How Chain Pharmacies Leverage Private Domain Operations to Break Through from Retail into Integrated Health Services

Listed companies serve as bellwethers for their respective industries. In the recently released semi-annual reports, six domestic listed pharmacy chains continued to make steady progress, with a stable increase in the number of stores and revenue growth rates all exceeding double digits. These achievements were attained despite objective adverse conditions caused by the recurring pandemic, including the intermittent removal and suspension of sales of “four categories of drugs,” store closures, and reduced customer traffic.

Revenue Performance of Six Chain Pharmacies in the First Half of the Year, Data Sourced from Company Announcements

It is normal for the turbulent external environment to make the survival environment of enterprises unstable. Enterprises must respond to the uncertainty of the external market with the certainty of their business models and internal operating mechanisms. It may be worth studying how chain pharmacies cope with environmental changes to achieve such growth.

In the past, the development model of chain pharmacies relied on large-scale expansion. However, as the industry has evolved, the break-even point has been rising continuously. Due to factors such as the pandemic, many pharmacy chains have extended their break-even period to two years, whereas it previously took as little as six months. While external expansion must continue, the approach needs to shift from the previous extensive mode to high-quality growth, emphasizing endogenous growth through refined management.

VCBeat aims to decode the secrets behind the sustained high growth of pharmacy chains and identify the types of partners they currently need by analyzing the semi-annual reports of six major chain pharmacies through the lens of “people,” “products,” and “places.”

“In the past, there was a view that the pharmaceutical retail industry had little to fear from the internet, as customers required services when purchasing medications. However, in recent years, the development of pharmaceutical e-commerce and the services it provides have far exceeded expectations. If the traditional pharmaceutical retail sector fails to undergo transformation, its fate is self-evident,” an industry insider told VCBeat.

Among the directions of transformation, one point that all six listed pharmacy chains emphasized is private domain operations.

As the marginal benefits of internet expansion diminish and traffic dividends fade, both offline and online sectors are facing a shortage of user traffic. Future success will depend not on acquiring new traffic, but on retaining existing users—“retention” volume, which constitutes private domain traffic.

Build a Segmented Membership System

For chain pharmacies, whether through offline activities, partnerships with third-party platforms, or even their existing member base, these essentially constitute mere “traffic” rather than “retained” customers. Pharmacies need a private-domain operational system to revitalize and upgrade these users into loyal, retained assets within their private domain, thereby becoming an engine for growth. The membership system is the foundation of all this.

