Amid Investment Winter, Oral Healthcare Upstream Sector Defies Odds with Over RMB 1.5 Billion in Funding: What’s Driving the Surge?

Smartee

Oral Medical Device R&D and Manufacturer

ANGELAIGN

Dental Medical Consumables Supplier and Service Provider

Amid this year’s capital winter, the dental industry continues to maintain its exceptionally high level of interest.

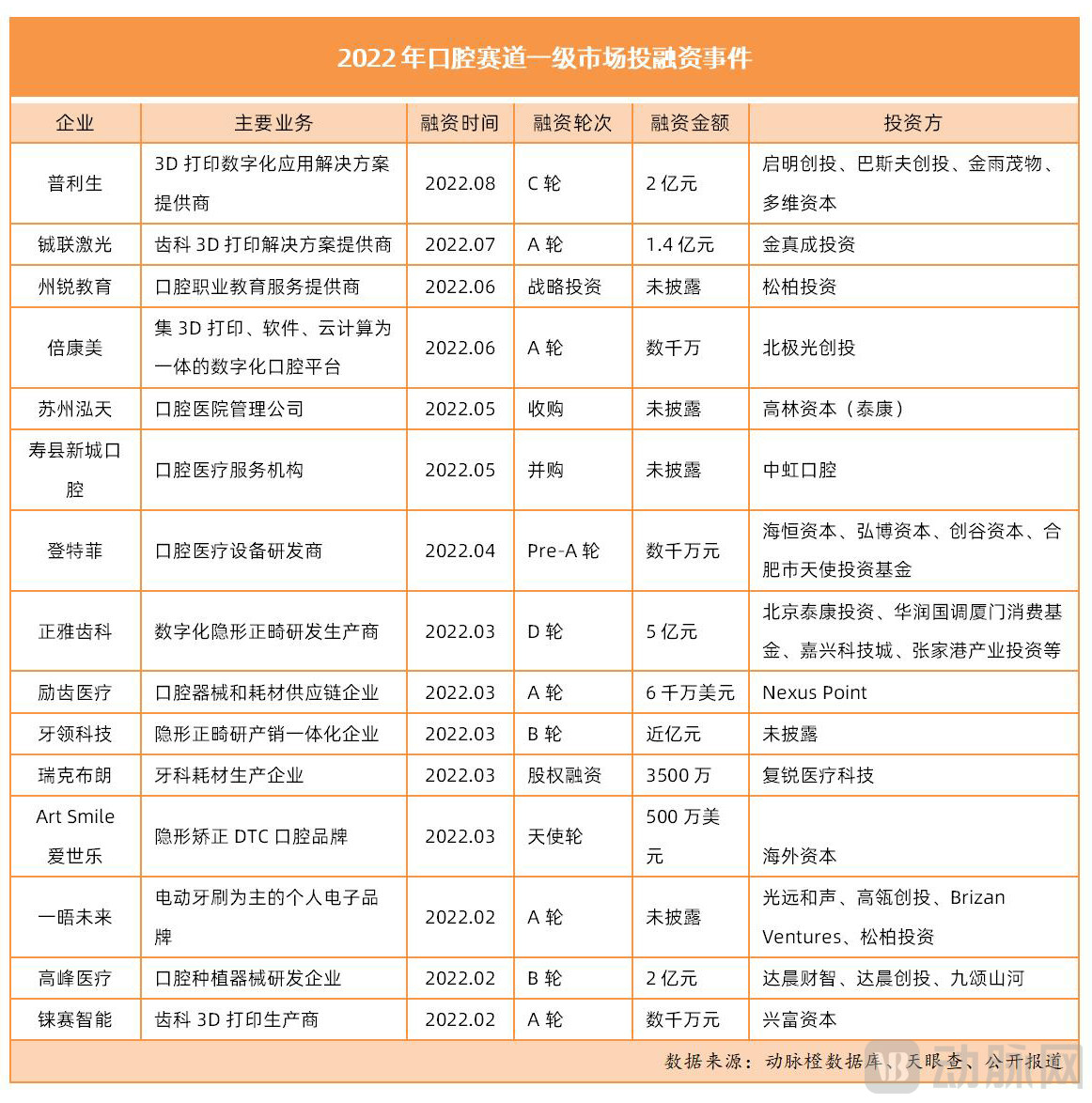

VCBeat’s statistics reveal that from January to August this year, there were 15 financing events in the primary dental market, with a total financing amount exceeding RMB 1.5 billion, reaching a high level in recent years.

