How Did Teladoc, the Pioneer of Telehealth, Lose Over $60 Billion in Just Six Months?

Teladoc

Telemedicine Service Provider

As the pioneer of internet-based healthcare in the United States and globally, Teladoc, founded in 2002, was the first telemedicine platform in the U.S. After experiencing various ups and downs, it went public on the New York Stock Exchange in 2015, becoming the first publicly listed telemedicine company and earning its reputation as a “living fossil” of digital health. As a benchmark for internet-based healthcare in the U.S., Teladoc has consistently led industry trends and serves as a key reference point for many digital health companies in China.

However, since the beginning of 2022, Teladoc’s performance has been deeply disappointing: its Q2 financial report showed a loss of $3 billion for the quarter, adding to the $6.67 billion loss in Q1,Teladoc has incurred a massive loss of nearly $10 billion in half a year, equivalent to over RMB 60 billion., its market capitalization has evaporated by nearly 90% from last year’s historical high。

This figure was highly unexpected. What exactly went wrong with Teladoc, which has always performed well? More importantly, what pitfalls did it actually fall into?

Teladoc, regarded as the pioneer of internet healthcare, has demonstrated strong performance since its initial public offering, with its business maintaining a trajectory of rapid growth. The company sustained exceptionally high growth rates from 2015 to 2018.

Teladoc’s Annual Revenue and Growth Rates in the Pre-Pandemic Era in the United States

Rapid business growth, coupled with optimism about the prospects of internet healthcare, has strongly supported Teladoc’s stock price. In 2016, its share price was still in the $10–$20 range. By the second half of 2017, it had stabilized above $30. In 2018, the stock price further climbed into the $50–$70 range.

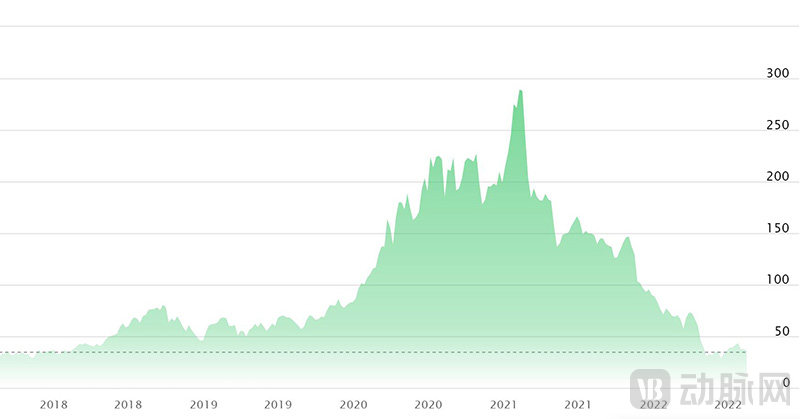

The COVID-19 outbreak in early 2020 was a typical “black swan” event. However, it precisely triggered a surge in demand for internet-based healthcare services in the United States, making Teladoc highly favored by a large number of investors and sending its stock price soaring along a remarkably steep trajectory.

In early 2020, Teladoc’s stock price was hovering around $80. By mid-year, it had surged to $190. In February 2021, Teladoc’s share price reached $294.54, marking its all-time high since going public.

Teladoc’s Stock Price Trend Over the Past Five Years (Screenshot from the Nasdaq Official Website)

It is no exaggeration to describe Teladoc at that time as “white-hot” and “extremely popular.”

Starting from the first quarter of 2020, Teladoc’s revenue and user base experienced a surge. In the fourth quarter of 2019, Teladoc’s total revenue, number of domestic members, and total number of domestic member visits were $156.5 million, 36.7 million, and 980,000, respectively. This represented relatively normal growth compared with previous quarters.

In the first quarter of 2020, the three indicators reached $180.8 million, 43 million (people), and 1.51 million (visits), respectively. In the second quarter, these figures surged further to $241 million, 51.5 million (people), and 2.11 million (visits). The magnitude of this growth is evident.