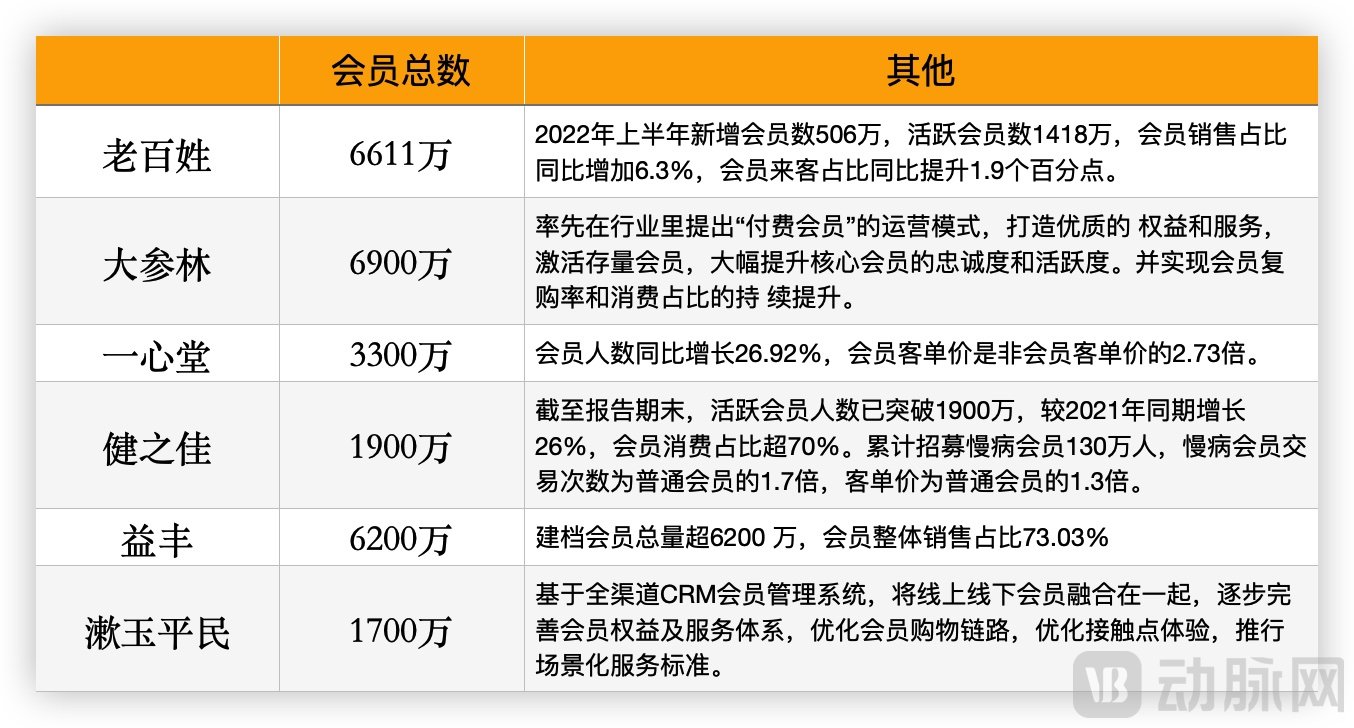

Taking the semi-annual report data of LBX Pharmacy Chain Joint Stock Company as an example, as of June 30, 2022, the total number of members reached 66.11 million, with 5.06 million new members added in the first half of the year. The number of active members was 14.18 million, accounting for 6.3% of member sales and 1.9% of member customer visits. It can be seen that member operations are still at a relatively early stage.

The establishment of a membership system is a gradual process that should revolve around four key scenarios: member acquisition, retention, engagement, and conversion. It requires implementing offline in-store advertising for member acquisition, segmenting online communities, facilitating interoperability and conversion between public and private domain traffic, leveraging digital tools for precise engagement, and ultimately achieving offline conversions.

For chain pharmacies, private domain operations entail an upgrade from traditional product-centric management to member-centric and people-centric operations.

Private domain operations refer not only to members themselves but also to their data assets, such as member profiles, demographic attributes, consumption data, and spending patterns. These data are leveraged for precise digital operations. For instance, six pharmacy chains have integrated their online stores with offline outlets through unified membership systems and designed tiered benefit structures for members. By utilizing digital tools like WeCom, these chains establish connections between members and physical stores to enable targeted operational strategies.

Membership Scale of Six Chain Pharmacies, Data Sourced from Company Semi-Annual Reports

In private domain operations, the establishment of communities is a crucial component. It serves to build intimate connections with members and unlock their value, forming the core of a closed-loop private domain ecosystem.

As times evolve, merely adding members to a group chat to disseminate promotional information or share bland marketing pitches clearly does not constitute refined operations.

Valuable communities bring together individuals who share similar value orientations (such as health needs and hobbies), consumption concepts (including price sensitivity and promotional sensitivity), and even humanistic sentiments (such as filial piety and parent-child bonding). By fostering shared goals among members and meeting their social needs, such communities can generate vibrant stickiness and achieve high-quality conversions.

Chronic Disease Management Becomes the Breakthrough Point

As the aging trend intensifies, the number of patients with chronic diseases continues to rise year by year. In the semi-annual reports of six chain pharmacy companies, chronic disease management was invariably highlighted as a key focus. For pharmacies, chronic disease management has become a significant contributor to revenue and remains a strategic area for future growth.

The six chain pharmacies also adopt different approaches to chronic disease management, with each striving to build a service model with its own distinctive features.