Notably, among the companies that secured financing, 11 were upstream enterprises, accounting for a significant 74%.Prominent firms, including Qiming Venture Partners, Northern Light Venture Capital, Hillhouse Investment Group, Songbo Investment, and Fortune Capital, have all made investments. Additionally, some companies have seen investors increase their stakes after completing the initial investment.

“The upstream segment of the dental industry primarily consists of consumables and equipment manufacturers, which can be divided into three subsectors: low-value consumables, high-value consumables, and equipment.” Yang Xin (a pseudonym), an investor focusing on the dental industry, told VCBeat, “Competition in the low-value consumables sector is fierce, while”High-value consumables and equipment have seen significant breakthroughs in recent years, emerging as high-potential growth areas within the dental industry, particularly in the fields of orthodontics and dental implants. Additionally, interest in dental 3D printing is rapidly increasing.”

Taking clear aligner orthodontics as an example, when ANGELAIGN, a dental clear aligner provider, listed on the Hong Kong Stock Exchange last year, it triggered frenzied buying from investors, with its stock price surging by 132% on the first day of trading; its current market capitalization exceeds HK$20 billion. Earlier this year, Smartee Denti-Technology, another leading enterprise in the clear aligner orthodontics sector, announced the completion of its Series D financing round, raising RMB 500 million.

On the other hand, the oral care industry is currently undergoing significant transformation. In mid-August, the National Healthcare Security Administration released the Notice on Launching Special Governance of Service Fees and Consumable Prices for Dental Implant Services (Draft for Comments). The Notice mandates the implementation of special governance over service fees and consumable prices for dental implant services, as well as the nationwide conduct of related price surveys and registration.

This means that the centralized procurement of dental implants has entered a critical phase.In fact, as early as six months ago, prefecture-level cities such as Ningbo in Zhejiang Province and Bengbu in Anhui Province had already taken the lead in piloting these initiatives.

“Once the centralized procurement of dental implants begins, it is highly likely to significantly alter the operational direction of the oral healthcare industry.“Yang Xin stated that, first, a major concern in the current market is whether the percentage reduction in prices of traditional dental implant consumables will lead to a shrinkage of the dental implant market size, thereby affecting the revenue of downstream service providers; second, the pricing of dentists’ medical services will be put on the agenda. ‘Previously, dentists’ medical services were bundled into the overall price, making quantitative analysis difficult. This volume-based procurement may set a precedent.’”

Why Is the Upstream Dental Sector So Hot? What Major Changes Have Occurred Since 2022? What Variables Will the Centralized Procurement of Dental Implants Introduce? What Are the Future Trends? To address these questions, VCBeat has conducted a comprehensive review and interviewed numerous industry experts and investors to shed light on the answers.

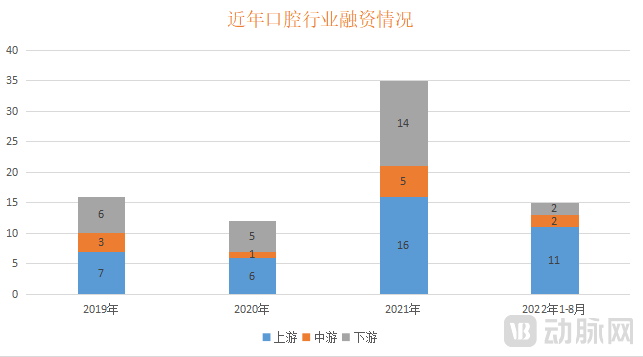

Based on the financing trends in the oral care industry in recent years, upstream segments have witnessed the most frequent financing activities and have attracted heightened attention from investment institutions this year.

