Rapidly Rising in Popularity: Can Regenerative Aesthetics Replicate the Hyaluronic Acid Wealth Myth?

The pursuit of youth and beauty is endless; people not only wish to enhance their appearance but also desire to do so discreetly, placing higher expectations on the natural and long-lasting effects of medical aesthetic products.

Since 2021, three domestic medical aesthetic products based on regenerative materials have been approved for market launch in China. Offering more natural and longer-lasting results than hyaluronic acid, these products are driving the transition of medical aesthetic injections from the “filler era” into the “regenerative era,” while also meeting the urgent demands of beauty seekers. In 2022, among emerging medical aesthetic procedures, regenerative sculpting material fillers witnessed the fastest growth in popularity.

In the past, hyaluronic acid became the “dominant force” in the injectable medical aesthetics industry, thanks to its technological maturity, product diversity, cost-effectiveness, and regulatory compliance, eventually expanding into the consumer sector. Today, regenerative medical aesthetic products are rapidly gaining popularity due to their significant efficacy advantages. Can they replicate the success story of hyaluronic acid? And how high is their growth ceiling? Here is VCBeat’s analysis.

Regenerative materials are novel substances capable of stimulating the regeneration of human fibroblasts and collagen. Currently, the mainstream regenerative materials in China’s medical aesthetics industry include poly-L-lactic acid (PLLA) and polycaprolactone (PCL). With advancements in production technologies, the application scenarios of regenerative materials have gradually expanded from the medical sector to the medical aesthetics sector, driving the diversification and efficacy optimization of injectable aesthetic products.

Prior to this, PLLA-based “Baby Face Injections” and PCL-based “Girl’s Needle” had already been marketed and used for many years in overseas medical aesthetics markets. According to survey reports released by the International Society of Aesthetic Plastic Surgery (ISAPS), among injectable medical aesthetic procedures from 2016 to 2020, PLLA dermal fillers experienced the fastest growth in treatment volume globally.

In China, Sculptra and Ellansé are also leading aesthetic injectables into the “regenerative era.”

Regenerative Material Fillers See Fastest Growth in Popularity, with Three Products Already Approved

Recently, the "2022 Analysis Report on China's Injectable Medical Aesthetics Industry" released by SoYoung indicated that the popularity of regenerative material fillers is rising rapidly in the injectable sub-sector. Based on the year-on-year growth rate of orders on the SoYoung platform, regenerative plastic material fillers have seen the fastest increase in popularity, far surpassing other emerging procedures.

The surge in market heat is driven by the approval and rapid commercial launch of three domestic products.

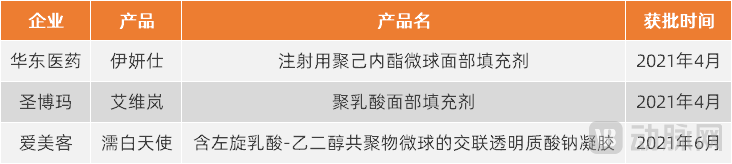

Regenerative Filler Products with Class III Medical Device Certification, Source: National Medical Products Administration

In April 2021, Ellansé, the collagen-stimulating filler under Huadong Medicine, received Class III import medical device certification from the NMPA. Prior to this, Ellansé obtained EU CE marking in 2009 and was launched in Europe. It has been used in more than 60 countries and regions worldwide for 12 years before being introduced into the Chinese market by Huadong Medicine in 2021.

In the same month, Shengboma’s Aivilan collagen-stimulating injection received regulatory approval. Leveraging its proprietary raw material—Kais® polylactic acid—and ultra-controllable degradable polylactic acid microsphere technology, the product demonstrates excellent biocompatibility and clinical safety, with no nodules, redness, swelling, or allergic reactions.

In June 2021, Imeik’s “Angel of Youth” collagen-stimulating filler received regulatory approval. This product utilizes amphiphilic microsphere suspension and dispersion technology to uniformly distribute microspheres within sodium hyaluronate gel, thereby reducing microsphere aggregation and enhancing product safety. It also provides immediate volumizing effects along with subsequent collagen stimulation.

Whether having been on the market for many years, mastering original research materials and self-developed technologies, or possessing dual efficacy, these three products each have their own characteristics. Their launch marks the entry of China’s medical aesthetics injection industry into the “Regenerative Era.”

Generated RMB 456 million in revenue, with products rapidly entering commercialization

The rising popularity of regenerative materials in medical aesthetics is also reflected in market data. Over the past year, three products have been aggressively promoted, with accelerated physician training and expanded hospital coverage.

