Over RMB 9 Billion Invested in Digital Therapeutics: How Top-Tier Investors Are Placing Their Bets

YuanBio Venture Capital

Venture Capital Institution

MARATHON VENTURE PARTNERS

Early-stage venture capital institution

Long Hill Capital

Venture Capital Institution

Judging whether an industry has prospects, the trend of the capital market is undoubtedly an important indicator. It is precisely for this reason that the recent boom in digital therapeutics serves as excellent evidence. Although this nascent industry still faces many challenges to be addressed, it has indeed taken off from the perspective of the capital market.

However, digital therapeutics encompasses many subfields, each with potentially different prospects. How do investors view this? VCBeat (WeChat ID: VCBeat) has compiled an overview.

According to VCBeat data,From 2017 to July 31, 2022, there were a total of 127 financing and investment events in the digital therapeutics sector in China's primary market., distributed among 63 companies.

Regarding total financing amounts, in addition to cases where specific figures were disclosed, many financing events described the amounts only in general terms such as “tens of millions,” “millions,” or “hundreds of millions.” For consistency, we calculated these as RMB 10 million, RMB 1 million, and RMB 100 million, respectively.

Furthermore, 34 financing events were excluded from our calculations as their specific amounts were not disclosed. However, given that these events accounted for one-third of all financing activities, the total capital involved is nonetheless substantial.

Using this conservative calculation method, digital therapeutics have raised a total of RMB 5.7888 billion and USD 492 million in financing from 2017 to the present.Combined, the total financing amount reached RMB 9.0852 billion.. In addition, the median financing amount for these 93 transactions was RMB 30 million.

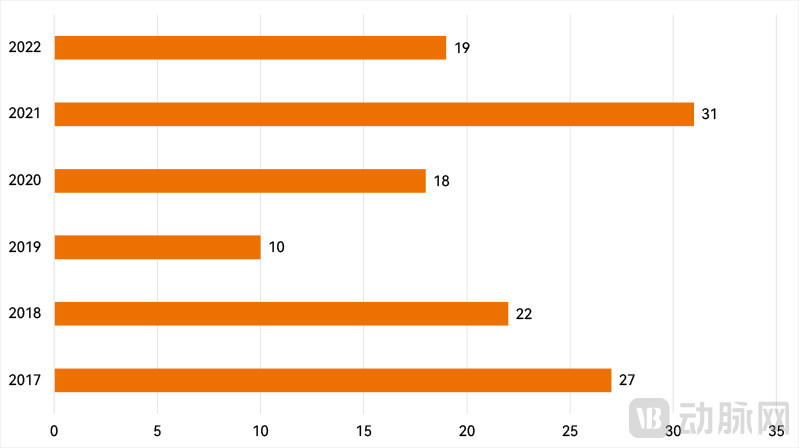

Distribution of Investment and Financing Events by Time

Based on the temporal distribution of these investment and financing events,2021 and 2017 ranked in the top two, with 31 and 27 investment and financing events, respectivelyThis aligns closely with key milestones in the development of digital therapeutics: In 2017, Pear Therapeutics’ prescription digital therapeutic received FDA approval, attracting widespread global attention. 2021 marked a year of significant heightened interest in digital therapeutics, regarded as the “Year One” of digital therapeutics in China.

However, several capital representatives who are relatively active in the field of digital therapeutics have candidly admitted that their early investments were not specifically targeted at digital therapeutics, but were more akin to “unintentional actions leading to favorable outcomes.” Although investors had heard of digital therapeutics at the time, their understanding and perception of the sector were rather superficial. Digital therapeutics only began to attract significant attention due to the pandemic, prompting investors to take notice of media coverage and regulatory approval information for certain products, and to make corresponding strategic moves.

Although 2018 temporarily ranked third with 22 financing and investment events, it was only three more than in 2022.Given that nearly half of 2022 remains, it should not be difficult for the full-year investment and financing levels in 2022 to surpass those of 2018.。

