China's Under-9% Localization Rate Niche: Five IPOs in Three Years Signal a Rising Dark Horse in Disposable Plastic Lab Consumables

Disposable Plastic Consumables for Biological Laboratories: An Overlooked High-Potential Segment Within the Laboratory SectorDisposable plastic consumables for biological laboratories, as an important branch of the laboratory sector, have long been an overlooked high-potential segment. Most people perceive the laboratory consumables market as being in its early stages of development, with low penetration rates and a small market size. In reality, however, disposable plastic consumables have already supported multiple initial public offerings (IPOs).

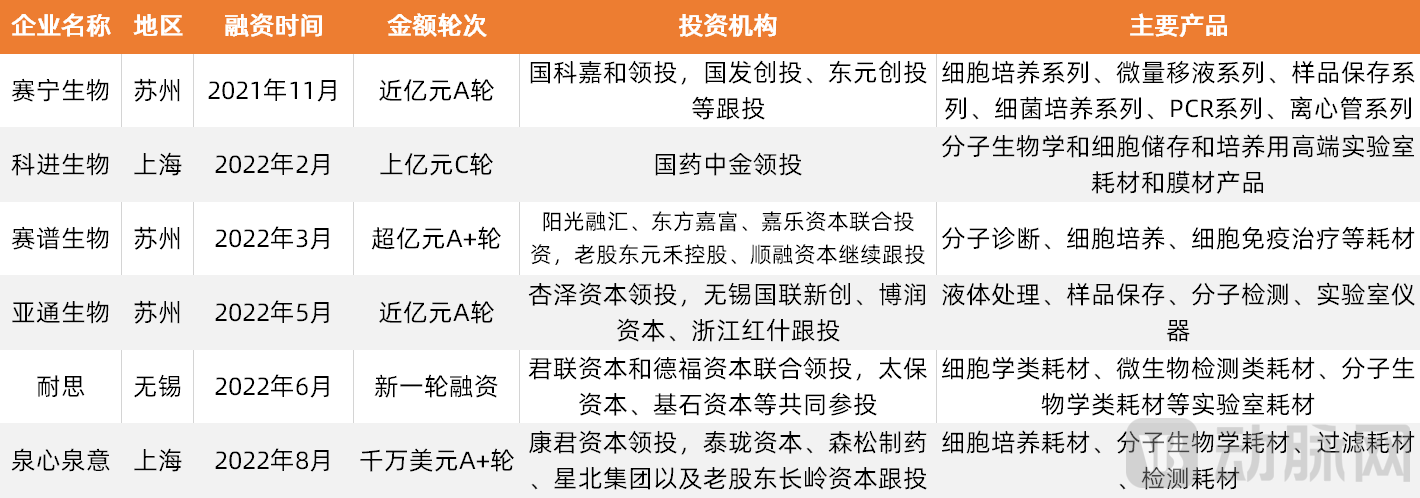

In 2020, Jet Biofil, Titan Scientific, and Gongdong Medical were listed on the Shanghai Stock Exchange; in December 2021, Kaishi Biotechnology’s application for an initial public offering (IPO) on the Shenzhen Stock Exchange was accepted; in August 2022, Shuohua Life Sciences submitted its IPO prospectus. In the primary market, several companies focused on or covering laboratory consumables, including Kejin Biotechnology, Suzhou Yatong Biomedical Technology Co., Ltd., Saipu Biotechnology, Nest Biotechnology, and Lab Direct China Limited, completed financing rounds in 2022 alone, attracting investment from numerous firms such as Legend Capital, Changling Capital, Xingze Capital, and Sunshine Ronghui Capital.

Biological laboratory consumables constitute one of the four major categories of life science services. Disposable plastic consumables represent an important subcategory of biological laboratory consumables and are widely used in experiments that demand high precision from supporting materials. Indeed, the quality and performance of disposable plastic consumables directly impact the accuracy and safety of such experiments or testing procedures.

Disposable plastic consumables have long been a critical bottleneck in China’s life sciences services industry. Due to technological limitations, the market for laboratory consumables in China has been dominated for years by international giants such as Thermo Fisher Scientific, Corning, VWR, and GE. According to data from the “2021 In-Depth Research Report on the Global and Chinese Disposable Plastic Consumables Industry for Biological Laboratories” published by Xin Si Jie Industrial Research Center, imported brands account for over 90% of the market share.

