Breaking Monopolies with Surge of Listings: Johnson & Johnson and Weigao Race to Capture the Orthopedic Robotics Market Amid National Reimbursement Pressure

Stryker

Medical Device R&D, Production, and Sales Company

In recent years, the orthopedics industry has been overshadowed by centralized procurement, yet orthopedic surgical robots have emerged as the brightest spot, with the entire sector accelerating its commercialization efforts.

Once, the RIO surgical robot developed by MAKO Surgical Corporation, a subsidiary of Stryker, was the only joint surgery robot approved in China. This monopoly was broken this year by several domestic companies.

Domestic Joint Replacement Surgical Robot Products Receive Intensive Approvals This Year, including joint replacement surgical robots from Hua Ruibo, Jianjia, Yuanhua Intelligence, and MicroPort MedBot, all obtained registration certificates this year. In August, MicroPort MedBot’s joint replacement surgical robot also received FDA approval for use in total knee arthroplasty.

At the same time, former giants in the orthopedic implant consumables sector have also begun to partner with orthopedic surgical robotics companies.Global joint leader Johnson & Johnson announced a partnership with Changmugu, a provider of digital orthopedic solutions; domestic leader Weigao Orthopaedics also announced a strategic cooperation with Tinavi.

Distributors, whose profit margins have been squeezed following centralized procurement, are also beginning to turn their attention to surgical robots.Tinavi Medical Technologies stated on its investor relations platform: “The orthopedics sector has undergone significant consolidation over the past two to three years, with distributors showing growing interest in orthopedic robots. Following the completion of volume-based procurement for spinal procedures this year, demand for surgical robots is expected to continue rising as volume-based procurement expands to the entire orthopedics sector next year.”

As stakeholders across the orthopedics industry increasingly focus on emerging orthopedic surgical robots, can these systems become a new profit growth driver for the sector? With orthopedic surgical robots successively obtaining commercialization approvals, what opportunities and challenges lie ahead in this new phase of development? VCBeat has compiled an analysis.

Although orthopedic surgical robots have attracted widespread attention from various industry stakeholders this year, they have actually been developing in China for many years, with their past commercial performance being less prominent.

Stryker’s Mako RIO joint replacement surgical robot was launched in China as early as 2014. Mako has achieved substantial overseas sales and a high utilization rate. Compared with 2020, the number of Mako surgical robots installed in 2021 increased by 27%, with approximately 1,500 units installed globally and a cumulative total of more than 500,000 procedures performed.

However, the installation base of Mako in China is not high. The main reason is that Mako is a closed system that requires the use of Stryker’s artificial joint prostheses. Overseas, many private hospitals can use a single prosthesis brand. However, in China, the introduction of prostheses into hospitals requires a bidding process, making it difficult for large orthopedic centers to rely on a single prosthesis brand.

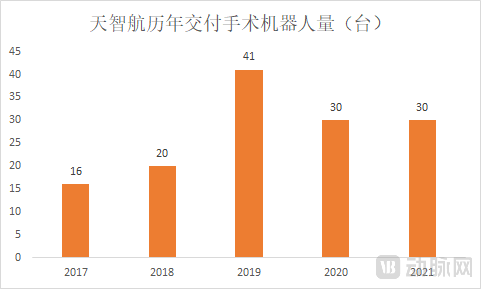

The earliest domestically produced product came from Tinavi. Tinavi was the first to launch an orthopedic surgical robot for spine and trauma surgeries in China. In 2016, Tinavi’s core product, the third-generation “Tianji” orthopedic surgical navigation and positioning robot, obtained the medical device registration certificate from the China Food and Drug Administration (CFDA). To date, Tinavi’s surgical robots have been used in more than 20,000 procedures.

Although its products were launched early, Tinavi Medical Technologies continues to incur sustained losses. Despite selling more than 30 orthopedic surgical robots annually, with each unit priced in the millions of yuan and generating additional revenue from subsequent consumables sales, Tinavi remains unprofitable at current sales volumes. In 2021, the net profit attributable to shareholders of Tinavi Medical Technologies was a loss of RMB 79.93 million, representing a 46.74% year-on-year increase in losses.

Orthopedic surgical robots are no stranger to the industry, and early entrants have revealed the commercialization barriers in this field. Why, then, are companies across the industry increasingly partnering with orthopedic surgical robot manufacturers this year?

It is evident that the trigger for the growing attention to surgical robots in the orthopedics industry has been the centralized procurement of orthopedic products.

Centralized procurement has dealt a heavy blow to domestic orthopedic implant manufacturers. The profit margins for orthopedic consumables, such as surgical instruments and tools previously sold in the orthopedic market, have been squeezed, making the high-price, high-gross-margin model unsustainable.

For leading domestic companies, the impact of centralized procurement is evident.Weigao Orthopedics, which has performed well in the centralized procurement program, rose from the third-largest to the largest domestic manufacturer in the artificial joint market by leveraging centralized procurement. It has surpassed some foreign competitors and rapidly narrowed the gap with international giants. However, centralized procurement has still impacted Weigao Orthopedics’ operating revenue. In the first half of 2022, Weigao Orthopedics reported operating revenue of RMB 1,105.2263 million, a year-on-year increase of 0.90%, indicating a slowdown in growth rate.