According to Huadong Medicine’s semi-annual financial report for 2022, since its launch in August 2021, Ellansé has signed cooperation agreements with more than 500 hospitals, trained and certified over 900 physicians, and established five designated physician injection training and certification centers across China.

Sinclair Aesthetics, the operating entity under Huadong Medicine responsible for domestic medical aesthetics businesses including Ellansé, achieved RMB 185 million in revenue in 2021 and turned profitable in its first year of operation. From January to June 2022, Sinclair Aesthetics generated RMB 271 million in revenue, with sustained improvement in profitability, making it a key growth engine for Huadong Medicine’s medical aesthetics segment.

In other words, Ellansé generated RMB 456 million in revenue for its operating company within nearly one year of its market launch.

“Ru Bai Tian Shi” is a gel-based injectable product under Imeik. In the first half of 2022, revenue from this product category reached RMB 237 million, representing a year-on-year increase of 59.7%.

Although Imeik did not disclose the revenue of Ru Bai Angel separately, it stated in its financial report that the promotion of Ru Bai Angel has been smooth, with strong growth momentum, bringing new incremental growth. The company adopts a physician injection licensing authorization system, integrating physician training with an authorization framework. Its efficient and stable channel development, along with a comprehensive learning platform system, has provided first-mover advantages for the promotion of new products. Currently, Ru Bai Angel has achieved rapid penetration across first- and second-tier cities in China, reaching various types of medical institutions.

Shengboma has also accelerated the commercialization of Aivlan, its poly-L-lactic acid (PLLA) facial filler, through physician certification programs, live-streamed expert sessions, brand salons, and social media promotion. Furthermore, Nordberg Medical AB, Shengboma’s wholly-owned subsidiary in Sweden, has obtained EU CE certification for its PLLA-based facial fillers manufactured at its Swedish facility. This achievement not only grants market access to the European Union but also signifies that Aivlan has secured regulatory approval in 65 countries and regions worldwide. Additionally, Shengboma has initiated the U.S. FDA submission process to accelerate its global market expansion.

Consequently, China’s regenerative aesthetic medicine market has entered its first phase of growth, driven by global market trends and the expansion of domestic products into international markets, thereby reshaping the global competitive landscape.

Regenerative materials are also favored by investment institutions and listed companies.

In addition to Changchun Shengboma Biological Materials Co., Ltd., which already has products on the market, several other companies, including Jinkun Biotech and Pulimeng, have secured financing over the past year. Listed companies such as Sihuan Pharmaceutical and Jiangsu Wuzhong are also expanding their medical aesthetics businesses into regenerative aesthetic products. With capital support and strategic moves by major corporations, at least seven “baby face” and “girl face” injectable products are currently in the research and development or registration stages.

Selected Financing Events in the Regenerative Aesthetics Sector Over the Past Year, Source: Public Reports

Aesthetic regenerative medicine products in the R&D or registration phase, source: public reports

Overall, there are three main approaches for industry players to lay out their regenerative medical aesthetic products.

First, acquiring products or companies to directly obtain production or sales rights.

In 2021, Jiangsu Wuzhong invested RMB 166 million through a combination of capital increase and equity transfer to acquire a 51% stake in Datou Medical; through this transaction, Jiangsu Wuzhong obtained the exclusive sales agency rights for Aishuomei in mainland China.

Aishumei is a poly-L-lactic acid (PLLA) dermal filler product under South Korea’s Regen Biotech, Inc. It was launched in South Korea in April 2014, has obtained EU CE certification, and is sold in 68 countries worldwide. Prior to the aforementioned transaction, Datou Medical had already conducted in mainland China a “randomized, evaluator-blinded, active-controlled, multicenter clinical study evaluating the efficacy and safety of poly-D,L-lactic acid versus sodium hyaluronate gel for improving nasolabial fold wrinkles.”

Currently, according to Jiangsu Wuzhong’s 2022 semi-annual financial report, Aisumei has completed the preparation of all registration application materials and has submitted the registration application to the NMPA as planned.

Previously, Huadong Medicine also adopted a direct acquisition approach for its poly-L-lactic acid (PLLA) dermal filler. As early as 2018, Huadong Medicine fully acquired the UK-based Sinclair Pharma Limited for RMB 1.5 billion. Ellansé, the core product independently developed by Sinclair Pharma Limited, thus came under Huadong Medicine’s portfolio, granting the company full intellectual property rights as well as global production and distribution rights.

