Financial Performance and Commercialization Challenges of Five Listed Digital Therapeutics Companies: Insights from Recent Filings

TALi

Software Solution Provider

Pear Therapeutics

Developer of Digital Healthcare Solutions

Better Therapeutics

Prescription Digital Therapeutics Provider

Aptar Pharma

Injection and Spray Delivery Systems, Healthcare Services, and Pharmaceutical Providers

DarioHealth

Digital Therapeutics Platform Operator

Digital therapeutics is an entirely new field, with the vast majority of companies in this sector still in their early stages. However, some industry pioneers have made significant strides and completed their initial public offerings, thereby entering a new phase of development.

In June 2021, Pear Therapeutics (hereinafter referred to as “Pear”), a star enterprise in the digital therapeutics sector, went public via a SPAC merger, with a transaction value reaching $1.6 billion, earning it the title of the “first digital therapeutics stock.” Shortly thereafter, Better Therapeutics (hereinafter referred to as “Better”) also went public via a SPAC merger in October 2021.

As early as March 2016, DarioHealth (hereinafter referred to as “Dario”), which originated in Israel, was already listed on the NASDAQ. However, the term “digital therapeutics” was not yet popular at that time, and Dario did not label itself as a digital therapeutics company.

In August 2022, these three star digital therapeutics companies listed on the U.S. stock market successively released their financial reports for the second quarter of 2022. Due to regulatory oversight of financial disclosures by publicly traded companies, their data is rigorous and precise. Analyzing these financial reports may provide valuable references for China’s digital therapeutics industry.

In addition to these U.S.-listed companies, Australia’s TALi Health (hereinafter referred to as “TALi”) and Voluntis, a benchmark for digital therapeutics in Europe, have also been publicly listed in their respective countries for several years. What do the financial reports of these digital therapeutics pioneers reveal about their actual performance? What are the prospects for the commercialization of digital therapeutics? What challenges do they face, and what strategies can break through these bottlenecks? VCBeat (WeChat ID: VCBeat) provides an analysis of these questions.

As one of the nine initial participants in the FDA’s Software Pre-Certification Program, Pear is undoubtedly a star company in the digital therapeutics sector. Currently, it has three FDA-approved digital therapeutic products for different indications, making it a leader in the industry.

Among them, reSET and reSET-O target substance use disorder and opioid use disorder, respectively, representing typical digital therapeutics for addiction withdrawal. Somryst is a digital therapeutic for chronic insomnia, treating adults with chronic insomnia through cognitive behavioral therapy.

Pear also has 14 products in development, with 10 candidate products falling within its two initial focus areas of psychiatry and neurology, and the other four in-development products spanning gastroenterology, oncology, and cardiovascular disease. The breadth of its product portfolio and the wide range of diseases covered are truly impressive.

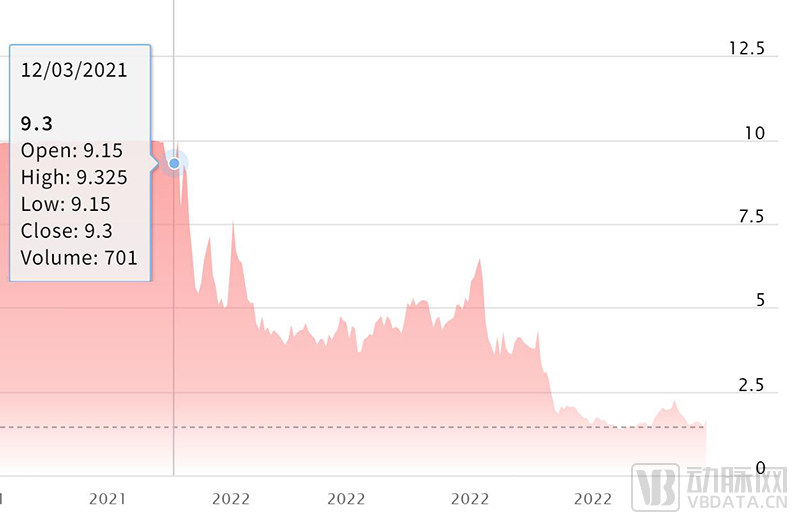

As previously mentioned, this star digital therapeutics company, founded in August 2013, completed the closing on December 3, 2021, merging with Thimble Point Acquisition Corp. under the agreement reached in June 2021, and went public via a SPAC.