Comparison of Teladoc’s Quarterly Key Metrics, 2019–2020 (in millions of USD/millions of people/millions of visits)

In 2020, Teladoc generated $1.094 billion in revenue, a 97.7% year-over-year increase; in 2021, it grew another 85.8% from the 2020 level, reaching $2.033 billion in revenue.。

In August 2020, Teladoc acquired Livongo, which had gone public just one year prior. Founded in 2008, this star enterprise in diabetes management launched its IPO in 2019. Its core business leverages digital technologies and smart devices to help patients manage their diabetes.

Under the terms of the transaction, each share of Livongo held by Livongo shareholders will receive 0.592 shares of Teladoc and $11.33 in cash,Based on this calculation, Livongo’s valuation reached $18.5 billion. According to estimates at the time by financial services firm Piper Sandler, the merged entity was valued at as much as $38 billion.。

Following its acquisition of Livongo, Teladoc’s services came to cover nearly every segment of the telehealth industry. At that time, Teladoc was in a strong position, appearing unstoppable in its forward momentum.

In April 2022, Teladoc announced its first-quarter financial results, reporting a staggering net loss of $6.67 billion. The announcement sent shockwaves through the market, triggering a rush of investors to divest. Its stock price plummeted 40%, diving from $55.99 to $33.51, and its market capitalization was halved. Many investors dubbed this event Teladoc’s “darkest hour” in the seven years since its IPO.

Infuriated by substantial losses, investors even filed a class-action lawsuit against Teladoc. In this lawsuit, investors accused Teladoc of failing to disclose “how increased competition and other factors negatively impacted Teladoc’s BetterHelp and chronic care businesses” and “how the growth of these businesses was not as sustainable as the defendants had led investors to believe.” Investors argued that these misrepresentations resulted in unrealistic financial projections for Teladoc’s current fiscal year.

The lawsuit alleges that Teladoc had projected full-year 2022 revenue of $2.55–$2.65 billion and adjusted earnings of $330–$355 million prior to its February earnings release. However, its first-quarter earnings report in April showed Q1 revenue of $565.4 million, which, although higher than the same period last year, fell short of expectations by $3.23 million. Consequently, the company lowered its full-year 2022 revenue guidance to $2.4–$2.5 billion.

A Teladoc spokesperson responded in an emailed statement: “The lawsuit is devoid of any factual basis, but unfortunately, such frivolous litigation has become all too common among publicly traded companies today.”

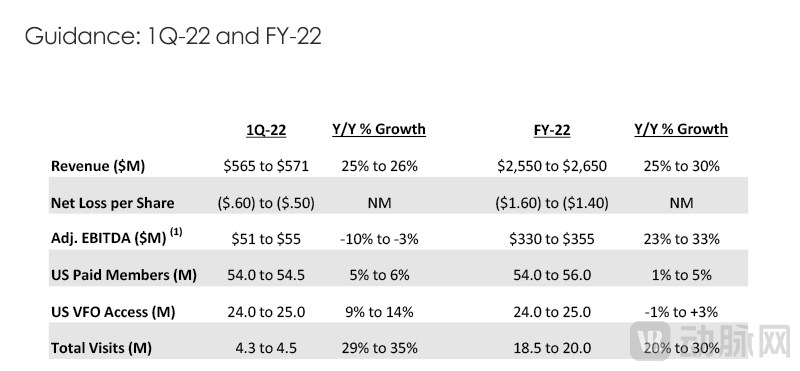

Investors’ anger is not without justification. In the fourth quarter of 2021, Teladoc issued rather optimistic guidance for the first quarter and full year of 2022, projecting a maximum loss of only $0.60 per share for Q1 2022. However, the actual result was a loss of $41.58 per share. The sharp plunge in its stock price on that day clearly indicated that the market had not anticipated such an outcome.

