China's First Cell Culture Media Stock Surges Nearly 70% on Debut, Highlighting High Growth Potential in Biopharma Upstream Sector

Optimize

Cell Culture Technology Development and Biopharmaceutical Contract Development and Manufacturing Organization (CDMO) Provider

On September 2, Optimize, a core raw material supplier for the domestic biopharmaceutical industry, officially listed on the STAR Market of the Shanghai Stock Exchange. As the first publicly traded company in China specializing in cell culture media, its stock price surged by nearly 70% at one point on its trading debut, closing up 58.65%. With its market capitalization exceeding RMB 10 billion, the company has secured a strong start in the capital markets for this highly competitive sector.

Through this public offering, Optimize raised over RMB 500 million. In addition to allocating a portion of the funds to its cell culture R&D center project and supplementing working capital, the company plans to invest more than RMB 300 million in establishing CDMO commercial-scale production capabilities for biologics, thereby accelerating its strategic expansion into key segments of the biologics CDMO value chain.

In 2013, Optimize was founded in the Zhangjiang International Medical Park in Shanghai. Its name is derived from the English word “Optimize,” reflecting its mission to provide cost-effective cell culture media to biopharmaceutical companies worldwide, while subsequently expanding into CDMO services. Prior to its IPO, Optimize was a highly sought-after star project in the primary market, completing five rounds of financing totaling over RMB 500 million and attracting top-tier institutional investors such as China Life Health Industry Fund, CITIC Private Equity Funds Management, Huaxing Capital Healthcare, and Fortune Capital.

According to Sullivan Consulting research data, amidst the wave of domestic substitution in cell culture media, Optimize has secured the second-largest market share among Chinese manufacturers, and even ranks first in the market for certain types of cell culture dishes. Meanwhile, its CDMO business, which has seen continuous expansion in recent years, has contributed to steadily growing revenue.

However, as a type of consumable in the upstream segment of biopharmaceutical manufacturing, cell culture media represents only a niche market with a total size of less than RMB 10 billion and a domestic production rate of merely around 20%. How, then, have companies in this sector achieved public listings with valuations exceeding RMB 10 billion? And why have they been consistently favored by the capital markets?

The years following the outbreak of the COVID-19 pandemic have been a golden period of growth for China's cell culture media industry.

Leading domestic cell culture media companies, including Optimize, Auscomp (Jianshun Bio), and BeiAnji, have witnessed their fastest revenue growth since inception and attracted intense capital interest. Meanwhile, emerging Chinese cell culture media firms such as ZhenGe Biotech, KangSheng Bio, and BaiYinNuo Bio have also become highly sought-after investment targets in the capital market. During this period, prominent venture capital firms—including Legend Capital, Hillhouse Capital, IDG Capital, Qiming Venture Partners, and CDH Investments—have flocked to invest in the sector. With Optimize listing on the STAR Market and Auscomp queuing for its IPO, these investors are now entering a harvest phase.

So, what makes cell culture media, a type of laboratory consumable, so captivating? The answer lies in its pivotal role within the biopharmaceutical industry chain.

Cell culture media are mixtures prepared by combining serum, glucose, lipids, inorganic salts, amino acids, and proteins according to specific formulations. Their purpose is to simulate the cellular growth environment in vitro, providing appropriate pH, osmotic pressure, and various nutrients suitable for cell growth.

Cell culture media are routinely used by manufacturers of biological products, such as conventional vaccines and biologics, as well as by life sciences research institutions.

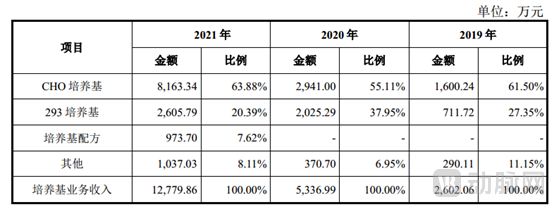

Depending on the cell lines cultured, cell culture media can be categorized into CHO cell culture media, HEK293 cell culture media, and vaccine-specific media such as those for Vero, MDCK, and MDBK cells. Among these, CHO and HEK293 cell culture media are the flagship products of most domestic manufacturers. This also holds true for Optimize: in 2021, approximately 60% of its total revenue, amounting to RMB 127 million, came from its cell culture media business, with revenues from CHO and HEK293 cell culture media reaching RMB 81.63 million and RMB 26.05 million, respectively.