Driven by strong national support for the biotechnology industry, the continued prosperity of the in vitro diagnostics (IVD) and biopharmaceutical sectors, the rising wave of domestic substitution, and the normalization of pandemic control measures, the laboratory consumables sector is poised for sustained growth. Currently, some leading domestic companies have achieved technological breakthroughs in certain single-use plastic consumables for biological laboratories and are expected to capture greater market share in the future. In light of this, VCBeat has conducted an industry overview of single-use plastic consumables for the benefit of our readers.

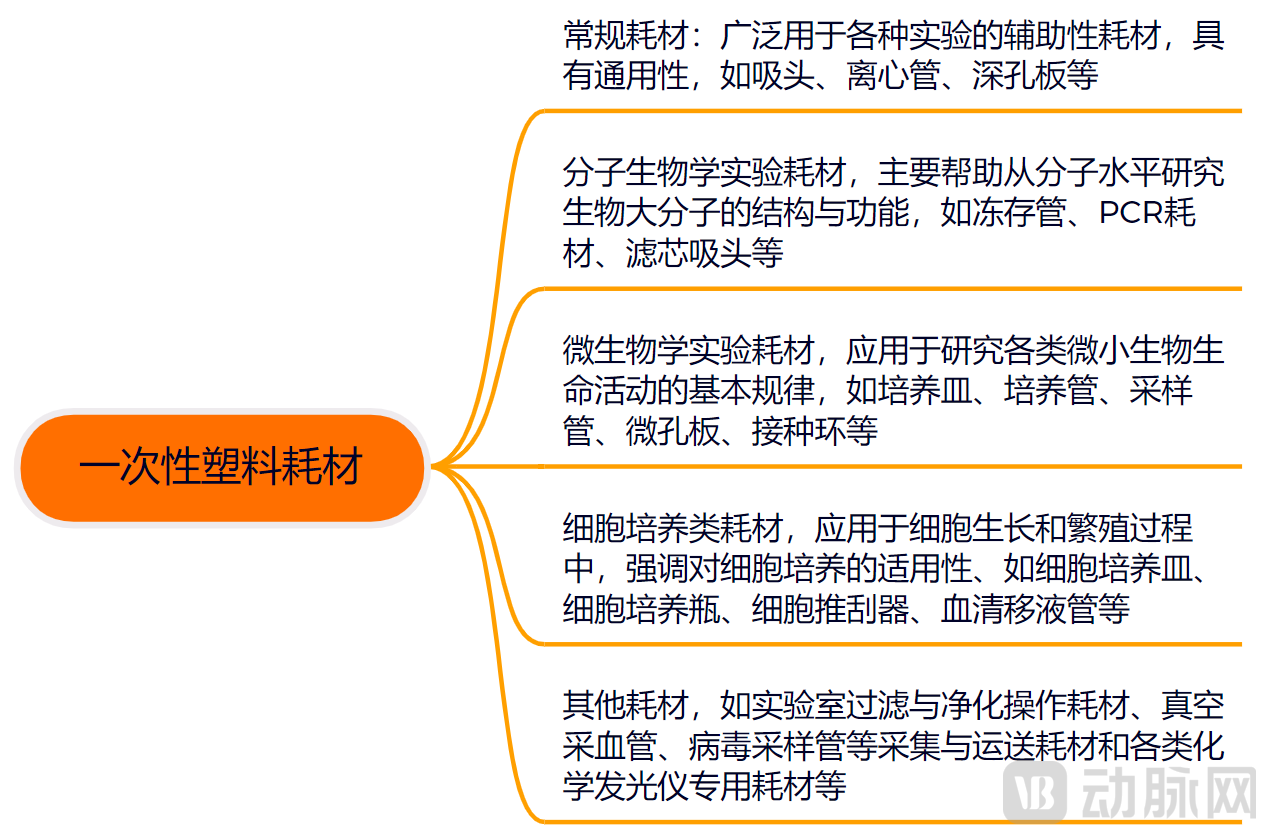

Life science services encompass four major categories: research reagents, laboratory consumables, instruments and equipment, and comprehensive services. Among these, laboratory consumables are divided into general-purpose consumables for daily laboratory use, high-end consumables for specific industrial production, and laboratory animals. This article primarily focuses on disposable plastic consumables within the category of general-purpose consumables.

