Stryker Acquires Amplitude Vascular Systems to Expand Peripheral Vascular Portfolio with Novel CO₂-Powered IVL Technology

Stryker

Medical Device R&D, Production, and Sales Company

AVS

Developer of Calcified Artery Disease Treatment Devices

Inari Medical

Cardiovascular Disease Treatment Device Developer

April 13, 2026Stryker (NYSE: SYK) announced the signing of a definitive agreement to acquire Amplitude Vascular Systems (AVS), with the transaction amount undisclosed.。AVS is a privately-held medical device company headquartered in Boston, with core products.Pulse IVL SystemBased on pressure waves generated by pulsed CO₂, calcified peripheral arterial disease (Peripheral Arterial Disease, PAD) is treated using Intravascular Lithotripsy (Intravascular Lithotripsy, IVL) balloon catheters.

This is Stryker's second acquisition in the peripheral vascular sector within 14 months.In February 2025, Stryker completed the acquisition of Inari Medical for $4.9 billion, gaining access to a venous thromboembolism (VTE) mechanical thrombectomy product line centered around FlowTriever and ClotTriever. This acquisition of AVS marks Stryker's further expansion from "thrombectomy" in the venous system to "calcium modification" in the arterial system, accelerating the formation of its peripheral vascular platform strategy.

The significance of this signal lies in:One of the largest orthopedic device companies in the world is shifting its growth engine from orthopedics to vascular intervention — and one of the end-stage manifestations of PAD is critical limb ischemia (CLI), which significantly overlaps with the patient population for orthopedic lower extremity surgeries.

# Pulse IVL: CO₂ Pulse Wave Pathway, POWER PAD 2 Pivotal Trial Ongoing

AVS's Pulse IVL System Uses CO₂ Gas Pulses to Generate High-Frequency Pressure Waves, Which Are Uniformly Transmitted to Vascular Wall Calcifications Through a Non-Compliant Balloon, Causing Them to Fragment and Restore Luminal Patency.This mechanism differs from both Shockwave Medical's (a J&J subsidiary) electrohydraulic shockwave and Boston Scientific's Bolt Medical/Seismiq system’s laser-generated acoustic pressure wave, which currently dominate the market.

AVS Obtained FDA Investigational Device Exemption (IDE) in June 2024, Launching the Pivotal POWER PAD 2 Clinical Trial (NCT06457685), Enrolling Approximately 115-120 Patients with Moderate to Severe Calcific Stenosis in the Superficial Femoral and Popliteal Arteries Across 20 Centers in the United States. The trial data is expected to be completed by 2026, serving as the critical pathway for AVS to obtain FDA marketing approval. In the fall of 2025, AVS had already released early clinical data for this platform.

Stryker stated that once Pulse IVL receives market approval in relevant markets, it will complement its existing peripheral vascular products to serve the revascularization needs of arterial diseases.

# IVL Track Competition Pattern: From Shockwave's Monopoly to Four-Way Struggle

The rapid adoption of IVL technology in peripheral and coronary calcified lesions has made it one of the fastest-growing segments in the interventional cardiovascular field. The utilization rate of Shockwave Medical's IVL technology in coronary procedures has exceeded 10% (disclosed by the company's CMO, Nick West). In June 2024, J&J acquired Shockwave Medical for $13.1 billion, pushing IVL to the forefront of global medical device M&A.

Following this, competitors entered the market in rapid succession. In January 2025, Boston Scientific acquired Bolt Medical for a total consideration of approximately $664 million (including $443 million upfront and up to $221 million in regulatory milestone payments), gaining access to the laser IVL platform. Bolt's system received FDA 510(k) clearance in April 2025 and was commercially launched in the U.S. under the Seismiq brand for ATK (Above-the-Knee) peripheral IVL, while patient enrollment for the FRACTURE IDE trial for coronary IVL has been completed.