The advantage of acquisitions lies in the fact that products have, to some extent, been validated by the market, offering greater certainty. Whether acquiring technology, product sales rights, or an entire company, this approach enables faster market penetration and the establishment of first-mover advantages. However, this strategy places significant demands on a company’s financial resources; mastering the core technologies of the target asset requires substantial investment.

Second, leverage proprietary materials or technological advantages to conduct product research and development, as well as sales.

In addition to Shengboma, there are other companies that fall under this model.

Taking Polymon as an example, the company has established two key technological platforms: engineered preparation of biodegradable polymer raw materials and personalized processing of biodegradable medical devices. This has enabled the formation of a complete industrial chain for absorbable medical devices and the development of a product pipeline encompassing “medical consumables + consumer aesthetic medicine.” Currently, Polymon’s flagship aesthetic product, Polyren Youth Restoration Injection, is in the clinical trial phase. The product holds patents for the preparation of poly-L-lactic acid (PLLA) injectable microspheres and microparticles and was expected to receive market approval in 2023. Clinical trials have demonstrated that Polyren Youth Restoration Injection requires shorter preparation time and offers greater convenience, with smooth microsphere particles that significantly reduce the severity of inflammatory responses.

Xihong Biotechnology has overcome technical bottlenecks such as narrow-particle-size microsphere sieving and the mixing and filling of high-viscosity materials. The company possesses core technological advantages in microsphere technology development, new material modification, cross-linking technology, and gel-microsphere hybrid technology. Its "Tongyan Needle" product currently under development features uniformly shaped microspheres and a short product activation time.

In this model, companies can master core materials or technologies, thereby establishing high competitive barriers; however, uncertainties in the product development process also give rise to corresponding risks.

Third, the business expansion of hyaluronic acid giants.

Imeik’s Ru Bai Tian Shi is a typical case in point, as it also achieves the combination of hyaluronic acid and regenerative materials.

Bloomage Biotechnology also disclosed in its financial report that it will lay out R&D in regenerative materials. The R&D of regenerative materials, such as lyophilized and liquid formulations of poly-L-lactic acid (PLLA) and polycaprolactone (PCL), has been included in the company’s medium- to long-term strategic plan, with clinical studies currently underway. Meanwhile, the company plans to conduct systematic technology development, performance evaluation, and clinical research to fully confirm the safety and efficacy of its products. To support the R&D of such products, the company intends to establish an innovative technology platform for bioactive proteins and regenerative materials, integrating internal and external resources to advance technological and product innovation.

Overall, the regenerative medical aesthetics market is poised for explosive growth in the coming years as more products under development reach the market. In future competition, key drivers for expanding market share will include enhanced product safety and natural-looking results, as well as greater ease of use for clinicians.

Currently, there is no unified concept in the industry for regenerative materials in medical aesthetics. In addition to the widely recognized PLLA and PCL, other novel materials with tissue repair or regeneration-stimulating functions are being or are about to be put into application.

In 2021, Weiyimei, a lyophilized fiber product containing recombinant humanized type III collagen developed by Jinbo Bio, was approved for market launch. It is indicated for dermal tissue filling of the face to correct dynamic forehead wrinkles and represents China’s first independently developed medical device fabricated using a novel biomaterial—recombinant humanized collagen.

Historically, collagen products in domestic and international markets have been primarily derived from animal tissues. They have been widely used in clinical settings for the repair of skin, bone, cartilage, the cardiovascular system, oral and luminal tissues, as well as in medical aesthetics and plastic surgery. In contrast, the repeating units of the amino acid sequence of recombinant type III humanized collagen are identical to those of the specific functional domains of human collagen. Its functional region features a flexible triple-helix structure with an angle of 164.88°, conferring high structural stability, excellent tissue compatibility, complete absorption and utilization by the human body, and a high safety profile. Products containing recombinant type III humanized collagen exhibit cell repair and regenerative capabilities, providing barrier protection, promoting repair and regeneration, achieving hemostasis, and facilitating wound healing when applied to traumatic surfaces.

Following its approval, WeiYiMei is in the process of gradually ramping up sales volume. According to Jinbo Bio’s prospectus, WeiYiMei generated RMB 28.42 million in revenue in 2021. Based on a unit price of RMB 1,133, approximately 25,000 units were sold.

In 2022, Sihuan Pharmaceutical and Bluepha Microbiology entered into a collaboration and established a joint venture to jointly develop polyhydroxyalkanoate (PHA) microspheres and bio-manufacturing-based regenerative medicine materials, covering product R&D, regulatory filings, and subsequent commercialization.