Teladoc’s Q4 2021 Forecast for 2022 Performance (Screenshot from Teladoc’s Quarterly Earnings Preview)

Such an unexpected, massive loss is likely the primary driver of investor outrage and the subsequent class-action lawsuit. After all, objectively speaking, merely lowering revenue guidance is commonplace for companies, and a single-quarter miss of $3 million is hardly significant against a revenue base in the hundreds of millions.

What investors found even more unacceptable was that Teladoc’s earnings forecast specifically explained that although the loss per share was $41.58, $41.11 of this amount was attributable to “goodwill impairment.” After excluding this item, the adjusted loss per share was only $0.47. For investors facing an actual loss of nearly $42 per share, this explanation clearly did not reflect their reality.

However, these angry investors probably did not expect that the blows they would endure were far from over.

Teladoc reported a massive second-quarter loss of $3.1 billion in its July earnings release. As this was in line with market expectations, the announcement did not trigger a plunge in its stock price; however, the stock has still plummeted 88% from its highs last year.

The release of two financial reports has resulted in significant losses for many investors, including Cathie Wood, known as the “female Warren Buffett.” The star investor, nicknamed “Sister Wood,” has long been bullish on Teladoc.

In its latest quarterly report, Teladoc significantly lowered its outlook, projecting full-year 2022 revenue of $2.4–$2.5 billion, a maximum expected annual net loss per share of $62, and adjusted EBITDA of $240–$265 million. All these metrics represent downward revisions compared to the forecasts issued at the end of 2021.

Comparison of Teladoc’s Full-Year 2022 Performance Forecasts Issued in Q4 2021 and Q2 2022

The primary reason for Teladoc’s precipitous drop in performance was not insufficient revenue for the quarter. In fact, although revenue growth slowed significantly, quarterly revenue still increased by 18%, reaching $592 million.The primary cause of the substantial loss was still the goodwill impairment resulting from the acquisition of Livongo two years ago.。

Goodwill, as an asset of an enterprise, refers to the ability to generate returns above the normal profitability level (i.e., excess earnings) and represents the present value of future excess earnings expected to be realized by the enterprise. Specifically, it is manifested as the portion of the purchase price paid in a business combination that exceeds the fair value of the net assets of the acquired enterprise.

In simple terms, goodwill arises in business combinations. The portion of the purchase price paid by the acquirer that exceeds the fair value of the acquiree’s net assets—i.e., the acquisition premium—constitutes goodwill.

In the early days, goodwill was typically reduced gradually through amortization over multiple years. According to Opinion No. 16 issued by the Financial Accounting Standards Board (FASB) in 1970, goodwill arising from business combinations could be amortized over a period not exceeding 40 years, known as goodwill amortization.

This approach is akin to treating goodwill as a piece of equipment and depreciating it gradually over its useful life. However, both the amortization period and method are subject to arbitrariness and potential earnings manipulation, nor do they provide guidance on a company’s future profitability. This diminishes the usefulness of financial information.

Therefore, in 2001, the FASB issued SFAS No. 141, Business Combinations, and SFAS No. 142, Goodwill and Other Intangible Assets, which eliminated goodwill amortization and replaced it with goodwill impairment testing. In this context, goodwill impairment arises when an acquired entity is determined to be unable to deliver expected growth, indicating to some extent that the merger or acquisition has failed to achieve its anticipated outcomes.

AOL Time Warner is a famous counterexample of goodwill impairment. AOL and Time Warner merged in January 2000, with the newly formed company boasting a market capitalization of $350 billion, earning it the title “Merger of the Century.” However, in January 2002, AOL Time Warner announced a $54 billion goodwill impairment, setting a record for the largest quarterly loss in U.S. history. In 2003, AOL Time Warner’s losses soared to $98.7 billion, with its market value plummeting by nearly $100 billion.

Teladoc’s $18.5 billion acquisition of Livongo was valued at 30 times the latter’s projected 2021 revenue, drawing industry criticism at the time for its excessive premium. It is worth noting that although Livongo had just achieved its first quarterly profit, its market capitalization only surpassed $10 billion in July 2020.