(Financing Trends in the Upstream and Downstream Sectors of the Oral Care Industry in Recent Years)

(Financing Trends in the Upstream and Downstream Sectors of the Oral Care Industry in Recent Years)

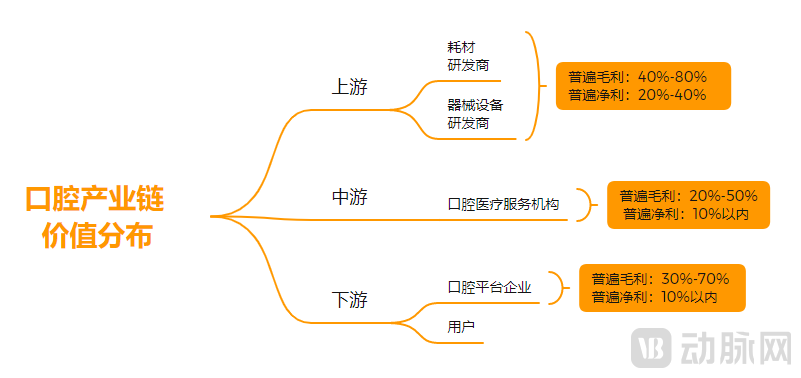

Behind the wave of investment firms shifting their focus lies a reality tied to the current state of the industry:A typical characteristic of China's current dental industry chain is the uneven distribution of value: upstream enterprises demonstrate strong profitability, while midstream and downstream enterprises show relatively weak profit performance, with an intensifying head effect.

How so? Upon reviewing the financial reports of four upstream dental companies—Sinocera, Meyer Optoelectronic, ANGELAIGN, and Align Technology—VCBeat found that their gross profit margins stood at 45.04%, 51.15%, 65%, and 71.33%, respectively. Such levels of gross profitability place them firmly in the top tier, even among the more than 4,000 companies listed on China’s A-share market.

Within the entire oral care industry chain, mid- and downstream enterprises—such as medical aesthetic service providers, supply chain companies, and health IT vendors—have average gross profit margins ranging from 30% to 60%, which is overall lower than that of upstream players. Additionally, mid- and downstream segments face challenges such as high customer acquisition costs and weak bargaining power.

(Value Distribution in the Oral Care Industry Chain, Chart by VCBeat)

(Value Distribution in the Oral Care Industry Chain, Chart by VCBeat)

Not only that, the penetration rate of dental services in China was approximately 24% in 2020 (according to data from the prospectus of a Chinese dental healthcare company), which is significantly lower than the 70% in the United States. In other words,Demand for dental services will remain robust over an extended period, while upstream consumables and equipment can translate this latent demand into reality.

Market data from 2022 supports this trend. For instance, Sinocera and Meyer Optoelectronic reported sustained performance growth, with their first-half revenues reaching RMB 1.731 billion (a year-on-year increase of 17.47%) and RMB 904 million (a year-on-year increase of 10.19%), respectively. Impacted by the pandemic, ANGELAIGN’s first-half revenue stood at RMB 571 million, remaining largely flat compared to the same period last year.

As mentioned in GaoHu Capital’s report, “Upstream of the Oral Care Industry: The ‘Chain Masters’ Behind the Golden Track, with Three Major Trends Launching a New Journey,”The upstream segment of the oral care industry is also characterized by high entry barriers, strong technical barriers, and significant scalability.

Specifically, high entry barriers refer to the fact that upstream dental consumables and devices must undergo rigorous clinical trials and regulatory approval, a process that can take as little as two years or more than five years, resulting in a lengthy timeline. Strong technical barriers exist because most dental products are multidisciplinary innovations, requiring the integration of engineering, biology, physics, and even aesthetics. High scalability is based on the standardized nature of upstream dental products, which enables expansion into global markets and the achievement of economies of scale.

In a nutshell, driven by continuously rising demand on the consumer side, coupled with exceptional revenue-generating capabilities and strong competitive moats, China’s oral care industry has truly entered a phase of business growth dominated by technological and product innovation, making the upstream segment the core rationale for investment institutions’ bets.