Revenue Structure of Optimize's Culture Media Business, 2019–2021 (Source: Prospectus)

In a WeChat Moments post prior to the company’s IPO, Dr. Xiao Zhihua, founder of Optimize, joyfully remarked that when selecting a stock code for Optimize, he was initially dissatisfied with the 20 options provided. By using his one-time opportunity to request a random assignment, he fortunately drew the final chosen code, 688293, as HEK293 culture medium is Optimize’s flagship star product. “It was destined that we would make the best culture media!” he stated.

Among these, CHO cells and HEK293 cells are both widely used cell types in biopharmaceuticals. To elaborate slightly, the former stands for Chinese Hamster Ovary cells. They are the most representative mammalian expression system in genetic engineering vaccine research and constitute the most extensively used and successful cell line for expressing exogenous proteins. Over 70% of protein-based drugs on the market preferentially utilize CHO cells for manufacturing. The latter originates from human embryonic kidney cells. Due to their high transfection efficiency, they are suitable for producing lentiviruses that deliver therapeutic nucleic acids or small nucleic acids.

Cell culture media provide the environment for cell growth and are therefore essential raw materials in the research, development, and manufacturing stages of biopharmaceuticals. They are widely used in human and veterinary vaccines, protein and antibody therapeutics, and cell and gene therapy products. Specifically, in the production of biological products such as viral and peptide vaccines, recombinant drugs like erythropoietin, antibody drugs, gene therapy agents, and cell-engineered therapeutics, selecting appropriate, high-quality culture media is critical to significantly enhancing product expression levels and reducing unit manufacturing costs. Furthermore, cell culture media are extensively applied in scientific and basic research.

According to Frost & Sullivan data, the global cell culture media market has experienced rapid growth in recent years, with a compound annual growth rate (CAGR) of approximately 11.7% from 2017 to 2021. In China, the cell culture media market has grown even faster. According to data provided by Frost & Sullivan, the market size of cell culture media in China was approximately RMB 1.52 billion in 2020, with a CAGR of 32.3% from 2016 to 2020. It is projected that by 2025, the market size of cell culture media in China will reach RMB 5.44 billion.

Similar to the upstream raw material market in most biotech sectors, China’s cell culture media market is dominated by three major importers—Thermo Fisher Scientific, Danaher, and Merck—which collectively hold over 60% of the market share. The monopoly by imported brands is particularly pronounced in the mid-to-high-end cell culture media segment used for antibody drugs, protein therapeutics, gene therapy, and cell therapy.

The reason lies in the fact that cell culture dishes have extremely high market barriers.

On the one hand, imported brands have cultivated strong brand loyalty among customers during their long-term market expansion.Due to the unique characteristics of the biopharmaceutical industry, it is difficult for new brands to break through this stickiness. Specifically, cell culture media are closely linked to drug research and development (R&D) and production, prompting customers to conduct rigorous screening before selection. On the R&D side, cell culture media directly impact the pace and success of development; on the production side, they affect manufacturing efficiency and quality. Consequently, customers tend to favor products with high brand recognition and are unlikely to switch suppliers once a choice has been made.

On the other hand, component formulation, as the foundational core technology of cell culture media, is complex and intricate.Cell culture media formulations are highly diverse and customizable, requiring specific selection based on the cell type being cultured and the expressed products. A typical formulation comprises 70–100 distinct chemical components. Since different cells have varying requirements for nutrients and cytokines, media formulations must be precisely tailored according to cellular metabolomics. Even within the same cell category, differences in the composition of synthesized drug molecules lead to variations in media component consumption, necessitating formulation adjustments based on the specific drug molecule. This further increases the complexity of media formulation. As a core proprietary technology of media manufacturers, these formulations significantly impact product quality and business operations.