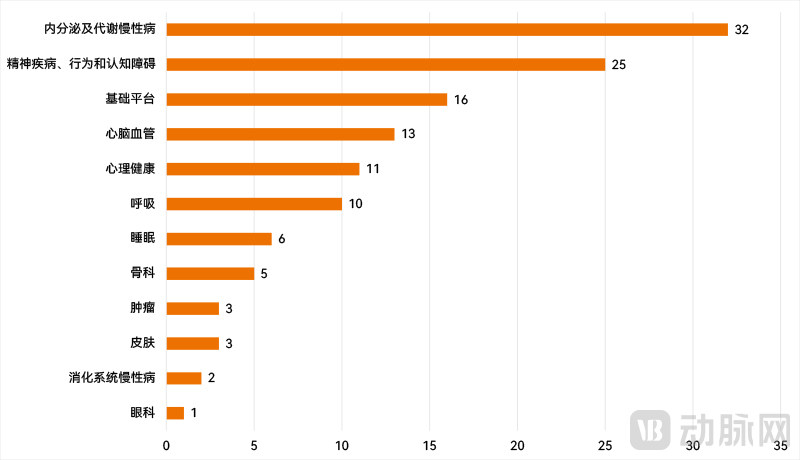

Distribution of Core Business Segments in Investment and Financing Events

In terms of the core businesses of these financed companies,The top three areas of greatest interest are endocrine and metabolic chronic diseases, mental illnesses, behavioral and cognitive disorders, and digital therapeutics platform services.。

Distribution of Investment and Financing Events by Core Business and Time

Chronic endocrine and metabolic diseases, including diabetes and kidney disease, have always been a major category for digital therapeutics. It is not surprising that the period from 2017 to 2018 marked a peak in financing for companies in this digital therapeutics segment, particularly in the aftermath of the intense “Hundred Glucose Wars.” During this two-year span, capital was deployed 16 times in this field, accounting for nearly one-third of the total 49 financing deals recorded over those years.

2020–2021 witnessed another investment peak in this sector. However, the majority of investments during this period were mid-to-late-stage rounds for companies that had already emerged as leaders during the previous investment surge. Notably, beyond diabetes, capital attention expanded to other chronic diseases; for instance, digital therapeutics companies focused on chronic kidney disease completed their early-stage financing during this time.

Mental disorders, behavioral conditions, and cognitive impairments, which rank second in prevalence, represent another major hotspot for digital therapeutics. Pharmacological treatments for these conditions often yield suboptimal results or are entirely unavailable, prompting the industry to look toward digital therapeutics for improved therapeutic outcomes. Notably, this sector has attracted significant capital attention since 2021. In just over a year and a half from 2021 to the present, there have been 13 investment deals in this field, surpassing the total number of financing rounds (12) recorded over the preceding four years.

However, the vast majority of the 25 financing rounds in this sector were early-stage, reflecting its current status as an area still awaiting further development.

As an emerging sector, digital therapeutics still has many areas in China that urgently need improvement, such as clinical services and channel promotion. Recognizing the immense potential of this field, many platform-based enterprises, especially internet healthcare companies, have begun to pivot toward providing platform services for digital therapeutics. From 2017 to the present, there have been 16 financing and investment deals in the digital therapeutics platform service category, ranking third among business classifications.

Furthermore, current digital therapeutics specializing in mental health are inherently linked to psychiatric disorders, as well as behavioral and cognitive impairments. It is not unlikely that they will evolve into treatments specifically targeting psychiatric, behavioral, and cognitive disorders, or sleep-related conditions. Statistically, there have been 11 financing rounds in the mental health sector, a considerable number.

Our statistical analysis also reveals that certain emerging categories of digital therapeutics have gradually attracted significant capital attention over the past two years. For instance, digital therapeutics in orthopedics, ophthalmology, dermatology, and oncology only began to garner attention and secure investment after 2020. This indicates that, as technology matures and industry understanding of digital therapeutics deepens, a broader range of diseases is increasingly being addressed through these solutions. It is foreseeable that more types of digital therapeutics will gradually come into view in the future.

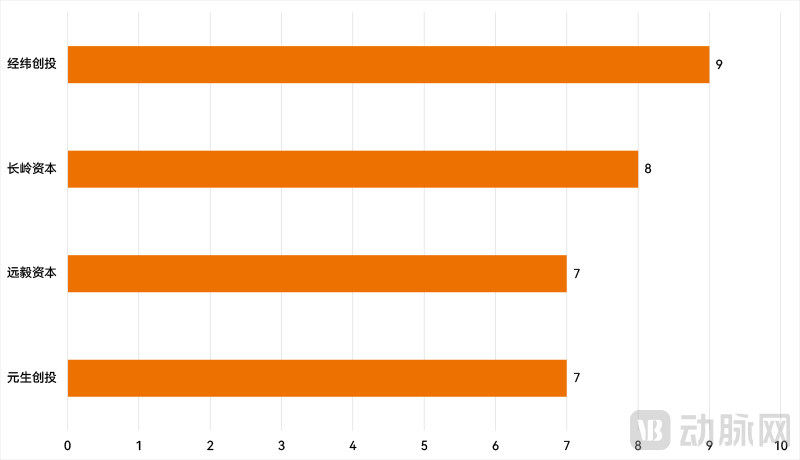

Top 3 Most Active Investors in Financing Deals

Statistically, a total of 176 institutions have invested in digital therapeutics companies, with each company attracting interest from nearly three investors on average, highlighting the sector’s strong momentum. Among these,Matrix Partners China, Long Hill Capital, YuanBio Venture Capital, and MARATHON VENTURE PARTNERS have demonstrated outstanding performance in investments within the digital therapeutics sector.。