As centralized procurement gradually covers the three major segments of the orthopedic market—trauma, joints, and spinal implants—there are now no restricted areas for orthopedic consumables under this policy. Companies whose livelihoods depend on orthopedic consumables have begun to intensify their collaborations with surgical robot manufacturers, leveraging their existing channel advantages to start selling orthopedic surgical robots.

Weigao Orthopedics has comprehensively deployed diagnostic, surgical, and rehabilitation robots across the entire care continuum this year. In February, MaiBu Robotics, an exoskeleton rehabilitation robot company, received strategic investment from Weigao Orthopedics. The two parties also established a joint venture to collaboratively develop and commercialize intelligent orthopedic therapeutic devices, orthopedic rehabilitation robots, and orthopedic rehabilitation assessment systems. Another collaboration was forged in the field of surgical robots: in August, Weigao and Tinavi Medical Technologies formally established a strategic partnership for the research, development, and application of surgical robots in orthopedics.

Chunli Medical also responded to investors, stating that it is developing orthopedic surgical robots for use in various joint replacement procedures, including hip and knee replacements.

Even multinational corporations with stronger risk resilience have begun to prioritize surgical robots after experiencing a cliff-like drop in product profits.

An industry insider stated that, taking artificial joints as an example, the price difference between the supply agent’s price and the end-user sales price for a foreign company’s ceramic-on-ceramic artificial hip joint is only 50 yuan, resulting in very low profit margins. Consequently, this year, when selling artificial joint products, the company has also begun recommending the use of its surgical robots or surgical navigation software.

"From current pricing, orthopedic surgical robots are priced relatively high, leaving substantial profit margins for orthopedic companies."

The average selling price of Tinavi’s trauma and spine surgery robots was RMB 5.2083 million per unit before 2019, and RMB 3.7197 million and RMB 3.8234 million per unit in 2020 and 2021, respectively. Compared with artificial joint prostheses priced at the thousand-yuan level, surgical robot systems are more attractive.

In addition to surgical robot systems, surgical robots typically involve proprietary consumables. Taking Tinavi as an example, its sales revenue from orthopedic surgical navigation and positioning robots amounted to RMB 110 million in 2021, while revenue from ancillary equipment and consumables reached RMB 14.78 million. Although consumable-related revenue remains relatively modest at present, it is growing rapidly, with operating income from ancillary equipment and consumables increasing by 59.07% year-on-year compared to the same period in 2020.

With the intensive approval of orthopedic surgical robots in China and the market entry of orthopedic consumables companies, has the commercialization of orthopedic surgical robots truly begun to accelerate?

From the perspective of advantages, the greatest clinical value brought by orthopedic surgical robots is the ability to control surgical precision to within millimeters.Spine and trauma surgical robots demonstrate significantly higher accuracy in pedicle screw placement compared to traditional surgery; the navigation and positioning technology of joint surgical robots can guide surgeons to precisely cut at planned sites, helping to preserve healthy bone and soft tissue. Surgeons can also modify the surgical plan intraoperatively to improve soft tissue balance and enhance the precision of osteotomy and implantation.

Despite their advantages, orthopedic surgical robots still have certain limitations.

First, from the perspective of clinical value, it is not easy to gain physicians’ acceptance of orthopedic surgical robots.In joint replacement surgery, procedures are primarily categorized into hip and knee replacements. For hip replacement, the surgical technique is highly mature; an experienced surgeon can complete the procedure in approximately ten minutes. Consequently, the demand for surgical robots among physicians is relatively low.

In knee arthroplasty, a successful procedure should encompass proper lower limb alignment, adept soft tissue balancing, consistent flexion and extension gaps, optimal patellar tracking, precise bone resection and prosthetic component positioning, strict aseptic technique, and minimally invasive principles.

Surgical robots must address three major challenges: achieving consistent flexion and extension gaps, ensuring osteotomy and prosthetic implantation meet required standards, and mastering soft tissue balancing techniques. However, the solutions offered by orthopedic surgical robots for soft tissue balancing still require improvement. Lower limb alignment and knee joint soft tissue balance are critical factors influencing patient satisfaction, clinical functional outcomes, and long-term prosthetic survival following total knee arthroplasty (TKA).

Regarding soft tissue balance, despite robotic assistance, the objective assessment of soft tissue balance and tension remains a challenge in total knee arthroplasty (TKA). In recent years, digital intraoperative gap pressure sensors, which have gradually gained adoption abroad, are expected to effectively address this difficulty. Among these, the Verasense system (OrthoSensor, USA) is the most representative example. The Verasense system is a disposable sensor used during TKA to measure joint gap pressure and pressure distribution, enabling real-time measurement of medial and lateral joint gap pressures throughout the full range of knee motion.