Pear’s Stock Price Chart Since Its IPO (Screenshot from the Nasdaq Official Website)

However, Pear’s stock performance has been lackluster since its public listing, with the share price falling from around $9 to the $3–$5 range in a short period. As of August 26, its stock price stood at just $1.69. This decline is attributable, on one hand, to its business performance and, on the other, to the generally depressed valuations of companies that went public via SPAC mergers.

Perhaps due to its current low share price, Pear’s stock has received one Hold rating and five Buy ratings on Wall Street. Analysts’ 12-month price targets for the stock range from $5 to $11. On average, Wall Street analysts expect the share price to reach $8.50 over the next 12 months.

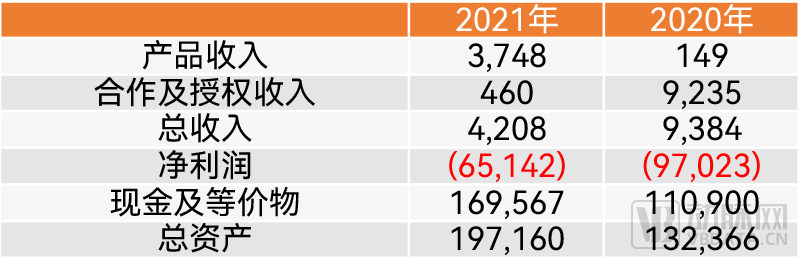

According to Pear Therapeutics' 2021 fiscal year annual report, itsAnnual revenue was modest, at only $4.208 million., falling short even of the $9.384 million in revenue recorded in 2020.However, its revenue structure has undergone a dramatic shift—product sales accounted for $3.748 million of the total $4.208 million in revenue, representing a 24-fold surge from the mere $149,000 in product revenue recorded in 2020.。

Pear Annual Report Metrics Comparison (in thousands of US dollars)

Pear Therapeutics also had highlights in Q1 2022:$2.749 million in revenueThe absolute value is not high, but it represents a nine-fold increase compared to the revenue of only $300,000 in the first quarter of 2021. Meanwhile, these revenuesAll derived from product revenue, nearly catching up with the total product revenue for the full year of 2021.。

Q2 maintained a high growth rate—revenue of $3.297 million represented a 19.9% quarter-over-quarter increase and a 274.5% year-over-year increase. However, the growth in product sales was less than ideal, with only a 9% quarter-over-quarter increase compared to Q1 2022.

Pear's Latest Quarterly Metrics Comparison (in thousands of USD)

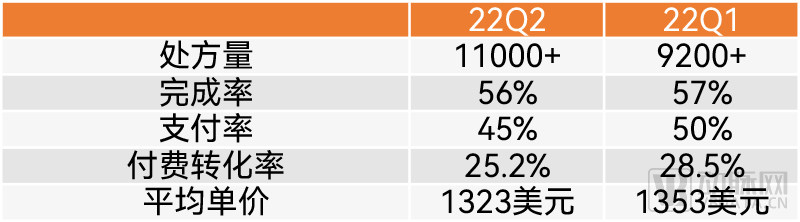

Notably, Pear experienced rapid growth in prescription volume during the first half of 2022. The company issued over 11,000 digital therapeutic prescriptions in the second quarter, adding to the more than 9,200 prescriptions written in the first quarter,Pear issued over 20,000 prescriptions in the first half of 2022, surpassing the more than 14,000 prescriptions issued throughout all of 2021.。

Pear’s prescription completion rate and payment rate in Q2 were 56% and 45%, respectively,The paid conversion rate was 25.2%, essentially on par with the 28.5% recorded in Q1.. This represents a significant improvement compared to the mere 10% paid conversion rate in 2021. In terms of average transaction value, Q2 was largely on par with Q1.

Comparison of Pear’s Prescription Volume and Related Metrics Across Two Quarters

From an analytical perspective, this is closely tied to its continuous release of positive real-world data on digital therapeutics. For instance, real-world data for its flagship product, reSET, showed that reSET could help patients reduce overall hospital visits by 50% within six months, with an estimated cost reduction of $3,591 per patient. In another real-world study, reSET-O demonstrated the ability to help patients save $3,832 in costs.