Laboratory consumables are made from materials such as glass, quartz, ceramics, metals, rubber, and paper. Glassware, owing to its inherent hydrophilicity, was once widely used in laboratory settings. However, its drawbacks have gradually become apparent during use, including cumbersome cleaning procedures, risks of cross-contamination, fragility, and potential safety hazards to laboratory personnel. Since the 1960s, developed countries in Europe and America have begun replacing glassware with disposable plastic consumables.

Disposable plastic consumables are primarily made from medical-grade polymers, which offer excellent mechanical properties and chemical stability. They can be easily surface-modified to meet various specific experimental requirements, thereby enhancing production and experimental efficiency. With the advancement of laboratory consumables, disposable plastic products have gradually replaced those made from other materials.

From the perspective of the entire industry chain, the upstream segment of the disposable plastic consumables industry includes suppliers of raw and auxiliary materials such as medical-grade general-purpose polystyrene (GPPS), polypropylene (PP), and polyethylene (PE), as well as mold suppliers and equipment suppliers such as injection molding machine manufacturers. Disposable plastic consumables are primarily used for cell culture and harvesting, pipetting in biological experiments, solution filtration and separation, and storage. The downstream sector encompasses laboratories in universities and colleges specializing in biology, medicine, agriculture, and environmental science; research institutions in life sciences and medicine; centers for disease control and prevention at all levels within the public health system, inspection and quarantine agencies, and drug and food administration authorities; testing laboratories in healthcare institutions at all levels; as well as pharmaceutical companies, contract research organizations (CROs), biotechnology firms, and scientific research service providers.

Due to their first-mover, technological, and brand advantages, imported brands have long dominated China’s market for disposable plastic consumables. According to data from the New Thinking Industry Research Center, imported brands accounted for 91.5% of the total market share for disposable plastic consumables in biological laboratories in 2020.

Geng Xinrui, Head of Private Label at Lab Direct China Limited“It indicates that the laboratory consumables industry is severely undervalued. The conventional perception is that a disposable plastic consumables factory can commence operations simply by investing in molds and injection molding machines and hiring some operators. In reality, the research, development, and production of laboratory consumables require substantial investments in human resources, materials, and capital. Moreover, due to the low unit price of consumables, profitability relies on high sales volumes. Consequently, many companies are reluctant to make large-scale investments in consumables manufacturing when the market size is limited and there is insufficient external impetus.”

In China, suppliers of disposable plastic consumables were initially dominated by traders, with the vast majority of such products relying on imports. As China’s economic level has continued to rise and its biotechnology industry has flourished, specialized manufacturers of laboratory consumables have emerged.

Li Jilong, Head of Strategy at Yatong BiomedicalIt is worth noting that most Chinese manufacturers of disposable plastic consumables emerged in the early 21st century. Constrained by technological capabilities, professional expertise, and process quality, these companies initially focused on low-value consumables. With improvements in domestic technological standards, innovation intensity, and other comprehensive capabilities, some enterprises have since expanded into the high-end consumables sector. In terms of application scenarios, the initial user base for disposable plastic consumables consisted primarily of research and industrial clients. The medical sector gradually opened up to these products only after their application in other fields had become well-established.

In 2020, domestically produced single-use plastic consumables entered a harvest period. Jet Biofil and Titan Scientific were listed on the STAR Market in January and November, respectively, while Gongdong Medical was listed on the Main Board of the Shanghai Stock Exchange in September. In interviews with multiple industry insiders, VCBeat consistently received the response: “This is both accidental and inevitable.”

On one hand, this represents the culmination of over a decade of dedicated efforts in the laboratory consumables sector in China. On the other hand, the COVID-19 pandemic, as an unexpected public health emergency, has to some extent propelled the transition of domestic substitution for single-use plastic consumables from rhetoric to reality. Although life sciences research in China started later, the market for single-use plastic consumables is now reaping the rewards after enduring past hardships, thanks to the increasingly favorable industrial environment in the country.