To address this issue, in 2021, two global orthopedic giants acquired sensor companies: Zimmer Biomet acquired Canary Medical, and Stryker acquired OrthoSensor along with its Verasense intraoperative sensor technology.

"An industry insider explained, 'The acquisition of two sensor companies is driven by the goal of integrating muscle tension data into the entire surgical procedure. If the issue of muscle tension cannot be addressed, and the focus remains solely on bony landmarking to improve osteotomy accuracy, the clinical value remains limited.'"

Second, from a cost perspective, surgical robots are relatively expensive.Surgical robots priced in the millions represent a significant cost burden for hospitals, while also resulting in higher surgical fees for patients. For Tinavi’s products, the startup fee is RMB 8,000, and the disposable kit costs between RMB 11,000 and RMB 13,000. Patients who opt to use the orthopedic surgical robot along with its associated consumables will face increased out-of-pocket expenses.

Moreover, against the backdrop of medical insurance cost containment, the high prices of surgical robots may also be compressed.. This year, the National Healthcare Security Administration issued two documents to regulate the pricing of orthopedic surgical robots.

In early March, the National Healthcare Security Administration issued the "Guidelines on Improving Pricing and Related Policies for Auxiliary Procedures Such as 'Surgical Robots' and '3D Printing' in Orthopedics (Draft for Comments)," initiating efforts to regulate the orthopedic robotics market by imposing price controls and restrictions on orthopedic surgical robots, thereby guiding the healthy development of the industry. This document has had a significant impact on the entire sector.

The “Opinions on Supporting Measures for the Centralized Volume-Based Procurement and Use of High-Value Medical Consumables (Artificial Joints) Organized by the State” also states that when public medical institutions employ intelligent systems such as “surgical robots” to assist in surgical procedures, they shall adhere to the principles of balancing labor value with equipment contribution and aligning fees with functionality. Additional charges shall be applied as a certain percentage increase over the base price of the “artificial joint replacement” procedure item, based on the actual functions of the intelligent system, without establishing separate fee items.

Finally, the commercialization challenges of orthopedic surgical robots also include intense competition.According to Frost & Sullivan, the number of robot-assisted joint replacement surgeries performed annually in China increased from zero in 2015 to 243 cases in 2020, and is expected to further increase at a compound annual growth rate (CAGR) of 162.8% from 2020 to reach 79,964 cases by 2026. The penetration rate of robot-assisted joint replacement surgeries in China was less than 0.1% in 2020 and is estimated to reach 3.1% by 2026.

Although the surgical volume is expected to grow rapidly, it is worth noting that currently only large tertiary Grade-A hospitals or specialized orthopedic hospitals can afford orthopedic surgical robots. However, there are limited large orthopedic centers in China, with only three to four such centers per province. If the grassroots market cannot be tapped, the market space for orthopedic surgical robots will be limited.

More than ten companies have secured a foothold in large domestic orthopedic centers. Manufacturers with regulatory approval for spinal products include Medtronic, Zimmer Biomet, Xinjunte (approved in 2021), and Zhuzheng (approved in 2022). Those with approval for joint products include Stryker, MicroPort Medical (approved in 2022), Gusheng Yuanhua (approved in 2022), Jianjia (approved in 2022), and Huaruibo (approved in 2022). Additionally, products from several other enterprises are in the clinical trial phase, underscoring the intensity of market competition.

The limited number of hospitals with payment capacity is not unique to the Chinese market. In the United States, Stryker’s Mako surgical robot, despite its commercial success, has also faced challenges due to hospitals’ constrained financial capabilities.

Stryker’s Q2 2022 financial report shows that sales of its Mako surgical robot increased by 19% in the second quarter compared to the same period in 2021. However, as more hospitals shift toward lease agreements or financing rather than purchasing equipment outright, the company’s quarterly revenue is declining.

Overall, the digitalization of orthopedic surgery represents a prevailing trend in medical advancement. The future market potential and rapid growth rate in this field may be difficult to gauge using historical industrial data.

However, products that can truly penetrate the market require multi-stakeholder recognition. Under the influence of centralized volume-based procurement (VBP), acceptance of orthopedic surgical robots within the orthopedics industry has increased significantly. Leveraging the mature commercialization expertise of orthopedic companies, channels for introducing orthopedic surgical robots into clinical practice have been opened. Nevertheless, for clinicians and patients alike, long-term market education and continuous product improvement remain necessary for orthopedic surgical robots.

Existing orthopedic surgical robots are categorized into spine surgery robots and joint surgery robots; a single robotic system is not universally applicable to all orthopedic procedures. For hospitals, purchasing two separate orthopedic surgical robots is overly burdensome. Current orthopedic surgical robots require greater integration and further innovation. Only companies with sustained innovative capabilities that listen to and address clinical needs will survive in the long term, rather than those merely chasing market trends.

References:

Zhang Xianlong | Selection of Lower Limb Alignment and Soft Tissue Balancing Strategies in Robot-Assisted Total Knee Arthroplasty——

Chinese Journal of Reparative and Reconstructive Surgery