Amid Economic Winter, China's Early-Stage MedTech Investment Thrives with 25 Deals Raising Over ¥1.4 Billion

“Pass the cold to everyone.”

Recently, Ren Zhengfei mentioned in an internal speech that the global economy will face a sustained recession and a significant decline in consumer spending power over the next decade, meaning that a capital winter will sweep across all sectors.

Review of Early-Stage Healthcare Financing in August 2022

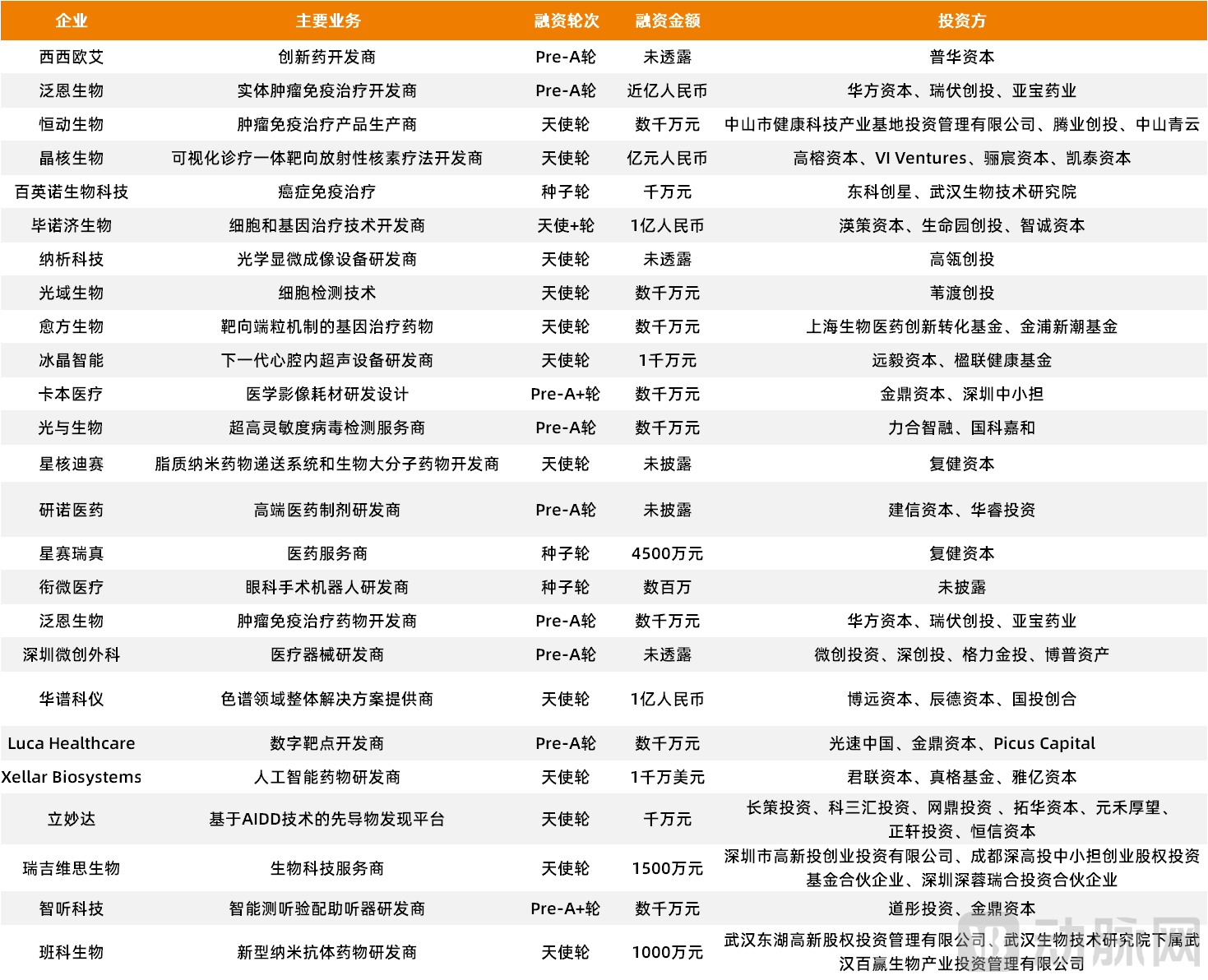

However, the early-stage healthcare financing market appears to have remained unaffected, instead continuing its upward trajectory. According toVCBeat Orange BureauAccording to incomplete statistics, a total of incidents occurred in China's healthcare and medical sector in August25+Early-stage Investment and Financing Events, Total Financing AmountApproximately RMB 1.4 billion。