Biotech Downstream Market Benefits from Favorable Policies, Driving Growth in Upstream Consumables.For instance, in May 2022, the National Development and Reform Commission (NDRC) released the "14th Five-Year Plan for Bioeconomy Development," which called for vigorous development of advanced diagnostic technologies and products, including molecular diagnostics, chemiluminescent immunoassays, and point-of-care testing. Against the backdrop of strong national policy support for domestic substitution of imported products, the biotechnology industry is poised to attract greater attention and capital investment, thereby further driving the development of single-use plastic consumables.

Life sciences, as a major focus of global research funding,The life sciences services and product markets continue to grow steadily. According to data from the 2021 Statistical Bulletin on National Science and Technology Expenditure, jointly released by the National Bureau of Statistics, the Ministry of Science and Technology, and the Ministry of Finance, R&D expenditure and intensity in China’s pharmaceutical manufacturing sector reached RMB 94.24 billion and 3.19%, respectively, in 2021—representing year-on-year increases of RMB 15.78 billion and 0.06 percentage points compared with 2020, with growth rates significantly outpacing those of other manufacturing industries. Advances in pharmaceutical R&D and medical device innovation are driving R&D and innovation within China’s pharmaceutical manufacturing sector, which in turn will stimulate upstream market demand for single-use plastic consumables.

Driven by a large population base and rapidly growing demand for life science services.According to Shuohua Life’s prospectus, the market size of biological laboratory consumables in China was RMB 23.126 billion in 2018, accounting for approximately 10% of the global market. Driven by China’s large population base and the continuous increase in research projects in the domestic pharmaceutical and diagnostic fields, demand for laboratory consumables is expected to keep growing, with a projected compound annual growth rate (CAGR) of 20% from 2019 to 2023. The Chinese market is gradually emerging as a new hotspot for life science laboratory consumables.

The demand for domestic substitution of high-end consumables for life science experiments in the Chinese market is growing stronger.After more than a decade of capability accumulation, some leading domestic consumable suppliers in China have reached parity with their international counterparts in terms of production processes and product quality. Although there remains significant room for growth in areas such as production scale and brand influence, the market share of domestic brands is steadily increasing. According to data from Jet Biofil’s prospectus, the localization rate of biological laboratory consumables rose slightly from 4.8% in 2016 to 5.5% in 2018. Furthermore, based on data from New Thinking World (Xinsi Jie) mentioned earlier, the localization rate of disposable plastic consumables for biological laboratories reached 8.5% in 2020. It is believed that as domestic enterprises continue to refine their R&D and production capabilities, and gradually improve their branding and sales channels, the market share of domestic brands will see further enhancement.

IVD Sector Embraces Centralized Procurement, Lab Consumables Stage a ComebackThe Chinese government has vigorously promoted centralized procurement of medical consumables, leading to a 50% price reduction for certain products. Domestic laboratory consumables can stand out by leveraging their “price advantage.” Li Jilong, Strategic Head at Suzhou Yatong Biomedical Technology Co., Ltd., cited an example: the unit price of an imported brand pipette tip ranges from RMB 2 to 3, and a single experiment may require four or five tips, resulting in high overall testing costs. With localization, costs have decreased significantly; the price of a single pipette tip may drop to one-eighth or even one-tenth of the original. Furthermore, as domestic companies continue to innovate technologically and improve fully automated production lines, cost control is becoming increasingly effective while ensuring quality, leading to a consistent downward trend in prices.

In addition, there areThe demand for high-end consumables driven by laboratory automation and digitalization, the short-term essential needs for vaccine R&D and procurement as well as testing and inspection brought about by the normalization of the pandemic, and international logistics constraints caused by the epidemic have made domestic brands a reliable choice for Chinese customers to ensure the normal operation of scientific research and production....the driving force brought by such factors. A product’s lifecycle progresses from formation to rapid growth, and then to maturity. The same holds true for industries. Currently, disposable plastic consumables are in the stage of rapid growth.

The 8.5% domestic production rate reflects over a decade of bittersweet struggles by Chinese companies deeply rooted in the industry, as well as the forceful defense of market dominance by international giants.

First, international giants have established an early and deep presence, boasting strong comprehensive capabilities. Companies such as Thermo Fisher Scientific, Corning, and VWR entered the Chinese market at an early stage. Leveraging their superior product performance and variety, brand influence, sales strength, and distribution networks, they have formed a competitive advantage across the entire industrial chain, spanning from upstream raw material R&D to downstream industrial applications. From the perspective of end-user habits, laboratory consumables are highly interconnected, where a change in one component can impact the entire system, thereby posing additional challenges for domestic substitution.