By comparison, Siemens’ acquisition of Varian, the giant commanding over 50% of the global radiotherapy market share, cost only $16.4 billion during the same period. This illustrates the substantial price tag of Teladoc’s merger. Following the announcement, shares of Teladoc and Livongo fell by 19% and 11.4%, respectively.

Notably, at the end of Q2 2020, prior to the acquisition of Livongo, Teladoc’s goodwill stood at $1.69 billion. The acquisition of Livongo increased Teladoc’s goodwill to $14.58 billion. Currently,Teladoc has already recorded $9.63 billion in goodwill impairment, yet its financial statements still reflect nearly $3 billion in goodwill stemming from the Livongo acquisition. Further impairments would place significant pressure on Teladoc.。

If both companies could sustain high-speed growth as expected, this would not be a major issue. In fact, it would not result in any goodwill impairment at all. The crux of the matter is that the growth momentum of both enterprises has slowed down significantly.

Taking Teladoc as an example, membership fees constitute the primary component of its revenue. These users are primarily covered by B-side clients, such as employers or insurance companies, on behalf of their employees. The membership subscription includes a specified number of visits, with additional pay-per-visit charges applied for usage beyond this limit.

Whether members pay an additional per-visit fee or opt for pay-per-visit only, the costs are significantly higher than the membership fee. According to estimates, in 2020, the unit price for members’ additional per-visit payments ranged from approximately $50 to $60, while the pay-per-visit-only rate ranged from $60 to $70. In contrast, the membership fee was less than $20. Therefore, B-end clients typically adjust the number of memberships they purchase based on member activity levels.

For this reason, the revenue contributed per member is actually not high; prior to the fourth quarter of 2020, the average quarterly revenue contribution per member to Teladoc had remained around $3. The sustained high growth in recent years has primarily relied on the continuous expansion of its member base, which has been driven mainly by ongoing acquisitions.

However, the trend of rapid growth in Teladoc’s membership numbers stalled in the second quarter of 2020, with figures hovering around 51 million for an extended period. Given that the U.S. population is only slightly over 300 million and competition is intensifying, the cost of relying solely on acquisitions to increase membership will continue to rise.

Acquiring Livongo, a company specializing in chronic disease management for diabetes, can effectively increase the average revenue per member. Livongo adopts an integrated model combining hardware and software services; users who purchase a membership are required to simultaneously buy connected devices such as Livongo’s blood glucose meters, blood pressure monitors, or smart scales to monitor relevant health data. Subsequently, users can pay for consultations on a monthly subscription basis or on a per-visit fee-for-service basis.

In the U.S. health insurance system, employers purchase commercial insurance for their employees, typically covering 80% of the premium costs. The exact proportion depends on the company’s benefits plan. Employees with chronic conditions represent the largest share of insurers’ expenditures, as insurers must not only cover the costs of their ongoing treatment but also bear the high expenses associated with hospitalization if their conditions are poorly managed. Since insurers foot these bills, they need to implement disease management programs for employees with chronic conditions.

Insurance companies, confident that expenditures are reduced and controllable, will inevitably return a portion of the benefits to employers in some form; for employers, improved employee health can reduce absenteeism due to sick leave and other work disruptions. Therefore, when Livongo demonstrates its return on investment with solid evidence, both insurance companies and employers will be willing to recommend Livongo’s services to their employees.

Thus, Livongo established a B2B2C business model: its clients are enterprises that purchase health insurance for their employees; insurers and pharmacy benefit managers (PBMs) serve as channel partners that help refer clients; while the corporate employees are the ultimate beneficiaries of Livongo’s innovative services.

Therefore, although Livongo had fewer than one million members, the revenue contributed per member was significantly higher than that of Teladoc. At that time, Livongo’s membership was also experiencing rapid growth, with a 74.4% year-over-year increase in the second quarter of 2021.