LBX Pharmacy Chain Joint Stock Company: “Hardware + Software + Services” Model

LBX Pharmacy Chain Joint Stock Company has deployed Bluetooth-enabled smart devices for self-monitoring of chronic conditions—including blood glucose, blood pressure, heart rate, serum uric acid, and blood lipids—across more than 6,500 stores nationwide. From 2020 to June 30, 2022, the company established health records for over 8 million individuals, facilitated more than 20 million self-testing instances, conducted over 20 million follow-up visits, and held more than 20,000 online and offline patient education sessions. These initiatives have not only helped patients with chronic diseases monitor their health indicators and improve medication adherence but also enhanced store foot traffic and customer stickiness.

Yixintang: People-Oriented, Patient Mutual Aid Model

Yixintang places people at the center of its services. By collaborating closely with renowned expert teams from public hospitals and adopting a centralized consultation model, Yixintang addresses patients’ needs for interdisciplinary, multi-disease medical and nursing care. This approach enables personalized, standardized, and collaborative chronic disease management plans. Furthermore, through a mutual-aid model, Yixintang establishes patient organizations grouped by disease type, where members supervise and support one another to jointly enhance self-management capabilities and improve quality of life.

Meanwhile, Yixintang Pharmaceutical Co.,Ltd. adopts a “five-in-one” approach to chronic disease management, integrating medication habits with behavioral patterns and incorporating internationally standardized exercise, nutrition, and psychological prescriptions. As of the end of June 2022, Yixintang had established a total of 996 in-store chronic disease health care stations across 45 branches in seven provinces and municipalities directly under the central government.

DaShenLin, Jianzhijia: Building a Specialized Chronic Disease Management System

DaShenLin, grounded in professional pharmaceutical services, has established a chronic disease management team and developed a patient-centric, full-lifecycle chronic disease management system. By prioritizing professional services to enhance patient adherence, the company has also launched a chronic disease membership benefits program. Dedicated chronic disease management specialists provide patients with services including health records, testing, safe medication information, medication guidance and follow-up, and complication management.

As of the end of June 2022, there were over 1,200 chronic disease management service personnel, nearly 1,400 chronic disease service outlets, and 20 types of chronic diseases under management.

Jianzhijia has cumulatively launched 303 stores covered by medical insurance for chronic diseases, and established a specialized network of nearly 700 chronic disease management stores targeting conditions such as hypertension, diabetes, heart failure, stroke, sleep disorders, and dermatological issues. Through training and professional guidance provided by specialized pharmacists, the company has developed comprehensive pharmaceutical care plans covering disease treatment, symptom improvement, complication management, nutritional support, and health management, along with programs for professional health knowledge training and patient education.

Subsequently, professional follow-ups on medication adherence and health consultations are conducted through the pharmaceutical management system to enhance the stickiness of chronic disease members. Currently, Jianzhijia has recruited 1.3 million chronic disease members, whose transaction frequency is 1.7 times that of regular members, with an average transaction value 1.3 times higher.

Summary

It is evident that chain pharmacies are shifting from a drug-centric to a patient-centric model. Chronic disease management has evolved from simple medication sales in the past to a comprehensive system covering patients’ entire life cycles. In addition to dispensing medications, these pharmacies now provide a range of services, including chronic disease health records, testing, safe medication information, medication guidance and follow-up, and complication management.

These services also require the participation of external enterprises.

For some pharmacies, the long-standing focus on business operations has resulted in significant deficiencies in professional services. Even when implementing a membership management system, they fail to design it around pharmaceutical care as its foundation. Such systems are ill-equipped to meet the comprehensive needs of chronic disease management.

At this juncture, a one-stop solution targeting the out-of-hospital market—spanning from pharmaceutical manufacturers to retail pharmacy terminals—would be highly attractive to pharmacies. Such a solution would not only respond promptly to consumers’ emergency and diverse scenario-based medication needs but also help pharmacies comprehensively enhance their operational capabilities across all stages, from customer acquisition and conversion to retention, by establishing an omnichannel, full-category, and refined marketing system.