Secondly, domestic brands still require substantial investment to enhance their overall competitiveness. Chinese manufacturers of biological laboratory consumables started late and still lag significantly in terms of experience, technology, product diversity, and production expertise, remaining in a phase of rapid catch-up.

VCBeat, through its industry insights and interviews with industry professionals, has concluded that the difficulty of domestic substitution lies primarily in technology, sales, branding, and funding.

Raw Materials, Molds, and Processing Techniques Are Key Constraints on Quality Control for Domestic Manufacturers:

Technically, disposable plastic consumables are primarily supported by polymer materials; therefore, the modification and processing technologies of polymer materials are the key technologies in this industry.

Polymer Modification Technologies Enable Disposable Plastic Consumables to Possess Specific Properties for Diverse Application Scenarios. For instance, cell culture vessels such as plates, dishes, and flasks serve as spaces and surfaces for cell growth and proliferation, and must meet the specific surface requirements of various cell types. Certain biological reagents are expensive; therefore, pipette tips and pipettes used for aspirating these reagents require strong hydrophobic properties to minimize liquid residue, ensure accurate volume aspiration, and reduce experimental costs. Additionally, raw materials for centrifugation equipment need exceptional toughness to prevent deformation or rupture under high centrifugal forces.

Geng Xinrui, head of the private-label division at Lab Direct China Limited, stated that disposable plastic consumables have stringent requirements for raw materials. However, due to China’s relatively late start in industrialization, there remains a significant gap between its basic industries and those of developed countries. As a result, high-polymer raw materials used in disposable plastic consumables for biological laboratories and medical devices—such as gamma-resistant polypropylene compounds and filter membranes—are heavily reliant on imports.

In fact, since the second half of 2020, shortages of key raw materials and consumables have become increasingly prominent. The pandemic has disrupted the stability of the global biopharmaceutical supply chain, making scarcity of critical materials and consumables a widespread phenomenon, particularly for items such as virus removal filters, chromatography resins, and single-use consumables.

The processing technology of polymer materials is mainly reflected in the design, operation, and maintenance of processes, equipment, and molds. For instance, while domestic molds have matched imported products in terms of precision, issues remain regarding processing efficiency and service life. The precision of injection molding, extrusion, and blow molding processes determines product quality and production efficiency; however, China still relies on imports for core injection molding equipment.

Meanwhile, consumables manufacturers sometimes need to provide customized services based on customers' production processes, which requires them to continuously upgrade and update relevant equipment and enhance product competitiveness while mastering core key technologies. However, the quality of domestically produced consumables varies significantly, with their stability and reliability still needing careful consideration.

Brand value is also a key area of soft power that domestic enterprises need to strengthen:

Disposable plastic consumables constitute an industry that places significant emphasis on brand equity. Laboratory consumables are widely utilized in high-cost sectors such as molecular biology, where the tolerance for error is low. Consequently, end-users with stringent requirements for manufacturing processes and quality stability tend to prefer products from internationally renowned brands with strong comprehensive capabilities to ensure the smooth progression of their experiments or R&D projects.

Li Jilong, Strategic Head of Yatong Biomedical, stated that imported brands have cultivated the market for many years, and end-users of laboratory consumables in China have formed relatively stable cooperative relationships through long-term use of international brands. As a result, it is difficult for domestic brands to penetrate the supply systems of local end-users. Furthermore, building a brand requires not only substantial corporate investment in technological upgrades and product portfolio enhancement but also long-term accumulation of collaborative experience. Committed to becoming a leading brand of laboratory consumables in China, Yatong Biomedical is leveraging its team’s extensive overseas resources to actively expand its international business and continuously enhance its brand recognition.

Rapid and comprehensive channel services are an indispensable element for domestic enterprises:

“The end-use applications of single-use plastic consumables span diverse customer segments, including universities, research institutions, and pharmaceutical companies. Given the large and fragmented customer base, many manufacturers rely on distributors and agents. Building a robust agency network is also critical, involving aspects such as regional exclusivity and territorial management, which cannot be established overnight,” said Geng Xinrui, Head of Private Label at Lab Direct China Limited.