Against this backdrop, identifying upstream innovative enterprises that can meet broader demands and deliver a greater volume of higher-quality products will become the mainstream trend in the dental industry.

Looking at the upstream dental companies that secured financing in 2022, digitalization is a prominent hallmark.

The reason is that the dental industry remains largely traditional, with low digital penetration across equipment, consumables, and management processes. Additionally, constrained by the vast number of SKUs and fragmented demand in the dental sector, mid- and downstream enterprises often require comprehensive solutions.

Therefore, digitalization aimed at improving diagnosis and treatment efficiency, and platformization focused on enhancing user experience, have consistently been the key directions of industry development.

At the sub-sector level, “clear aligner orthodontics,” “dental implants,” and “3D printing in dentistry” have emerged as the three core areas attracting investment this year. Given the distinct investment rationales and trends across these three sub-sectors, each will be discussed separately below.

Invisible Orthodontics: The Blueprint of a Trillion-Yuan Blue Ocean Market Emerges, with Digitalization Accelerating Industry Transformation

The development of the orthodontics market is correlated with the overall prevalence of malocclusion in China.

A national survey conducted by the Orthodontic Committee of the Chinese Stomatological Association shows that,The prevalence of malocclusion in China is as high as approximately 70%, and this demand is driving the rapid development of the orthodontic market.

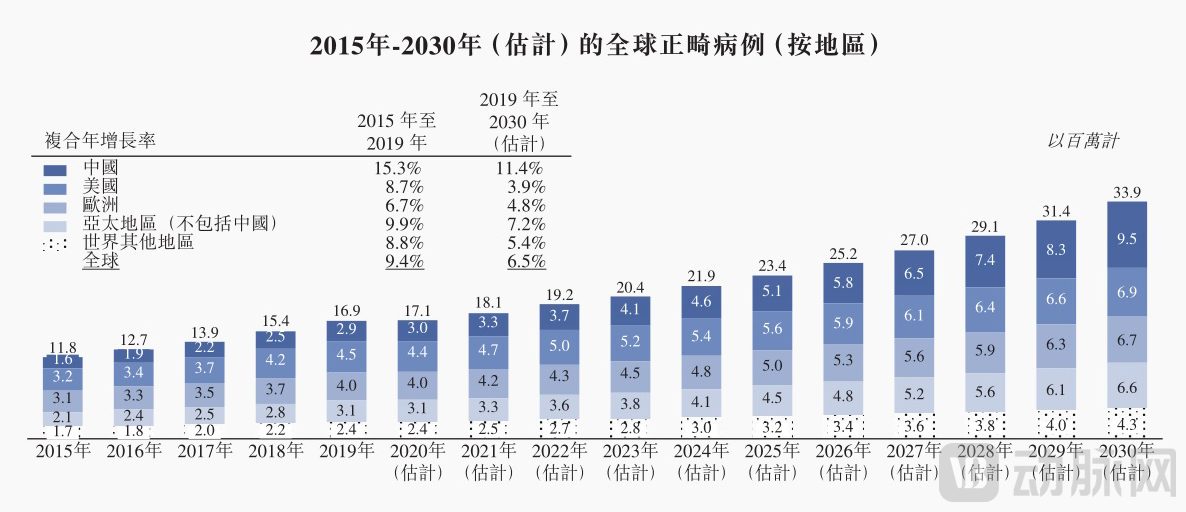

Currently, the number of orthodontic cases in China has increased from 1.6 million in 2015 to 3.1 million in 2020. Among these, the number of orthodontic cases treated with clear aligners is projected to reach 3.8 million by 2030, representing a compound annual growth rate (CAGR) of 27.6%. The market holds immense potential, with its size estimated to reach the hundred-billion-yuan level within a decade.