Meanwhile, Teladoc can leverage this opportunity to further expand the range of disease conditions covered, thereby providing members with more comprehensive services and even facilitating internal cross-utilization—for instance, Livongo’s diabetes management users may also have consultation needs for other health conditions. According to Teladoc’s estimates, an employer with 10,000 employees adopting a multi-product service portfolio would generate 4.1 times the revenue compared to offering single-disease services.

Based on the member revenue reported in Teladoc’s quarterly earnings releases since the acquisition,The inclusion of Livongo has indeed significantly increased membership revenue. The average revenue per member per quarter more than doubled from around $3 to reach the $7 level.。

Surprisingly, since the acquisition was completed, Livongo’s membership has reversed its previous trend of rapid growth, stagnating at around 700,000.

Not only Livongo, but Teladoc’s own growth has also slowed significantly, with revenue growth decelerating for the fifth consecutive quarter and key metrics such as member count and visit volume showing weak momentum. In fact, Teladoc is not alone in facing this challenge; its main competitors, Amwell and One Medical, are encountering similar issues.

According to Amwell’s Q2 2022 financial report, the company’s quarterly revenue reached $64.5 million, representing a modest 7% increase from the $60.2 million recorded in the same period last year. Of this total, subscription revenue amounted to $29.6 million, up 10% year-over-year, while visit-based revenue stood at $29.7 million, reflecting an 8% increase compared to the prior year.

This revenue level is even lower than that of Q1 2022, when the company reported revenues of $64.2 million, a 12% year-over-year increase; subscription revenue amounted to $28.7 million and visitation revenue to $30.7 million, representing year-over-year growth of 17% and 10.4%, respectively.

One Medical, recently acquired by Amazon, fared slightly better, reporting revenue of $255.8 million and 790,000 members in the second quarter of 2022, representing year-over-year increases of 112% and 27%, respectively. However, a comparison with the first quarter reveals similarly sluggish growth: One Medical generated $254.1 million in revenue and had 767,000 members in Q1.

Meanwhile, One Medical’s net loss widened from $90.9 million in the first quarter to $93.8 million.

Clearly, the star players in the U.S. internet healthcare sector are having a tough time.Part of the reason is that the relaxation of COVID-19 control measures in the United States has led to a weakening demand for telemedicine compared to before. This has caused a slowdown in the growth rate of demand for internet-based healthcare services.。

However, in the long term, the utilization rate of internet-based healthcare in the United States has indeed shown significant growth compared to pre-pandemic levels.According to Fair Health’s monthly statistics, in May 2022, telemedicine visits accounted for 5.4% of all reimbursed medical visits in the United States, representing a 10% increase from 4.9% in April. In contrast, this proportion was a negligible 0.38% in February 2020, prior to the pandemic.

Among these, consultations for mental health disorders have dominated the market share for several months. In May’s statistics, such consultations accounted for as high as 62.8% of all internet-based medical services.

Deloitte’s findings from its 2022 Connectivity and Mobile Trends Survey were more optimistic, with 49% of respondents indicating that they had used online healthcare services at least once in the past year. When broken down by age, 59% of Generation Z respondents reported having used online healthcare services at least once.

Secondly,Competition in the U.S. telemedicine market is also intensifying.. In late July, Amazon announced its $3.9 billion acquisition of One Medical, marking the third most expensive acquisition in Amazon’s history. CEO Andy Jassy also stated that Amazon would further increase its investment in the healthcare sector.

In addition to the entry of industry giants, there are alsoNumerous small service providers specializing in specific disease areas are also emerging in large numbers.. As a benchmark enterprise in internet healthcare, the competitive pressure faced by Teladoc is no longer comparable to what it was during its period of rapid growth.

