How Can Health Insurance Reach the RMB 2 Trillion Target? New Regulations, Product Innovations, and Growth Strategies

Recently, the Property and Casualty Insurance Supervision Department of the China Banking and Insurance Regulatory Commission (CBIRC) issued the “Notice on Issues and Related Risks Identified in Short-Term Health Insurance Business of Certain Property and Casualty Insurance Companies” (hereinafter referred to as the “Notice”), thereby regulating certain aspects of short-term health insurance.

In accordance with the requirements set forth in the “Circular,” certain companies, in the course of collaborating with related business clusters affiliated with internet hospitals, health technology firms, and insurance brokerage agencies, have underwritten post-diagnosis pharmaceutical treatment costs for pre-existing conditions through group medical insurance plans covering specific drugs. Regulatory authorities have since imposed oversight on such products.

Phenomena that contradict industry norms and regulatory policies should indeed be “braked” in a timely manner; however, several industry challenges revealed by the aforementioned products—such as the difficulty for non-standard risks to obtain insurance coverage, achieving healthy growth in health insurance performance, and the lack of payers in internet healthcare—remain issues that the industry must directly confront and overcome. Meanwhile, the “Internet + Pharmaceutical Insurance” integrated innovation model that has emerged in recent years also needs to undergo iterative updates under the premise of compliance.

What are the breakthroughs for the major challenges ahead? Where do the innovation opportunities lie? VCBeat engaged in discussions with numerous entrepreneurs and innovators across the health insurance industry chain to provide analysis and outlook.

For a long time, mainstream health insurance products have largely targeted healthy individuals. Currently, non-standard risks have become a key target customer segment for health insurance expansion.

Non-Standard Health Insurance Emerges as a Blue Ocean

Due to higher health risks and greater health management costs, substandard risks pose stricter requirements on insurers’ risk control capabilities. Historically, such individuals were typically declined coverage. Even when substandard risks are able to obtain insurance, their coverage benefits are inferior to those offered to healthy individuals; for example, policy terms may exclude pre-existing conditions, or higher premiums may be required to secure coverage comparable to that provided to standard risks.

However, from the demand-side perspective, the large populations of individuals in suboptimal health status and those with chronic diseases have generated robust demand for commercial health insurance. According to reports from research institutions such as the National Center for Cardiovascular Diseases and the National Cancer Center, there are approximately 500 million patients with thyroid nodules, around 100 million each with pulmonary nodules and breast nodules, and about 360 million patients with hypertension in China.

From the supply-side perspective, the penetration rate of health insurance among healthy individuals is increasing, but growth has slowed, necessitating the expansion of coverage to non-standard risk populations to generate new growth. Meanwhile, products targeting healthy individuals offered by insurers are highly homogeneous, leading to intense competition, whereas the non-standard risk population presents greater opportunities for differentiation.

From a policy perspective, in 2021, the General Office of the China Banking and Insurance Regulatory Commission issued the "Guiding Opinions on Further Enriching the Supply of Life Insurance Products," encouraging the moderate relaxation of underwriting conditions to meet consumers' diversified insurance needs.

Over the past two years, the gradual expansion of health insurance coverage to include non-standard risks has become an inevitable trend, with the non-standard risk health insurance market regarded as a blue ocean.

With the emergence of Huiminbao (city-specific supplemental medical insurance) and single-disease insurance products for non-standard risks, the challenges in obtaining coverage have been alleviated to some extent; however, there remains significant room for improvement in terms of coverage scope and benefit entitlements.

Gradually expand market penetration based on technical capabilities

“Non-standard risks are further segmented into several groups based on health status: the ‘abnormal’ group, referring to individuals with abnormal test indicators but without a diagnosed disease; the ‘general pre-existing condition’ group, referring to those who have already entered a disease state; and the ‘severe pre-existing condition’ group, covering serious conditions such as cancer and severe sequelae of cardiovascular and cerebrovascular diseases.” Zhang Qingfeng, founder of AIXuan Technology, introduced that currently, the accessibility of health insurance varies across these segmented populations. Overall, accessibility is highest for the “abnormal” group, which may even be eligible for standard insurance benefits, while accessibility for the “severe pre-existing condition” group remains extremely limited.