From the supply-side perspective, chain pharmacies must prepare for incremental drug volumes. In their semi-annual reports, six major pharmacy chains explicitly outlined various measures to accommodate the outflow of prescription drugs from hospitals.

In recent years, the National Health Commission and the National Healthcare Security Administration have successively introduced policies to advance “dual-channel” management and establish prescription circulation centers, thereby incorporating designated retail pharmacies into the national medical insurance drug supply and guarantee system. This ensures the certainty of future separation between prescribing and dispensing, as well as the outflow of prescription drugs from hospitals.

According to the semi-annual report data of Yifeng Pharmacy Chain Co., Ltd., the sales share of retail pharmacies in the three major terminals (public hospital market, pharmacy market, and public primary healthcare institutions) has increased by 3.2% over the past few years, with prescription outflow playing a significant role in this process.

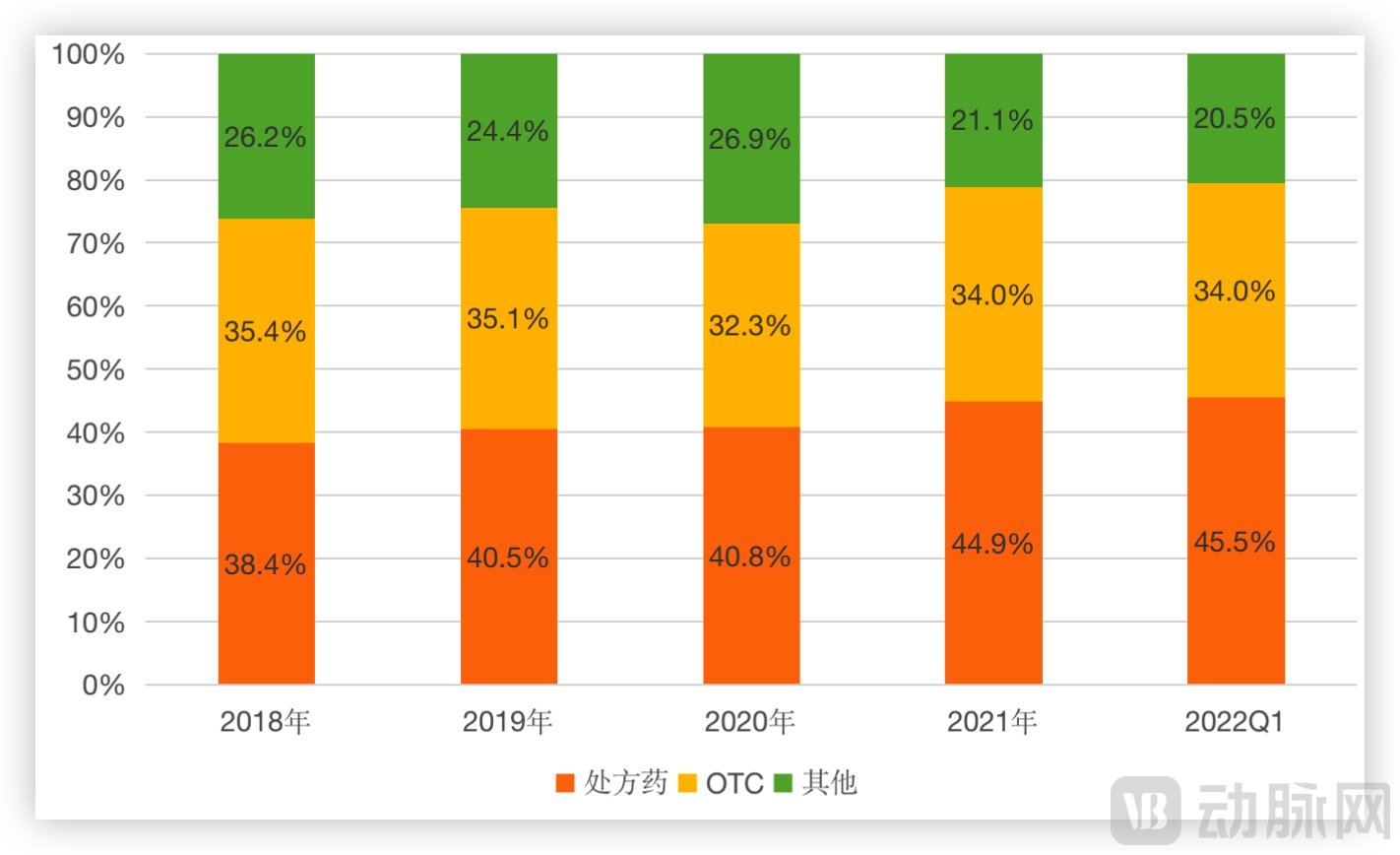

From the perspective of the retail pharmaceutical market, the proportion of prescription drugs continues to rise.

The Proportion of Prescription Drug Sales in the Retail Sector Has Been Increasing Year by Year, Data Source: Zhongkang CMH

According to data from Zhongkang CMH, the proportion of prescription drugs has been increasing year by year. In 2018, prescription drugs accounted for 38.4% of sales in China's retail pharmaceutical market; by Q1 2022, this share had risen to 45.5%, an increase of 7.1 percentage points. The share of OTC drugs remained relatively stable during this period, hovering around 34–35%.

According to IQVIA data, in 2018, the hospital-based market accounted for 71.8% of China’s prescription drug market. There remains significant room for the outflow of prescription drugs from hospitals, which will be gradually realized over the coming years. Starting in 2018, provincial-level authorities actively established prescription circulation platforms to facilitate the outflow of prescriptions.

As the circulation of drugs covered by national price negotiations and those under the “dual-channel” management policy accelerates, pharmacies will see incremental revenue growth in the short term. Pharmacies should therefore collaborate with pharmaceutical manufacturers to ensure a stable supply of these medications.