Acquisitions are undoubtedly one of the direct factors that have led Teladoc into crisis. For other internet healthcare companies, the lessons learned from Teladoc’s acquisition strategy are equally worthy of reference. In Teladoc’s past successes, aggressive acquisitions were a key driver. Compared with slow organic growth, acquisitions can indeed rapidly expand a company’s scale. Scale is precisely one of the most critical elements in Teladoc’s business model.

However, mergers and acquisitions (M&A) are a double-edged sword; if mishandled, they can severely harm the acquiring company. Just as excessive food intake over a short period can cause indigestion in the human body, mega-mergers can similarly lead to corporate “indigestion.”

The acquisition of Livongo allows the two star players in internet healthcare to complement each other’s strengths and weaknesses, forming a new flagship and pioneering a novel consumer-centric model of internet healthcare. Frankly speaking, there is nothing fundamentally wrong with Teladoc’s long-term strategy. The key issue lies inTeladoc’s acquisition was poorly timed, with the transaction value significantly overvalued, and the anticipated “1+1>2” synergy being merely an overly optimistic projection.。

Interestingly,Livongo’s Core Team Resigned at Lightning Speed Following the Acquisition, including CEO Zane Burke, President Jennifer Schneider, CFO Lee Shapiro, and Senior Vice President of Business Development Steve Schwartz. Additionally, Livongo founder and chairman Glen Tullman soon left the company to embark on a new entrepreneurial venture.

Given the emergence of an ultra-high premium and the exodus of the acquired company’s executive team, it is questionable whether this acquisition involved any transfer of benefits. What is certain, however, is that those who once led Livongo to successCorporate culture and the team have been completely eroded. This is undoubtedly a major taboo in acquisitions.。

The stagnation in membership numbers at several benchmark companies highlightsThe B2B Channels Driving Rapid Growth in U.S. Internet Healthcare Are Peaking. On the one hand,Large, well-resourced employers and insurance companies are beginning to build their own telemedicine services.. Amazon previously launched Amazon Care, a service exclusively for its employees, later expanded it nationwide across the United States, and ultimately entered the market directly through acquisition. On the other hand,Due to the limitations of internet-based healthcare, there has been a declining trend in existing members’ willingness to utilize these services.。

Teladoc has also recognized this issue. On one hand, it seeks to attract users by acquiring specialized disease management providers such as Livongo; on the other hand, it is expanding its direct-to-consumer (DTC) channels. For instance, in February, Teladoc partnered with Amazon to leverage Alexa-enabled smart speakers in providing customers with 24/7 non-emergency general medical services.

Furthermore, Teladoc has intensified its promotion of BetterHelp, its mental health services brand. This service addresses a critical social need for consumers who lack mental health insurance or are unable to find a therapist within their health plan’s network.

However, this has also led to a surge in marketing costs. Its advertising and marketing expenses reached $187 million in the first quarter of 2022, representing a significant year-on-year increase of 49%. Advertising and marketing expenses remained high in the second quarter, reaching $165 million, a 69% year-on-year increase, and accounting for as much as 27.8% of its revenue for that quarter.

Nevertheless, although Teladoc’s growth rate has slowed, it continues to expand. The team that once created the myth of high-speed growth remains in place, and the company still holds $880 million in cash and cash equivalents. Furthermore, investors remain convinced that telemedicine offers substantial room for future growth. “Cathie Wood,” who has suffered significant losses, continues to accumulate shares at lower price levels. Currently, her ARK ETF holds nearly 12% of Teladoc’s outstanding shares, making it the company’s largest shareholder.

This star investor stated in an interview, “We want the companies we hold to invest aggressively; we are not seeking profits at this stage. We encourage them to invest actively because we are entering many winner-take-all markets.”

She cited Amazon as a source of encouragement for Teladoc. Amazon’s initial public offering (IPO) price was approximately $18, which subsequently surged to around $180. Around 2001, Amazon lost roughly 90% of its market capitalization, falling back to its original level, which essentially meant that its cost of capital increased tenfold. Today, Amazon’s stock price has once again returned to those earlier levels.

