Orthokeratology Lenses Surge in Popularity as Top-Tier Investors Back Rising Chinese Players

Autek China

Rigid Gas-Permeable Contact Lens Manufacturer

Eyebright Medical

Ophthalmic Medical Product R&D Provider

During the summer vacation, Mr. Liu from Chongqing picked up his daughter’s orthokeratology lenses and posted on his WeChat Moments: “First time getting orthokeratology lenses; my daughter feels the world is much clearer.”

To his surprise, parents of children his daughter’s age flooded his WeChat Moments with comments, sharing their experiences with orthokeratology lenses. Previously, Mr. Liu had assumed it was a niche product, until a doctor recommended fitting his 11-year-old daughter with the lenses and he discovered how widespread their use had become among children in his community.

Indeed, as myopia prevention and control assume growing importance, orthokeratology lenses, one of the three major mainstream interventions, are seeing rapidly increasing penetration rates, with domestic brands also accelerating their sales volume. In a market worth tens of billions of yuan, product innovation and commercialization efforts are gaining momentum.

During the recently concluded summer vacation, optometry clinics at ophthalmic medical institutions experienced their traditional peak season, with orthokeratology lenses emerging as the “top-tier” product.

“From fitting and lens collection to achieving therapeutic effects, the process takes a considerable amount of time; patients also need to invest time in learning how to insert, remove, and care for the lenses. As holidays offer relatively ample time, this has led to a surge in demand during winter and summer vacations,” Kuang Yi, Chief Physician and Vice President of Chongqing Aier Eye Hospital & Optometry Hospital (Aier Eye Hospital Group), told VCBeat. He noted that during this year’s summer vacation, the number of patients undergoing screening for orthokeratology (Ortho-K) lens fitting at the hospital increased by 20% compared to the previous year, with some excluded due to unsuitable ocular conditions. Overall, the proportion of Ortho-K lens wearers among all spectacle wearers rose by 10% year-on-year.

In fact, orthokeratology lenses had already demonstrated a rapid growth trend prior to this, with corporate revenue data serving as important evidence.

Eyebright Medical’s Purotong orthokeratology lenses have seen continuous volume growth and maintained rapid expansion since their market approval in 2019. In the first half of 2022, revenue from Purotong orthokeratology lenses reached RMB 75.93 million, representing a year-on-year increase of 71.7%, significantly higher than the company’s overall revenue growth rate of 32.33%. In 2021 and 2020, the product’s revenue achieved high growth rates of 159.5% and 479.6%, respectively.

In 2021 and 2020, Autek China’s DreamVision orthokeratology lenses generated revenues of RMB 670 million and RMB 522 million, respectively, representing year-on-year growth of 28.5% and 19.2%. In the first half of 2022, revenue reached RMB 346 million, a year-on-year increase of 3.8%, with growth slowing due to the impact of the pandemic.

In 2022, new orthokeratology lenses were added to the domestic market: Shidajia orthokeratology lenses were launched, and Tian Tong Medical and Menicon’s orthokeratology lens products received approval. The number of approved products has now increased to 14.

NMPA-Approved Orthokeratology Lens Products, Source: NMPA Official Website

Based on feedback from medical institutions regarding the peak demand for glasses during the summer vacation, revenue from orthokeratology lenses is expected to grow further in the second half of the year.

With the continuous approval and market launch of products, coupled with surging end-user demand, the penetration of the orthokeratology lens market has continued to expand in recent years. According to a research report by Haitong Securities, the current penetration rate of orthokeratology lenses in China is approximately 1.6%. This figure represents a significant increase from the less than 1% recorded a few years ago.

Despite the increase in penetration rate, multiple research institutions have pointed out that compared to the 5%-10% penetration rates in European and American countries as well as neighboring Asian nations, there is still significant room for growth in China's orthokeratology lens market.

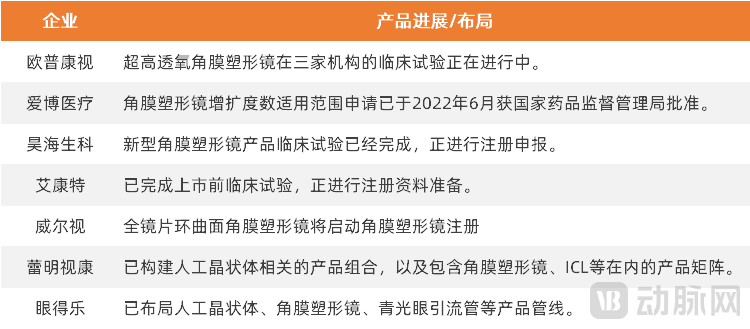

As a result, a wave of companies has been actively investing in the research and development of orthokeratology lenses or upgrading their existing products; domestic brands, in particular, are making rapid strides to catch up.