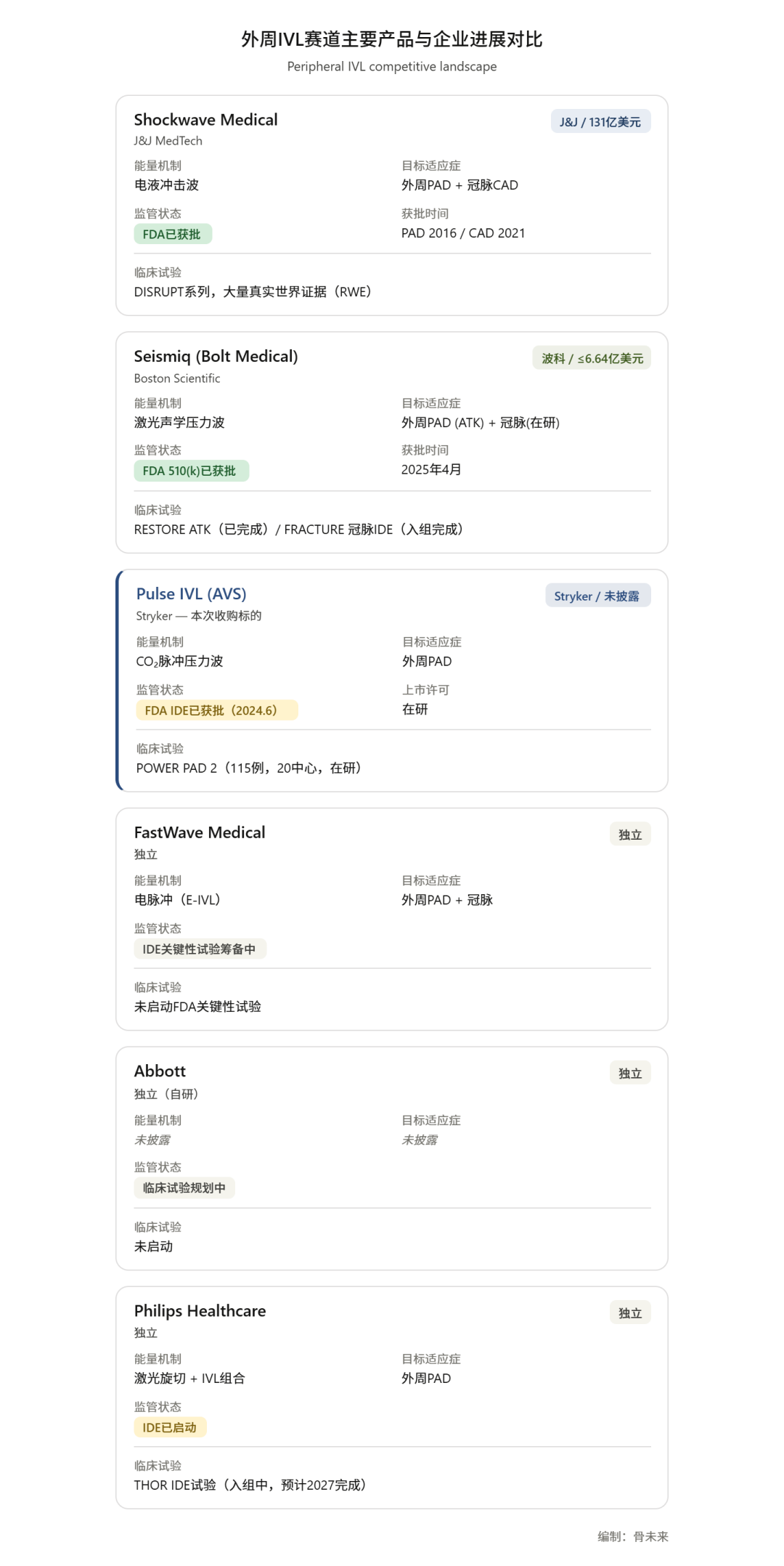

Comparison of Main Products and Corporate Progress in the Peripheral IVL Market

# Stryker's Peripheral Vascular Puzzle: From Orthopedic Giant to Vascular Intervention Platform

Stryker's position in the orthopedic field goes without saying — its four core business lines, including joint replacement, spine, trauma, and sports medicine, constitute its main sources of income. However, based on the M&A trajectory from 2024 to 2026, the company is rapidly building a second growth platform.

Stryker's neurovascular business (centered around the Target series of thrombectomy stents, Surpass Streamline flow diverter, etc.) has been operating for many years and serves as the foundation of its interventional vascular field. In 2025, Stryker acquired Inari Medical for $4.9 billion, directly entering the peripheral venous thrombectomy (VTE) market—this is one of Stryker’s largest acquisitions in history. Inari Medical’s revenue in 2024 was approximately $603 million. With this latest acquisition of AVS, Stryker expands its peripheral vascular portfolio from "venous thrombectomy" to "arterial calcium fragmentation," forming a more comprehensive peripheral vascular solution suite.

CEO Kevin Lobo clearly positioned this acquisition as part of the strategy to "build a comprehensive peripheral vascular platform" in the statement. In contrast, three giants—J&J (through Shockwave), Boston Scientific (through Bolt/Seismiq), and Stryker (through Inari + AVS)—have already formed a clear competitive landscape in the peripheral vascular intervention field, all entering through mergers and acquisitions.

# Conclusion

Stryker’s acquisition, while potentially limited in scale (AVS is still in the IDE trial phase with no approved products yet), sends a clear signal from a strategic narrative perspective:Traditional orthopedic giants are systematically building their "second engine," with peripheral vascular intervention being the clearest direction at present.Two M&A Deals Within 14 Months (Inari Medical $4.9 Billion + AVS Undisclosed), Corresponding to Two High-Growth Segments: VTE Thrombectomy and PAD Lithotripsy, Stryker’s Peripheral Vascular Platform Takes Shape.

For participants in the orthopedic industry, a trend worth considering is: as joint replacement and spinal procedures enter a phase of routine centralized procurement with slowing growth rates, leading companies are shifting their growth narratives towards "pan-interventional" solutions.

Key Enterprises and Institutions

▌Well-known Medical Technology Innovation Enterprises:Medtronic | Boston Scientific | Kaili Medical | Alcon | Minimally Invasive Robot | Rosenthal | Cosmind | Maipu Medical | Sino Great Wall

▌Well-known Medical Technology Innovation Service Agency:Bachu整形医学概念验证中心 | Tonghe Lita