To this end, six major pharmacy chains have concurrently increased the proportion of stores located near hospitals, thereby progressively strengthening their specialized capabilities to accommodate the outflow of prescription drugs from hospitals.

Yifeng PharmacyEstablished a Strategic Leadership Group for Prescription Outflow and a Professional Prescription Drug Business Unit to comprehensively capture prescription outflow across all channels.

For offline operations, leveraging various specialized pharmacies as a foundation, we have deepened cooperation with relevant manufacturers. Currently, we carry 200 drugs included in the National Medical Insurance Negotiated Drug List and nearly 650 varieties subject to hospital prescription outflow, while having established in-depth partnerships with over 150 suppliers.

In the online sector, Yifeng Pharmacy Chain Co., Ltd. has deployed its electronic prescription services. As one of the first listed companies to integrate with Hunan Province’s Prescription Circulation Platform, it has successfully implemented the routing of electronic prescriptions to its own retail stores.

Shuyu Pingmin PharmacyIt also stated in the semi-annual report that it would continue to strengthen the development of projects such as hospital-adjacent stores, stores with “Dual Channel” qualifications, and compliant pharmacies. As of the end of the reporting period, Shuyu Pingmin had opened 57 designated special drug pharmacies for major diseases, over 270 hospital-adjacent stores, and 8 compliant pharmacies in Shandong Province, with DTP gross sales (including tax) exceeding RMB 570 million, a year-on-year increase of 84.13%.

LBX PharmacyIn the first half of 2022, hospital-adjacent stores accounted for approximately 10% of the total. There were 168 stores qualified under the "Dual Channel" policy and 151 DTP (Direct-to-Patient) pharmacies. Sales from DTP pharmacies represented about 10% of total sales, while prescription drug sales accounted for approximately 37%. Moving forward, we will further leverage the strategic layout advantages of hospital-adjacent stores, advance the acquisition of unified medical insurance qualifications for DTP pharmacies, "Dual Channel" stores, and outlets covering special outpatient and chronic disease programs, and effectively capture outbound prescription flows.