(Source: Frost & Sullivan Report)

(Source: Frost & Sullivan Report)

In addition to the vast blue-ocean market, the exceptionally high gross profit margins of clear aligner products are also highly valued by investors and enterprises.This is because the clear aligner industry features a high degree of market concentration, with leading companies demonstrating strong profitability, thanks to significant technological barriers and substantial potential for market growth. According to the latest financial report from ANGELAIGN, China’s first publicly listed clear aligner company, its gross profit for the first half of this year reached RMB 331 million, with a gross margin of 60.2%.

High barriers to entry and favorable profit margins have made companies in the clear aligner orthodontics sector frequently sought after. It can be seen that,This year alone, companies that have secured financing include Yaling Technology, Prismlab, Smartee Denti-Technology, and Aishile, with single-round funding amounts generally approaching RMB 100 million.

Of course, clear aligner orthodontics is a technology-driven sector where R&D is paramount. Take Smartee, which secured RMB 500 million in financing earlier this year, as an example. Since 2019, Smartee has collaborated with Professor Shen Gang’s orthodontic team from Taikang Bybo to develop the Smartee GS product series. Centered on the concept of “jaw position reconstruction,” this joint effort has produced the Smartee GS product series, which uses facial aesthetics as a starting point and incorporates factors such as occlusion, alveolar process protrusion, and jawbone relationships into its diagnostic and treatment standards.

Another example is Yaling Technology, which secured financing in March. Its flagship brand, “SmileAlign,” is a bracketless clear aligner brand featuring patented technologies such as the “RAS Root and Bone Analysis System” and “RMS In-Treatment Monitoring.” In less than three years, “SmileAlign” has entered numerous large chain clinics across China, serving tens of thousands of patients.

In August, Prismlab secured financing and leveraged its strengths in 3D printing to launch a comprehensive solution for clear aligner therapy. Centered on 3D printing equipment, the solution covers the entire industry chain—from 3D printing and orthodontic film materials to automated thermoforming and cutting—thereby establishing a complete manufacturing and processing system for clear aligners.

From the perspective of market structure, the market is currently dominated by Align Technology’s Invisalign brand and ANGELAIGN, while other companies hold relatively small market shares.

As clear aligner therapy is an interdisciplinary field integrating five major technological domains—orthodontics, computer science, materials science, modern intelligent manufacturing, and biomechanics—it requires seamless integration of technology and clinical practice, resulting in high overall technical demands and significant challenges in commercial implementation.

AndAs more companies enter the clear aligner orthodontics sector, industry competition is becoming increasingly intense.In response, many industry experts believe that invisible orthodontics companies should prioritize building technical barriers for product differentiation and establishing robust business models; those with room for downward pricing adjustments may be able to carve out a viable path.

Dental Implants: Amid the Centralized Procurement Trend, Domestic Substitution Is Accelerating

Dental implants, as a major standalone sector in dentistry akin to clear aligner orthodontics, have long been favored by investors.However, the announcement of centralized procurement for dental implants has introduced significant uncertainty into this sector.

From the perspective of the current market, the pricing for dental implants mainly consists of three components: consumables, physician service fees, and hospital operational costs. Among these, consumables account for approximately 25%, physician service fees make up about 40%, and the remainder covers hospital operational expenses.

To standardize the pricing of dental implant services, the "Draft for Comments" released in August addresses the composition of service items by implementing three key measures: separating technical service fees from consumable costs, consolidating price items, and rationalizing price ratios.From this perspective, the centralized procurement of dental implants has entered a critical phase.

“In addition to the high cost of consumables themselves, high physician service fees are also a significant factor hindering price reductions for dental implants.” Yang Xin, an investor focused on the oral healthcare industry, stated that the previous lack of “separation of technical services and consumables” in dental implant procedures, along with the opacity of surgical treatment fees—which constitute the majority of the cost—is one of the reasons why patients perceive dental implants as expensive.“As the centralized procurement program approaches, dental implant prices are highly likely to fall to reasonable levels, thereby accelerating the substitution of domestic products for imports.”

It is important to note that in the dental implant sector, domestically produced implants in China hold a small market share of approximately 7%, largely due to their late entry into the market. This situation stems from insufficient accumulation of technology and clinical experience with domestic implants, as well as the relatively lagging commercialization of the entire industry chain.