From a financing and investment statistics perspective, digital therapeutics for chronic disease management and mental health are clearly popular. However, this may not fully reflect investors’ true intentions—some well-known firms have stated in communications with VCBeat that their investments are made from the standpoint of digital health rather than digital therapeutics. Although the underlying logic is similar, such overlaps are indeed unintentional. Therefore, we also engaged in discussions with several investors who are active in this field.

Song Yiran, Managing Director of MARATHON VENTURE PARTNERSHaving clearly defined its strategic direction in digital therapeutics, MARATHON VENTURE PARTNERS has largely structured its investments around two core logics:

First, disease types must be carefully selected, taking into account factors such as the overall incidence of the disease and its derivable market size, the existence of consensus-based clinical treatment pathways, and quantitative assessment methods. Priority should be given to disease types that have clear pain points throughout the entire treatment process and where digital and intelligent technologies can achieve significant efficiency improvements.

Secondly, she believes that the timing for market entry needs to be clearly defined. “For instance, the centralized procurement of coronary stents has significantly reshaped the value landscape of the cardiovascular industry, creating a favorable window for the development of digital therapeutics in this field. Alternatively, as the diagnosis and treatment models for immune-mediated skin diseases enter a phase of rapid growth driven by the launch of numerous biologics, digital therapeutics focused on efficacy assessment for these conditions have also become a key area of our focus,” explained Song Yiran.

Adhering to these investment logics and combining them with the actual conditions of China’s healthcare industry, MARATHON VENTURE PARTNERS has gradually concentrated its investments in two directions: first, disease management and digital therapeutics for chronic diseases, helping doctors and patients objectively understand treatment and management methods, monitor disease progression, and clarify clinical value outputs at different stages; second, neurological and neuropsychiatric disorders targeting specific indications, improving treatment outcomes through evidence-based physical therapies or behavioral interventions.

Long Hill Capital’s investment strategy in digital therapeutics shares similar underlying logic, albeit with subtle differences in its choice of entry points.Jiang Xiaodong, Managing Partner of Long Hill CapitalLong Hill Capital stated that it has been seeking standardized and accessible means to achieve health management and intervention, which is why digital therapeutics have come into its focus.

The broad field of mental and psychological health was the initial entry point chosen by Long Hill Capital, encompassing conditions such as cognitive disorders. Traditional therapies for these conditions have shown limited efficacy. Digital therapeutics enable long-term disease management and continuous intervention, thereby slowing disease progression and ensuring sustained benefits for patients.

After making initial progress in its investments and gaining valuable experience, Long Hill Capital began to expand its investment focus in digital therapeutics, gradually shifting from areas where traditional drugs or therapies had failed toward long-term chronic diseases, such as chronic kidney disease. However, the core logic remains unchanged: it continues to follow the approach of benefiting patients by slowing disease progression through effective disease management.

“If left unmanaged, chronic kidney disease will eventually progress to uremia, necessitating long-term dialysis. This is not only extremely painful for patients and their families but also imposes a significant financial burden. If a large number of patients prematurely reach this stage, it would place an enormous strain on the entire healthcare system. Alzheimer’s disease is quite similar; essentially, digital therapeutics are used to prevent and manage chronic diseases, thereby slowing disease progression,” added Jiang Xiaodong.

In addition, some capital follows the logic of vertical specialty layout—Liu Xiao, Executive Director of YuanBio Venture CapitalIn discussions with VCBeat, it was stated that its strategy in the digital therapeutics field follows a vertical specialty-oriented approach. It has prioritized investments in digital therapeutics companies focused on brain science. This is because digital therapeutic products for psychiatric and neurological disorders offer significant clinical value in both treatment and diagnosis, presenting substantial growth potential.