However, the excessive fragmentation of equity leading to a loss of control is likely bad news for Teladoc. After all, the ultimate goal of capital remains profit generation. “Cathie Wood” and her cohort, having incurred losses, will ultimately seek opportunities to recoup their investments, which will lead toTeladoc’s Long-Term Strategy Carries Uncertainty。

Ali Parsa, CEO of the prominent digital health company Babylon Health, also believes that Teladoc can learn from Amazon’s resurgence two decades ago—when Amazon focused on areas that differentiated it from competitors during its downturn, zeroing in on e-commerce. Today, Amazon has become a global e-commerce giant.

Teladoc can address competition by demonstrating value to payers through a focus on capabilities that differentiate it from competitors, such as providing users with better health prevention.Investing more heavily in technology is a prudent strategy, enabling service providers to remotely monitor patients’ health status, deliver personalized care recommendations, and differentiate themselves by intervening before health issues escalate into costly acute treatments. This is precisely the path Babylon Health has been pursuing.

In contrast,Although China’s internet healthcare sector differs significantly from that of the United States in terms of industry background and business models, it is by no means inferior to foreign counterparts in exploring the application of digital technologies.。

For instance, the recently released financial report of Ping An Good Doctor highlighted the increased adoption of digital operational technologies and extensive resource integration in its managed care services for corporate clients, incorporating digital tools such as blood pressure-monitoring smartwatches into its management processes. JD Health recently convened a Digital Intelligence Healthcare Conference themed “Integration of Digital and Physical Realms, Winning the Future with Intelligence.” Meanwhile, WeDoctor has been exploring innovations in AI-powered medical devices.

Meanwhile, domestic internet healthcare providers are increasingly exploring the integration of digital therapeutics to directly address diseases themselves, moving beyond the previously somewhat ineffective model of lightweight online consultations. This shift will significantly enhance their ability to tackle patients’ actual pain points, rather than merely serving as a tool for prescribing medications.

Given the current situation, the company renowned for its acquisitionsIt would not be surprising if Teladoc were to become an acquisition target in the future.After all, Teladoc, whose stock price is hovering near its trough, still maintains a vast network and strong brand recognition, while the industry holds immense potential for growth.

For example, Amazon was even a customer of internet healthcare services just a year ago. Yet in less than a year, Amazon progressed from building its own employee-focused service, Amazon Care, to rapidly acquiring One Medical to enter the market. As its competitor, Walmart has also acquired several smaller healthcare providers. Furthermore, there are many other major players that have quietly demonstrated strong interest in the healthcare sector.

As time goes on, after gaining experience through the operations of smaller service providers, these giants may well make a move on Teladoc—provided it has still not emerged from its predicament by then—thereby solidifying their leadership position in healthcare.

What does the future hold for this benchmark enterprise in global internet healthcare? We will continue to monitor developments closely and provide first-hand reporting.

References:

Bao Xicheng, Friends of Accounting, 2004, Issue 5: “Implications for Us from the FASB’s Standard on ‘Goodwill and Other Intangible Assets’”

Goodwill Impairment or Amortization? First, Understand the Context.

Ryan Furhmann,Investopedia.com:Writing Down Goodwill

Fair Health:Monthly Telehealth Regional Tracker

Katie Adams,Medcity.com:Teladoc can recover by looking at what Amazon did 20 years ago, Babylon Health CEO says

Latitude Health: “$6.6 Billion Goodwill Impairment: Examining the Ceiling of Digital Therapeutics Through Teladoc”

Michael Schroeder,Medcity.com:Teladoc, Amazon partnering to offer voice-activated virtual care

Deloitte:2022 Connectivity and Mobile Trends Survey

Eddie Pan,Investorplace.com:Cathie Wood keeps buying Teladoc (TDOC) stock. Here’s why

Taylor Carmichael,The Motley Fool:Are Walmart and Amazon a Threat to Teladoc?

Pharma Watch: “The $18.5 Billion Digital Health Merger of the Century”