Meanwhile, Pear continues to expand its market reach, extending the coverage of its digital therapeutics for addiction to eight U.S. states and including them in pharmacy benefit plans across 14 states. Furthermore, backed by real-world performance, its products have gained increasing recognition from insurance plans.

These optimistic developments have led Pear to project full-year 2026 revenue of $14–16 million, with 35,000–45,000 prescriptions issued, and both completion and payment rates reaching 50–65%. For a company that has been public for less than a year, this represents a solid performance.

Of course, more time is needed to observe Pear’s subsequent performance.

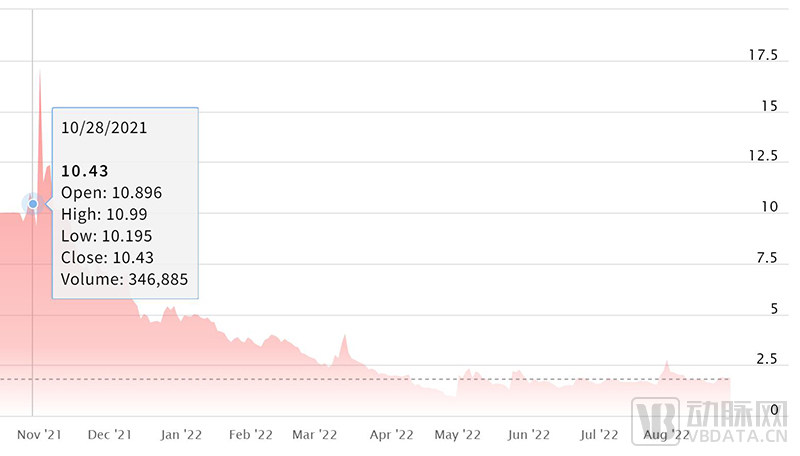

On October 28, 2021, Better completed its merger with Mountain Crest Acquisition Corp. II, going public via a SPAC. Its share price has been on a downward trend since the listing, currently standing at $1.89 (as of August 26), which is in line with its average trading price.

Stock Price Chart of Better Since Its IPO (Screenshot from the Nasdaq Official Website)

It is somewhat surprising that Better Therapeutics has gone public following Pear Therapeutics. After all, Better Therapeutics’ digital therapeutics have not yet completed FDA approval and cannot currently achieve commercial implementation.

This digital therapeutics company primarily develops digital therapies for the treatment of diabetes, heart disease, and other cardiometabolic disorders. Its approach leverages novel cognitive behavioral therapy to modulate neural pathways in the brain, thereby helping patients establish healthy lifestyle habits. This fundamentally improves health outcomes for individuals with diabetes and reduces healthcare costs.

BT-001 is a digital therapeutic based on nutritional cognitive behavioral therapy (nCBT) for type 2 diabetes, which Better Therapeutics is currently prioritizing. It has just completed its first batch of randomized controlled clinical trials. The good news is that the clinical trial results demonstrated achievement of both primary and secondary endpoints. Compared with the control group receiving standard care, patients using BT-001 showed sustained reductions in blood glucose levels and a significant decrease in medication usage.

Better Therapeutics plans to submit an application to the FDA in the third quarter and complete the approval process.

In addition, Better is planning clinical trials to evaluate its nCBT digital therapeutic as a potential treatment for non-alcoholic fatty liver disease (NAFLD) and non-alcoholic steatohepatitis (NASH). The clinical trials are expected to be completed in the fourth quarter of 2022.

As the FDA has not yet approved any effective therapies for these two liver diseases, which affect over 64 million adults in the United States and incur more than $100 billion in direct healthcare costs annually, there is significant potential upon approval.

Better: Latest Annual Report Metrics Comparison (in thousands of USD)

"As the product has not yet been approved, its financial statements show that the company has no revenue.", currently relying primarily on financial measures to sustain its operations. It holds $29.7 million in cash, which is projected to last until the first quarter of 2023 according to plan. Therefore,Whether BT001 can secure FDA approval as scheduled and successfully achieve commercialization will be the key determinant of Better Therapeutics’ fate.。

Better Therapeutics Latest Quarterly Report Metrics Comparison (in thousands of USD)

It is worth noting that, as an R&D-focused enterprise, research and development (R&D) expenses account for the largest proportion of its expenditures. In 2021, annual R&D expenses reached $19.436 million, representing an increase of nearly fivefold compared to 2020. In the first half of 2022, R&D expenses amounted to $7.914 million, remaining the primary expenditure category.