In terms of its entity form, digital therapeutics is a type of software. Upon obtaining medical device regulatory approval, it becomes part of Software as a Medical Device (SaMD). This falls within the realm of computer software development; whether considering underlying logic, technical processes, or technological pathways, the requirements for developing conventional software and SaMD are essentially identical.

Precisely for this reason, as digital therapeutics have garnered increasing attention, many cross-industry enterprises—such as those in the internet and IT/telecommunications sectors—have begun exploring opportunities to enter the healthcare field through digital therapeutics.

This is not uncommon—the core team of Happify Health, a pioneer in digital therapeutics, was in fact the development team behind Spider Solitaire, the classic game bundled with Windows. China’s gaming industry has also begun to enter the digital therapeutics sector and has secured medical device approvals.

Investors generally believe that this trend may not be a bad thing for the early-stage industry, but it is essential to focus on the essence of healthcare—prioritizing “therapies” over “digital.”

Drawing on his personal experience, Liu Xiao candidly acknowledged that many companies previously lacked a sufficient understanding of the characteristics of the healthcare industry, resulting in immature products and business models. However, he also noted that with the passage of time, the overall situation in 2022 showed significant improvement compared to 2021.

He also offered his advice from an investor’s perspective to the numerous digital therapeutics startups.

"First, it is necessary to select disease indications, assessing whether there is sufficient market size and significant commercialization potential. At the same time, it is essential to clarify the positioning within the healthcare system and the possible business models. 'Pursuing a direct-to-consumer (2C) approach in isolation is very difficult. The key question is whether to collaborate with physicians, pharmaceutical companies, or medical device manufacturers. Defining the company's position within the entire ecosystem is critical,' he stated."

Secondly, certain entry barriers must be established. Digital therapeutics must demonstrate definitive clinical value, which requires companies to conduct corresponding clinical trials or real-world studies. Furthermore, they must address significant clinical pain points sufficiently to motivate physicians to recommend them to patients.

“Some Class II medical devices appear to be approvable without clinical trials, but we place significant emphasis on the presence of clinical evidence and actively encourage our portfolio companies to conduct clinical studies. This serves as a key differentiator, distinguishing genuine science from pseudoscience and indicating whether a product has meaningful barriers to entry. Of course, the presence or absence of clinical trial data is not the sole indicator of clinical value. Some digital therapeutics may lack formal clinical trials, yet their underlying principles have been extensively validated in real-world settings. For instance, Cognitive Behavioral Therapy (CBT) is grounded in principles with a long history of proven efficacy; therefore, we recognize the effectiveness of digital therapeutic products based on such established foundations.”

Finally, the feasibility of the business model remains a key consideration. Liu Xiao believes that although various business models exist, physicians currently remain the primary customers for digital therapeutics. While physicians do not directly pay for these solutions, leveraging the inherent trust between physicians and patients enables the most efficient promotion. Meanwhile, collaboration with physicians is also essential during the product development and clinical stages of digital therapeutics.

“It is difficult for startups to allocate substantial funds for marketing campaigns like large enterprises do, which is not very feasible in the short term. While direct patient services can be offered after scaling up, leveraging physicians to serve patients may be a more efficient approach in the early stages,” Liu Xiao added.

Song Yiran stated that digital therapeutics represent the digitization of professional medical services: “This necessitates respect for the attributes and characteristics of professional medical services. Such services are highly individualized. As a digital abstraction of professional medical services, digital therapeutics must be grounded in clinical practice. This requires the team to have a profound understanding of clinical practice, as well as in-depth knowledge of the industrial structure, academic distinctiveness, and regional characteristics of specific disease areas, thereby abstracting products and systems from the process of serving physicians and patients.”

“The team behind digital therapeutics should also possess comprehensive capabilities to serve the entire industry chain, including business collaboration and physician-patient engagement skills. This enables them to coordinate with multiple stakeholders across the value chain to serve patients, create incremental value, and translate that value into commercial outcomes,” she added.

Jiang Xiaodong believes that some startups have a skewed understanding of digital therapeutics, focusing more on digital tools. Their products resemble tools for physicians to manage patients rather than demonstrating therapeutic efficacy. Therefore, although also delivered in software form, these products differ from the core essence of digital therapeutics.

“Digital therapeutics do not follow the same logic as internet products; one cannot simply release a product and rely on rapid iteration to complete the process. I believe this approach is unacceptable—this is not merely management software, but a serious therapeutic intervention for disease treatment, which must deliver effective and efficient outcomes for the disease and its course.”