Finally, there is the large-scale production process.In China, particularly during the market boom triggered by the COVID-19 pandemic, large-scale production capacity has become the core competitiveness of domestic cell culture dish manufacturers. The selection of production processes (such as raw material grinding, mixing techniques, and temperature control) directly affects product solubility, yield, and batch-to-batch stability, thereby influencing product quality. The production of powdered culture media demands high precision in grinding and blending processes to ensure that components with concentration differences spanning several orders of magnitude are uniformly added and mixed, while maintaining homogeneity during transportation and storage. Furthermore, raw material supplier management is critical; variations in raw materials from different suppliers or even different batches from the same supplier can impact cell growth outcomes. In the commercialization phase, the ability to ensure stable production and large-scale supply of culture media is a key factor influencing customer choices.

For domestically produced cell culture media to gradually replace imported brands, it is essential to possess superior formulation capabilities and manufacturing processes, while ensuring a stable supply.

According to the prospectus, Optimize has been deeply engaged in the field of cell culture media development for nearly 10 years, accumulating extensive development experience,"Outstanding capabilities in the development of chemically defined media formulations.", successfully completed the development of culture media for various cell types, mastered core technologies to enhance product expression, and achieved breakthrough progress in increasing product yield while ensuring product quality. Furthermore, it has continuously strengthened its capabilities in customized formulation development, enabling targeted proportioning based on the specific ratio and concentration requirements of culture medium components for different biologics, thereby significantly improving cell growth density and antibody expression levels.

Production Capacity and Process, Optimize has established advanced production lines for large-scale powder and liquid cell culture media, enabling mass production capacities ranging from 1 to 2,000 kg. Furthermore, Optimize continues to invest in R&D across cell culture product development, technical processes, and platform development, refining manufacturing processes for diverse media products. The company has achieved full autonomous control over technology, team, production capacity, and, most notably, the performance and quality of its culture media.

These capabilities have also helped Optimize rapidly capture market share. According to the prospectus, in 2019, Optimize’s sales revenue from culture media applied to protein and antibody drug production amounted to approximately RMB 21.54 million, accounting for 82.78% of its total revenue, with a market share of about 4.6%. It has become the leading domestic manufacturer, ranking only after three imported brands—Thermo Fisher Scientific, Danaher, and Merck. Its related products and brand have gradually gained market recognition and continue to increase their market share.

As previously mentioned, the market size of cell culture media in China is approximately RMB 4 billion. Even if domestic substitution were fully achieved, this figure would still fall far short of half the market capitalization of Optimize at the time of its IPO. In reality, market expectations for Chinese cell culture media companies are more focused on their second growth curve: biologics CDMO services. According to incomplete statistics from VCBeat, leading domestic cell culture media companies, including Optimize, Auscan, Biogene, and Bainuo, have already begun to lay out their CDMO businesses.

First, the biological drug CDMO is a much faster-growing market with an overall scale hundreds of times larger than that of cell culture media.According to Frost & Sullivan statistics, the global market size for biological drug CDMOs grew from $9.4 billion in 2016 to $18.0 billion in 2020, representing a compound annual growth rate (CAGR) of 17.6%. Driven by the launch of innovative biologics and increased drug accessibility due to biosimilars, this market is expected to maintain rapid growth, reaching $46.0 billion by 2025.