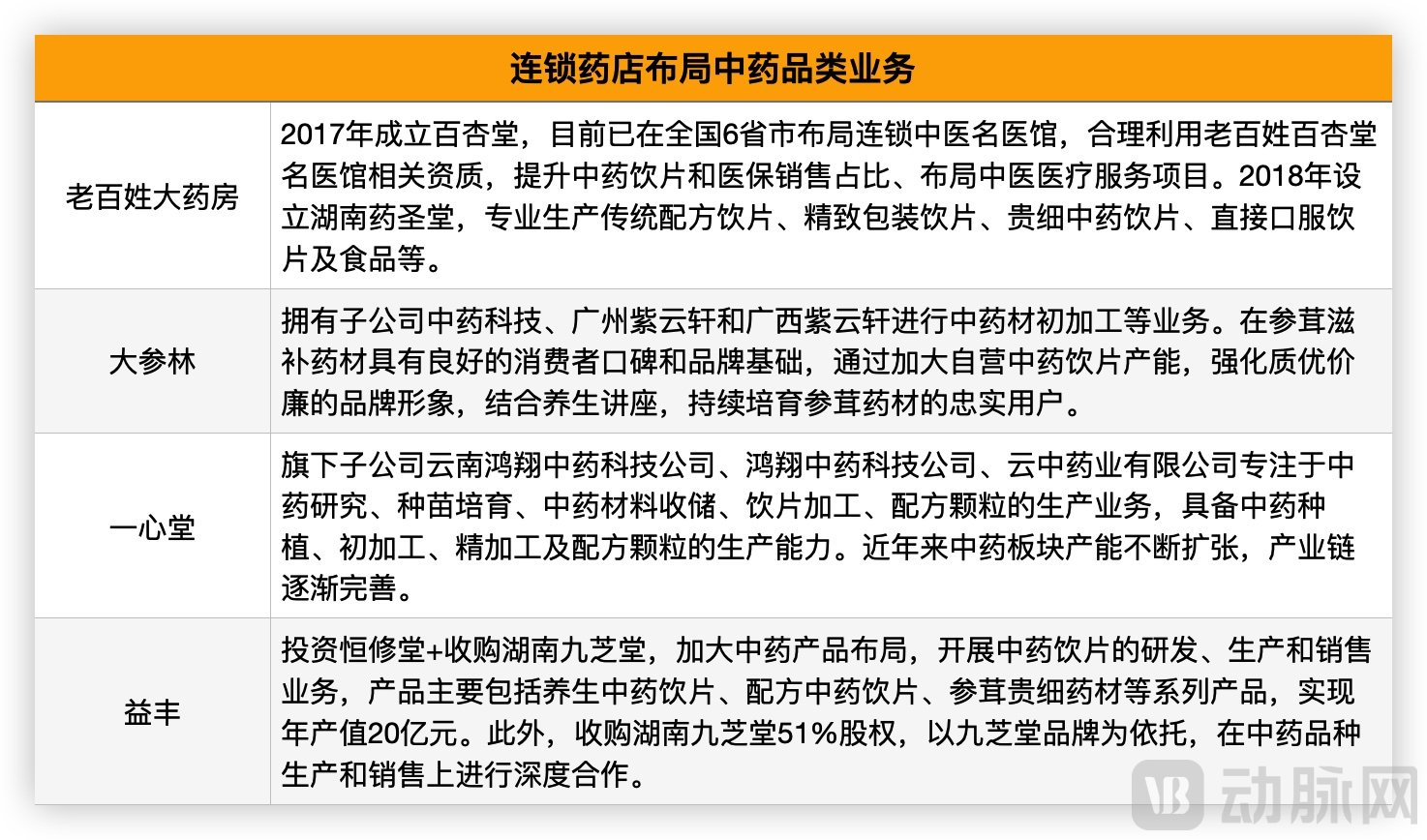

Chain Pharmacies' Layout in the Traditional Chinese Medicine Business, Compiled from Public Sources

In addition to the incremental market driven by prescription outflow, traditional Chinese medicine (TCM) products, which have relatively high gross profit margins, also represent a significant area for growth.

