Clinical Mass Spectrometry Hits Exponential Growth Inflection Point: MALDI-TOF Emerges as an Undervalued Treasure

How Hot Is China’s Clinical Mass Spectrometry Sector? Financing Data Offers the Most Intuitive Insight.

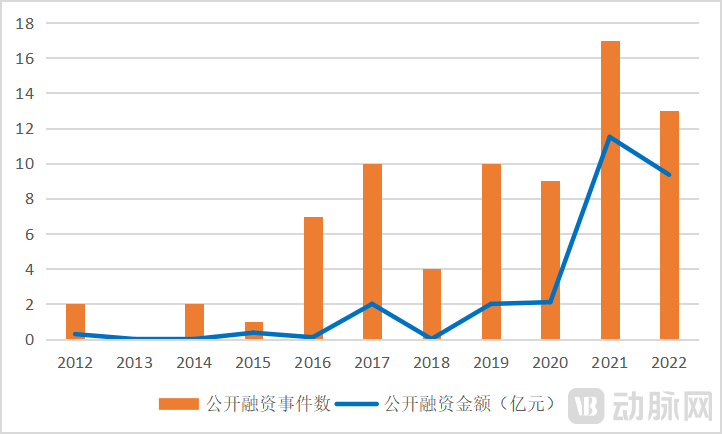

According to statistics from VCBeat, the clinical mass spectrometry industry has witnessed a total of 80 financing events, with cumulative funding exceeding RMB 2.7 billion; some companies have already advanced to Series D financing. In 2021, there were 17 financing deals, with annual funding surpassing RMB 1.15 billion—the highest level in the past decade. Prominent investment firms such as Hillhouse Capital, IDG Capital, Legend Capital, Sherpa Capital, and Matrix Partners China have made significant investments, demonstrating their confidence in this sector.

Particularly in 2022, clinical mass spectrometry has garnered even greater favor from the capital market. Since 2022, there have been a total of 13 financing rounds in the clinical mass spectrometry sector, with the total amount exceeding RMB 900 million. It is projected that both the number of financing deals and the total amount raised in clinical mass spectrometry will reach record highs in 2022.

Historical Financing Trends in Clinical Mass Spectrometry

Clinical mass spectrometry has reached an inflection point of exponential growth, with companies across the upstream and downstream supply chains accelerating their development. Amidst this intense market fervor, how can stakeholders calmly identify the next growth opportunity? VCBeat believes that future opportunities lie in areas such as MALDI-TOF, localization of instruments, and improvements in operational efficiency. We have conducted an analysis from the perspectives of instruments, technology platforms, and operational efficiency.

Clinical mass spectrometry does not refer to a single technical platform, but rather comprises multiple platforms, including tandem mass spectrometry (MS/MS), MALDI-TOF, and ICP-MS. Each platform has its own unique characteristics, enabling precise detection of various biomarkers.

Based on the characteristics of various technical platforms, tandem mass spectrometry offers superior quantitative performance with high sensitivity and specificity, making it suitable for the detection of small molecules. Its applications are rapidly expanding in areas such as newborn screening, therapeutic drug monitoring, and vitamin testing.

MALDI-TOF still has immense untapped application potential.The application of MALDI-TOF in microbial identification is well-established. In fact, MALDI-TOF has a broad molecular weight range, enabling the detection of both biomacromolecules and small molecules.There is significant application potential in nucleic acid testing, mass spectrometry imaging, and quantitative protein analysis.

Summary of the Characteristics of Different Technology Platforms

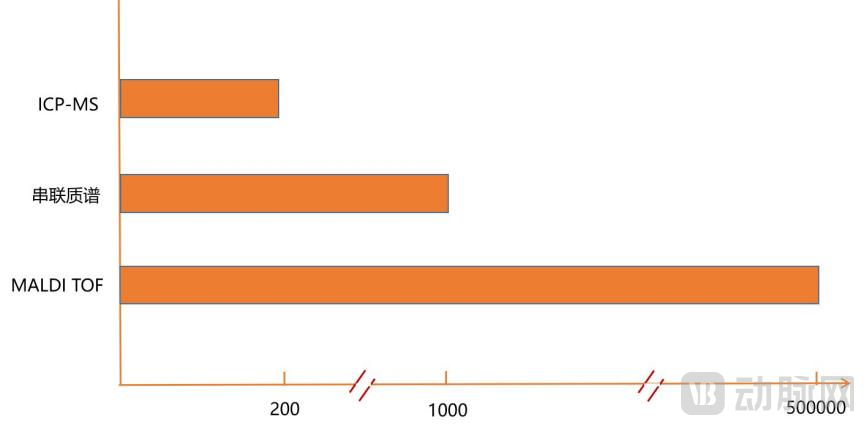

According to data provided by Yixin Mass Spectrometry, the market size for MALDI-TOF exceeds RMB 100 billion. Of this, the market for microbial identification is approximately RMB 2 billion; pharmacogenomics (covering psychiatric, oncology, antihypertensive, lipid-lowering, anticoagulant, and anesthetic drugs) is estimated at RMB 40–50 billion; genetic testing for hereditary diseases (including genes associated with deafness and thalassemia) ranges between RMB 5–8 billion; and infectious disease testing accounts for approximately RMB 20 billion.