Taking surface treatment technology as an example, data from Gaohe Investment Research Center indicates that most domestically produced dental implant brands remain at the second- and third-generation levels, characterized by simple coating and sandblasted acid-etching treatments. In contrast, the two industry leaders, Nobel Biocare and Straumann, have adopted fourth-generation technologies: TiUnite anodic oxidation treatment and SLActive (hydrophilic SLA) hydrophilic sandblasted acid-etching treatment, respectively. These advanced techniques offer superior biocompatibility, corrosion resistance, and bone-implant bond strength. This highlights a significant gap between domestic dental implant manufacturers and their international counterparts.

Certainly, the dental implant industry achieves scale through volume; if volume increases, the profitability of R&D-driven enterprises will also rise. ThereforeThe implementation of centralized procurement for dental implants has promoted the development of domestically produced implants with price advantages.

According to the "2020 China Oral Healthcare Industry Report," the average number of missing teeth among young and middle-aged adults aged 20 to 44 reached 0.4, while the penetration rate of dental implants was only 2%. This indicates substantial room for growth in the penetration of dental implants in China: following the inclusion of dental implant products in centralized volume-based procurement, the cost per implant has decreased significantly, which is expected to unleash the strong and unmet demand for dental implants.

“There is another trend that is not easily noticed. As far as I know, domestic dental implant manufacturers have had limited success in establishing accounts with public hospitals, especially those in Beijing, Shanghai, and Guangzhou. In previous years, domestic brands had almost no opportunity to enter these institutions, so they primarily focused on private hospitals or clinics that did not require such account setup. However, the introduction of centralized procurement may help open this channel. Once a company successfully establishes an account with a public hospital, its distribution channels and other aspects will naturally become smoother.” Lü Sang, a senior investor in the oral care industry, previously told VCBeat that there are also risks in this process. “Companies must continue to invest boldly in R&D. If the price of dental implants drops and volume increases, but production capacity cannot be expanded and quality cannot be controlled, this would pose a significant problem.”

However, the substitution of domestic products for imports is not an overnight process. From a clinical perspective, it also takes time for physicians to adapt to the various impacts of new (domestic) dental implants on patients.

Therefore, once volume-based procurement (VBP) is implemented, companies should actively participate in VBP for relatively low-end products to expand market share, while for mid-to-high-end products, they should target specific high-value customer segments and capture user mindshare through comprehensive solution offerings.

3D Printing in Dentistry: A Nascent Market Poised for Major Growth Driven by Technological Innovation

Also drawing significant capital attention this year are companies in the dental 3D printing sector, with innovative enterprises such as Becoming Medical, Chamlion Technology, and Rayshape Intelligence securing financing.

The driving force behind this surge is that the oral cavity represents one of the key application scenarios for 3D printing companies.Among these, 3D printing technologies used in dentistry mainly fall into two categories: one is metal 3D printing, primarily used for manufacturing metal crowns, dental frameworks, and other similar products; the other is photopolymerization-based 3D printing, mainly employed to produce dental models, surgical guides for dental implants, and clear aligner molds for orthodontic treatment.

“3D printing has brought opportunities for digital upgrading to the dental industry, enhancing diagnostic and treatment efficiency and quality.” Yang Xin, an investor focusing on the dental sector, stated that 3D printing technologies commonly used in the dental industry are mainly divided into four types: stereolithography (SLA), selective laser melting (SLM), PolyJet inkjet printing, and direct metal laser sintering (DMLS). “Each technology is suited for processing different dental products.”

Taking stereolithography (SLA) as an example, this technology is primarily used for the fabrication of dental surgical guides, temporary crowns and bridges, as well as resin patterns for lost-wax casting.

In addition to technological differences, companies are also making efforts in application scenarios and business model construction.

For instance, Shining 3D focuses on providing one-stop digital dental solutions encompassing 3D scanning, CAD design, and 3D printing. Prismlab, mentioned earlier, has developed a closed-loop application ecosystem for digital dentistry by establishing a system integrating a digital dental platform, 3D printing, and high-performance materials. SprintRay, which has secured multiple rounds of financing, has launched the SprintRay series of 3D printing equipment families and already possesses a relatively comprehensive digital dental solution, with a global presence.