It is understood that PHA is an intracellular polyester synthesized by microorganisms. It exhibits excellent biocompatibility with cells in vivo, and its final degradation products are carbon dioxide and water, which are non-toxic to cells. Cells can grow well on scaffolds made of PHA; therefore, PHA has broad applications in the medical field. Medical devices made from PHA, such as surgical sutures and absorbable surgical membranes, have received FDA approval for market entry in the United States. Whether in terms of entering the highly scarce light medical aesthetics market as a new material or regarding the inherent safety of the material itself, PHA holds considerable promise. Technologically, it is regarded as the next generation of regenerative materials following PLLA and PCL.

Furthermore, there are products on the market based on materials such as demineralized bone matrix and acellular dermal matrix that primarily feature regenerative functions.

If these materials or products can achieve safety and efficacy that are verifiable in both clinical and market settings, they will, together with Ellansé and Sculptra, jointly expand the market space for regenerative medical aesthetics.

As previously mentioned, regenerative aesthetic products offer numerous advantages over hyaluronic acid. The process of gradually stimulating collagen regeneration results in more natural and longer-lasting filling effects. Given these clear advantages and the continuous pipeline of subsequent products and technologies, can regenerative materials replicate the “beauty-creating” and “wealth-generating” myth of hyaluronic acid?

Dongxing Securities’ industry research report posits that regenerative materials are in the early stage of market growth. Regenerative injectables hold relative advantages in natural appearance and longevity, and their mass production as synthetic materials is assured; they are expected to capture a certain market share by leveraging these benefits. The terminal market size for regenerative injectables is projected to reach approximately RMB 11.2 billion by 2025, compared with RMB 39.1 billion for hyaluronic acid fillers.

The regenerative injectables mentioned in the above report primarily refer to PCL-based “Girl’s Needle” and PLLA-based “Youthful Face Needle.” If freeze-dried fiber filler products containing recombinant humanized type III collagen are included, and as more regenerative materials are applied and more new material-based products gain regulatory approval for market launch, the end-user market size of medical aesthetic regenerative products is expected to expand further.

As for replicating the “hyaluronic acid” myth, regenerative materials still have a long way to go and must overcome multifaceted challenges.

First, at the technical level, the functionality requires further optimization.

“Regeneration” is a double-edged sword for this product: while it promises longer-lasting effects, it also carries the risk of irreversible consequences. If patients are dissatisfied with the post-injection results, the material’s resistance to dissolution or complete removal may lead to long-term, irreversible damage.

Therefore, next-generation regenerative products that combine the material properties of slower passive degradation and faster active degradation would be more attractive.

Secondly, at the product level, compliance must be strengthened.

Currently, the reason why there are only three widely recognized and heavily promoted injectable products based on regenerative materials in the market (or four if Jinbo Bio’s Weiyimei is included) is not because regenerative medical aesthetics is a completely new concept, but because these products have obtained Class III medical device certifications, with indications that include wrinkle correction in corresponding facial areas.

Meanwhile, some products based on regenerative materials are being used for anti-aging filler injections despite either lacking Class III medical device certification or having indications that do not include correction of facial wrinkles. Should risks arise with these products, they could negatively impact the overall development of the industry.

Furthermore, emphasize product diversification and differentiation, including factors such as applicable anatomical sites and pricing.

After years of development, the hyaluronic acid market now offers products for multiple anatomical sites at various price points, catering to a broad consumer base; its applications are even expanding into the consumer sector.

Currently approved regenerative medical aesthetic products primarily target nasolabial fold wrinkles and dynamic forehead wrinkles. Future new products could be positioned for filler applications in other anatomical areas, thereby expanding penetration among aesthetic seekers while avoiding intense competition (“involution”) in the same treatment zones. Meanwhile, the terminal prices of current regenerative medical aesthetic products are generally high, with compliant products typically priced at approximately RMB 13,000–18,000 per syringe. Whether future product development can incorporate a multi-tiered pricing strategy to broaden application scenarios will also determine the potential for further expansion of market share.

Overall, the rapid rise of regenerative aesthetic products offers consumers an alternative for “subtle enhancement,” while providing the industry with new growth opportunities as the hyaluronic acid market becomes increasingly saturated. The commercialization and mature application of new materials and products will not proceed without challenges; nonetheless, all stakeholders must prioritize safety above all else in every innovation.

References:

Dongxing Securities: Aesthetic Medicine Dermal Fillers—Investment Opportunities from the Perspectives of Development Pathways and Life Cycles

Li Bin of Regi: The Crossroads of Regenerative Aesthetic Medicine Products