In recent years, multiple regions have issued policies to liberalize the sale of traditional Chinese medicine (TCM) decoction pieces in retail pharmacies. Furthermore, driven by population aging and heightened health awareness among residents, the market for TCM products is poised for further expansion, a trend that many pharmacy chains have already strategically anticipated.

Summary

Centering on the “product” element, the six major pharmacy chains have made extensive strategic arrangements in incremental markets, which have also driven revenue growth from the sales end.

As the sales volume of prescription drugs in chain pharmacies grows, the supply of prescription drugs will gradually shift from distributors to pharmaceutical manufacturers. Collaboration between pharmaceutical manufacturers and chain pharmacies with scale effects creates a win-win situation for both parties. Pharmacies can reduce their procurement costs, while pharmaceutical manufacturers can more rapidly penetrate the market, driven by the scaled store networks of chain pharmacies.

According to the prospectus of Yunnan Jianzhijia Chain Health Pharmacy Co., Ltd., in 2016, pharmaceuticals accounted for only 32.2% of sales by product category in Japanese retail pharmacies, while cosmetics represented 21.1%, and daily necessities and other products made up 46.8%. Furthermore, U.S. chain pharmacies adopted a diversified business model combining pharmacy services with convenience store offerings at an early stage, expanding their product portfolios to include health- and beauty-related items.

Therefore, drawing on the experiences of the United States and Japan, domestic chain pharmacies have been actively exploring diversified business operations.

YixintangExpand the "Yixin Convenience" business, increase promotion of lottery tickets and personal care and beauty products, and aim to attract and broaden the potential consumer base through a diversified business model. In the first half of 2022, Yixintang’s sales of personal care and beauty products covered 36 SKUs. The company focused on establishing 657 dedicated counters in Yunnan Province to promote these products. Within just six months, sales exceeded RMB 100 million.

Shuyu Civilian PharmacyFor the predominantly elderly customer base in stores, we are accelerating the online and offline deployment of age-friendly products, while also establishing dedicated online O2O zones for age-friendly products to deliver refined services within a 3-kilometer radius. For younger consumers, we are expediting the diversified layout of health snacks and imported nutritional supplements, and rapidly expanding categories such as eye-care products, small home appliances, and household cleaning supplies in the context of normalized pandemic conditions.

By establishing a dedicated zone for age-friendly products as a breakthrough point, implementing age-friendly or accessibility modifications in stores not only enhances the shopping experience for seniors but also improves the in-store experience for customers of all age groups.

In addition, multiple chain pharmacies are also exploring“Medical + Pharmaceutical + X” Integrated Business Model。

As health awareness rises, public perception of health is shifting from treating illness to preventing it. Pharmacies are increasingly exploring the integrated “medicine + pharmaceuticals + X” business model, aiming to build a comprehensive healthcare service system spanning prevention to treatment, thereby serving as a supplement to hospital-based care.

Chain pharmacies are gradually recognizing the empowering value of commercial insurance for their businesses and have begun exploring this area. For instance, the specialized pharmacy business mentioned earlier relies on third-party commercial insurance to connect pharmaceutical companies, pharmacies, physicians, and patients.

Commercial health insurance serves three primary functions for pharmacies: expanding product categories, maintaining existing customer stickiness, and promoting to attract new customers.

LBX PharmacyIn its semi-annual report, it proposed building a multi-tiered medical payment system and services comprising “basic medical insurance + commercial insurance,” exploring various cooperation opportunities with insurance companies to seek new business growth points and create a “medical care + pharmaceuticals + insurance” development model.

DaShenLinWe will actively explore the “medical care + pharmaceuticals + elderly care + diagnostics + insurance” model, providing one-stop health services through continuously innovative service formats. By assuming social responsibility, expanding our business scope, serving a vast customer base, and enhancing customer stickiness, we have entered the insurance sector through the acquisition of Shanhkang Henuo Insurance Brokerage Co., Ltd. by our subsidiary last September.