Historically, health insurance excluded non-standard risks, largely due to technical constraints such as limited actuarial data and modeling capabilities, which made scientific pricing difficult. With the advancement of big data, artificial intelligence, and other technologies, more reasonable pricing for coverage of non-standard risks has become feasible.

Zhang Qingfeng pointed out that, at this stage, technology is no longer the absolute hurdle for non-standard health insurance; the greater obstacles lie in consumer awareness and sales services.

In the early stages of introducing non-standard health insurance products to the market, insurers either excluded certain pre-existing conditions or charged higher premiums. This approach negatively influenced consumer perception, leading many to believe that coverage was inadequate and thus reducing their willingness to purchase. The lack of consumer demand, in turn, prevented health insurance products from achieving economies of scale, which diminished insurers’ incentives to continue offering such products, thereby disrupting the virtuous cycle between supply and demand.

In terms of sales, the key challenge lies in determining how to sell insurance to substandard risks. For highly standardized products such as critical illness insurance, explanations can be clearly communicated through both traditional and internet channels. However, substandard risks present more varied scenarios and involve more complex issues that require clarification.

Therefore, he believes that the key to resolving these issues lies in the gradual liberalization across three dimensions.

First, access should be gradually expanded to include individuals with non-standard health profiles and the elderly, adopting a stratified, proportional, and stepwise approach. “For instance, coverage for patients with type 2 diabetes could initially be extended to 50% of this population; once risks are deemed controllable, it can be progressively increased to 70% and then 90%, based on comprehensive assessments of their physical condition.”

Second, releasing benefits. First, collaboration among all parties in the industrial chain enables individuals with abnormal health indicators and those with general pre-existing conditions to receive the same coverage benefits as healthy individuals, which is also key to addressing consumer perceptions. Second, specific benefits are designed starting from a small subset of individuals with severe pre-existing conditions. “For example, recurrence insurance for breast cancer; coverage for targeted therapies for lung cancer patients, which can only be used based on specific targets after genetic testing. These products can be offered to patients with severe pre-existing conditions, provide leverage, and comply with the principle of aleatory contracts.”

Third, there is the expansion of services, encompassing medication and healthcare services. In terms of pharmaceuticals, the focus has shifted from rudimentary to refined offerings, moving from low-probability drugs to conventional medications, thereby complementing the National Reimbursement Drug List. Regarding healthcare services, it is essential to effectively meet consumer demands while ensuring high operational leverage.

Wang Yanping, Founder and CEO of UPlus Health, also noted that the market has been actively exploring underwriting for non-standard risks in recent years. “Individuals with thyroid nodules, breast nodules, the ‘three highs’ (hypertension, hyperglycemia, and hyperlipidemia), pulmonary nodules, as well as those exhibiting pre-disease symptoms, are all key targets for accelerated coverage by health insurance products, with more benefits and services being tailored to these groups. Only by leveraging data analytics and gaining a deep understanding of the core needs of non-standard risk populations can insurers develop superior products, thereby enhancing customers’ willingness to purchase. Meanwhile, identifying appropriate sales scenarios—such as health check-up settings—is also crucial in the sales process.”

As health checkups become more widespread and frequent among the general public, the number of identified substandard risks will continue to grow significantly. By designing products with compliance as a prerequisite and addressing key market challenges, health insurance is poised to achieve substantial growth in the substandard risk segment.

In the early stages of internet healthcare development, growth was constrained by exclusion from national medical insurance coverage and a lack of commercial insurance payment initiatives. Following the introduction of policies on medical insurance reimbursement for internet healthcare services between 2019 and 2020, a large number of public internet hospitals were designated as approved providers under the national medical insurance scheme, while only a very small minority of internet healthcare companies gained access to insurance reimbursement through their affiliated medical institutions. Since then, the industry has increasingly pinned its hopes for payer solutions on commercial health insurance.