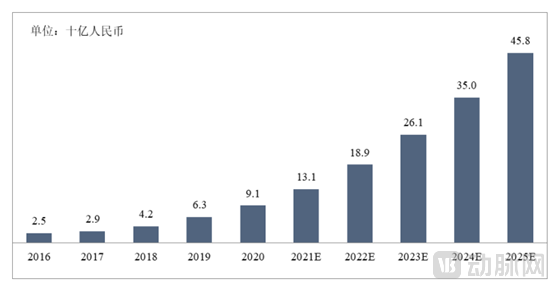

In China, the biological drug CDMO market is also experiencing rapid growth. According to statistics from Frost & Sullivan, the market size for biological drug CDMOs in China grew from RMB 2.5 billion in 2016 to RMB 9.1 billion in 2020, with a compound annual growth rate (CAGR) of 38.3%. Driven by the sustained demand for innovative drugs domestically, the market size for biological drug CDMOs in China is projected to reach RMB 48.5 billion by 2025.

China’s Biologic CDMO Market Size and Forecast (Source: Prospectus)

Secondly, cell culture dish manufacturers have inherent advantages in engaging in the CDMO business for biologics.In fact, in the earliest stages of its development, the cell culture media sector spun off from biological drug CDMO companies. Specifically, biological drug CDMOs primarily encompass cell line construction, optimization of cell culture processes, antibody expression and pilot-scale production, as well as commercial-scale antibody manufacturing and preparation—all centered on cell culture and antibody expression and spanning the entire R&D and production lifecycle of biological drugs. With the continuous iteration of cell culture media technologies, the industry has extended further downstream into outsourced services, resembling a return to its roots.

In its prospectus, Optimize confidently stated that the organic integration of cell culture media products with biologics contract development services would create a mutually reinforcing synergy. Taking protein/antibody drug development as an example, leveraging its profound understanding of culture media formulations and optimized platform processes, Optimize can develop tailored processes for different cell lines, providing customers with customized drug development workflows that significantly enhance development efficiency and outcomes—namely, higher expression titers and faster turnaround times. Meanwhile, in-house production of culture media reduces the cost of contract development services and ensures a stable supply of media.

Furthermore, for Optimize, there is an underlying logic to its expansion into the biologics CDMO sector: leveraging its foundational advantages as an upstream player in the industry chain to proactively capture service opportunities with early-stage biopharmaceutical companies.To meet the needs of upstream cell culture process development for biological drugs on their mature CDMO platform, they conduct media screening and process optimization. This approach helps identify clients during the early stages of drug development and, provided the screening results are outstanding, integrates the selected media into their projects. Throughout this process, Optimize continuously provides clients with media products and technical support, facilitating the advancement of client projects through clinical trials and toward market approval, thereby enhancing customer stickiness and deepening and broadening collaborative partnerships.

Third, although the domestic biological drug CDMO market exhibits a clear pattern of monopoly by industry giants, the concentration in the more mature global biological drug CDMO market remains relatively low.A key driver behind this competitive landscape in China’s biologics CDMO industry is the first-mover advantage. Drawing on global experience, the inherent characteristics of the biologics CDMO sector dictate that contract service providers with specific biotechnological strengths will secure a foothold in the market. For instance, companies like Optimize have won market share by leveraging their cell culture media—a core upstream raw material—to deliver differentiated services.

Of course, for domestic cell culture media companies, the biologics CDMO business is still in its early stages. Taking Optimize as an example, its biologics CDMO revenue from 2018 to 2021 was RMB 14.14 million, RMB 32.50 million, RMB 71.60 million, and RMB 84.88 million, respectively. In contrast, the top five players—WuXi Biologics, WuXi AppTec, Hepalink, GenScript, and Boehringer Ingelheim—reported biologics CDMO revenues of RMB 5.612 billion, RMB 1.037 billion, RMB 797 million, RMB 278 million, and RMB 261 million, respectively, in 2020. Clearly, there is still a long way to go. Moreover, during this process, these domestic companies will face competition from the relatively mature top five players as well as powerful biopharmaceutical enterprises, making the future market landscape undoubtedly uncertain.

Certainly, the enthusiastic response from the capital market on its first day of listing has undoubtedly bolstered the confidence of Optimize and other leading domestic cell culture media companies. Now, as they stand at a new starting line in the biologics CDMO sector, we are eager to see whether they can emerge as competitive players in the various markets that gained momentum during the COVID-19 pandemic.