MALDI-TOF offers the widest molecular weight range, enables the detection of a greater variety of analytes, and thus corresponds to a larger market potential.

In the clinical mass spectrometry sector, nucleic acid mass spectrometry is the next significant growth driver.

PCR has low throughput and can only detect a few loci, whereas NGS offers high throughput capable of detecting tens of thousands of loci but at a significantly higher cost. Pharmacogenomic testing typically involves dozens to one or two hundred loci, while genetic testing for deafness and thalassemia requires the detection of more than 20 loci. In these cases, PCR lacks sufficient throughput, and NGS is prohibitively expensive and time-consuming.Nucleic acid mass spectrometry offers low cost, rapid turnaround, and simple operation, filling the gap in medium-throughput testing.

An increasing number of companies are focusing on nucleic acid mass spectrometry. Yixin Mass Spectrometry has taken the lead in clearing the regulatory approval hurdle for nucleic acid mass spectrometry instruments, with other domestic enterprises, such as Huangjia Biology, following closely behind.

In 2016, Clin-ToF, developed by Yixin Mass Spectrometry, was approved for nucleic acid detection., enabling simultaneous microbial identification and nucleic acid testing,Pioneering single-platform multi-omics testing. Currently, Clin-ToF has been widely applied in pharmacogenomic testing, genetic testing, and epidemiological testing. Yixin Mass Spectrometry has also participated in the development of China’s first expert consensus on the clinical application of nucleic acid mass spectrometry.

Currently, in addition to the regulatory approval barriers for instruments, the entry barriers for nucleic acid mass spectrometry also include chips, reagents, and related software databases.Yixin Mass Spectrometry has fully established an integrated development pathway encompassing nucleic acid mass spectrometry instruments, chips, reagents, and software databases.Published multiple papers and holds several patents.

In 2015, Yixin Mass Spectrometry and Shimadzu entered into a collaboration on nucleic acid mass spectrometry, which has now continued for seven years. Furthermore, the Institute for Viral Disease Prevention and Control of the Chinese Center for Disease Control and Prevention recently evaluated the effectiveness of eight multiplex detection kits for respiratory pathogens developed by Yixin Mass Spectrometry based on microarray chip–time-of-flight mass spectrometry. The results demonstrated that the product exhibits high accuracy, consistency, and reproducibility.

In the future, obtaining regulatory approval for nucleic acid mass spectrometry reagents will require sustained long-term commitment and substantial capital investment. As more companies enter the nucleic acid mass spectrometry market and secure reagent approvals, this technology is poised to drive the clinical mass spectrometry industry into its next phase of explosive growth.

Currently, companies are already deploying across all major technical platforms in clinical mass spectrometry.

Strategic Layouts of Domestic and International Companies Across Various Clinical Mass Spectrometry Technology Platforms

Upstream in the clinical mass spectrometry sector, similar to the gene sequencing industry, the significant challenges associated with domesticating upstream instruments have meant that the surge in interest has first manifested on the testing application side.

Achieving domestic production of medical instruments requires substantial long-term R&D investment, typically spanning 5 to 10 years. By initially focusing on the testing and application segment, companies can rapidly bring their products and services to market, generate cash flow, and ensure rapid corporate growth. Given the industry’s characteristics,It is a common practice in the industry, particularly among LC-MS companies, to first seek breakthroughs in the testing application sector, and then develop domestically produced instruments to achieve import substitution once clinical education has matured and the market has opened up.

Therefore, at this stage, companies in the diagnostic application sector have demonstrated more impressive fundraising performance, securing substantial investments from numerous institutional investors. Fewer companies are focused on the domestication of instruments, with only a handful such as Yixin Mass Spectrometry and Guoke Medical Engineering.

A growing number of companies are now positioning themselves in the field of clinical mass spectrometry testing. Products for routine applications such as newborn screening, vitamin testing, and therapeutic drug monitoring have already received regulatory approval, while an increasing number of enterprises are also venturing into innovative applications including Alzheimer’s disease detection and cancer testing.

In the early stages, mass spectrometry testing applications drove explosive growth in China’s clinical mass spectrometry industry. Now, as registration certificates for routine applications continue to increase, the testing application segment is becoming increasingly crowded, andThe market for domestically produced upstream instruments remains underdeveloped, presenting significant opportunities. Driven by the trend of domestic substitution, it is now a critical time to focus on the localization of upstream instruments.

Domestic substitution of instruments is a policy-encouraged direction. The "Guidance Standards for Reviewing Government Procurement of Imported Products," jointly issued by the Ministry of Finance and the Ministry of Industry and Information Technology in 2021, clearly stipulates the proportion requirements for government agencies (public institutions) to procure domestically produced medical devices and instruments. It mandates that fully automated mass spectrometry analysis systems must be entirely sourced from domestic products, and the procurement rate of domestic brands for high-performance liquid chromatography-tandem mass spectrometers must be at least 25%.

It is essential to recognize that the localization of instruments is an inevitable choice for the industry. The healthy development of the sector requires a long-term perspective, urging companies to commit themselves to the research and development of domestically produced instruments.