Better Therapeutics managed to go public without obtaining FDA approval, partly because it rode the wave of SPAC listings, and partly because the vast market potential in chronic disease management, such as diabetes, was a key factor driving its IPO.

According to data from the Centers for Medicare & Medicaid Services (CMS), the United States spent $4.1 trillion on healthcare in 2020, with 75% of these costs attributable to chronic disease care. To address the cost challenges associated with chronic disease management, three major shifts are required.

First, the market must shift from a provider-centric approach to a consumer-centric one, embracing the transformative impact of consumerization as a means to engage more patients in their own care, thereby expanding effective chronic disease management.

Secondly, healthcare digitization will connect patients, healthcare providers, and payers, enabling patients to receive health care between clinical visits and transforming healthcare from episodic care to continuous care, thereby achieving scalability. Telemedicine addresses the synchronous aspects of care, while digital health provides large-scale, continuous support.

Finally, performance-based care models are becoming a reality. Unsustainable cost increases and the growing demand for transparency are putting pressure on all healthcare stakeholders to find solutions that address poor health outcomes and reduce care costs.

Digital therapeutics can thus offer a promising outlook. However, it will still take time for these expectations to become reality.

Given that Pear and Better are still in very early stages, it may be premature to draw conclusions. So, how have some digital therapeutics companies that have been public for several years performed?

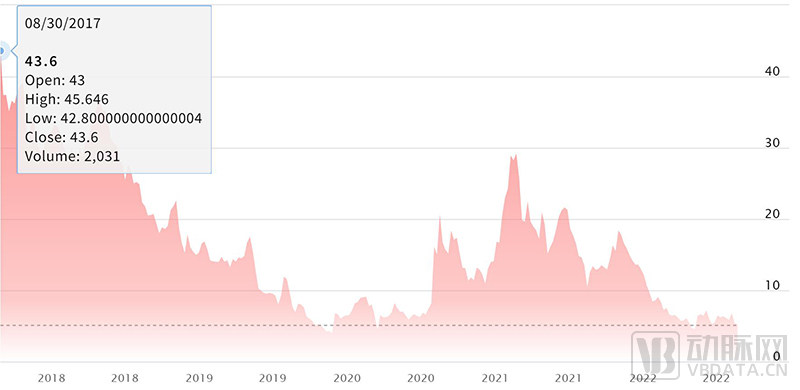

At this point, it is impossible not to mention DarioHealth, an Israeli-born leader in digital therapeutics and one of the pioneers in digital therapeutics for diabetes.As early as March 2016, DarioHealth completed its IPO on the NASDAQ., it has been over six years. As of August 26, its stock price stood at $4.87, nearly on par with its historical low.

Dario’s Stock Price Trend in Recent Years (Screenshot from the Nasdaq Official Website)

Dario, originally named Labstyle, was founded in August 2011. On the eve of its initial public offering in 2016, the company changed its name to DarioHealth. In its early stages, the company focused on intelligent management solutions for chronic diseases such as diabetes. Its Dario smart diabetes management solution received CE certification from the European Union as early as 2013 and subsequently obtained regulatory approvals in Australia, New Zealand, Canada, Israel, and South Africa.

In late 2013, Dario launched its free Dario Smart Diabetes Management App in the UK, marking the inception of its digital therapeutic solution. In March 2014, Dario introduced a digital therapeutic that integrated a hardware-based blood glucose monitoring system. In December 2015, Dario’s product received FDA clearance (under the name Labstyle), enabling it to begin selling its products in the United States in 2016.

The market potential for consumer-focused diabetes management is enormous, but competition in this sector is also fierce. Dario’s initial competitors included pharmaceutical and medical device giants such as Abbott, Asensia (formerly Bayer’s diabetes care division), Johnson & Johnson’s LifeScan, Roche, and Sanofi. These industry leaders hold the majority of the market share in blood glucose monitoring systems (BGMS) for self-management, making it challenging to compete against them.

Therefore, Dario is also attempting to achieve competitive differentiation through digital solutions, including digital therapeutics. However, competition in this segment is equally intensifying. In addition to Livongo, which has been acquired by Teladoc, the landscape includes a host of digital health companies such as Hinge Health, Omada Health, Vida Health, Virta Health, and Glooko.

