MGI Tech Surges 22% on Market Debut as China's First Domestic High-Throughput Gene Sequencer Manufacturer Eyes Global Disruption

MGI

Gene Sequencing Instruments and Related Reagent & Consumables R&D Manufacturer

On September 9, after much anticipation, MGI, the leading domestic manufacturer of gene sequencers, officially listed on the STAR Market of the Shanghai Stock Exchange. With an offering price of RMB 87.18 per share, its stock surged more than 22% at the open, pushing its market capitalization above RMB 40 billion.

MGI, established in 2016 and initially spun off from BGI, a pioneering enterprise in China’s gene sequencing sector, is built upon core gene sequencing technologies introduced at an early stage. It focuses on the research and development, production, and sales of instruments, equipment, reagents, and consumables in the fields of life sciences and biotechnology. MGI is the only company in China and one of only three companies worldwide with the capability for mass production of high-throughput gene sequencers.

Born with a silver spoon and anchored in the crown jewel of genetic technology, MGI has been a star project in the primary market since its inception, enjoying strong favor from capital. It has been accompanied all along by a host of renowned investment institutions, including IDG Capital, CITIC Securities, Jinshi Investment, Sinopharm Capital, CPE, China Renaissance New Economy Fund, Guofang Capital, Huatai Zijin, Taixin Capital, Shanghai Sailing, CDH Investments, Shanghai Dingfeng, Guotai Junan Venture Capital, GF Xinde, and Dongzheng Capital.

However, in reality, it is not an easy decision for investment institutions to invest in such a high-end instrument manufacturer.

A project lead at IDG Capital told VCBeat that in 2019, Wang Jian, founder of BGI Group, led a team to visit them, and one PowerPoint slide left a deep impression. During the discussion, Wang Jian started from the microscopic scale, moving from DNA and RNA to proteins and embryos; from newborns to the elderly; and from molecules to cells, then to organs and the life cycle of individuals—birth, aging, sickness, and death. He emphasized the necessity of developing life science tools and highlighted the importance of China mastering these tools for the advancement of the life science and technology industry. “What was originally scheduled as a one-hour lunch meeting extended to nearly three hours.”

Subsequently, the IDG team began a systematic assessment of MGI’s feasibility. For this financing deal, they conducted three to four times the number of interviews typically carried out for other projects, speaking not only with MGI’s senior executives, downstream customers, competitors, and domestic and international experts, but also with MGI’s distributors and customers in other global markets, including South Korea, Spain, and India. The team’s final research conclusion was that MGI’s products are highly reliable and that its patent protection is robust. “Based on this, we concluded that MGI is poised for rapid growth in overseas markets in the future,” said the person in charge.

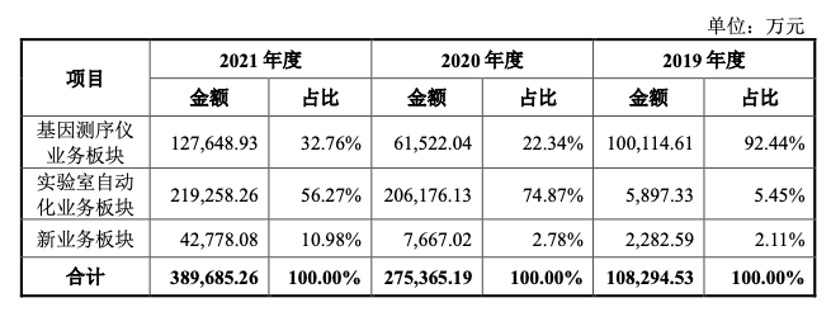

Since its establishment, MGI has rapidly launched a series of independently developed gene sequencers, gradually breaking the long-standing monopoly of imported brands in the upstream segment of the genomics industry chain despite the intellectual property barriers erected by industry giants. Regarded as a flagship domestic brand in the cutting-edge field of life science tools, MGI has also expanded into laboratory automation, driving steady revenue growth.

With its post-IPO status, MGI will undoubtedly possess stronger capital strength and greater brand influence. How it will reshape the global genomics market landscape is certainly more worth anticipating.

Gene sequencing is one of the most high-profile innovative technologies in cutting-edge science and clinical applications, and it is also a technology that has spawned numerous lucrative market segments.

Specifically, gene sequencing refers to the process of determining the order of DNA bases using sequencing equipment to decipher the genetic code of DNA, thereby providing guidance for life science research, clinical diagnosis, and treatment.

Embedded within the human genome is a wealth of critical information related to human disease and health. For instance, abnormalities in the 2,057 genes located on chromosome 1 may trigger more than 350 diseases, including Parkinson’s disease, Alzheimer’s disease, intellectual disability, and cancer. The 1,080 genes on chromosome 3 are closely associated with olfaction, inflammatory processes, and clear cell renal cell carcinoma, the most common type of kidney cancer. Meanwhile, variations in chromosome 21 can lead to Down syndrome, the most prevalent chromosomal disorder in humans.