This raises a compelling question: Why has the early-stage healthcare investment market defied the winter chill? What is the underlying logic driving this trend? From a corporate perspective, what types of startups are attracting capital, and do they share common characteristics? Finally, from the standpoint of investment firms, what exactly is their investment thesis for early-stage healthcare ventures? To answer these questions, VBInsight will examine the early-stage healthcare financing data from August to gain deeper insights.

Why Is Early-Stage Healthcare Investment "Hot"?

Investing in early-stage ventures is becoming a consensus.

This is not baseless speculation, but is backed by real data. According to previous statistics from VCBeat’s Orange Fruit Bureau, in the first half of 2022, there were a total of 121 early-stage investment and financing events in China’s healthcare sector, with total funding approaching RMB 10 billion. Both the number of financing deals and the total amount raised far exceeded the figures for the entire previous year.

The substantial growth in data is not without reason.

Let’s begin by examining the source. In recent years, under the direct pressure of “performance evaluations,” research institutes have continuously encouraged scientists to launch startups through various means and have spared no effort in creating a favorable environment for them, with the core objective being to hopePromoting the translation of scientists' research achievements.This has, to some extent, prompted a group of scientists to take the lead in stepping out of the laboratory.

Secondly, from the perspective of the overall healthcare market, there is a greater focus on original innovative technologies than ever before. Currently, China's healthcare sector has moved beyond the entrepreneurial era dominated by "domestic substitution" under traditional business models; the low-hanging "fruits" have largely been picked.Future opportunities will undoubtedly favor innovative enterprises that possess truly original technologies and can meet clinical needs.

Finally, from the perspective of investment institutions,Investment boundaries will become increasingly blurred, forcing a strategic shift toward early-stage investing.

In recent years, the trend of younger companies going public in the healthcare sector has become increasingly pronounced. Taking 2021 as an example, among the 98 newly listed companies, 31 had been established for less than 10 years, indicating a significant compression of the traditional 15–20 year timeline for healthcare firms to go public.

As going public becomes increasingly “easy,” the pace of investment and financing is accelerating accordingly. According to the 2021 Global Healthcare Industry Capital Report released by VCBeat, China’s total healthcare industry investment and financing reached a record high of RMB 219.2 billion in 2021, a year-on-year increase of 32.84%; the number of financing transactions reached 1,362, a year-on-year increase of 77.57%.

It is worth noting that many startups have completed two or even three rounds of financing within a single year, a pace far exceeding previous norms. It is precisely under this investment environment characterized by “rapid matching” that investment boundaries are becoming increasingly blurred. Investment institutions that previously focused exclusively on mid-to-late stages are finding it difficult to identify suitable entry points; consequently, they are shifting their focus to early-stage projects, nurturing them from the ground up (“from zero”).

In a sense, China’s healthcare sector has transitioned from “imitation” to “innovation.” Consequently, both the sources of innovation and the industry side, represented by investment institutions, have shifted their focus to the early stages. Therefore, even during a capital winter, startups with genuine original technologies and vast market potential will always remain highly sought after by investors.

Startup Financing Essentials: Star Team + Hard-Tech Focus

Having clarified why the early-stage healthcare investment market has gained momentum, we now turn to a specific question: what types of startups are favored by capital?

By conducting a case-by-case analysis of the 25 companies that completed early-stage financing in August, VCBeat’s Orange Bureau has identified two common characteristics: first, all founders are scientists, and their core teams possess strong technical backgrounds; second, these startups are all targeting frontier technology sectors, exhibiting a pronounced “hard tech” profile.

