatment. Regardless of whether capital interest surges or wanes, they maintain a rational approach amidst the hype.

Frankly speaking, the global MIGS market has developed most robustly in the United States. In other regions, particularly in China, MIGS adoption remains in its very early stages. To gain broader acceptance among physicians and patients, more domestic data from China are needed to address key questions.

Meanwhile, beyond glaucoma, numerous other ophthalmic conditions warrant attention. The field of ophthalmology is emerging as a hotbed for global medical device innovation. In addition to minimally invasive glaucoma surgery (MIGS) instruments, ophthalmic surgical robots are also garnering significant interest. In July 2022, ForSight, an Israeli company specializing in ophthalmic surgical robotics, secured $55 million in financing. Its surgical robot is designed to perform cataract surgeries. A wave of innovation in ophthalmic devices is also surging in China, holding promise for delivering more innovative solutions to the treatment of eye diseases worldwide.

Reference Article:

Alcon tries again in Migs——Evaluate

VBInsight Research | Ophthalmic MIGS Surgical Instruments: Next-Generation Glaucoma Diagnosis and Treatment Technology

Professor Zhang Chun: A New Device Turning Old Ideas into Reality—Minimally Invasive Glaucoma Surgery Market Scope, “2021 Glaucoma Surgical Device Market Report”, July 2021; Jonas JB, Aung T, Bourne RR et al, “Glaucoma”, Lancet 2017; 390: 2083–93