A diverse product portfolio means more choices for doctors and patients, as well as intensified competition for companies. Differentiated positioning has become a fundamental principle in product development. Overall, companies are primarily differentiating themselves through indications for use, design, and materials.

R&D Upgrades and Product Portfolio Strategies for Orthokeratology Lenses at Select Companies, Source: Public Reports

First, the expansion of the applicable range of diopters.

Currently, marketed orthokeratology lenses are primarily indicated for myopia up to -4.00 D, with a few products covering up to -5.00 D. Prior to Eyebright Medical’s expansion of the diopter range for its PurnoTone orthokeratology lenses, only Autek China’s DreamVision orthokeratology lenses were indicated for myopia up to -6.00 D.

In June 2022, Eyebright Medical’s application to expand the indicated diopter range for its product was approved. According to the medical device registration information published by the National Medical Products Administration (NMPA), the applicable range has been expanded from the previous -1.00 D to -4.00 D to include patients with myopia between -4.00 D and -6.00 D, with-the-rule astigmatism not exceeding 1.75 D, and against-the-rule astigmatism not exceeding 1.50 D. For these patients, the product can provide temporary visual correction to a certain extent; however, the degree of correction depends on the corneal deformability of the patient, and complete correction may not be achieved in some cases.

Expanding the diopter range means covering more patients, which enhances product competitiveness for companies and contributes to increased penetration rates for the industry.

In terms of design, improvements are made with personalization and comfort as the primary considerations.

The reshaping effect of orthokeratology lenses is achieved through their specialized design; the design approach determines the corrective efficacy, wearing comfort, and other factors.

“Although orthokeratology lenses are customized based on patients’ ocular examination parameters, in practice, individual patients report varying levels of comfort with the product; for the same brand, some users find them comfortable while others provide only moderate feedback. This is related to individual patient differences and the degree of myopia,” said Kuang Yi.

Therefore, designs aimed at personalization and enhanced comfort are becoming increasingly important.

For instance, Aikangte’s orthokeratology lenses feature a more novel and unique design compared to current VST and CRT designs, striving to provide patients with a better wearing experience.

Wellsee has designed full-lens toric orthokeratology lenses that can simultaneously correct myopia and variable astigmatism; its personalized alignment zone design enhances fitting success rates and patient wearing comfort.

In terms of materials, proprietary materials continue to achieve breakthroughs.

In the past, orthokeratology lenses in the Chinese market were predominantly imported products, and domestic brands also relied mainly on imported materials. In recent years, domestic brands have been making breakthroughs in material self-sufficiency, enhancing their competitiveness from the source.

Haohai Biological Technology acquired Contamac in 2017. As one of the world’s largest independent manufacturers of ophthalmic materials, Contamac supplies raw materials for ophthalmic products, such as intraocular lenses and orthokeratology lenses, to customers in more than 70 countries and regions worldwide. Currently, Haohai Biological Technology is leveraging its independently developed optical design system to develop new orthokeratology lens products based on Contamac’s high-oxygen-permeability materials. The clinical trials have been completed, and the company is proceeding with regulatory registration filings.

Eyebright Medical previously procured materials from Contamac; however, it initiated independent material R&D in 2017 and conducted comparative testing against externally sourced materials, meeting the standards for consistency evaluation. After its self-developed materials received regulatory approval in 2020, Eyebright Medical gradually introduced them into production, progressively replacing the externally purchased material blanks. In August 2022, during an investor survey, Eyebright Medical stated that all material blanks for its orthokeratology lenses had been fully transitioned to in-house production.

Recently, Autek China disclosed during an investor survey that its self-developed lens material has passed full-performance testing and biological evaluation by the Testing Center of the National Medical Products Administration. The company is currently establishing a standardized production workshop, which will enable partial use of in-house raw materials upon completion, thereby reducing costs.

“For domestic brands, achieving self-sufficiency in raw materials is an urgent priority,” said Lu Jing, Head of the Medical Division at Aikangte. He emphasized that a mindset focused on developing domestic alternatives should be applied to design, manufacturing processes, and other aspects. Currently, Aikangte’s orthokeratology lens products still utilize mainstream imported materials; however, the company has established a dedicated R&D team to actively pursue the development of proprietary raw materials and has already made significant progress.

After a product is launched into the market, service capability will also become one of the dimensions for differentiated competition among enterprises.

The complex and time-consuming fitting process for orthokeratology lenses tests the service efficiency of terminal institutions.