In the early stages, the clinical mass spectrometry market expanded rapidly, driven by diagnostic applications, and its current market size has reached billions. However, to sustain long-term growth, it is indispensable to leverage the advancement of domestically produced instruments and adhere to a long-term strategic perspective.Domestication of instruments is the key to truly unlocking the blue-ocean clinical mass spectrometry market, valued at hundreds of billions.

Currently, the localization of mass spectrometry instruments is still in its early stages.

In terms of MALDI-TOF and ICP-MS,As one of the earliest clinical mass spectrometry companies in China, Yixin Mass Spectrometry, its independently developedClin-ToF is the first MALDI-TOF approved in China., enabling simultaneous microbial identification and nucleic acid detection,under its bannerClin-ICP-QMS is the first ICP-MS approved in China.

Among these factors, patents are the key for clinical mass spectrometry companies to achieve rapid advancement and overtake competitors. In the field of MALDI-TOF patents, Bruker, bioMérieux, and Agilent are the holders of core MALDI-TOF technologies. Yixin Mass Spectrometry’s patent portfolio keeps pace with foreign applicants, with more than 200 cumulative patent applications filed and over 60 patents granted, ranking leading in China.

Currently, Yixin Mass Spectrometry has deployed over 100 units of its self-developed mass spectrometers, covering more than 60 renowned medical institutions and testing centers in China, including Peking Union Medical College Hospital, the PLA General Hospital (301 Hospital), Zhongshan Hospital, the Chinese Center for Disease Control and Prevention, and BGI Genomics. Its market share ranks among the leading positions in China.

Domestication of instruments is a crucial component in building a China-led clinical mass spectrometry ecosystem. In the near future, attention from enterprises and investors toward the domestic production of mass spectrometry instruments will rise rapidly.

Clinical mass spectrometry represents a market worth tens of billions of yuan, with untapped potential expected to surpass that of gene sequencing. Amid the explosive growth of the clinical mass spectrometry industry over the past two years, companies have accelerated their development, with many demonstrating impressive capabilities in fundraising, R&D, and marketing.

Financing capability serves as the foundational support for R&D and marketing. R&D capability determines a company’s ceiling—specifically, the size of the market it can access—while marketing capability plays a decisive role as well. However, this scenario is common across various industries: some companies boast significantly superior financing capabilities yet fail to create practical value; others possess strong R&D strength but achieve unsatisfactory results in commercializing their products.Beyond fundraising, R&D, and marketing capabilities, operational efficiency is even more critical.Pay attention to the return on investment.

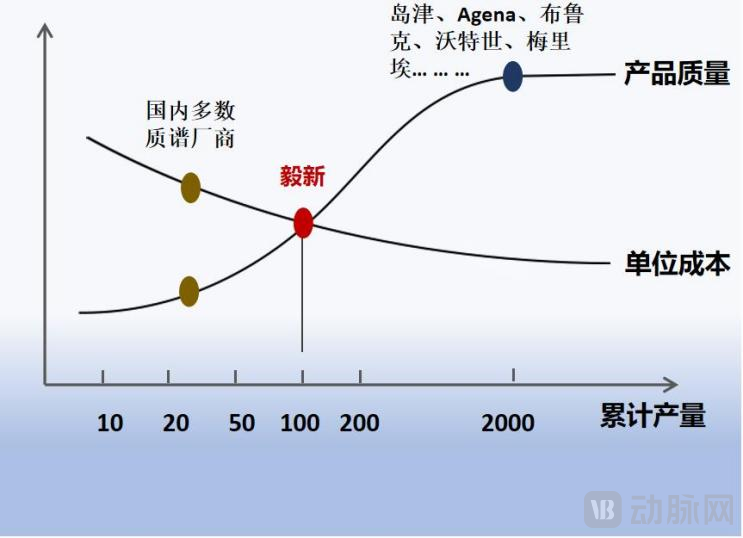

Yixin Mass Spectrometry has 19 years of experience in the mass spectrometry field, with robust technical products. Its production volume has exceeded 100 units, unit costs have gradually entered a plateau phase, and its scale advantages are prominent.Meanwhile, the company has accumulated a large number of clients from Grade 3A hospitals.In 2021, the revenue reached RMB 27 million, with sales expenses accounting for only 10%, indicating operational efficiency far above the industry average.In June 2022, Yi Xin Mass Spectrometry and Kindstar Global reached a cooperation agreement covering their entire product lines.

As production volume increases, unit costs gradually decline while quality steadily improves.

In the future, the strategic importance of domesticating mass spectrometry instruments in China will become increasingly prominent, and MALDI-TOF will emerge as one of the mainstream technology platforms. New opportunities for the development of clinical mass spectrometry include the localization of instrument manufacturing and nucleic acid mass spectrometry. This transition—from diagnostic applications to domestically produced instruments, and from microbial mass spectrometry to nucleic acid mass spectrometry—will eliminate a large number of companies. Key competitive factors among enterprises will center on financing capabilities, R&D capabilities, and marketing capabilities, requiring companies to achieve breakthroughs in operational efficiency.