Let’s begin with the first feature.

According to statistics from VCBeat’s Orange Fruit Bureau, among the 25 companies that completed early-stage financing in August, all founders had scientific backgrounds, as did their core teams behind them. Moreover, most of these scientists hailed from top-tier research institutions either in China or internationally.

which completed an angel round of financing worth nearly RMB 100 million in AugustJinghe BioTake, for example, its founding team, which comprises four PhDs. Dr. Yu Haihua previously worked at GSK, where he spent over a decade engaged in new drug development before joining Huayi Technology to lead molecular imaging and pharmaceutical research. Another co-founder, Dr. Wang Yu, has more than 20 years of experience in the development of various targeted conjugate drugs, including small-molecule radiopharmaceuticals, at internationally renowned pharmaceutical companies such as Endocyte (acquired by Novartis) and Eli Lilly. He possesses extensive experience in new drug development, having supported multiple New Drug Applications (NDAs) and Investigational New Drug (IND) applications in the United States.

In fact, the trend of scientists assuming founder roles aligns with the fundamental dynamics of current entrepreneurship in the healthcare sector. On one hand, policy orientations are encouraging scientists to launch ventures; on the other, the healthcare industry is increasingly extending into high-tech domains. Today’s startups require greater “hard” technological capabilities than in the past, thereby imposing higher demands on founders.

However, it is crucial to recognize that entrepreneurship for scientists is a process of “survival of the fittest,” with only a small minority achieving true success. The transition from scientist to entrepreneur entails a long and arduous journey, involving shifts in cognitive mindset, the ability to leverage market resources, and the development of corporate management capabilities.

This is clearly no easy task, especially for the vast majority of scientists in China today, who are constrained by various limitations and find it difficult to master these core competencies in a short period. As a result, we have observed that startups which completed their early-stage financing in August are all adopting a “scientist + professional manager” team management model, wherein scientists are responsible for technical research while professional managers oversee business operations.

Such “collaborative partnerships” not only help scientists address blind spots in their entrepreneurial ventures but also maximize the strengths of both parties, a trend that is bound to define the future.

Having discussed people, let us now turn to the second characteristic, namelyStartups have all clustered in the hard-tech sector.

According to statistics from VBInsight, among the 25 companies that completed early-stage financing in August,“Hard-tech” enterprises account for 100% of the total, among which 18 are biopharmaceutical companies (72%) and 7 are medical device companies (28%).

Upon further analysis, more than 70% of these 25 companies are focused on medical subsectors such as oncology and cardiovascular diseases, which currently face significant unmet clinical needs and require breakthroughs in many technologies.

Taking Fanen Biotech, which closed a Pre-A financing round of nearly RMB 100 million in August, as an example: to address the technical challenge of lacking comprehensive capabilities to resist and remodel the solid tumor microenvironment, Fanen Biotech employed a whole-genome coverage high-throughput screening platform (HAP) to systematically investigate the impact of each gene on T-cell migration, proliferation, function, and microenvironment remodeling within the tumor microenvironment. Ultimately, by leveraging its Whole-Genome T-Cell Signal Optimization Platform (GSOP), the company identified optimal gene combinations that comprehensively enhanced the functions of CAR-T and TCR-T cells—including tumor infiltration, sustained proliferation and cytotoxic efficacy, and tumor microenvironment remodeling—thereby achieving effective treatment of solid tumors.

In fact, it is inevitable for startups to tackle these hard nuts to crack. In the current healthcare landscape, established leaders have already emerged in nearly every mature niche sector. To carve out a share of the market, startups must possess key technologies capable of breaking industry monopolies or driving sector-wide transformation. These technologies must genuinely address clinical needs and offer irreplaceable value.

A senior investor told VCBeat’s Orange Bureau that “investing early” is not actually about the founders, but rather focuses more on the technology itself and sector selection. This is because many characteristics of founders do not yet manifest in the early stages, making it difficult to predict their future development. Even if founders have “shortcomings,” this is not a major concern, as these issues can be gradually addressed and improved over time.