It is precisely for this reason that gene sequencing technology has been rapidly adopted and iterated, giving rise to a vast industry chain in a very short period. This chain comprises upstream sectors focused on gene sequencers and their consumables, midstream sectors providing sequencing and data services, and downstream sectors applying these technologies in research and clinical settings. According to Illumina’s projections, the global genetic testing market exceeds $20 billion.

At present, the primary downstream application scenarios for gene sequencing are clinical testing and research services. Among these, gene sequencing projects that directly serve clinical practice constitute the mainstream, fostering multiple application markets valued at tens of billions or even hundreds of billions of yuan. Specifically, reproductive health and oncology represent the two most mature and widely adopted areas in clinical gene sequencing applications.

Let us begin with reproductive health. In this application scenario, the core product is non-invasive prenatal testing (NIPT), specifically non-invasive genetic testing for fetal chromosomal aneuploidy. This represents a major breakthrough in prenatal detection technologies for fetal chromosomal abnormalities and marks the first commercialized application of next-generation sequencing (NGS) technology in clinical practice. This product sequences cell-free fetal DNA found in maternal blood, assisting clinicians and patients in the early assessment of whether the fetus is affected by chromosomal aneuploidy-related disorders.

Beyond this, the application of gene sequencing technology in fertility scenarios is continuously expanding. For instance, in assisted reproductive technology, genetic screening is performed on embryos created through in vitro fertilization prior to uterine transfer. By selecting embryos without chromosomal abnormalities for implantation, the pregnancy success rate of in vitro fertilization (IVF) procedures is enhanced.

Secondly, its application in oncology. The various precision diagnosis and treatment scenarios associated with the entire lifecycle of tumors represent both the most fiercely contested “red ocean” and the vastest “blue ocean” for the clinical application of next-generation sequencing (NGS). Specifically, tumor gene sequencing applications include companion diagnostics, early detection and screening, and recurrence monitoring, among other scenarios. Compared with traditional clinical screening or diagnostic methods, the greatest advantage of NGS technology lies in its higher precision, enabling the capture of more subtle changes and differences.

Among these, companion diagnostics are a significant product of the transition of oncology treatment into the precision era of targeted and immunotherapies. For instance, cancer immunotherapies represented by PD-1/PD-L1 inhibitors have achieved superior clinical outcomes compared to traditional therapies; however, only approximately 20%–40% of patients respond to immunotherapy, necessitating the use of companion diagnostics. In this context, next-generation sequencing (NGS)-based tumor companion diagnostics can simultaneously detect specific genomic regions, rapidly identify complex variants, and provide more precise solutions for clinical diagnosis and treatment planning.

Early diagnosis, screening, and recurrence monitoring represent emerging application areas for next-generation sequencing (NGS) technology in oncology diagnosis and treatment, with commercialization and product development efforts gaining momentum across the industry. For patients with early-stage or potential tumors, non-invasive assays of biomarkers such as circulating tumor DNA (ctDNA) methylation enable early detection of lesions, facilitating timely follow-up and intervention. For postoperative cancer patients, long-term and effective monitoring of disease progression is particularly critical; however, existing methods suffer from low sensitivity and specificity, as well as poor predictive capability for early warning. In contrast, biomarkers like ctDNA have short half-lives and high sensitivity, allowing real-time reflection of dynamic tumor changes, and are increasingly being adopted in clinical practice.

According to Frost & Sullivan, the market size of next-generation sequencing (NGS) applications for oncology in China increased from RMB 700 million in 2016 to RMB 4.1 billion in 2021, representing a compound annual growth rate (CAGR) of 41.1%. The market is projected to reach RMB 14.9 billion by 2025 and RMB 49.1 billion by 2030, maintaining a trajectory of rapid growth.

In addition, within the overall application market for gene sequencing technology, scientific research services catering to users such as research institutions, pharmaceutical companies, contract research organizations (CROs), and third-party laboratories account for approximately 30% of the market. While competition in this segment is exceptionally fierce, sustained growth has been maintained due to its status as an essential demand for life sciences research and continuous increases in national-level investment. Meanwhile, gene sequencing technology is being progressively applied across multiple fields, including forensic identification, environmental pollution control, biodiversity conservation, and agricultural and livestock breeding.

Over the past few years, surging demand in the midstream and downstream segments of the gene sequencing industry chain has made gene sequencers the most sought-after tools in the life sciences field. Meanwhile, these complex, high-end instruments have increasingly become a bottleneck in efforts to reduce the cost of applying gene sequencing technologies.