Based on this, Jiang Xiaodong believes that digital therapeutics need to provide evidence of their efficacy: one is based on traditional clinical trials; the other is based on the results of real-world studies. The former is essentially a controlled small-scale trial, while the latter goes further, generated by a large number of customers during use and management.

“Both clinical trials and real-world studies require long-term accumulation; they are not as easy as one might imagine. Several companies in our portfolio have already amassed substantial real-world usage data, with their products being utilized in hundreds of hospitals or by tens of thousands of users. This data, in turn, feeds back into the iterative development of their products, enabling continuous refinement and improvement.”

“Digital therapeutics is not about spinning a narrative or coining a concept, nor is it synonymous with digital health or internet-based healthcare simply because the terms look similar. Its core lies in the therapy itself; your product must demonstrate genuine efficacy,” he summarized.

In addition to the continuous influx of startups into the digital therapeutics sector, a growing number of investors are also closely watching this space. However, as a major area of innovation, digital therapeutics is clearly not yet mature, with significant room for improvement in areas such as regulation, clinical efficacy, and reimbursement. During discussions, Liu Xiao noted that the rapid influx of capital into digital therapeutics in the short term has already led to signs of market bubble.

“This bubble primarily affects valuations. I personally believe that the current valuations of some digital therapeutics companies are excessively high. Obtaining regulatory approval is indeed a milestone that can support a company’s valuation to a certain extent. However, beyond this level, investors will place greater emphasis on the company’s ability to achieve commercial implementation. Without this capability, obtaining additional approvals—whether five or ten—will not provide significant added value. Some of the faster-growing companies in the industry have reached the stage where they must demonstrate their commercialization capabilities; the next phase will test the team’s competencies in other dimensions,” he added.

He believes that digital therapeutics are still in a very early stage. Although the industry appears vibrant and there have been some promising commercialization attempts, it is premature to claim commercial success. With regulatory approvals having been granted only recently, there remains significant room for improvement in key metrics such as revenue scale and market penetration.

Therefore, Liu Xiao believes that digital therapeutics need to return to the essence of healthcare, adhere to clear regulatory boundaries, and first demonstrate clinical value through clinical trials or real-world studies. Only on this basis can market potential be discussed and commercial value proven. These two aspects still warrant greater attention from the industry.

Song Yiran also raised a similar point regarding the current large-scale business model in the early stages of market validation and conversion: “Both hospitals and pharmaceutical and medical device companies have well-established and scientific decision-making chains. All stakeholders involved in the decision-making process need to recognize, understand, and believe in the value of digital doctor-patient services, which is a process that requires time to accumulate.”

From a regulatory perspective, current regulations already meet present needs and can evolve further as the industry develops. In addition, she advocates that the industry should avoid excessive hype around concepts and instead focus on pragmatically creating value and outcomes in medical practice that are mutually recognized by both physicians and patients.

Jiang Xiaodong stated that digital therapeutics still face challenges in reimbursement, which can only be addressed by providing evidence of their efficacy and efficiency. If digital therapeutics can help slow disease progression in patients with chronic conditions, and health economics studies demonstrate the resulting cost savings for medical insurance programs, payers will naturally accept covering these treatments. It is even possible that they could be included in volume-based procurement programs in the future.

“I firmly believe that as long as digital therapeutics demonstrate superior efficacy and efficiency, a viable business model is inevitable,” Jiang Xiaodong added.

Meanwhile, under the overarching policy of cost containment in medical insurance, greater emphasis will be placed on healthcare efficiency. Digital therapeutics, with their inherent advantages in this area, are poised to receive significant momentum, provided they truly address clinical pain points and demonstrate clear advantages in both efficiency and efficacy through evidence.

“I believe we have an opportunity to reshape the value chain of the healthcare system. The direct impetus comes from cost-containment policies implemented by medical insurance programs, such as the ‘Three-Year Action Plan for DRG/DIP,’ which will inevitably change physicians’ behavioral patterns. This will significantly accelerate the adoption of digital technologies, including digital therapeutics, in the healthcare sector.”

“I believe the greatest potential for digital therapeutics companies lies in the data accumulated throughout their business operations. To date, data sharing in the healthcare industry has been hindered by prohibitively high costs and significant implementation challenges. One of the key byproducts of the commercialization process for digital therapeutics firms is real-time, online, patient-centric clinical data, whose potential value is immeasurable.”

“In fact, we have already seen many doctors proactively embracing digital technologies, including digital therapeutics. Once this trend takes hold, it will be irreversible and accelerate over time,” Liu Xiao said, expressing cautious optimism about the industry’s outlook.