Payment Oriented by Real Needs

“A key issue to recognize is that commercial insurance does not create demand,” stated Zhang Qingfeng. “If consumers are unwilling to pay for services on internet healthcare platforms, they are unlikely to generate such demand simply because they have commercial insurance.” Fundamentally, without genuine demand, any number of insurance products would be meaningless and constitute pseudo-demand. Ultimately, the role of commercial insurance in internet healthcare platforms or internet-based services is to meet existing demand and pool payment resources.

Currently, the industry has launched internet-based medical care and commercial health insurance products, represented by internet outpatient insurance. These products typically charge an annual premium of several hundred yuan, provide a certain number of online consultation services throughout the year, and offer reimbursement for medication costs within specified limits, making them generally similar to traditional offline outpatient insurance.

However, from the perspective of internet healthcare, even with active expansion into commercial insurance payments, a sustainable profit model has yet to be identified.

“Insurance requires medical services, and medical services also require insurance as a payer; the relationship between their integrated development is inherently natural,” said Wang Yanping. She noted that enterprises need to give more consideration to how to effectively leverage commercial insurance as a payer, determine the principles guiding product design, and conduct more in-depth segmentation and needs assessment of target populations, so as to achieve deep integration between insurance and services.

Long-Term Commitment to Validating the Effectiveness of Health Management

In 2020, the General Office of the China Banking and Insurance Regulatory Commission (CBIRC) issued the "Notice on Regulating Health Management Services Provided by Insurance Companies," stipulating that the cost proportion of health management services in insurance products could reach up to 20%. Since then, internet-based medical health management services have also been able to use commercial insurance as the payer.

Wang Yanping stated that, after connecting medical, nursing, health management, and pharmaceutical services, the internet can penetrate insurers’ operational systems by delivering customized products to insurance companies, thereby creating greater customer value for them.

Internet-based medical services encompass a wide variety of offerings. Beyond basic online consultations, they include post-diagnosis follow-ups, remote multidisciplinary consultations, remote monitoring, and home nursing care. The key to their deep integration with commercial health insurance lies in collaborating with insurers to tailor service bundles for different customer segments. In particular, if internet-based healthcare can deliver effective health management for insurance policyholders and thereby reduce claims expenditures, its service value becomes even more pronounced.

Behind this lie two prevailing realities facing the health insurance industry. First, penetration among non-standard risks is gradually expanding; the higher health risks associated with non-standard risks necessitate more rigorous risk control. Second, premiums for short-term health insurance continue to grow. As the insured population skews younger, claim ratios remain relatively low in the short term. However, as population aging intensifies in the future, claim ratios are likely to rise. Even if insurers respond by raising premiums, they will still have to address health risk management issues such as disease prevention and post-diagnosis rehabilitation.

The ability of internet-based healthcare to bridge the spatial gap between doctors and patients gives it an advantage in efficiently delivering health management, although its effectiveness still requires validation.

New Growth Directions for Health Insurance and Internet-Based Medical Services: Seemingly Independent Niche Sectors, Yet Intricately Interconnected—This Is the “Internet + Pharmaceutical Insurance” Integration Model That Has Emerged in Recent Years. From the perspective of healthcare payment reforms driving changes in medical service delivery, and the pathway of state-led centralized drug procurement, this model is underpinned by a specific foundational logic. However, given the industry’s current realities, there are no shortcuts to integrated innovation; progress must be made step by step, with the premise of maximizing benefits for all stakeholders, rather than focusing solely on short-term growth in any single dimension.

In this model, technological empowerment is a prerequisite. Previously, participants in the health insurance industry chain incurred high costs when providing services to users through traditional face-to-face interactions and telephone support. Technology has driven the online migration and digitalization of various segments within the industry, thereby reducing associated costs. Meanwhile, digital means have connected different roles and projects across the industry chain, enabling the supply side to link and reconfigure service resources in a more flexible manner, thus facilitating product segmentation and differentiation.