The high cost of gene sequencing affects scientists, clinicians, and patients alike. This is due to both objective and subjective factors.

From an objective standpoint, gene sequencing itself is inherently expensive. On one hand, the human genome comprises vast and complex data, making complete sequencing and analysis an extremely challenging task. This data framework includes genetic maps, sequence maps, and transcript maps, corresponding to more than 6,000 genetic regions and over 52,000 DNA fragments, respectively. It was not until 2003 that scientists from six countries completed the mapping of the human genome through collaborative efforts, a project that spanned 13 years and cost more than $3 billion.

On the other hand, gene sequencing has not been widely applied for very long, and gene sequencers themselves are still in transition from elite instruments to mainstream devices. To date, four major categories of mainstream sequencing technologies have emerged based on differing principles: the well-known first-generation sequencing (Sanger method), second-generation sequencing (NGS), third-generation sequencing (SMRT single-molecule real-time sequencing), and fourth-generation sequencing (nanopore technology).

Although the generations of gene sequencing technologies are delineated by their nomenclature, they do not completely replace one another; each of the four generations has its own advantages and disadvantages. For instance, Sanger sequencing offers high accuracy but suffers from very low throughput, resulting in prolonged processing times. Next-generation sequencing (NGS) provides high throughput but features short read lengths, which may overlook certain complex variants. Third- and fourth-generation sequencing technologies boast long read lengths, thereby expanding the frontiers of genetic sequencing applications, yet their accuracy still requires improvement. Overall, each generation of gene sequencing technology is still undergoing its own optimization and iteration, and all demand a high level of professional expertise from operators. Currently, next-generation sequencing remains the most widely applied technology.

The primary subjective reason for the high cost of gene sequencing lies in the market structure, which is highly monopolized by a few industry giants. For a long period, the global gene sequencer market was dominated by three companies: Illumina, Life Technologies (acquired by Thermo Fisher in 2012), and Roche, with Illumina holding the largest market share. Data shows that, leveraging the continuous upgrades and promotion of its HiSeq series of gene sequencers, Illumina continued to capture remaining market shares, gradually establishing a dominant position. Since 2016, Illumina’s gene sequencers and associated reagents have accounted for more than 80% of the global gene sequencing market.

Consequently, midstream and downstream manufacturers have little room for premium pricing when procuring gene sequencers themselves. More critically, imported brands that monopolize the gene sequencer market tend to continuously raise the prices of proprietary reagents required for each run, aiming to maximize revenue. BGI, having deeply experienced these pains, was motivated to independently develop gene sequencers, which ultimately led to the establishment of MGI.

However, breaking the monopoly is no easy feat. According to IDG Capital, an early investor in MGI, beyond patents covering chips, reagents, and related sequencing methods, the successful commercialization of gene sequencers requires cross-disciplinary integration of multiple technologies, including chemistry, optics, mechanics, and electronics. As a highly complex and integrated scientific instrument, it demands exceptional comprehensive technical capabilities from manufacturers, which explains why only a handful of companies worldwide have achieved mass production of gene sequencers.

In fact, Wang Jian was well aware from the outset of the significant challenges involved in localizing the production of gene sequencers. He once stated to IDG Capital that he hoped to find an institution with a longer-term vision to collaborate with BGI on this endeavor, “because the path to independent research and development of life science tools is inevitably difficult, requiring long-term, patient investment and steadfast support from investors. However, once achieved, it will have a substantial impact on China’s entire biotechnology industry and even on the global development of life sciences, creating immense social value.”

Now that MGI has entered the capital market, an increasing number of gene sequencers tailored to diverse application scenarios are being launched. This development is poised to alleviate cost constraints stemming from a lack of supply diversity and will likely transform the competitive landscape of the mid- and downstream gene sequencing markets. VCBeat has previously learned that in China, a growing number of gene sequencing service providers are adopting dual-platform strategies—combining imported and domestically produced instruments—to enhance efficiency. Furthermore, as gene sequencing services become increasingly localized and integrated within hospitals, the selection of supporting sequencers is profoundly shaping future trajectories from the outset.

The fact is that MGI’s market share in the global gene sequencer market is not high.

Data show that in 2019, the global upstream market for the sequencing industry was valued at approximately $4.138 billion. Illumina held a market share of about 74.1%, with related business revenue reaching $3.068 billion; Thermo Fisher accounted for roughly 13.6% of the market, generating $563 million in related revenue; while MGI’s related revenue amounted to approximately $145 million, representing only 3.5% of the global upstream sequencing market share. According to the prospectus, MGI’s gene sequencer business segment saw only a slight increase in revenue in 2021 compared to 2019, suggesting that its market position has not undergone any fundamental change.

Nevertheless, we remain optimistic about MGI’s future momentum.