A well-established sales channel enables companies to promptly identify customer needs, ensure product timeliness, and provide after-sales support, making it a key criterion by which industry players evaluate enterprises. However, building such a channel requires substantial long-term capital investment and back-end support from professional management and operational teams. New entrants to the industry, constrained by limited funding, lack of professional management and operational experience, and insufficient product maturity, find it difficult to establish comprehensive marketing and service channels in the short term.

VCBeat also learned through interviews that the production of single-use plastic consumables involves a great deal of know-how. Manufacturers of laboratory consumables must have a deep understanding and accumulated experience in the application scenarios, workflows, and business needs of life science research and related industries, so as to design and develop products that meet customer requirements and ensure experimental outcomes and detection efficiency. Currently, the shortage of talent with both theoretical knowledge and practical experience is also constraining the development of domestic enterprises.

Furthermore, strong financial backing is required across all stages of the research and development, manufacturing, and sales of single-use plastic consumables. In summary,Technical expertise, brand influence, sales channels, and industry experience are critical factors enabling disposable plastic consumable manufacturers to achieve substantial growth, as well as key elements in building core competitive barriers.

In China’s market for disposable plastic consumables, imported brands hold over 90% of the market share. Wherever there is monopoly, local brands are emerging and growing. Throughout the development of medical devices, import substitution by domestically produced alternatives has been the dominant trend. In this fast-growing segment of disposable plastic consumables, a cohort of innovative enterprises is also beginning to take root.

In addition to the already listed Changhong Technology, Jet Biofil, Titan Technology, and Gongdong Medical, as well as Shuohua Life and Kaishi Biology, which are preparing for their IPOs, a batch of innovative companies is beginning to emerge. It should be noted that the products of the companies compiled below are not limited to disposable plastic consumables.

Data compiled from VCBeat and public sources. For any omissions, please contact VCBeat.

In terms of industrial distribution, manufacturers of laboratory consumables are primarily concentrated in the Yangtze River Delta and Pearl River Delta regions. Most enterprises have small production scales, rudimentary manufacturing processes, and weak independent R&D capabilities, resulting in uneven product quality and low industry concentration.

In its response to the listing inquiry, Jet Biofil disclosed that, “based on publicly available industry information, an analysis and aggregation of manufacturers selling product categories including cell culture consumables, filtration consumables, centrifuge tubes, pipettes, and pipette tips revealed 1,439 companies marketing products similar to those of Jet Biofil. After excluding traders, approximately 318 companies were identified as manufacturers of such comparable products.” Driven by the COVID-19 pandemic and other factors, this number has only increased since then.

As a digital supply chain platform, Lab Direct China Limited offers some insights from a supply chain perspective. Geng Xinrui, head of private label at Lab Direct China Limited, stated that the pandemic spurred the emergence of numerous consumables manufacturers whose primary business was COVID-19 testing. However, as COVID-19 constitutes a sudden public health emergency, the revenue generated from related consumables is incidental. Once the epidemic is effectively controlled, sales of viral testing consumables by these manufacturers will decline significantly. Furthermore, many consumables manufacturers remain heavily focused on the production and sales of low-value consumables, which involve low technological content, lack market competitiveness, suffer from pronounced homogenized competition, and incur substantial internal friction.

Opportunities also exist. The highly fragmented market offers ample room for growth and consolidation among participants. Amid the historical opportunities presented by globalization and the substitution of imported products with domestically produced ones, high-quality Chinese manufacturers of disposable plastic consumables are better positioned to stand out, leveraging their robust technical systems, strong product development and iteration capabilities, and comprehensive sales networks.

Overall, the domestic market for single-use plastic consumables in China is still in its early stages of development. The process of establishing local brands remains lengthy, whether in terms of technical proficiency, product manufacturing processes, brand building, or sales channel development. However, as increasing attention is drawn to this market, the momentum for domestic substitution will intensify.

The road ahead will be no straighter or smoother than the one behind, yet domestic entrepreneurs will press on.

We extend our gratitude to Lab Direct China Limited, Suzhou Yatong Biomedical Technology Co., Ltd., and numerous industry professionals for their support.

Reference link for this article:

Jet Biofil Prospectus

Shuohua Life IPO Prospectus

“Prosperity in the Life Sciences Industry: The ‘Water Sellers’ Upstream May Be the Ones Making Money”