On one hand, competition is extremely fierce; on the other, the “ceiling” for a business focused solely on chronic disease management for diabetes is beginning to show. Dario’s financial reports clearly indicate that its revenue experienced significant annual growth from 2015 to 2018. However, since 2018, its annual revenue has stabilized at around $7.5 million, with little change.

Dario’s Latest Annual Report Metric Comparison (in thousands of USD)

To change this situation,Dario has begun to gradually adjust its business model, transitioning from direct-to-consumer (DTC) to B2B2C.. This will significantly expand opportunities for commercial growth and reduce marketing costs.

Meanwhile,Dario also entered other types of chronic disease management through three acquisitions in 2021.In early 2021, Dario acquired Upright Technologies, followed by the acquisition of Physimax in early 2022. Through resource integration, it launched Dario Move, a digital therapeutic for chronic pain. In mid-2021, Dario also acquired PsyInnovations, announcing its entry into the behavioral health sector.

At least from the annual report, this strategy demonstrates its sophistication—In 2021, DarioHealth generated $20.513 million in revenue, representing a substantial 2.7-fold increase from the previous year. In the first half of 2022, it achieved $14.242 million in revenue, marking a 1.6-fold growth compared to the $8.856 million recorded during the same period in 2021.。

Dario: Latest Quarterly Report Metrics Comparison (in thousands of USD)

In addition, DarioHealth announced several pieces of good news in its Q2 financial report. First,SignedThe total value of the commercial contract has reached $55 million., laying a solid foundation for its subsequent operations. Meanwhile,Revenue from the B2B2C business exceeded that from the B2C business in the first half of 2022., demonstrating that the shift to the B2B2C model was a prudent move.

Dario’s strategy to broaden its product line has also proven effective—Its behavioral health solutions have been included in a U.S. national health plan, enabling Dario to cover an additional 10 million members and with revenue generation expected to begin in the third quarter of 2022.。

Furthermore, Dario’s multi-product lineup has generated a synergistic effect—increasingly more members are participating in multiple programs, and the anticipated “1+1+1>3” outcome is taking shape.

Barring any unforeseen circumstances, Dario’s revenue is expected to see significant growth in the second half of the year. This will help Dario gain solid momentum for development.

Pear, Better, and Dario are all publicly listed companies in the U.S. stock market. So, is there a certain difference in the performance of digital therapeutics companies in other regional markets? The annual reports of TALi, listed in Australia, and Voluntis, listed in France, can also provide a reference.

Australia, located in the Southern Hemisphere, has a climate markedly different from that of the Northern Hemisphere; consequently, the fiscal year for its listed companies differs as well, running from July 1 to June 30 of the following year.

TALi, formerly known as Norvita Health, is a renowned digital therapeutics company in Australia. On December 30, 2019, Norvita completed its name change on the Australian Securities Exchange (ASX), and the new company has continued to operate under the name TALi ever since.

TALi has remained focused on the fields of ADHD and ASD. Its evidence-based digital therapeutics for the screening and treatment of attention-deficit/hyperactivity disorder (ADHD) and autism spectrum disorder (ASD) in children have been validated by the market and have secured multiple patents.

In August 2021, TALi entered into an agreement with Akili, under which Akili would introduce TALi’s digital therapeutic for ADHD in children aged 3–8 to the U.S. market and drive its regulatory approval and commercialization in the United States. Upon achieving the agreed-upon milestones, TALi would receive revenue of AUD 51 million (equivalent to USD 37.5 million).

Meanwhile, TALi is consolidating its markets in Australia, New Zealand, and Singapore while attempting to enter the markets in India, South Korea, and Japan.

Meanwhile, TALi is also exploring new clinical indications for its existing digital therapeutics. Mild cognitive impairment, considered a precursor to Alzheimer’s disease, is its next key focus of exploration.