Yixintangwent even further. In the first half of 2022, third-party insurance services generated sales revenue of RMB 371 million, a year-on-year increase of 33.11%. The proportion of third-party insurance service sales to the total sales of chain stores reached 5.78%. The scale of third-party insurance services continued to maintain a growth trend.

JianzhijiaJianzhijia began laying the groundwork for a diversified community health service ecosystem several years ago. According to its prospectus, Jianzhijia’s business formats cover specialized community convenience pharmacies, convenience stores, traditional Chinese medicine (TCM) clinics, community clinics, and medical examination centers, among others. Building on its core pharmacy business, Jianzhijia has gradually explored models such as “pharmacy + convenience store,” “pharmacy + clinic,” and “pharmacy + medical examination center.” In the first half of this year, the total revenue of its convenience retail segment reached RMB 197 million.

Summary

Long-standing consumer habits have made community pharmacies a natural gateway to holistic health. How to leverage this gateway to evolve from a traditional drug-selling model into a comprehensive disease-management service model, integrate diverse business formats, and unlock a health management market larger than the pharmaceutical sector itself, is the development path currently being explored by pharmacy chains.

Taking insurance companies as an example, the presence of community chain pharmacies as a channel enables more precise reach to target customer segments. These pharmacies serve a screening function, thereby further reducing insurance sales costs.

Whether it involves refined private-domain operations, expansion of product categories, or the integrated development of multiple business formats, all rely on the support of information technology systems.

Currently, the informatization of pharmacies primarily focuses on inventory management, membership management, medical insurance processing, and product management, remaining at a relatively rudimentary stage. Such systems offer limited support in meeting the future demands of one-stop health service scenarios and digital marketing in pharmacies.

In terms of development stages, this type of information system construction represents the first step in pharmacy digitalization.

A review of the semi-annual reports from six pharmacy chains reveals that, driven by external shifts such as the outflow of prescriptions, the decentralization of medical resources, and the integration of medical and elderly care services, traditional business models and mere scale-based expansion no longer constitute the core competitiveness of pharmacy operations. Transformation is an indisputable imperative.

Whereas pharmacies historically focused primarily on drug sales, the intensifying market competition and evolving consumer habits are driving a strategic shift in enterprise development: from store-centric operations to user-centric management, from a "traffic" mindset to a "retention" mindset, and from promotional marketing to customer service. These transformations necessitate that enterprises leverage digital intelligence as a core driver, integrating their business, application, data, and technical architectures to build a digital-intelligent big health service platform tailored to their specific operational needs.

Furthermore, pharmacies must strengthen their capabilities in diversified operations and enhance deep-level service competencies, such as pharmaceutical care services, to provide consumers with more high-quality medical services. In the future, as one of the key carriers of primary healthcare resources, pharmacies will evolve into convenient health centers, offering a more diverse range of medical services.

All of this hinges on pharmacies’ transition from digitalization to digital intelligence. In this process, those who can provide comprehensive solutions will have the opportunity to capture a significant market share.

The era in which chain pharmacies could sustain rapid growth solely by “selling drugs” has passed. In the mobile internet age, driven by consumers’ rising pursuit of quality of life and the normalization of the pandemic, profound transformations have taken place in consumer mindsets, purchasing patterns, and demand.

Middle-aged and elderly populations have been compelled to rapidly complete their initiation into online shopping, emerging as a new wave of e-commerce users; brick-and-mortar pharmacies, once considered the most impregnable stronghold for e-commerce, are now grappling with declining foot traffic; meanwhile, the post-95s generation, more passionate about wellness and fitness than their elders, has transformed into the new vanguard of health-conscious consumers.

In the face of this major upheaval in the pharmaceutical retail industry, chain pharmacies are responding proactively. They have opened their doors to attract any potential partners capable of achieving win-win outcomes, leveraging their strong community penetration to connect various services with diverse populations. Although the ultimate impact remains to be seen, every exploratory effort they make is laying a solid foundation for the future development of the industry.