In Lu Jing’s view, manufacturers of orthokeratology lenses should not merely supply products to medical institutions but also deliver comprehensive services. This includes developing digital tools to enhance fitting efficiency, establishing training systems to support talent development at medical institutions, and striving to provide diverse solutions through a multifaceted product portfolio.

“Currently, the penetration rate of orthokeratology lenses is relatively high in provincial capital cities. Moving forward, if the market expands to lower-tier regions, manufacturers will need to possess the service capabilities required for these markets,” said Lu Jing. She added that if qualification requirements for fitting and prescribing orthokeratology lenses are relaxed in the future—allowing independent optometry clinics or vision care centers to obtain such credentials—the diversification of business formats will necessitate that manufacturers establish professional teams to collaborate with distributors in serving end-user institutions. “Undoubtedly, service capability will become one of the key competitive advantages for manufacturers seeking to expand their market share.”

In the field of orthokeratology lenses, two listed companies, Autek China and Eyebright Medical, have already emerged; Haohai Biological Technology’s products are also about to be approved for market launch.

In the primary market, investment institutions have focused on the upstream ophthalmology sector and are optimistic about orthokeratology lenses; firms such as Sequoia China and Qiming Venture Partners have even made consecutive investments in the same company.

Since its establishment, Aikangte has secured consecutive rounds of financing from prominent investors including Sherpa Capital, Sequoia China, Temasek, ClearPool Capital, Sanzheng Health Investment, Sinowood Capital, Honghui Fund, Yuansheng Venture Capital, Fosun, and Hengqin Jin Tou. The company focuses on providing comprehensive solutions for innovative ophthalmic and optometric devices, with a product portfolio spanning rigid endoscopes, flexible endoscopes, ophthalmic diagnostic equipment, care solutions, and innovative materials.

From an investor’s perspective, optometry and vision care represent a cross-sector domain that combines both medical and consumer attributes, with robust demand driven by consumption upgrading in recent years. The relatively high technical barriers have led to insufficient supply, thereby limiting the market penetration of high-demand products such as orthokeratology lenses. Domestic emerging brands with solid technical foundations and keen market intuition have the potential to become a vital force in meeting, and even stimulating, market demand.

In 2020, Leiming Vision Care completed a Series C financing round worth hundreds of millions of yuan, led by Hillhouse Venture Capital and participated by Chuanliu Investment and C&D Emerging Investment. In its previous Series A and B financing rounds, the company was continuously led and co-invested by Qiming Venture Partners.

Focusing on key materials to drive innovation and upgrades across various categories of high-value ophthalmic consumables, the company has developed a robust portfolio of intraocular lens (IOL) products and a diversified product matrix that includes orthokeratology lenses and Implantable Collamer Lenses (ICL). This strategic positioning is a key reason why Liming Vision Care is highly regarded by top-tier institutions.

Continuous backing by prominent institutions has not only laid a solid foundation for domestic brands of orthokeratology lenses in terms of material breakthroughs, product development, and commercialization, but also serves as one of the indicators of the industry’s high growth potential.

Survey results released by the National Health Commission of China show that in 2020, the overall prevalence of myopia among adolescents and children in China reached as high as 52.7%, with rates of 14.3% among 6-year-olds, 35.6% among primary school students, 71.1% among junior high school students, and 80.5% among senior high school students. Myopia prevention, control, and correction have become major public health issues of widespread societal concern requiring urgent attention.

Haitong Securities’ research report pointed out that, by referencing the specific myopia prevention and control targets for 2030 and drawing on Japan’s relatively mature orthokeratology lens market, assuming a penetration rate of 10%, the domestic terminal market size for orthokeratology lenses in China is expected to reach RMB 68.41 billion by 2030.

The recommended replacement cycle for orthokeratology lenses is one year; in practice, well-maintained lenses may be used for up to one and a half years, after which refitting should be performed based on individual circumstances.

“Among patients wearing orthokeratology lenses, few voluntarily discontinue use; at our hospital, some patients have been wearing them for five years,” mentioned Kuang Yi. Most patients who stop wearing the lenses do so because follow-up examinations reveal unsuitable ocular conditions, or because they enter higher grade levels with demanding academic schedules, leaving insufficient time for lens care and maintenance.

Furthermore, orthokeratology lenses require specialized care products, including cleaning solutions and protein removers, with annual costs amounting to several thousand yuan, which will also be added to the lens market size.

Overall, the orthokeratology lens market has immense potential and is poised for steady growth.

This summer vacation, orthokeratology lenses are not the only products gaining popularity. In the field of myopia control, another contact lens product has “emerged onto the scene.”