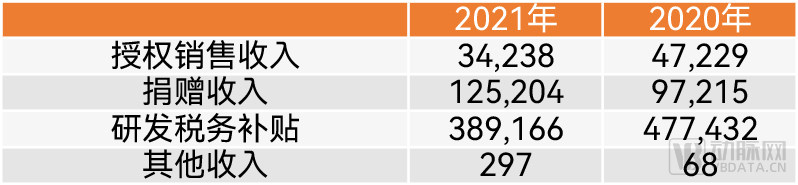

However, TALi's financial reports in recent years do not look optimistic:TALi’s revenues over the past two years were AUD 549 million and AUD 622 million, respectively. While these figures appear substantial on the surface, a closer examination reveals that recurring revenue from licensed sales accounts for less than 10%! The vast majority of its income stems from R&D tax incentives, i.e., government subsidies.。

TALi’s Latest Annual Revenue Breakdown (in thousands of Australian dollars)

Even under these circumstances, its losses have been gradually widening over the past two years. The full-year net loss for FY2019–2020 amounted to AUD 4.198 billion, which further expanded to AUD 4.858 billion in FY2020–2021. Although TALi emphasized in its financial report that its cash flow is sufficient to sustain operations for four quarters, the outlook remains bleak without additional revenue streams.

TALi's Latest Annual Report Metrics (in thousands of Australian dollars)

Meanwhile, the experience of Voluntis, an early leader in digital therapeutics from France, also illustrates a common ailment among publicly listed digital therapeutics companies: a lack of commercialization capability.

Founded in 2001 and headquartered in Paris, France, Voluntis initially operated as a medical software development company. With the rise of digital therapeutics, the company pivoted to focus primarily on chronic disease management for diabetes and digital therapeutics for oncology. In May 2018, Voluntis went public on Euronext, capitalizing on its prominence in the digital therapeutics sector.

In November 2016, Voluntis’ digital therapeutic Insulia received FDA clearance and CE marking. Subsequently, through several additional approvals, the indications for Insulia were expanded to cover a broader range of insulin brands. In August 2019, Voluntis’ oncology management digital therapeutic, Oleena, received FDA clearance. Designed to integrate patient self-management with remote telehealth monitoring, Oleena serves cancer patients undergoing radiotherapy, chemotherapy, immuno-oncology therapy, and targeted cancer therapy.

However, annual reports over the years have consistently reflected a rather bleak revenue performance. The full-year revenues for 2018, 2019, and 2020 were €5.17 million, €4.67 million, and €5.18 million, respectively. That said, its losses were not substantial either. In 2020, the company reported a net loss of €11.977 million, while still maintaining €11 million in cash on hand.

TrueVoluntis’s unceremonious exit was due to its poor performance in the first half of 2021.——In the first half of 2021, Voluntis generated only €1.892 million in revenue, representing a 16% year-on-year decline. The company incurred a loss of €4.269 million for the period. With cash reserves of just €6.357 million, it was no longer able to sustain ongoing operations.

Voluntis’ Latest Annual Revenue Breakdown (in thousands of euros)

In July 2021, Voluntis announced an agreement with Aptar, a leader in the design and provision of drug delivery, consumer product dispensing, and active packaging solutions.. The latter will acquire a 64.6% equity stake in Voluntis for approximately €50.8 million (equivalent to $61.5 million); and subsequently acquire the remaining shares through a mandatory cash offer, bringing the total transaction value to €78.8 million (equivalent to $95.3 million).

In September of that year, the acquisition received approval from the French government and was officially completed. Since then, this early benchmark enterprise in digital therapeutics has vanished from history, a development that evokes much lamentation.

Based on the current performance of several publicly listed digital therapeutics (DTx) companies, even in relatively mature overseas markets, these enterprises still exhibit insufficient commercialization capabilities. In particular, the ceiling effect associated with single-indication DTx products is quite evident, at least as reflected in their annual reports, leading to considerable struggles in their market performance.

This indicates that digital therapeutics are still in the early stages, and the market still requires cultivation.Both enterprises and investors need to have considerable patience., awaiting further market maturity.

The good news is that Pear has seen encouraging gains in key metrics. This at least indicates that,Digital therapeutics are gaining increasing recognition from all stakeholders in the healthcare sector, and this momentum is accelerating and irreversible.。

DarioHealth’s timely adjustments offer valuable insights; leveraging resource integration to broaden indication coverage and transitioning from a 2C to a B2B2C model may well be a viable path for digital therapeutics companies to survive and thrive. Of course, the prerequisite remains that the corresponding products must have clear clinical evidence-based support.

Of course, given different national contexts, the development of digital therapeutics in China may follow a distinct path. After all, “for actually the earth had no roads to begin with, but when many men pass one way, a road is made.”