“Technology is critical, but it is not everything.” Li Shuo, Co-founder and COO of insgeek, believes that while adhering to the fundamental principles of insurance, one must also be prepared for a long-term commitment.

Li Shuo cited group insurance as an example, noting that the sector suffers from low levels of digitalization and urgently requires technological solutions to enhance efficiency. “From the perspective of fundamental insurance principles, group insurance pools a large number of individuals with varying health statuses—some require medication while others do not, and usage levels differ significantly among members—thereby fully embodying the law of large numbers. The overall aging of society has led to an ‘aging’ workforce within enterprises, prompting companies to place greater emphasis on employee health; consequently, the group insurance market is experiencing sustained long-term growth. However, integrating data across insurance companies, healthcare institutions, and enterprises is not something that can be achieved overnight.”

Secondly, transformation will occur following the integration of medical and health services. It is foreseeable that insurance companies will gradually evolve from single-purpose risk protection providers into comprehensive service providers offering a diverse range of services, including prevention, medical care, rehabilitation, and health management.

Zhang Qingfeng speculates that the development of health insurance will inevitably undergo such a process: in the early stage, it assumes the function of pooling payments; in the long term, the direction is “insurance as a service,” where insurance coverage also entails providing services required by customers. Therefore, if insurance is to cover both payments and the provision of pharmaceutical and medical services, integration is imperative. “Similar to pension insurance, which initially provided pension payments, the next step is to integrate elderly care communities and home-based elderly care services.”

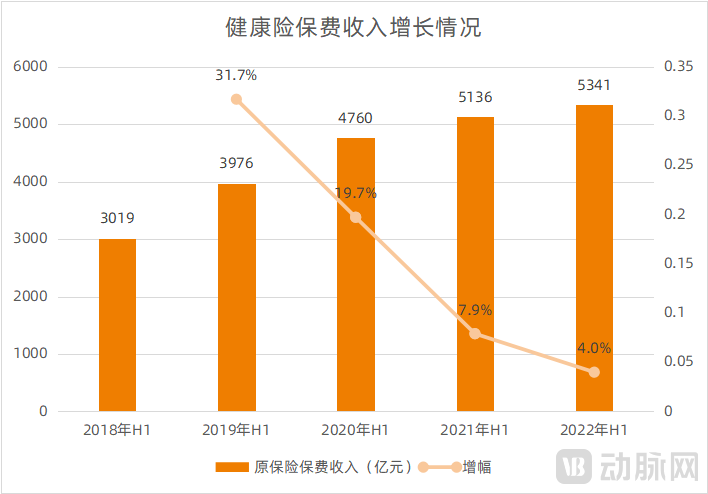

According to statistics from the China Banking and Insurance Regulatory Commission (CBIRC), premium income for health insurance reached RMB 534.1 billion in the first half of 2022, a year-on-year increase of 4%. This represents a slowdown in growth compared to the 19.7% and 7.9% increases recorded during the same periods in 2020 and 2021, respectively.

Health Insurance Premium Growth in Recent Years, Data Source: China Banking and Insurance Regulatory Commission

In accordance with the “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector” issued by 13 departments, including the China Banking and Insurance Regulatory Commission, efforts will be made to expand the supply of commercial health insurance, with the goal of having the market size of commercial health insurance exceed RMB 2 trillion by 2025.

To achieve the established goals, the market needs to further accelerate its growth in the coming years. Whether it is tapping into new growth points such as non-standard risk individuals, or leveraging technology and fostering synergy among pharmaceuticals, insurance, and healthcare services, these factors will serve as key drivers for market acceleration.

“Innovation should be encouraged, and integration remains a major trend.” Wang Yanping believes that under such circumstances, enterprises need to pursue more refined and specialized operations.