Therefore, startups must have sufficiently strong “long planks.” These so-called “long planks” refer to selecting market segments with substantial addressable markets and possessing robust proprietary technologies, which constitute the core drivers truly propelling corporate growth.

As Early-Stage Investing Becomes the New Trend, How Should Investment Institutions “Keep Pace with the Times”?

Investment institutions remain the focal point of the early-stage medical investment market. According to statistics from VCBeat’s Orange Fruit Bureau, 61 investment institutions participated in the 25 early-stage financing deals completed in the medical sector in August, representing an increase of 32 institutions compared to the previous month.

In addition to a significant increase in the number of deals, diversification among investment institutions has also become a prominent feature. Through an analysis of these 61 investment firms, VCBeat found that, besides support from leading investors such as Hillhouse Capital and Legend Capital, there were many regional venture capital funds. Examples include Shenzhen High-Tech Investment Venture Capital Co., Ltd., Wuhan East Lake High-Tech Equity Investment Management Co., Ltd., and Zhongshan Health Technology Industrial Base Investment Management Co., Ltd., all of which completed early-stage investments this month. These local funds were established with the aim of better incubating early-stage projects in their respective regions.

In addition, as sources of innovation, research universities and institutes are currently raising angel capital. Typical representatives include ShuiMu Ventures and Hetang Capital, both affiliated with Tsinghua University. These are specialized investment institutions for the industrialization of scientific and technological achievements established under the Tsinghua Industrial Technology Research Institute, with their core mission being to invest in scientific and technological achievements originating from the Tsinghua ecosystem.

Although investment institutions are currently shifting toward earlier-stage investments, this trend, much like scientist-led entrepreneurship, presents numerous challenges.

First, there is the challenge of precisely accessing scientific talent and resources. Research projects at Chinese academic and research institutions are relatively closed off; without a “bridge,” it is difficult for investors to gain entry. Second, there is the issue of how to evaluate scientist-led projects. Unlike mid- to late-stage investments, which focus on relatively mature ventures that have already been validated by the market, early-stage medical projects exhibit high uncertainty, making the evaluation criteria more numerous and complex. Finally, there is the question of how to support the rapid growth of startups. For early-stage ventures, capital may not be the only critical factor; more importantly, investors must provide the necessary post-investment services, which can be more effective than money alone.

How can this be resolved?

The first point isConduct industry research, proactively identify high-potential sectors, conduct in-depth research on companies within these sectors, and then match them with early-stage investment targets.

The second point isTo Establish Multi-Channel AccessCao Wei, a partner at BlueRun Ventures, once stated that to access high-quality early-stage projects, referrals from friends serve as an important channel. Another key avenue is platform engagement, including empowerment initiatives and industry events. Additionally, in terms of industry research, it is essential to actively participate in trade shows. Finally, one should expand their network by proactively connecting with key individuals.

In addition, we have also observed that many investment institutions are linking to a broader pool of scientific resources from various dimensions by establishing incubators, training camps, and scientist forums.

The third point isLearn to Shift PerspectivesDuring interactions with scientist-founders, you should position yourself as a co-founder of the team. Such engagement not only helps build trust with the scientists more quickly but also enables a more comprehensive understanding of the scientific achievement, including what type of company should be built around it, what opportunities exist, and what capabilities and strategic pathways the startup should pursue.

The fourth point isTo hone one's post-investment capabilities. This is critically important. As previously mentioned, scientist-led startups have inherent limitations; therefore, investment institutions must deeply engage in the specific project incubation process and possess strong execution capabilities.

Ren Bobing, Executive Director of Sinovation Ventures and General Manager of its Frontier Technology Fund, has stated that investment institutions must demonstrate targeted coverage, deep understanding, and strong execution capabilities when engaging with early-stage projects. They should help scientists achieve phased progress, such as by refining and validating technologies and building teams that balance forward-looking vision with practical implementation. Only in this way can startup teams grow, thereby enabling investment institutions to reap corresponding benefits.