Chamlion Technology, which completed a RMB 140 million Series A financing round in July, is a one-stop provider of digital 3D printing solutions for dentistry. By establishing a large-scale distributed cloud factory for denture manufacturing, it integrates the entire data-driven design and production workflow for dentures, thereby building a comprehensive digital service platform for the dental industry.

Currently, Chamlion Technology has installed over 600 3D printing devices and successfully established more than 130 cloud factories worldwide, achieving a daily production capacity of 50,000 dental crowns and 5,000 removable partial denture frameworks. The company has partnered with numerous dental hospitals and denture laboratories.

Having secured tens of millions in Series A financing in June, Becoming Medical launched its first chairside digital implant 3D printing system, Yunyinmei, at the end of 2020 to address the challenges of difficult quality control and prolonged treatment waiting periods associated with traditional digital implant technologies.

In addition, Becoming launched 3D-printed temperature-sensitive materials with superior application performance and enhanced user experience in 2022, thereby providing dentists and patients with better medical products and service experiences.

Raysmart Intelligence, which secured financing in February, possesses independent R&D capabilities in photopolymerization 3D printing equipment, 3D printing software, and photosensitive resin consumables. Its main products include desktop and professional-grade high-precision DLP 3D printers.

It is worth mentioning that,In addition to capital support, policy incentives are also one of the factors driving the surge in popularity of dental 3D printing this year.For instance, the “National Healthy Oral Health Action Plan (2019–2025)” released in 2020 played a significant role in boosting the momentum of dental 3D printing enterprises. The document stated that efforts should be made to advance the localization of high-end dental devices and materials, such as those involving biological 3D printing.

However, as an emerging technological force, dental 3D printing companies must adhere to a “long-term development mindset” during their continuous growth, establishing an integrated closed-loop efficiency across technology, products, branding, and distribution channels, in order to achieve sustainable long-term success.

Financing in the upstream dental sector has been exceptionally robust this year, indicating that the industry’s upstream segment has entered a phase of accelerated growth.

This window period presents a significant opportunity for domestic brands. Under this overarching theme, first, attention should be paid to the incremental market opportunities driven by rapid growth; second, given that foreign brands still hold the majority of the market share, focus should be placed on new differentiated models and approaches that leverage business model innovation and online-offline integration.

With regard to the selection of specific targets, Gaogu Capital, in its report “The Upstream Dental Sector—The ‘Chain Masters’ Behind a Golden Track: Three Trends Launching a New Journey,” identifies three indicators for reference.

· First, possessing independent R&D and innovation capabilities. In the process of domestic substitution, two key factors are assessed: the speed and the depth of a company’s R&D efforts. R&D speed determines whether a company can seize first-mover advantages during the domestic substitution phase, although channel capabilities should not be overlooked. R&D depth determines whether a company can develop products with competitiveness across China and even globally; this fundamental attribute defines the company’s long-term growth ceiling. Together, these two factors determine the effectiveness and sustainability of a company’s R&D investment.

· Second, the ability to integrate hardware and software. The digitalization trend has imposed new requirements on enterprises: only companies with accumulated expertise in both core products and data can deeply engage in the clinical diagnosis and treatment process, thereby optimizing overall efficiency, user experience, and therapeutic outcomes.

· Third, the enterprise’s platform-based management capability. Platform-based enterprises hold distinct advantages in terms of market ceiling, risk resilience, and synergistic effects. Key focus should be placed on the product competitiveness across various product lines and the company’s organizational strength, to avoid mediocrity in products and managerial chaos resulting from multi-front operations.

With the influx of capital, the dental sector undoubtedly experienced sustained explosive growth in 2022, and this trend is set to continue.

However, it is important to recognize that heated capital interest does not equate to industry maturity. Therefore, dental enterprises must continue to deepen their technological expertise and iterate their business models amidst an ever-changing market environment.