In July 2022, CooperVision’s MiSight soft hydrophilic contact lenses were launched in mainland China. MiSight is the first and currently the only soft contact lens approved by the U.S. Food and Drug Administration (FDA) to slow myopia progression in children aged 8–12 years at initial fitting. Following FDA approval in 2019, it was marketed in the United States in 2020. In 2021, MiSight received registration approval from the National Medical Products Administration (NMPA).

According to NMPA registration information, MiSight is indicated for myopia correction in phakic individuals aged 8–12 years at initial fitting, with a spherical refraction of -0.75 D to -4.00 D and astigmatism no greater than 0.75 D, who are free from ocular diseases; the recommended replacement frequency is daily.

In other words, this daily disposable soft contact lens can be used to control myopia progression in children; its distinctive feature lies in the concentric bifocal design, which allows part of the light passing through the optical zone to focus in front of the retina, creating myopic defocus with the aim of slowing changes in axial length.

CooperVision’s previously published research findings indicate that a prospective, multicenter, randomized, double-blind clinical trial of MiSight enrolled 144 myopic children aged 8–12 years across Asia, North America, and Europe. The trial quantitatively assessed the efficacy of MiSight versus single-vision daily disposable soft contact lenses in controlling myopia progression in adolescents over a three-year period.

Using the relative change in mean refractive error (cycloplegic spherical equivalent) as the efficacy endpoint, MiSight demonstrated a 59% reduction in myopia progression; using the relative difference in mean axial elongation as the efficacy endpoint, it achieved a 52% effect in myopia control.

Meanwhile, dual-focus contact lenses were well accepted by pediatric patients, with no significant impact on their daily activities—such as school activities, reading, outdoor sports, and computer use—compared to the control group. Furthermore, no significant adverse ocular events occurred during the follow-up period.

Although there are currently no studies directly comparing MiSight with orthokeratology lenses, as both are “prescription” contact lenses designed to slow myopia progression, they inevitably share areas of competition.

Compared with orthokeratology lenses, the greatest advantage of MiSight lies in its “softness.” Visually, it is indistinguishable from conventional soft contact lenses, resulting in higher psychological acceptance and faster adaptation among children.

However, although MiSight has provided extensive research data, limitations remain. To further evaluate the long-term safety and efficacy of the product in the Chinese population, CooperVision needs to conduct post-marketing clinical follow-up studies in China, using parallel controls with conventional soft hydrophilic contact lenses already on the market. The sample size must be sufficient to provide adequate data for evaluation. The endpoints of the follow-up study include, but are not limited to, patients’ visual perception, adverse events, stability of refractive error after discontinuation of lens wear, changes in axial length after three years of wear, and other factors. Additionally, attention must be paid to the incidence of infectious keratitis during the wearing period.

Meanwhile, in accordance with NMPA registration requirements, MiSight must also be fitted by licensed ophthalmologists with intermediate or higher professional titles at medical institutions, and regular follow-up examinations must be conducted.

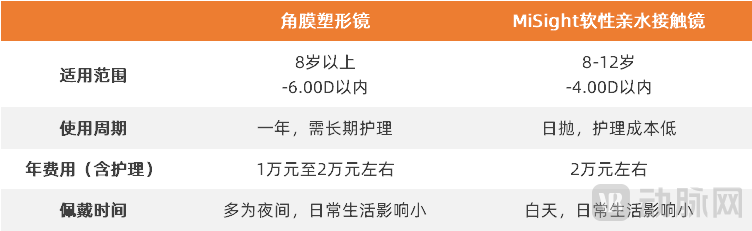

Comparison of Product Features Between Orthokeratology Lenses and MiSight

Source: NMPA, Expert Consensus on the Fitting Process of Orthokeratology Lenses (2021), and public reports

Based on the comprehensive comparison in the figure above, MiSight and orthokeratology lenses each have their own advantages in terms of scope of application, convenience of care, and cost. Overall, MiSight undoubtedly provides a new option for myopia control in children. However, due to its relatively short time on the market and limited target population, whether the product can achieve rapid widespread adoption in the short term remains to be seen, given considerations of safety and efficacy. Therefore, it may not necessarily pose a significant impact on the orthokeratology lens market.

In the long run, orthokeratology lenses still have a long way to go, especially for domestic brands.

Following its FDA approval and launch in the United States, MiSight quickly targeted China as its next market, further underscoring the emphasis multinational ophthalmic giants place on the Chinese market. Meanwhile, imported orthokeratology lenses from brands such as Menicon have continued to enter the domestic market over the past two years.

In the future, competition will intensify both within the orthokeratology lens sector and against similar products. It is worth considering whether domestic brands need to further diversify their myopia control product portfolios beyond orthokeratology lenses to capture market share as quickly as possible.