First, MGI has mastered the key technologies for the research and development and production of gene sequencers. As can be seen from the analysis in the previous section, this is a highly valuable achievement. Specifically, MGI possesses multiple foundational core technologies in the field of sequencing, represented by its signature core technology packages such as “DNBSEQ Sequencing Technology,” “Patterned Array Chip Technology,” and “Opto-Electro-Mechanical System Technology for Sequencers.” These technologies offer significant advantages in improving sequencing quality and reducing sequencing costs.

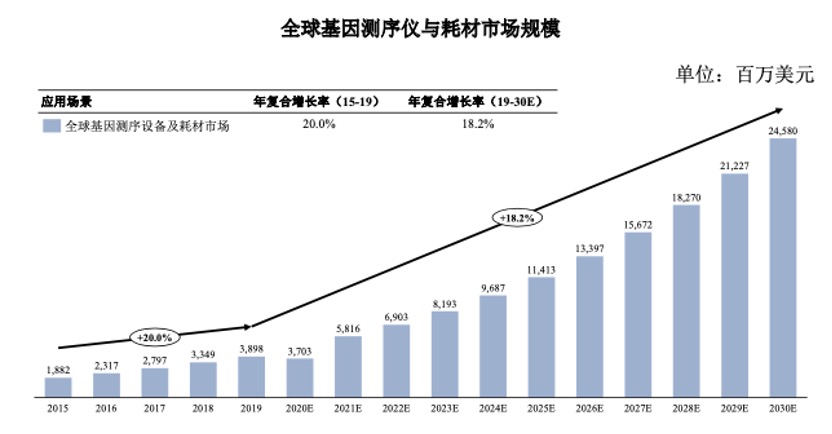

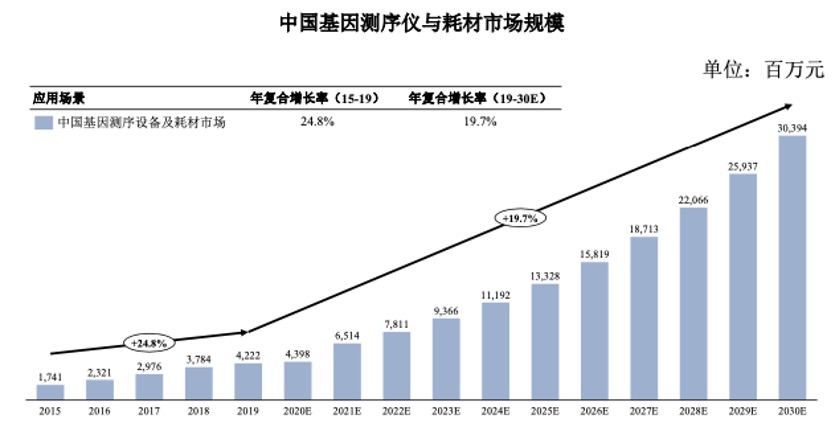

Secondly, the global market for sequencers is sufficiently large and growing rapidly, providing MGI with opportunities to capture emerging market demands. According to the prospectus, the global market for gene sequencers and consumables has maintained double-digit growth in recent years. It is projected that by 2030, the global market size for gene sequencers and consumables will reach USD 24.58 billion, while the domestic market in China will reach RMB 30.39 billion. Furthermore, as indicated by the analysis at the beginning of this article, the application scenarios for gene sequencing continue to expand, which will sustainably drive demand for gene sequencers.

Notably, in May 2022, MGI achieved a complete reversal of fortune in its patent litigation against Illumina concerning microfluidic sensor technology, securing RMB 2.2 billion in damages. Two months later, the two parties reached a settlement, under which Illumina agreed to pay the compensation to CG, a subsidiary of MGI. Furthermore, for the next three years, neither party would sue the other or their respective customers in the United States for patent infringement, violations of U.S. antitrust laws, or unfair competition, nor would they seek damages for any potential losses associated with existing sequencing platforms. Since then, MGI has aggressively expanded into mainstream overseas markets, including Europe and the United States.

Third, MGI has demonstrated the capability to respond rapidly to emerging market demands. Between 2019 and 2021, MGI’s laboratory automation business segment experienced rapid revenue growth. This was driven by MGI’s swift integration of technical resources to develop comprehensive solutions in response to the COVID-19 pandemic. The company quickly launched a series of new products, including the MGISTP-7000 Automated Tube Dispensing System and the MGISP-960 Automated Sample Processing System, while continuously enhancing the automated detection capabilities of its equipment. These efforts not only supported epidemic prevention and control but also contributed to significant performance growth.

For MGI, going public is both a milestone and a new beginning; the same holds true for China’s gene sequencing industry at this moment. We continue to look forward to gene technology providing more and better solutions to help humanity maintain health.